MirageC/Moment via Getty Images

MirageC/Moment via Getty Images

MannKind (NASDAQ:MNKD) is down 14% since my "Buy" recommendation in October. This is in spite of favorable advancements. In January, MannKind sold 10% of its Tyvaso DPI, developed in collaboration with United Therapeutics (UTHR), for $150 million upfront (with the potential for an additional $50 million depending on Tyvaso DPI revenue) to Sagard Healthcare. The milestone payment is outlined as follows:

$50 million in the event that the trailing 12-month net sales of Tyvaso DPI equals or exceeds $1.9 billion by December 31, 2026; or if the preceding milestone is not achieved, $45 million in the event that the trailing 12-month net sales of Tyvaso DPI equals or exceeds $2.3 billion by September 30, 2027.

The math is simple here. If 1% of Tyvaso DPI is worth upwards of $200 million, the remaining 9% figures to be close to $1.8 billion. MannKind's enterprise value, according to Seeking Alpha, is $1.18 billion. Obviously, things are that simple. I do believe Tyvaso DPI has a reasonable chance of $1.9 billion in TTM revenue before the end of 2026. United reported total Tyvaso (DPI and nebulized) of $325.8 million in Q3 '23, with Tyvaso DPI making up $205 million of that (up 225% year over year). Patients are switching to the DPI, which provides clear convenience advantages over the Tyvaso nebulizer (e.g., less equipment required and a less complex and time-consuming administration method). Even if we assume a 50/50 chance of United meeting either of Sagard's two requirements for the milestone payment, that values 1% of Tyvaso DPI royalties at $175 million. If we multiply that by nine (MannKind's remaining stake), this implies a remaining value of $1.575 billion.

However, a competitor, Liquidia (LQDA), has made legal progress with its own dry powder formulation, YUTREPIA, which utilizes the same active drug (treprostinil) as Tyvaso. Liquidia's drug figures to enter the market later this year. While it may take some market share away from MannKind and United, I don't think it will be a significant amount, as Liquidia's offering doesn't appear to provide meaningful differentiation to the first-to-market and popular Tyvaso DPI. Moreover, Sagard must have been aware of Liquidia's likely market entrance at the time they struck the deal.

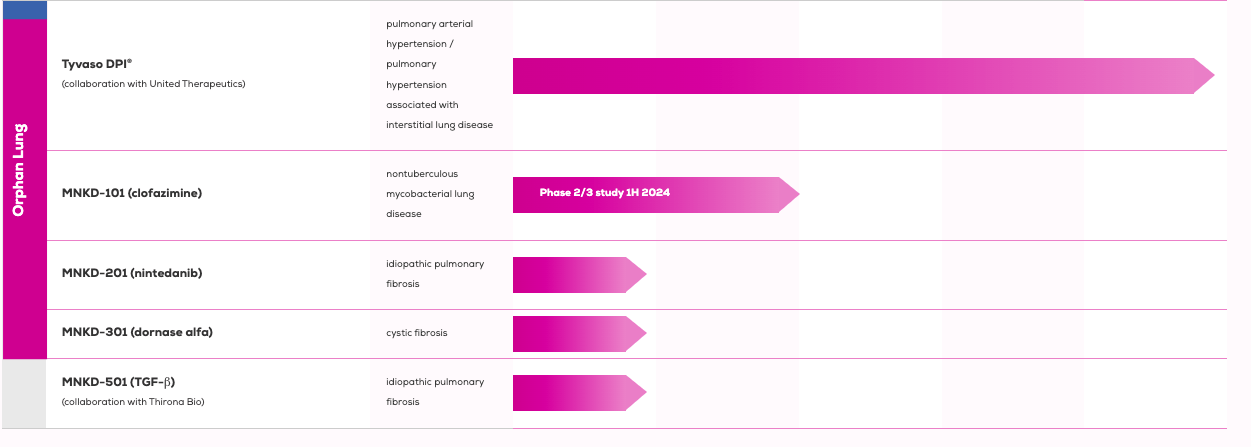

Outside of Tyvaso, MannKind has other ventures, incorporating its proven technology into other applications.

MannKind's pipeline

MannKind's latest earnings reveal a strong Y/Y surge for the quarter ending September 30, 2023. Revenues jumped to $51.253 million from $32.825 million. This leap stemmed from rises in product sales, partnerships, and royalties. A net loss turned into a $1.721 million profit. Despite a slight uptick in expenses, operational income rose. Research and development spending soared, showcasing a commitment to innovation. Yet, share dilution became apparent. The count of shares for earnings per share calculations grew from 259.3 million to 268.7 million, sparking concerns over equity dilution.

Turning to the balance sheet, the company's liquidity improved, with $144.3 million in assets. This includes $83 million in cash and equivalents plus $58 million in short-term investments. With current liabilities at $96.4 million, the current ratio hits 1.50, suggesting sound short-term liquidity. Over nine months, operating activities generated $12.4 million in cash, bolstering resources. Despite historical data, future performances remain uncertain. The recent $150 million Tyvaso DPI deal reduces near-term financing needs. However, a debt-heavy balance sheet, with $572.1 million in liabilities versus $320.3 million in assets, poses long-term risks.

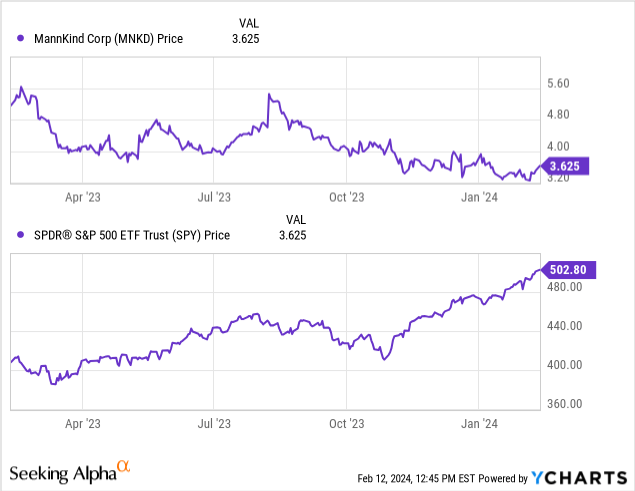

According to Seeking Alpha data, MNKD's market capitalization stands at $946.21 million, indicating a mid-sized biotech entity. Growth prospects appear promising, with analysts projecting revenue growth from $193.64 million in 2023 to $306.82 million by 2025, signifying a substantial upward trajectory. However, the stock's momentum is weak compared to the S&P 500 (SPY), with MNKD showing a decline of -31.45% over the past year against SPY’s increase.

Short interest is notably high at 13.31%, suggesting a significant bearish sentiment or speculative interest in the stock. Institutional ownership is robust at 50.47%, with a notable increase in positions by 29 new institutions, totaling 2,570,492 shares, and 19 institutions exiting, summing up to 1,636,602 shares sold out. Leading institutional holders include Blackrock, Vanguard, and State Street, albeit with mixed changes in their holdings. Insider trades over the past 12 months have displayed positive net activity, with 1,464,598 more shares bought than sold, indicating some insider confidence.

Considering these factors, MNKD's market sentiment can be classified as "adequate," balancing between solid growth prospects and challenging stock momentum.

MannKind's recent strides, notably its 10% stake sale in Tyvaso DPI to Sagard, continue to merit a "buy," despite recent lackluster stock performance. This move, in my view, highlights MannKind's overlooked worth and bolsters its finances, providing a buffer for future risks. The transaction's terms reveal MannKind's assets are undervalued compared to their enterprise value, hinting at a possible stock reevaluation.

Liquidia's market entry barely dims Tyvaso DPI's outlook. MannKind's rich pipeline and tech edge ensure its growth. Liquidia's offering, a slight concern, doesn't eclipse Tyvaso DPI's long-term potential, given MannKind's varied projects.

Investors should heed this advice to curb risk: diversify within biotech to temper MannKind-related volatility. Employ dollar-cost averaging to soften short-term price swings. Keep abreast of pulmonary arterial hypertension market trends, including regulatory moves and new product debuts. Watch MannKind's finances, focusing on debt and operational cash flow, to gauge growth sustainability.

While MannKind's Tyvaso DPI royalty sale signals a "buy," risks loom: