SrdjanPav/E+ via Getty Images

SrdjanPav/E+ via Getty Images

Stride (NYSE:LRN) provides an alternative education source online for students of all ages in the United States as well as internationally. Primarily, the education is provided from kindergarten through to the 12th grade, ranging across school subjects and topics. Stride also provides career learnings programs for adults ranging across multiple industries.

Stride Q2/FY24 Investor Presentation

The stock has had a good run with great and profitable historical growth. In the past decade, the stock has appreciated at a CAGR of 11.1%. As Stride uses cash flows for stock repurchases and complimentary acquisitions to fuel growth, the company doesn’t currently pay out a dividend.

Ten Year Stock Chart (Seeking Alpha)

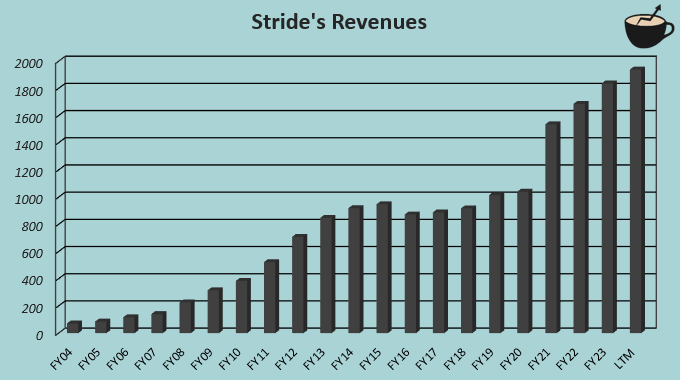

Stride has achieved a very impressive amount of long-term revenue growth at a CAGR of 18.4% from FY2004 to current trailing revenues as of Q2/FY2024.

The company revenues benefited from the Covid pandemic, resulting in a growth of 47.7% in FY2021 among with the small complimentary acquisitions of MedCerts and Tech Elevator among other small M&A. Still, the growth can’t be attributed to the pandemic’s boost and M&A alone as revenues have continued the growth trajectory organically in recent quarters, showing no signs of slowing down.

Author's Calculation Using TIKR Data

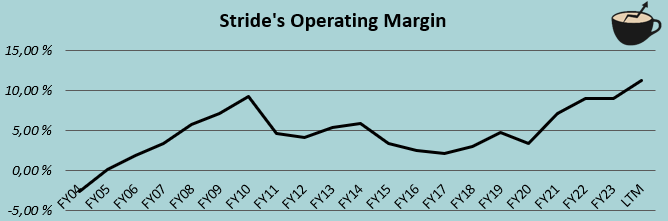

Expenses have mostly scaled alongside revenues on a long-term basis, but the recent growth seems to now be outpacing fixed costs – Stride has been able to drive margin expansion from a low single-digit GAAP operating margin in pre-pandemic years into a current trailing margin of 11.2%. A growing number of customers seems to allow for significant efficiencies of scale, contributing to great bottom line growth. Stride’s current trailing gross margin of 37.2% should also provide further room for margin expansion. Still, investors should mainly focus on topline growth, as the margin trajectory is largely a byproduct of revenues; historically speaking the operating margin and revenue growth seem to have had a large correlation.

Author's Calculation Using TIKR Data

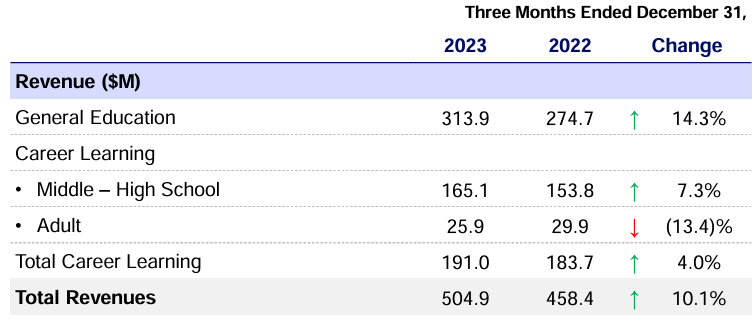

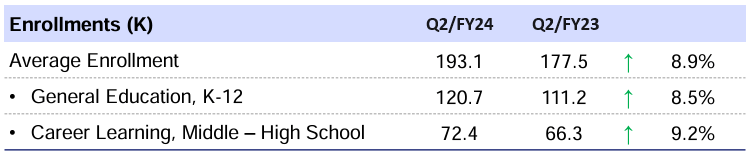

Stride continues to grow. In Q2/FY2024, the company scaled revenues by 10.1% year-over-year. The company has had decreasing enrollment trends in the General Education segment that accounts for the majority of Stride’s revenues, as the Covid pandemic has subsided, making in-person education more attractive. The pandemic’s peak has now been melted, showing Stride’s underlying growth performance; the company has again started to show positive growth in the segment, with a year-over-year increase of 8.5%.

Stride Q2/FY24 Investor Presentation

The current FY2024 guidance of $1.99 billion to $2.04 billion implies a growth of 9.7% with the middle point of the guidance, showing an expected performance in line with Q2. The long-term growth trend is continuing well. Along with the topline growth, Stride is scaling margins well, with a GAAP operating margin increase of 1.8 percentage points year-over-year in Q2.

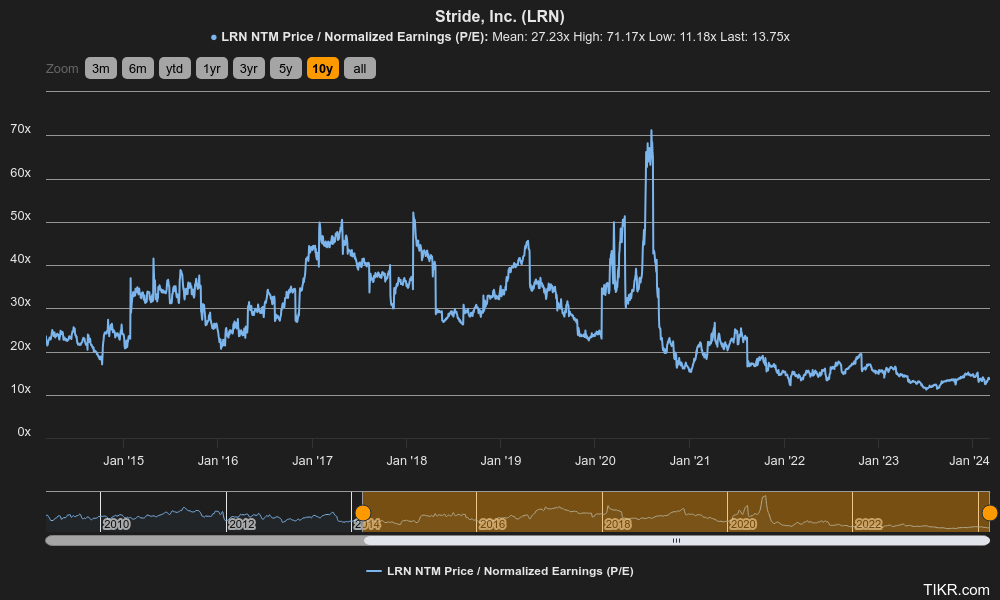

Despite a significant rally in the past year, Stride’s valuation is lower than it has historically been. The current forward P/E multiple stands at 13.8, around half of the stock’s ten-year average of 27.2. With Stride’s now larger scale that makes growing at a similar pace more difficult, and higher overall interest rates, the lower ratio seems partly justified. Still, the gap into the historical P/E seems very wide with 9.7% growth guided for FY2024.

Historical Forward P/E (TIKR)

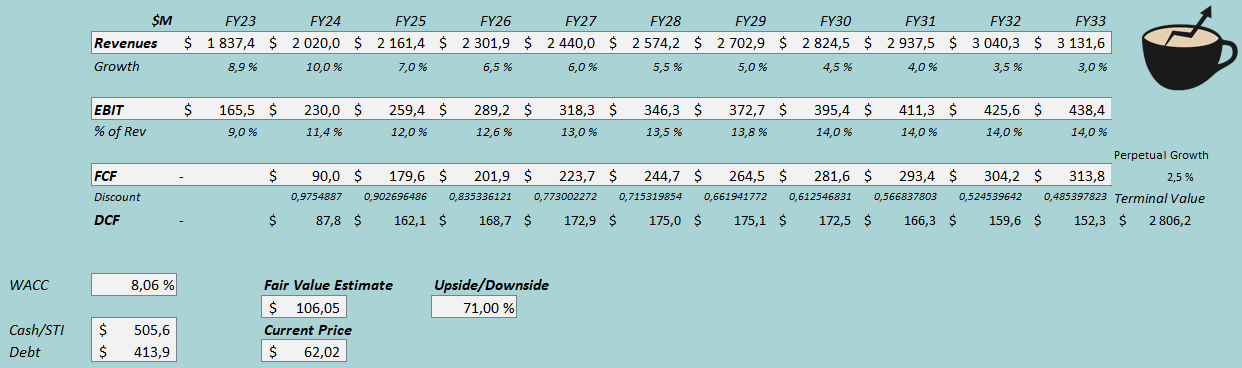

As usual, I constructed a discounted cash flow model to value the stock. In the DCF model, I estimate Stride’s growth to continue at a slowly slowing rate; after a FY2024 revenue growth of 10%, I estimate the growth to slow down into a perpetual growth of 2.5% gradually, representing a CAGR of 5.5% from FY2023 to FY2033. Along with the revenue growth, I believe that further operating leverage is likely, and I estimate the EBIT margin to scale into 14.0% from an estimated 11.4% in FY2024. The company has a great cash flow conversion with modest capital expenditures and quite high D&A from past acquisitions.

With the mentioned estimates along with a cost of capital of 8.06%, the DCF model estimates Stride’s fair value at $106.05, around 71% above the stock price at the time of writing. I believe that a bet on future growth represents quite a good risk-to-reward at the current stock price, as represented by the DCF model.

DCF Model (Author's Calculation)

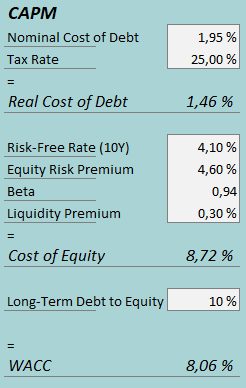

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2/FY2024, Stride had around $2.0 in interest expenses. With the company’s current amount of interest-bearing debt, Stride’s annualized interest rate comes up to an astoundingly low 1.95%. I believe that Stride doesn’t have any rationale to pay off the debt with such an interest rate prematurely, and estimate the long-term debt-to-equity ratio at 10%, slightly lower than the figure currently stands at. While the cost of debt is currently very low, refinancing the debt will inevitably increase the cost of debt in the future.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.10%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates Stride’s beta at a figure of 0.26. While the business is quite resistant to macroeconomic turbulence, I instead use the average of --- peers – Strategic Education’s beta of 0.51, Coursera’s beta of 1.52, and Laureate Education's beta of 0.79 create an average of 0.94, which I use in the model. Finally, I add a small liquidity premium of 0.3%, creating a cost of equity of 8.72% and a WACC of 8.06%.

I believe that the investment case relies very heavily on achieved future growth. Enrollments need to show continued growth, as costs are also scaling to support larger operations. Longer periods of weak growth have come with weak margins historically, making stopped growth deadly for earnings, at least in the short term.

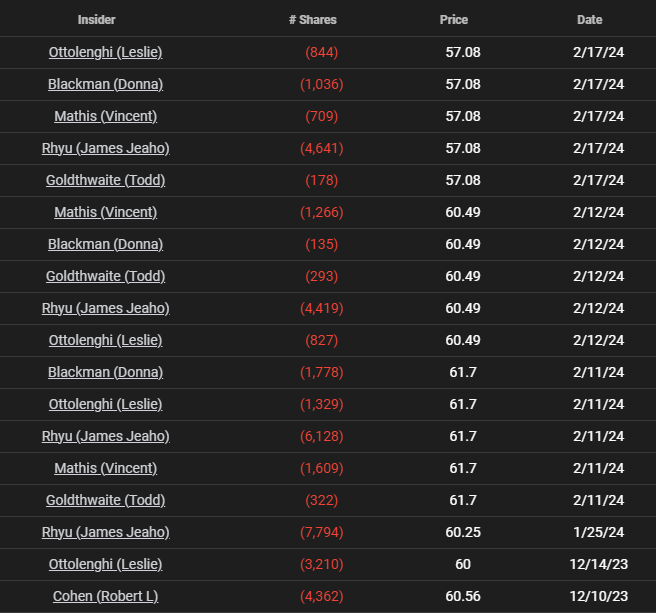

Multiple investors have also sold shares in the company quite recently in late 2023 and early 2024. I don’t see the amount signifying too much fundamentally, but such sales should always be noted critically.

Recent Insider Transactions (TIKR)

Stride has grown revenues impressively in the long term with organic efforts and complimentary acquisitions. After the pandemic boosted Stride’s enrollment figures into an unsustainably high level, the company has now returned into the historical trend of good growth. Along with revenues, Stride has also achieved significant operating leverage in recent years, improving earnings into a great level. Despite a good stock rally, the stock seems to be priced way below my financial assumptions, making the investment case highly attractive if the growth can be continued beyond FY2024. For the time being, I have a buy rating.