Miquel Benitez/Getty Images News

Miquel Benitez/Getty Images News

Readers may find my previous coverage via this link. My previous rating was a hold, as I believed Logitech International S.A. (NASDAQ:LOGI) valuation at that time had fully priced in my expectations. I am reiterating my hold rating for LOGI, given its weak second-quarter 2024 results. The company is grappling with challenges such as a decline in revenue growth and varied growth outcomes across different regions. Additionally, the aftermath of the pandemic pull-forward demand is currently weighing on its sales and is expected to have an impact on its FY24 revenue. While it's commendable that LOGI is recognizing the growing AI market and actively positioning itself, this venture is still in its infant stage. The future success of this initiative remains uncertain, making it difficult to project its long-term impact on the company's performance.

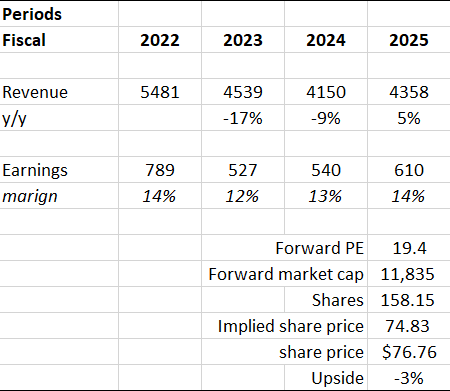

Based on my view of the business, I forecast a 9% decrease in LOGI's revenue for FY24, with a subsequent 5% growth in FY25. My forecast for FY24 derives from the upper limit of the management's guidance shared during their earnings call. The anticipated 5% growth in FY25 is attributed to the recovery of the pandemic pull-forward demand impact. However, as LOGI transitions into FY25 and beyond, I expect this surge to diminish. The prevailing high inflation and the ongoing recovery from the semiconductor shortage don't incentivize consumers to purchase LOGI's products at the moment, preventing a cascading impact in the future. Moreover, LOGI has identified the rapidly expanding AI market and is proactively positioning itself to capitalize on this growth. However, as LOGI is still in its infancy stage for AI, I expect this benefit to only come in FY25 onwards.

Based on author's own math

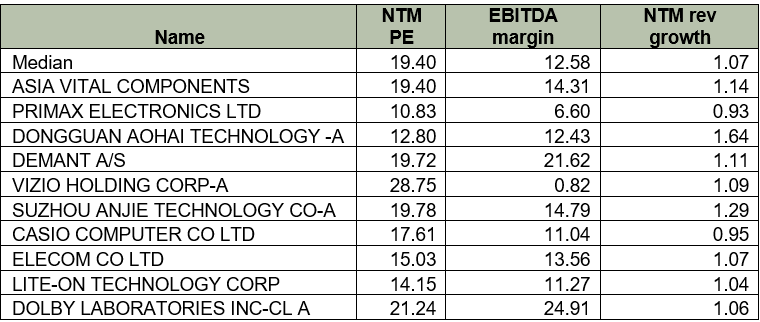

Peers overview:

Factset

Currently, LOGI is trading at a forward P/E of 23.55x, which, in my assessment, is considerably high compared to the median of its peers at 19.40x. My rationale for this viewpoint is twofold. First, LOGI's EBITDA margin of 12.58% aligns closely with that of its peers. Second, the expected revenue growth for LOGI over the next twelve months is -1%, which contrasts sharply with the positive 7% anticipated for its peers. Given these factors, I believe that LOGI should be trading closer to the median forward P/E of its peers, which stands at 19.40x. Based on this multiple, my target price for LOGI is $74.83, aligning closely with its current trading price. Given these, I maintain my hold rating for LOGI.

LOGI reported weak second-quarter 2024 results. The company reported a decline in its net sales, with a 9% decrease, settling at $1.06 billion. This contraction might hint at potential challenges in revenue streams or market-specific issues that the company faced during the quarter. However, not all regions echoed this decline. Europe, for instance, emerged as a beacon of growth. The European market showcased both sequential and year-over-year growth when measured in US dollars, indicating its robustness and significant contribution to LOGI's revenue. On the other hand, the Americas and Asia Pacific regions painted a more complex picture. While both regions demonstrated sequential growth, suggesting a potential rebound or improvement from the previous quarter, they lagged when the year-over-year comparison was drawn. This mixed performance could be attributed to market saturation, external challenges, or other region-specific factors.

Furthermore, the company's mention of "working through pandemic pull-forward demand" provides another layer to the challenging narrative. The term "pull-forward demand" typically refers to a situation where consumers make purchases earlier than they would have due to external factors, in this case, the pandemic. This can lead to a surge in sales during the period of pull-forward but can be followed by a lull, as future demand has effectively been "borrowed." For LOGI, this means that while they might have seen a spike in sales during the height of the pandemic due to increased remote work and gaming, the subsequent periods could witness a slowdown as that demand has already been catered to.

Yet, amidst these regional variances, LOGI managed to outshine its own sales expectations. This overperformance in sales not only boosted the topline but also signaled the company's strong product offerings or perhaps its adept sales strategies. Another feather in LOGI's cap was its proficiency in channel inventory management. The company's ability to reduce channel inventory underscores its operational efficiency, hinting at effective demand forecasting and a keen understanding of market dynamics.

Additionally, LOGI showcased its adaptability by aligning its product portfolio with evolving global trends. The company placed a strong emphasis on solutions tailored for the hybrid work environment, ensuring that businesses and employees are equipped for both remote and in-office settings. Additionally, they fortified their position in the video conferencing domain, understanding its growing indispensability in modern communication.

On the leisure front, LOGI tapped into the booming gaming industry, offering advanced peripherals that cater to both casual and professional gamers. Parallelly, they recognized the surge in content creation, driven by platforms like YouTube and TikTok, and introduced tools to empower creators to produce high-quality content.

Beyond immediate product innovations, LOGI displayed foresight by embracing the transformative potential of artificial intelligence. The company envisions a future where it plays a central role in bridging the interface between humans and AI technologies, positioning itself not just as a tech accessory provider but as a key player in the broader technological evolution. In 2022, the worldwide market for generative AI stood at $10.5 billion. It's anticipated to surge to $191.8 billion by 2032, with an annual growth rate of 34.1% spanning from 2023 to 2032. Thus, this represents a big addressable market for LOGI to tap into, bolstering its long-term growth outlook.

A potential upside risk to my hold rating for LOGI is inflation recovery, which could boost retail spending and expedite the end of the pull-forward demand's impact. In such a scenario, the management's FY23 guidance might appear overly conservative. If LOGI surpasses these expectations, it could drive the company's share price upward.

LOGI's recent quarterly results revealed a decline in net sales, with varied outcomes across different regions. Europe stood out with positive growth, while the Americas and Asia Pacific showed inconsistencies. The company's mention of "pandemic pull-forward demand" hints at potential sales challenges in upcoming periods. However, LOGI's ability to surpass its sales expectations and its efficient inventory management are commendable. Strategically, LOGI is aligning with global trends, emphasizing hybrid work solutions, gaming, and content creation. Their focus on the growing AI market suggests a vision for long-term growth. However, when considering its current valuation in comparison to its peers, I believe LOGI's forwards are too high and should trend down towards the peer's median. Given these factors, I am maintaining my hold rating for LOGI.