JHVEPhoto/iStock Editorial via Getty Images

JHVEPhoto/iStock Editorial via Getty Images

While they have recovered from lows, Lincoln National (NYSE:LNC) shares have been a significant laggard over the past year, losing about 12% in what has been a strong bull market. With shares down by nearly half over the past decade, LNC has been a perennial disappointment, even with large share repurchases (largely executed at higher prices). I last wrote about Lincoln in September, when I rated shares a sell. Since that recommendation, shares have returned 9%, underperforming the S&P 500’s 15+% rally, a level of underperformance I view as consistent with the recommendation. Still, with shares offering a ~7% yield, LNC could be a temping “value” stock, making now an opportune time to review the company. I continue to reach a negative conclusion and offer a Sell rating in this article.

Seeking Alpha

Lincoln reported its Q4 financial results on February 8th, beating estimates by $0.12, with adjusted EPS of $1.45. Adjusted EPS excludes the impact of unrealized gains and losses on its large securities portfolio. Given these bonds are largely held to maturity and hedge insurance liabilities, these movements have minimal economic impact, and so it is best to exclude them to understand how Lincoln’s underlying business is doing. Overall, the answer is mixed, with some units performing better than others.

On the positive side in Q4, annuities sales hit a record, as fixed annuity sales surpassed $2 billion for the first time. Total sales were $4.4 billion, up 36% from last year. Income from operations rose by 1.5% to $279 million in Q4. Thanks to strong sales, net flows were a positive $278 million, and account values are up 3.7% from last year to $147.4 billion. Its core indexed-annuity offering is up to 18% of balances from 14% a year ago. This unit is performing solidly, and the business mix shift continues to be favorable.

In the middle of the pack, its group protection unit saw profits double to $52 million, though operating margins remain quite narrow at 4.1%. Its loss ratio fell from 76.6% to 81.1%. There is some improvement in disability. Sales rose by 12% to $398 million. This unit is profitable, and margins are improving, both of which are good. On the other hand, on an absolute basis, margins remain low and translating its lowered loss ratio into higher profits by reducing expenses remains a key objective.

On the negative side, its life insurance unit continues to be the weak point. Its life unit lost $14 million before taxes ($6 million after taxes) on $1.7 billion in revenue. Average balances are down 5% to $45.6 billion and sales fell by 22% to $144 million, as LNC continues to de-emphasize this unit. Life liabilities are obviously very long-dated, stretching often for decades. As such, even if it ceases writing new policies, this unit will be substantial for a long time, and any underwriting errors can have an impact years later.

For the full year, life generated just $37 million in operating profits, or about 3.5% of the total company’s earnings. With nearly $50 billion in assets, that is a less than 0.1% return on assets. This is simply a very capital inefficient business that generates essentially no free cash flow. LNC has had to increase reserves as underwriting assumptions proved too favorable in recent years, and it continues to expect ongoing reserve builds, albeit at a declining pace. Having a unit this large that consistently underperforms and cannot quickly be turned around given the nature of the liabilities has been a major reason shares have underperformed.

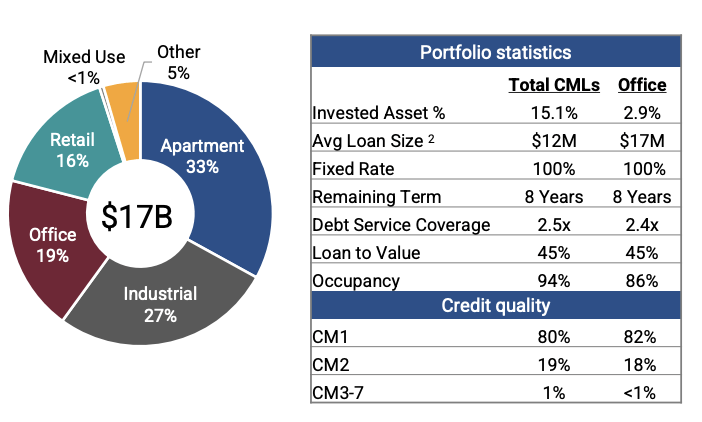

I would also note that Lincoln carries $113 billion investment portfolio, of which 97% is investment grade. This is a largely conservative portfolio. It does carry $17 billion of commercial real estate exposure, which bears watching. However, office, the most challenged sector, is only about 3% of total assets. Loans also have a conservative 45% loan to value, and less than 2% of commercial mortgages matures over the next two years. As such, I expect minimal credit losses but would continue to monitor the exposure closely.

Lincoln

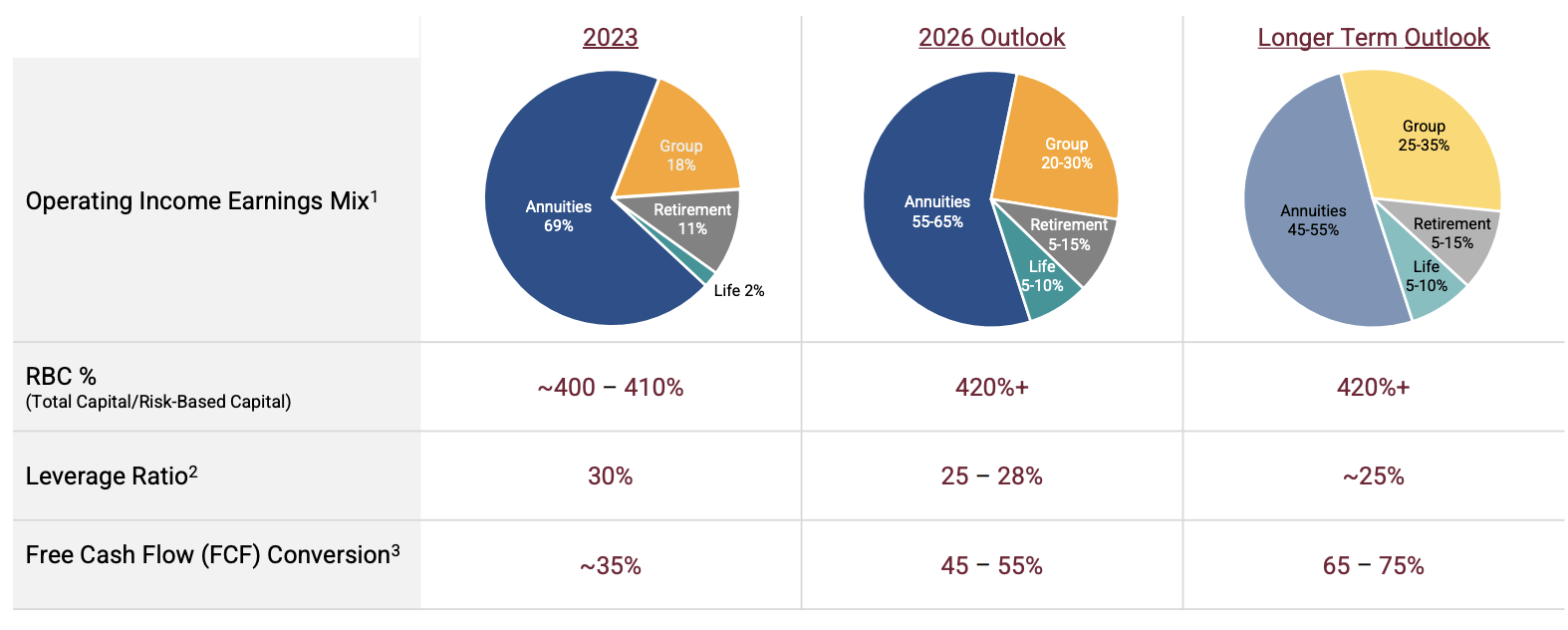

Lincoln has been plagued by two problems: low capital as its financial results have underwhelmed in recent years and poor free cash flow generation as low capital has forced LNC to retain more cash inside of its insurance entities. Its capital position was exacerbated by large share repurchases, at higher prices. LNC has made material progress on capital, and its outlook calls for some improvement in free cash flow generation.

Because the primary challenge for the company has been weak capital, management entered into a reinsurance contract last year. Essentially, by ceding some of its annuity insurance risk to another firm, it is trading lower earnings for higher capital, as the reinsurer receives a share of premiums. The reinsurance contract reduced assets by $28 billion. It reduced Q4 earnings by $15 million; this impact will rise to $25 million in Q1 as there is a full quarter impact vs less than 2 months in Q4. As a result, its risk-based capital ratio is back above 400% from ~380% in Q3.

400% is a critical mark for a life insurance company that can essentially be viewed as having capital adequacy. Below 400%, insurers need to find ways to build capital, either by retaining earnings, raising equity, or like LNC did, by reinsuring risk. As capital moves past 400%, there is a more comfortable buffer of excess capital, which can be returned to shareholders. LNC is now at the “adequacy point,” a meaningful step in the right direction.

Going forward, management’s three year plan to improve free cash flow consistency will “require” LNC to “hold more capital than we have previously.” Essentially, the company aims to get RBC to 420%, so that even in downturns, it holds above the 400% level. That will enable the firm to be able to more sustainably return capital to shareholders during downturns, rather than be compelled to do a reinsurance contract or issue expensive preferred stock as it did during this past downcycle in capital. Alongside this, LNC will reduce financial leverage over time by paying down debt. Lincoln carries $5.95 billion of debt and $986 million of preferred stock.

Lincoln

This transition makes sense. Holding more capital and also holding less debt can reduce returns on equity. However, by having a cushion, capital returns can be less volatile overtime. Combined with the movement away from variable annuities to fixed annuities and group insurance, LNC should be a steadier company going forward. LNC shareholders have not benefitted from its more aggressive financial policies, as evidenced by years of underperformance, and so I believe this shift is prudent.

On the positive side, the capital shift should happen quickly. As noted above, capital has been brought above 400%. Further, Lincoln is selling its wealth management business to Osaic for $700 million, which will bring capital near 420%. This deal should close in H1. Wealth management is a capital un-intensive business with recurring revenue, which can make it attractive, but absent this sale, reaching capital targets could take another 9-12 months. Additionally, proceeds may be used to reduce debt and accelerate its deleveraging.

LNC has acted aggressively and quickly to resolve it capital issue. Now, given the long-dated nature of its liabilities, improving operating performance will take longer. Insurance companies earn money in their operating entities, and some of those earnings can be dividended to the parent holding company, which in turn is the entity that buys stocks and pays shareholder dividends. LNC has been plagued by poor free cash flow conversion. In 2023, it generated about $1.06 billion in operating earnings and generated $370 million in free cash flow, including $61 million of excess capital retained by the life insurance subsidiary. That is a poor ~35% conversion rate that essentially just covers its $300 million dividend. The holding company has also $458 million of cash to provide liquidity.

It aims to bring free cash flow to 45-55% of earnings in 2026 from 35%. This is still a relatively low conversion rate; for instance, Prudential (PRU) aims for about 65%. As such, while Lincoln generates substantial non-GAAP earnings, only a portion of this can be used to benefit shareholders with most remaining trapped in the insurance entity or paying interest and dividends to bond and preferred stockholders. The problem is that the life unit is forecasted to generate no free cash flow through 2026 as it expects ongoing reserve builds, albeit at a slowing pace. This unit contributed just $37 million in operating income last year. Other units will drive about 70% free cash flow conversion on average, a solid level with limited scope for further improvement.

LNC is saddled with a nearly-$50 billion entity that is providing no financial contribution, significantly weighing down the capital efficiency of the company. Because policies are locked in for so long, it will take years to materially diversify away from it. Additionally, having seen reserve builds in recent years, there is an ongoing perceived risk that life could incur further losses and drain capital from other units. Just given its size, even small underwriting misses can contribute meaningful losses.

Now in 2024, LNC targets ~$1.15 billion of operating income targeted in 2024 from $1.06 billion in 2023. That leaves shares just about 4x operating earnings. However, free cash flow is unlikely to be much above $400 million, which shares trade 11.3x, for a free cash flow yield of about 8.9%. Given its $300 million dividend payment and deleveraging goal, this is why management has no “specific timing” to the resumption of buybacks.

Now, if the company hits its goals, in three years, it could be a $600 million free cash flow business, at which point it could resume some buybacks, but late 2026 is likely the soonest a buyback would resume. For 2024 and 2025 and possibly 2026, the current dividend is likely the entire capital return.

Currently, I rate Prudential a hold, with its 7% capital return yield, based on its free cash flow generation. If Lincoln hits targets in 2024, its free cash flow yield is 8.5-9%. In my view, LNC should trade at a discounted valuation to PRU, given its history of poor performance, question marks on the long-term value of its life business, need to deleverage, and low cash flow generation.

LNC’s dividend is likely secure, which provides a 6.8% yield, but investors will likely need to wait 3 years to see a dividend increase or buyback, and that assumes LNC can meet its objectives. I expect markets to be hesitant to price in much improvement until it is visible in results, given LNC’s operating history. As such, shares are likely to languish, and investors will need a very long timeframe and confidence in management to see much return. I would expect shares to languish in the mid-$20’s and view this as a value trap, rather than opportunity, and would continue to avoid LNC.

Now, given where shares are and with the dividend on offer, I can see investors tempted to hold the stock. Management has done a solid job raising capital, and so the situation is certainly less dire than it was six months ago. The stated strategy of holding more capital structurally is also sound, even as that means recent capital-raising actions will not boost shareholder returns in the near-term. Additionally, if the company were able to engage in a transaction where it reinsures substantial portions of its life insurance risk without significantly impairing free cash flow, I expect shares would react positively as that overhang is lifted. This is likely the biggest potential near-term catalyst for the stock, though no transaction appears imminent or likely.

In no way do I believe LNC is an institution likely to fail--it is financially sound. Rather, I struggle to see the upside case. For investors who seek income, I would simply rather own the preferred shares (LNC.PR.D), which yield 8.2%, 140bp more than the common stock, and they are further up in the capital structure. Given I expect LNC to see minimal cash flow from life and that it will need to use its slowly building excess free cash to deleverage, investors will need to wait ~3 years before LNC boosts its dividends or repurchases stock, assuming all goes right. With that long of a horizon, I would rather own the preferred, collect the higher income stream over the next three years, and be higher up in the capital structure.

At a ~6.8% yield, LNC has a similar capital return yield to a firm like Prudential (including its dividend and buybacks). At that capital return yield, I would simply rather own PRU, which is performing better across all metrics and likely to be raising its divided in coming years. With three years of no growth and an uncertain turnaround, I believe investors should want an 8+% dividend yield to be that patient with LNC when there are so many other investments to choose from. That would argue a fair value of $22.50.

At that level, investors are being more fully paid to wait the three years it will take for LNC to increase shareholder returns. This is why I view shares as a "dead money" or "value trap" stock where the yield can entice but is not sufficient to push shares. I suspect in twelve months, you will be able to buy LNC at a similar or lower price than today. For investors focused on current income, LNC's preferreds are a better opportunity, while other insurers with more growth prospects like Chubb (CB), Arch (ACGL), or even Prudential likely offer more upside. That is why, while I see an argument for a "hold, given the lack of negative near-term catalysts, I believe investors would be better to sell LNC and invest their capital elsewhere, whether they seek income or growth.

If we see an action that further raises capital, or if we begin to see reserve builds in life insurance cease, that could bring forward the timeline for LNC to increase capital returns. I believe focusing on risk-based capital and assumptions review for its life business are the most critical metrics to watch. Material improvement would result in me shifting my view, but given the nature of the liabilities, I expect this to be a slow-moving situation rather than one that shifts quickly. While I will continue to monitor this upside risk and re-evaluate shares if they occur, I remain at the conclusion that you should invest elsewhere for now.