Chip Somodevilla/Getty Images News

Chip Somodevilla/Getty Images News

The Fed's Jerome Powell spoke on Wednesday, releasing the March FOMC summary, which can be found here.

At the press conference that followed, the opening statement of which can be found here, Powell made several points very clear:

I am adjusting my fixed-income holdings accordingly, positioning out further on the yield curve and taking on more duration. In this article, I will discuss the Fed's direction, and guidance, and how we might profit off the tonal shift we saw Wednesday.

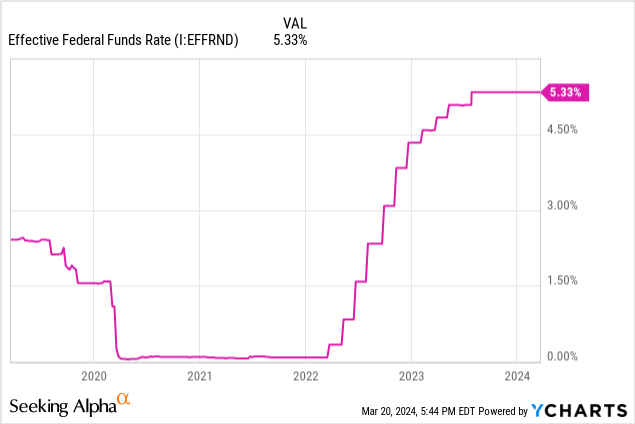

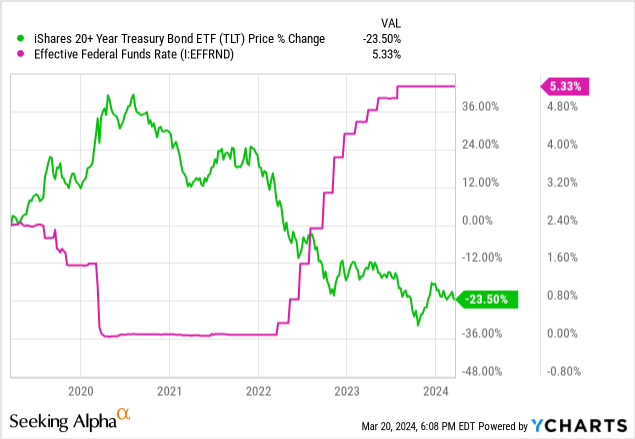

The effective Fed Funds rate has been on a plateau for the better part of a year and it seems that we have been at peak rates since the last hike in July 2023.

That was confirmed by Powell at Wednesday's meeting when he outright said it:

We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year. The economic outlook is uncertain, however, and we remain highly attentive to inflation risks. We are prepared to maintain the current target range for the federal funds rate for longer, if appropriate.

It was a real "have your cake and eat it too" moment when Powell proclaimed both the end of rate hikes and the beginning of rate cuts in the same sentence. This is good news for bond investors who have time to load up on treasuries at the highest they are set to go for this cycle.

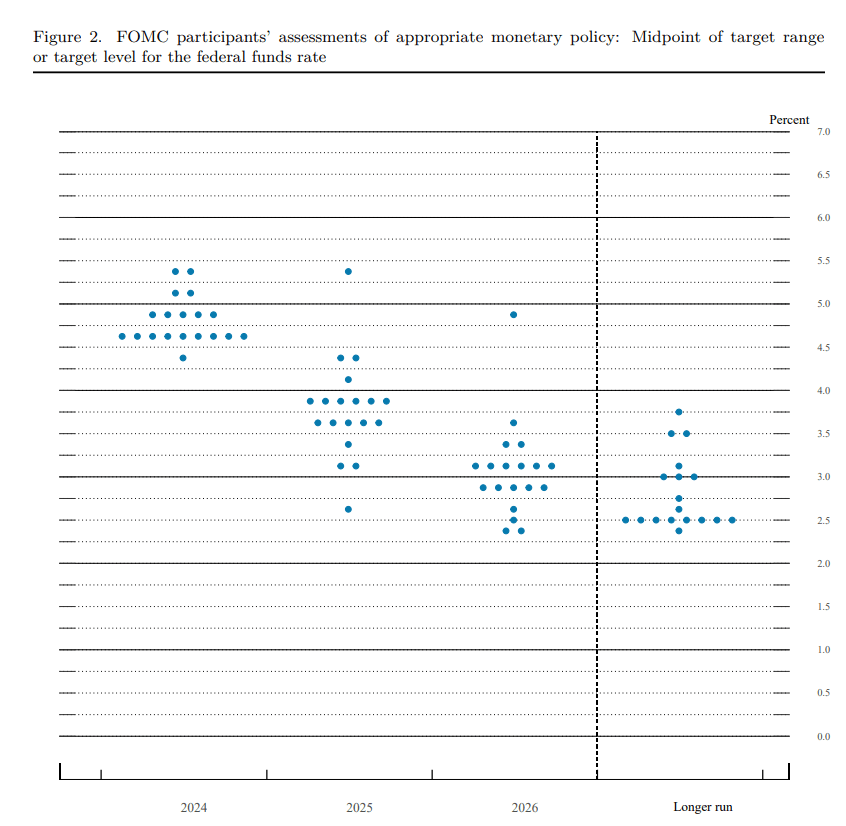

Here is the "dot plot" the FOMC publishes showing their rate projections for the future. Each dot is a member of the committee's projection for that year's target rate.

Figure 1 (FOMC)

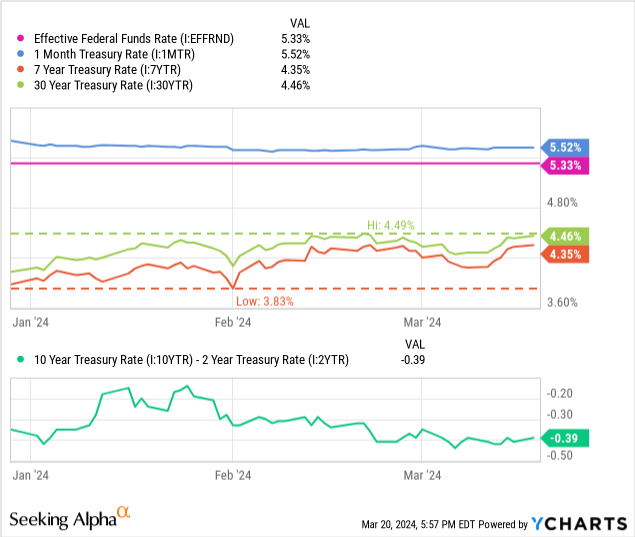

This means that we are likely to see long bonds temper their yields in the coming months, potentially driving prices back up. The chart below shows the YTD changes in yields for the 1mo, 7yr, and 30yr US Treasuries. Note how the rates are still around their YTD peaks.

The spread of the 10yr and 2yr bonds is still negative, meaning that our yield curve is still inverted. It is unlikely to invert any further, since that would require an expectation of even higher short-term rates than 5.52%.

Figure 2 (US Treasury)

This is the greatest buy signal that investors can expect in the US bond market. Powell is telling us that rates will not rise and that he intends to, within this year, take us down at least three notches.

That would take the effective rate down from 5.25 - 5.5% to 4.5% - 4.75%. This kind of cut would push long bonds up quite a bit. With a duration of 16.5 years, funds like the iShares 20+ Year Treasury Bond ETF (TLT) stand to gain almost 20% in value if all goes according to the Fed's plan.

This recovery will be welcome for long-term holders and presents a buying opportunity in the present.

The Fed's primary focus for this cycle has been on inflation, and until now, they have used the phrase "totality of data" to describe the need for more than just good CPI readings to justify lowering rates.

At Wednesday's meeting, Powell's tone changed. Powell seemed far more confident about the Fed's ability to curb inflation, rebutting a question about higher CPI and PCE readings:

I think [the higher CPI and PCE readings] haven't really changed the overall story, which is that of inflation moving down gradually on a sometimes bumpy road toward 2%...We're not going to overreact to these two months of data, nor are we going to ignore them.

To show his confidence, Powell evoked the markets by predicting that the Fed would reach its 2% inflation goal.

The markets believe that we will [get inflation to 2% p.a.]. They should believe that, because we will achieve that goal.

Regardless of what the markets are pricing in, the Fed promises to still base their decisions on data but is making it clear that they would need particularly bad data to steer them from this course.

The other thing is, in the second half of the year, you had some pretty low readings, so it might be harder to make that 12 month window forward...Nonetheless, we're looking for data that confirm the low readings that we had last year...And give us a higher degree of confidence that what we saw was really inflation moving sustainably down to 2%.

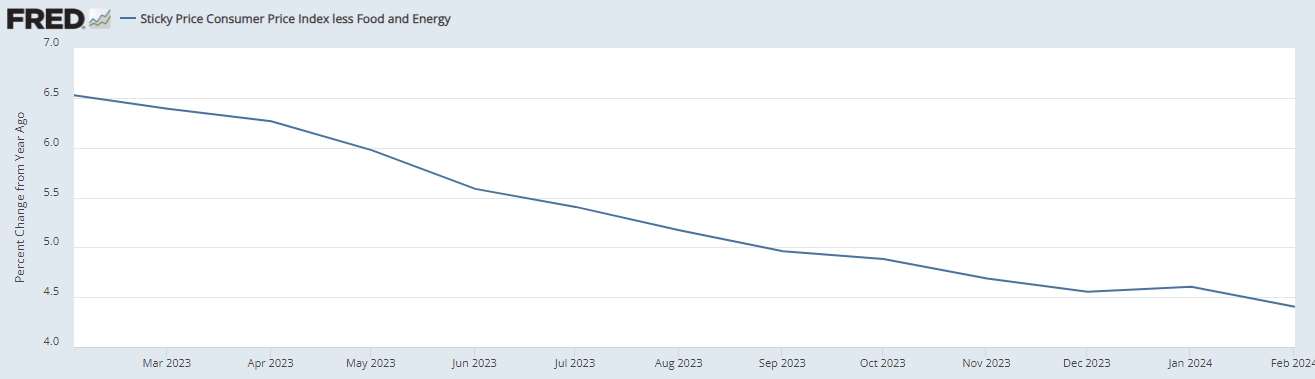

When you look at one of my preferred inflation metrics, "sticky CPI," which is CPI less food and energy, you see a compelling story that lends to their credibility.

Figure 4 (FRED)

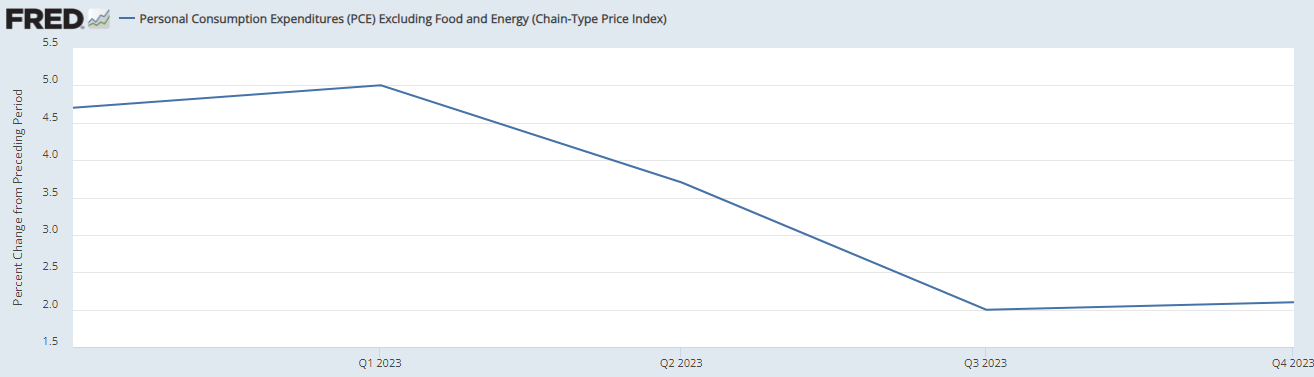

This downtrend is also visible in personal consumption expenditures ("PCE") index. This tells us that consumers are spending less, which is a disinflationary pressure.

Figure 5 (FRED)

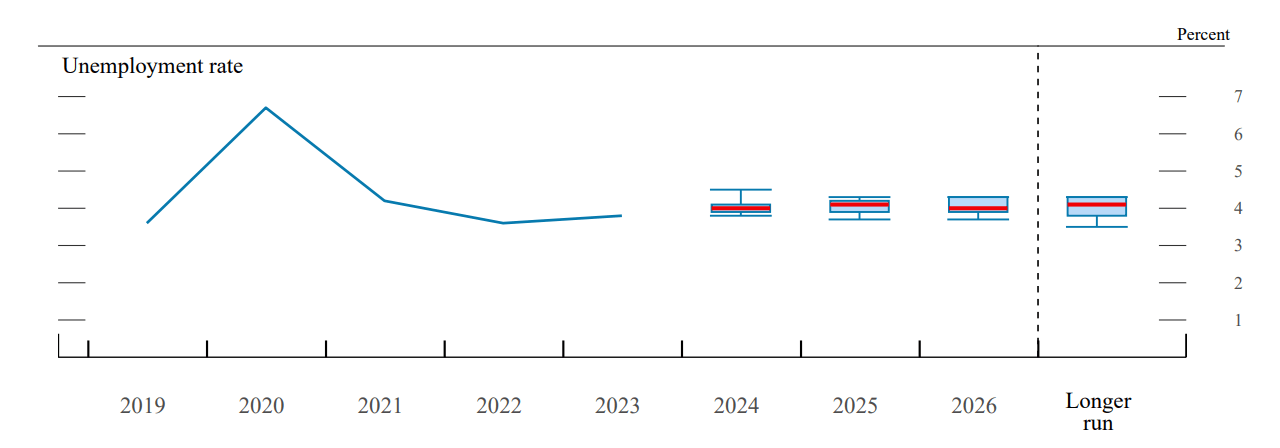

This is the one place where Powell seemed a little more hawkish on, the labor market. He stated outright that bad labor data would hinder his plan to cut rates, but that a weakening in the labor market is unlikely in the Fed's view.

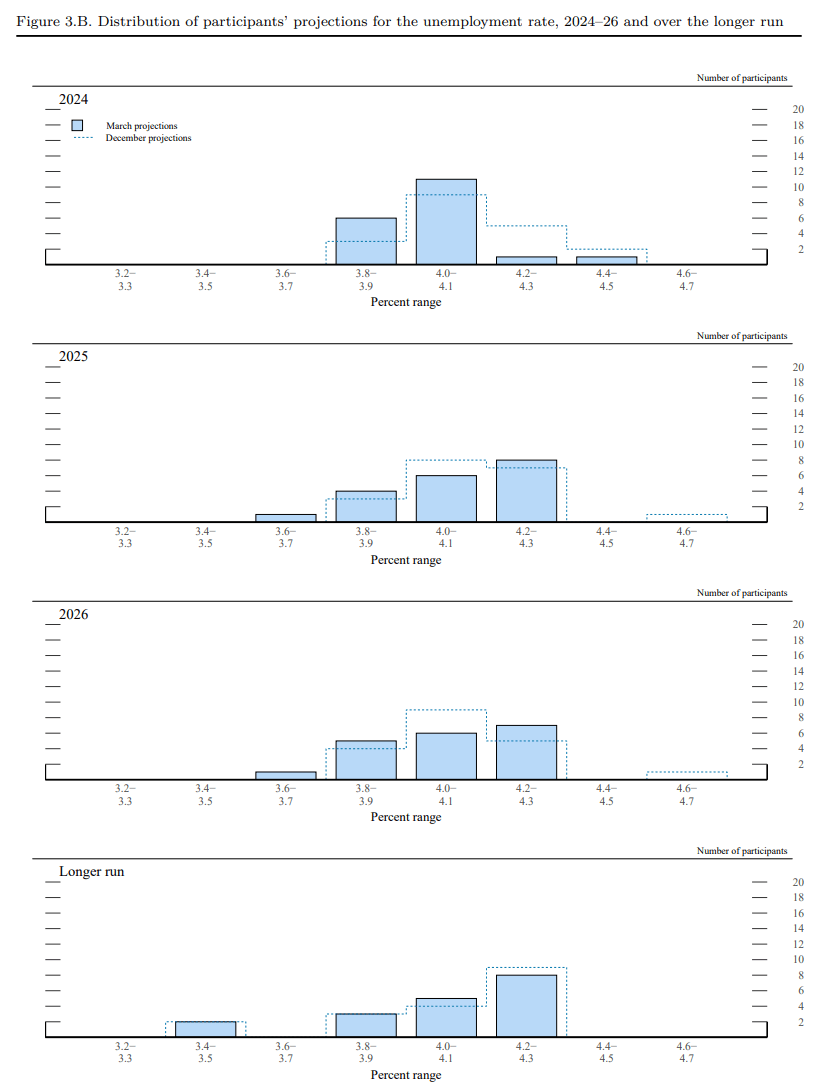

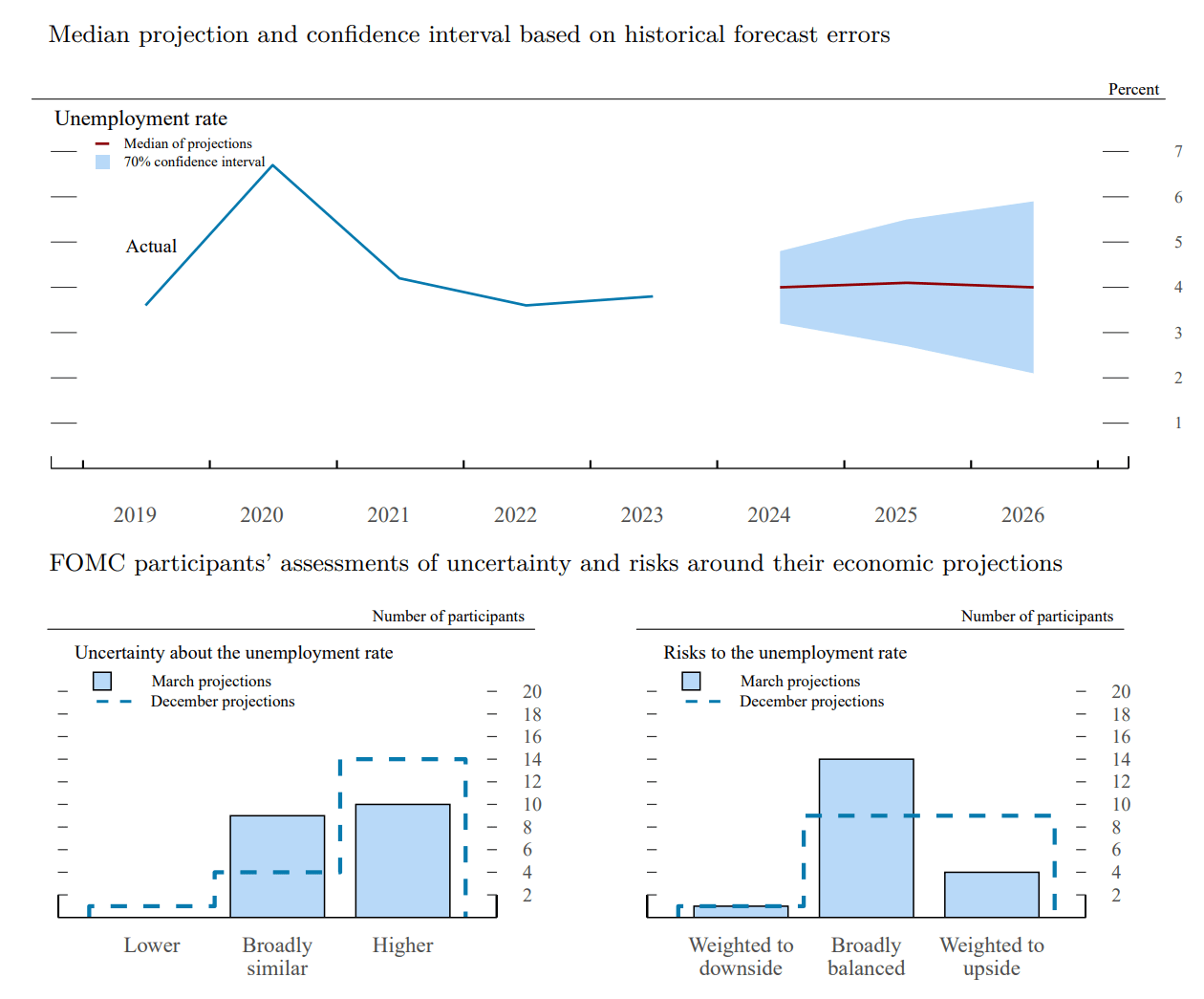

Right now, the Fed projects a 4% unemployment rate moving forward, in line with where we are today.

Figure 6 (FOMC)

This is the "natural rate" of unemployment in the US, more or less, and the Fed projects gradual shifts around the 4% mark for the next few years.

Note in the next chart where the dotted lines are. Those are the projections from December's meeting, and the solid bars are the current, revised projections.

Figure 7 (FOMC)

There is less uncertainty about the labor market within the FOMC, which is a good sign, and has certainly led to Powell's even-more dovish tone.

Figure 8 (FOMC)

The chart above shows how since December, FOMC members have become more certain about the unemployment rate moving forward. This is a good sign, as Powell has said that the labor market is a driving factor in the FOMC's decision making regarding rate guidance.

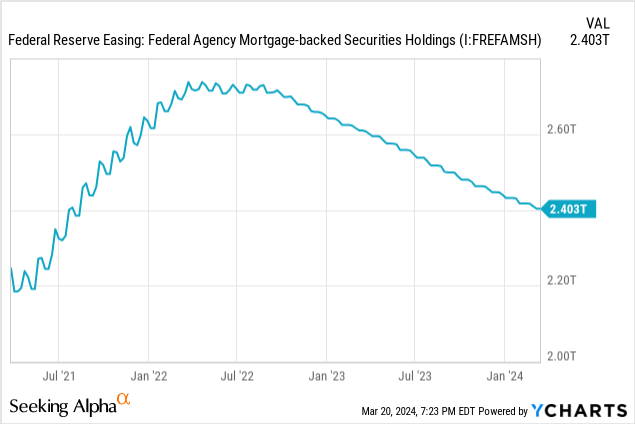

Lastly, we need to talk about the Fed's balance sheet. They hold a lot of agency-backed mortgages and US Treasury bonds that they have been letting run off since their rate-hiking began.

[The] committee will continue reducing its holdings of Treasury securities, agency debt, and agency mortgage-backed securities...

Powell later confirmed that along with rate cuts, the Fed plans to slow this run-off.

The general sense of the committee is that it will be appropriate to slow the pace of run-off fairly soon, consistent with the plans we've previously issued...

This is a potential boon for bonds, as the Fed's run-off has driven down demand for the aforementioned securities. This is best seen in the Fed's ABS holdings.

If this eases and the Fed levels its balance sheet off, we could see a stabilization in the treasury market. This could be a catalyst for a support level. In the past, the Fed has used this balance sheet to inflate bond demand, raising prices and lowering yields. This is a tool that the Fed could deploy again now that they have let the run-off take its course.

There are a few trades I would consider currently, given this new information.

In December's article, I wrote about how I've been holding both investment grade corporate bonds via LQD and intermediate treasuries via IEF. I am still holding those, although I have moved my IEF exposure to TUA and TYA. I still recommend those for the foreseeable future as well, likely until we see the first rate hike.

I expect that to come in June, but it may come sooner or later given large shifts in economic data. Rate cuts in June, August, and November make sense to me, as it will give the Fed time between each announcement to watch the data. Typically, the Fed likes to lag a month between changes in rates.

The Fed has spoken and Powell seemed even more dovish than before. This is a good sign and is very bullish for the bond market. While we can expect rate cuts coming this year, Powell made it very clear that it is dependent on continued good data.

For now, the most important indicators to watch seem to be inflation and unemployment, with the Fed giving CPI and PCE metrics some breathing room and calling a natural 4% unemployment that should persist for the next few years.

To that end, I am recommending investors increase their duration in anticipation of these rate cuts. It is also prudent to begin locking in high-yield fixed rates like CDs, individual treasury bonds, and other timed deposits.

I am still recommending investors consider investment grade corporate bonds and intermediate-term treasuries in the current market and continue to believe in their outperformance over the aggregate bond market.

Thanks for reading.