John Morrison/iStock via Getty Images

John Morrison/iStock via Getty Images

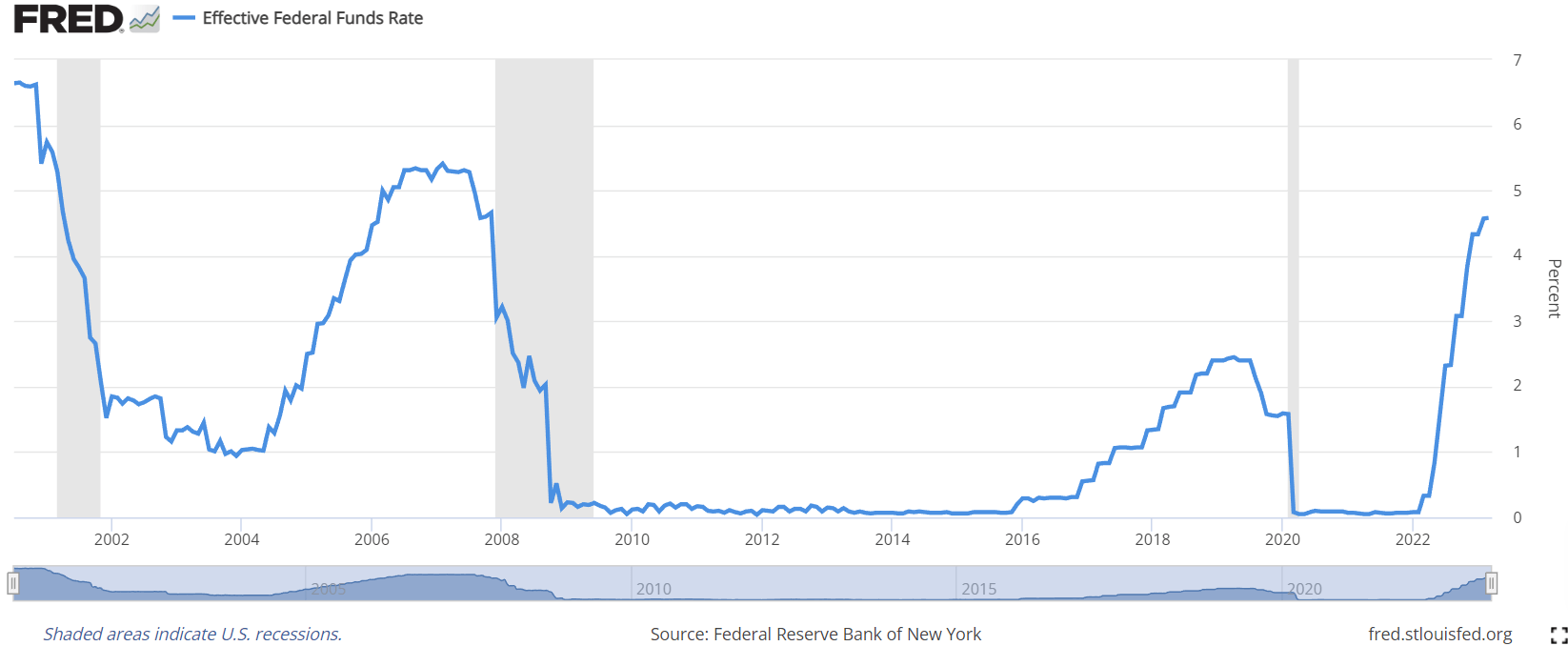

Mortgage Real Estate Investment Trusts (mREITs) focus on real estate financing and often profit on net interest margin, the spread between interest income generated by mREITs' mortgage assets and their funding costs. For mREITs, rising interest rates can become the Big Bad Wolf that blows their house down. The following plot reflects the Federal Reserve's most recent 0.25% hike.

Effective Federal Funds Rate

Federal Reserve Bank of New York

Over the last year, the Effective Federal Funds Rate has increased from 0.08% to 4.58% or 5,725%. mREITs' revenues can be reduced when rising interest rates reduce their net interest margins or increase their capital costs. Rising interest rates can also drive down the value of mREIT's mortgage assets and, ultimately, share price.

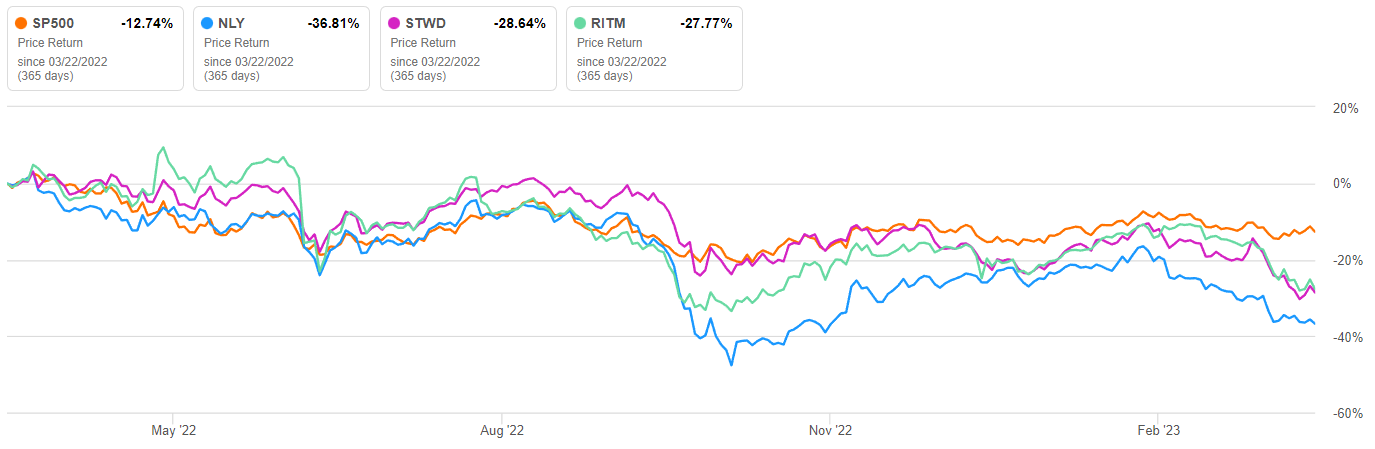

mREITs: 1YR Price Return

Seeking Alpha

1YR price return is plotted for three largest (by Market Cap) mREITs: Annaly Capital Management, Inc (NLY); Starwood Property Trust, Inc (STWD), and Rithm Capital Corp. (RITM). Over the time period, all three underperformed SP500. NLY, STWD, and RITM declined 36.8%, 28.6%, and 27.8% respectively.

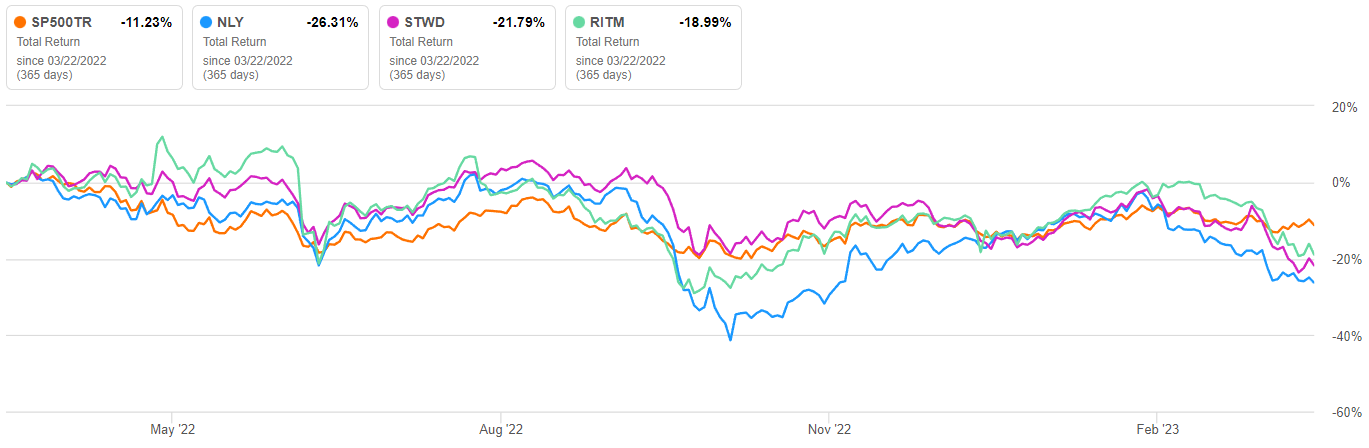

mREITs: 1YR Total Return

Seeking Alpha

1YR total return is plotted for the same three mREITs: Even while accounting for dividends over the last year, NLY, STWD, and RITM returned -26.3%, -21.8%, and -19.0% respectively.

Based on 1YR performance of the three largest mREITs and rising interest rates, clearly the Big Bad Wolf is lurking. A prudent investor will want to know which little pig is living in a straw house.

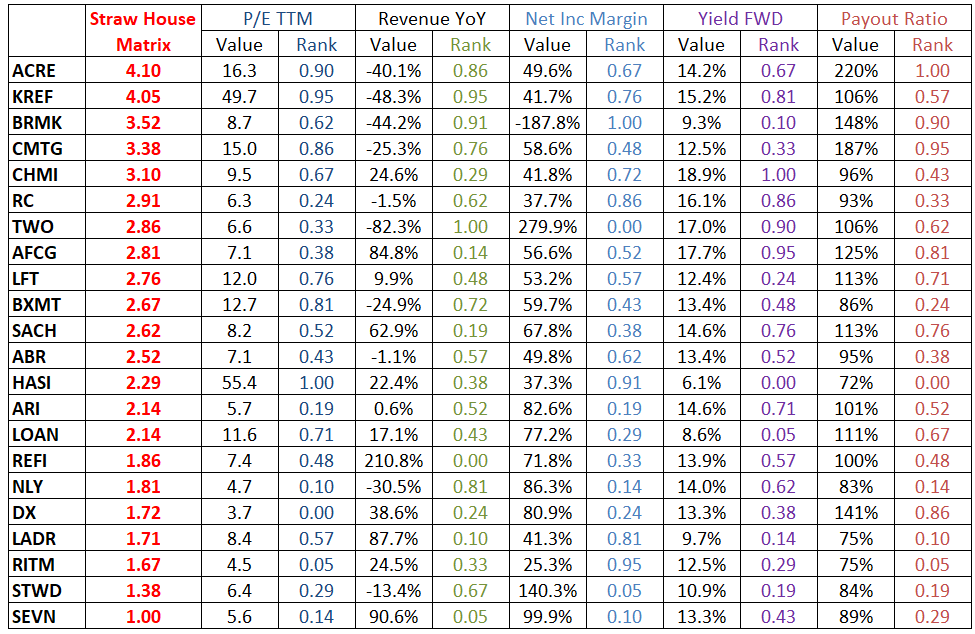

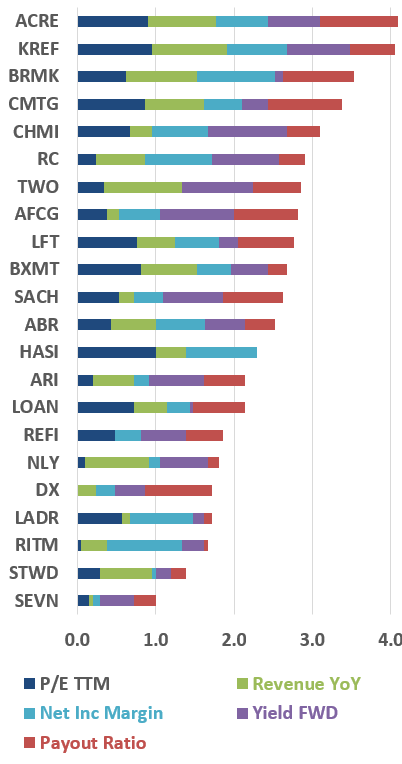

22 mREITs were evaluated using a straw house matrix with factors including Price/Earnings, YoY Revenue Growth, Net Income Margin, Forward Yield, and Payout Ratio. The values for each factor were normalized by means of statistical percent ranking with relation to the group. The straw house matrix was calculated as the sum of the percent ranks of the factors.

mREIT Straw House Matrix

Author, SA Data

The above chart is sorted in descending order of the highest straw house score (highest risk) to the lowest straw house score (lowest risk).

mREIT Straw House Matrix Plot

Author, SA Data

The straw house matrix is presented graphically in the stacked bar chart to the left, with cumulative inputs for each factor.

Based on this analysis: Ares Commercial Real Estate Corporation (ACRE), KKR Real Estate Finance Trust Inc. (KREF), Broadmark Reality Capital Inc. (BRMK), Claros Mortgage Trust (CMTG), and Cherry Hill Mortgage Investment Corporation (CHMI) appear to be living in straw houses. These mREITs are likely most at risk of further price declines.

Please note, stocks with higher forward yields can be great investments. However, in this analysis, those stocks with higher yield received a higher risk score for that factor. High yield stocks are risky when dividends are not supported by revenue. If the payout ratio is consistently high over time, the dividend is unsupported by earnings and is at high risk of a cut with a resulting price decline. I warned investors of exactly that situation in a previous analysis entitled Newtek Business Services: A Risky High Dividend. I'm proud to say that I was right while warning readers 4 months in advance of NEWT's steep price decline.

Investors should consider the straw house matrix a screen only. The matrix factors, normalization method, and weights could all be adjusted and yield different results. Further, the matrix is based on the most readily available and common metrics. These metrics can change rapidly with share price or as new company reports are released. It does not include company-specific data available in quarterly reports and presentations. Every investment decision regarding an individual equity should be based on comprehensive analysis of that equity.

Several Seeking Alpha authors cover mREITs including Brad Thomas. He recently wrote an analysis entitled Stop Chasing 'Sucker Yield' Syndrome wherein he discusses several mREITs and their unique difficulties.

For some mREITs, rising interest rates can decrease revenue, erode profit margin, and leave high dividends unsupported by earnings. The 1yr price returns and even total returns of the largest mREITs are dismal. Interest rates may remain elevated for longer than expected and continue to climb.

I would advise investors who hold any mREIT and especially ACRE, KREF, BRMK, CMTG, or CHMI to carefully review their positions.

Investors who are interested in safer high yield investments may find my recent articles, Wireless Services: Defensive Outperformance and U.S. Oil Refining Stocks Ranked By Quality helpful.

Only the mountain has lived long enough to listen objectively to the howl of the wolf - Aldo Leopold

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.