RyanKing999

RyanKing999

Lemonade (NYSE: LMND) reported earnings on February 27, 2023, which looked excellent initially. The company exceeded its guidance for Revenue, In-Force Premium ("IFP"), Gross Earned Premium ("GEP"), and Adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). The company also looks like it remains on track to achieve positive net cash flow in the first half of 2025. In addition, it beat analysts' revenue guidance by $3.99 million and GAAP (Generally Accepted Accounting Principles) earnings-per-share ("EPS") guidance by $0.19.

However, the company's guidance stuck in the craw of some analysts and investors. The stock dropped 27.72% the day after the company released its earnings due to analysts' disappointment with its first-quarter and full-year revenue forecasts, which came in lower than analysts' projections. Should investors use this pullback to buy Lemonade?

This article will discuss the company's forays into Europe, the company's quarterly results, why investors were disappointed in guidance, a few risks, the company's valuation, and why investors willing to speculate on a potentially high upside stock should consider buying this pullback.

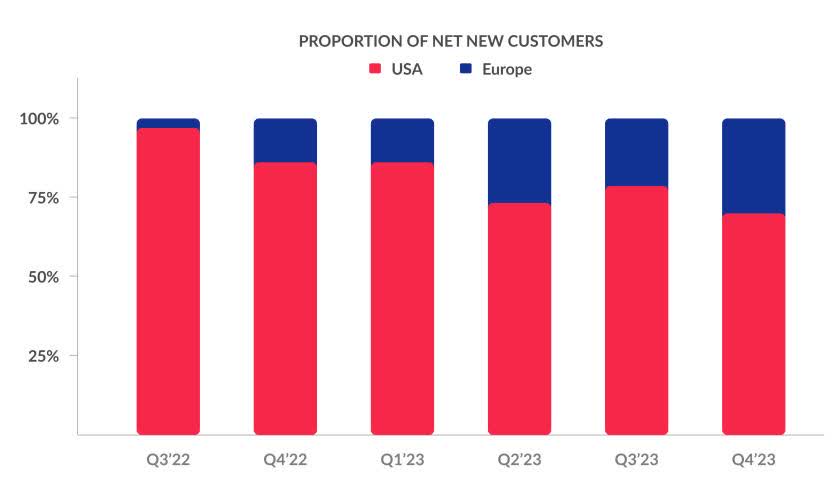

Management had not talked much about its European operations until now, likely because the business had yet to produce enough to move the needle. However, the European insurance operations have become meaningful enough to get a discussion section in Lemonade's fourth quarter 2023 Shareholder Letter. The image below shows that in the third quarter of 2022, Europe only made up 3%, a tiny fraction, of net new customers, and as of the fourth quarter of 2023, that number has risen substantially to around 30%. The company explained in the Shareholder Letter that although the U.S. adds more new customers in absolute numbers, it also has higher churn levels. Therefore, net new customers in Europe are closing the gap with the U.S.

Lemonade Fourth Quarter 2023 Shareholder Letter

Lemonade's ability to expand in other markets outside the few markets where it already has operations within the U.S. represents much of its future growth potential. And European markets represent a substantial part of that potential future upside. The company has a pan-European license to sell insurance in 30 European countries. So far, it only has operations in Germany, the Netherlands, France, and, in 2022, the United Kingdom ("U.K."). The European market is attractive to Lemonade because the company has more freedom to adjust pricing without pre-approvals, the regulatory environment is more favorable than the U.S., and Europe has fewer catastrophic storms than the U.S.

Lemonade's fourth quarter 2023 shareholder letter stated the following about the European business:

Our European business made solid strides in 2023, with increasingly healthy loss ratios and profitable unit economics, and the launch of the U.K. market - which quickly became our largest customer base in Europe. Our European business is still dwarfed by our U.S. book, but it is faster growing (~100% IFP growth in 2023) and has much to commend it.

Source: Lemonade Fourth Quarter 2023 Shareholder Letter

Lemonade could grow European insurance operations even faster. A large part of the reason Lemonade has proliferated in its existing U.S. markets is its business model of upselling and cross-selling additional insurance products. Until now, all of Lemonade's European operations were monoline renters' insurance, meaning no opportunity to upsell or cross-sell. However, that will change when Lemonade launches homeowner insurance in the U.K. and France in 2024. If it can replicate the success of its U.S. multi-line insurance upselling and cross-selling strategies in Europe, the company's potential upside will increase.

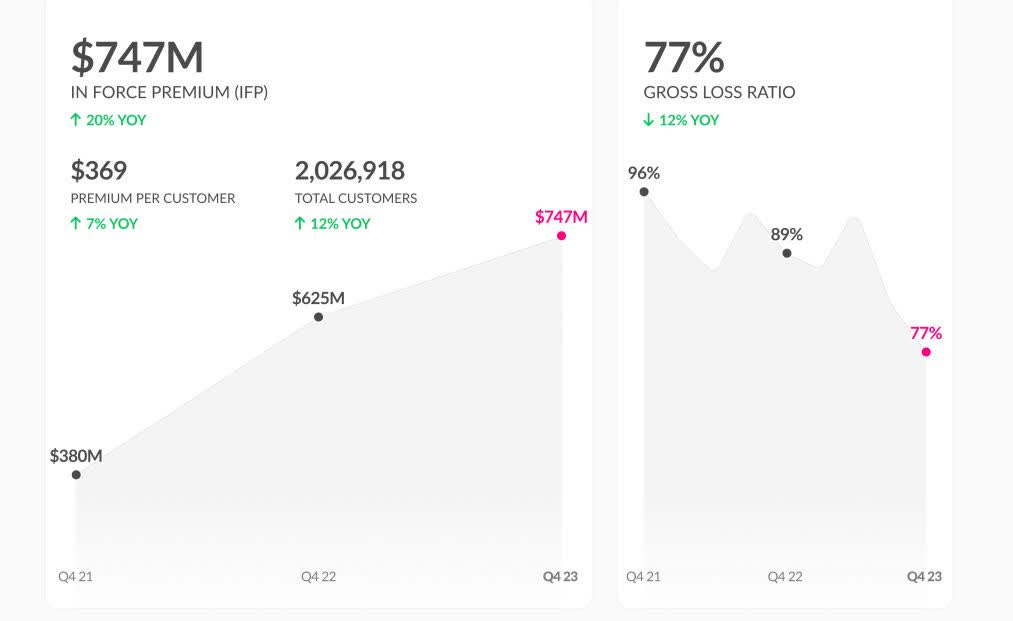

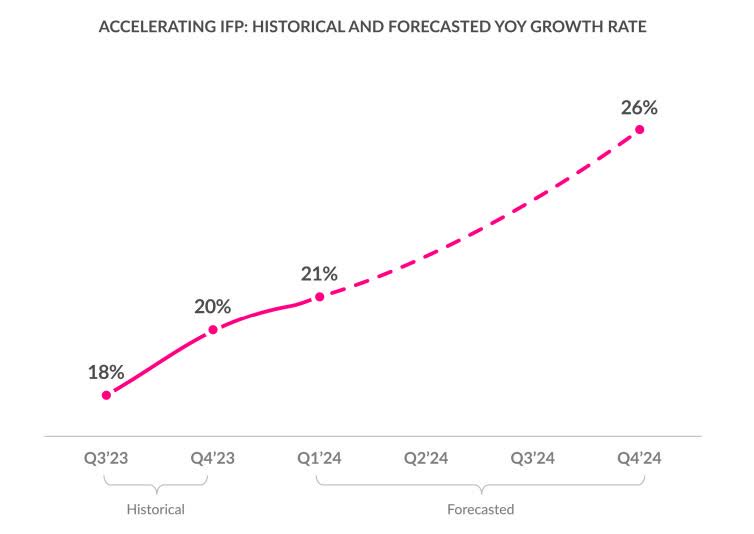

Lemonade grew In-Force premium (IFP) by 20% year-over-year to $747 million, beating management's guidance for the fourth quarter of $726 - $729 million. IFP represents the total value of all currently active insurance contracts. This number is significant because it reflects the total monetary value an insurance company expects to receive if the policies remain in effect. Lemonade suggests using IFP as a more consistent topline metric rather than revenue because management sometimes negotiates different levels of ceded premium when renewing contracts with reinsurers, which can distort revenue comparisons from period to period. IFP is better for making apple-to-apples topline comparisons.

Lemonade's Fourth Quarter 2023 Shareholder Letter

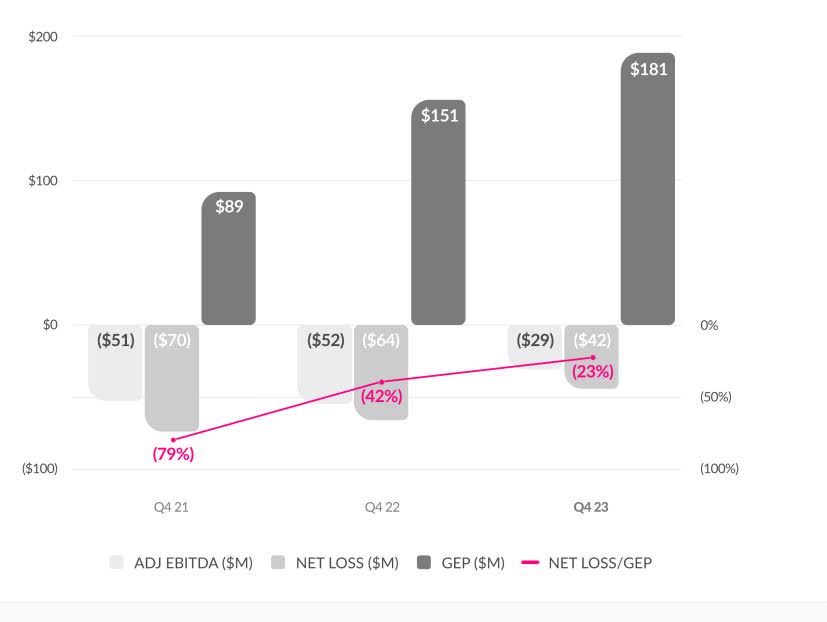

Since IFP only represents potential revenue, it is essential to analyze the gross earned premium ("GEP") in concert with IFP, as GEP represents the total amount of insurance premiums earned by Lemonade during the quarter and directly translates to revenue once the company cedes the contracted premium to reinsurers. The company grew gross earned premium ("GEP") by 20% year-over-year to $181 million, which exceeded company guidance that called for $174 - $176 million in GEP. The following chart shows Lemonade's GEP and fourth-quarter profitability trends between 2021 and 2023. The company reported an Adjusted EBITDA loss of $29, a reduction of 44% year-over-year. This number exceeded company estimates for an adjusted EBITDA loss of between $44 - $42 million and exceeded analysts' estimates by 28%, indicating outstanding profitability growth. The company's net loss also improved from $64 million in the previous year's comparable quarter to a net loss of $42 million in the fourth quarter of 2023.

Lemonade Fourth Quarter 2023 Shareholder Letter.

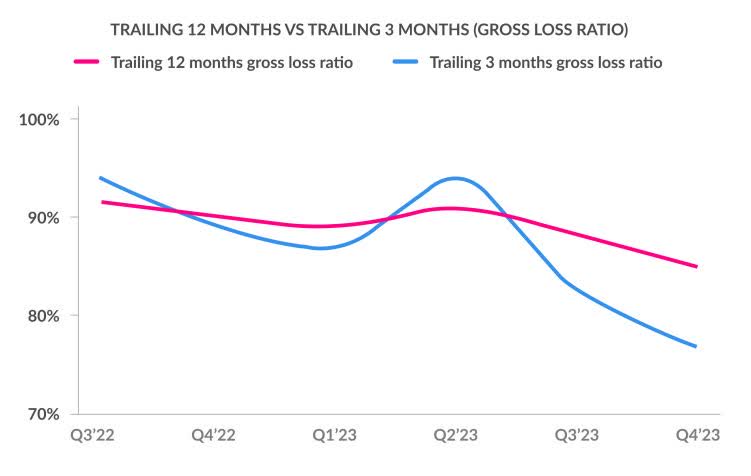

Lemonade achieved a gross loss ratio of 77% in the fourth quarter, down 1200 basis points ("bps") from the fourth quarter of 2022 and down 1900 bps from the fourth quarter of 2021. However, management warned investors that the company is not out of the woods yet and the gross loss ratio could return to the 80s. The company still seeks more premium rate approvals from regulators to write profitable business. Because the gross ratio can fluctuate from quarter to quarter based on seasonal adverse weather patterns or unpredictable natural disasters, management decided to introduce the gross loss ratio on a trailing 12-month ("TTM") basis this quarter to smooth out volatile fluctuations. Presenting the gross loss ratio on a TTM basis gives investors a better idea of how the metric trends.

Lemonade Fourth Quarter 2023 Shareholder Letter.

Next, let's go over Lemonade's cash flow and financial condition.

Some investors have shunned Lemonade because of its lack of free cash flow, which raises the risk that the company could eventually burn through its cash reserves enough for insurance regulators to shut down Lemonade's insurance operations. Management had some good news on the cash flow front in its fourth quarter 2023 Shareholder letter, which stated:

Something noteworthy happened in H2 2023: our total cash levels rose. We ended Q2 with $942m in 'cash and investments', while we ended both Q3 and Q4 with $945m. This suggests we've been flirting with net cash flow positivity (i.e. a favorable change in cash and investments) for a couple of quarters now. This isn't our new normal quite yet, though we're not far off either. During 2024 we will likely burn, rather than generate cash, but far less than our projected Adjusted EBITDA losses would imply.

Source: Lemonade Fourth Quarter 2023 Shareholder letter

The above statement emphasizes that the company is closing in cash flow positivity. While Lemonade might produce some cash burn in 2024, management expects the losses to be far less substantial than those implied by Adjusted EBITDA figures. The shareholder letter also projects net cash flow to turn consistently positive in the first half of 2025. Suppose Lemonade does achieve positive net cash flow in the first half of 2025; a few concerns about Lemonade running into near-term financial difficulties would evaporate. Based on known information, Lemonade appears to have a relatively healthy financial position.

As of December 31, 2023, Lemonade had approximately $945 million in cash, cash equivalents, and investments, providing a meaningful cushion to sustain operations during periods of temporary unprofitability. In addition, its insurance subsidiaries have a statutory surplus of $182 million for the benefit of policyholders.

Lemonade falls under Risk-based capital ("RBC") regulations from New York, Delaware, and California regulators that require it to maintain a minimum amount of capital based on its risk profile. This capital acts as a financial buffer to ensure the company can meet its obligations to policyholders even if it faces unexpected losses. Suppose Lemonade falls below a minimum threshold (called the "mandatory control level"). In that case, regulators can take various actions, with the worst outcome being that the company could lose its regulatory approvals to conduct business. In Lemonade 2022 10-K, on page 18, it stated that "As of December 31, 2022, LIC (Lemonade Insurance Company) maintained a risk-based capital level of 376% and MIC (Metromile Insurance Company) maintained a risk-based capital level of 440%," meaning that Lemonade's insurance subsidiaries have significantly higher RBC ratios than the minimum required level and are unlikely to face regulatory intervention due to insufficient capital.

However, that was as of the end of 2022. Last year, Lemonade released its fourth quarter 2022 earnings on February 22, 2023, and its 10-K on March 3, 2023. If you are interested in investing in Lemonade, consider looking up Lemonade's RBC ratios when the company releases its 2023 10-K in early March to ease your mind about whether the company's subsidiaries have adequate capital.

Lemonade Agency B.V., and Lemonade B.V. Lemonade Insurance, operate under European insurance regulations and the regulators from each country where it has operations. I could not find detailed information about how much capital European regulators require Lemonade to have.

Analysts were disappointed in Lemonade's revenue guidance for the fourth quarter and the full year of 2024, as Wall Street consensus analysts' forecast called for the company to generate 22% year-over-year growth in 2024. Instead, Lemonade forecasted only 19% growth for 2024. The first quarter consensus analysts' expectations were for approximately 26% year-over-year quarterly growth in the first quarter, compared to management, who called for only 19% growth. Additionally, the company called for more customer acquisition spending in 2024. Management added the following commentary in its fourth-quarter shareholder letter:

We plan to roughly double our growth budget in 2024, from the $55m spent in 2023. Doubling spend won't double our growth rate, since (i) the number of customers we acquire organically won't be impacted much, and (II) our denominator has swelled - but in dollar terms we expect to add about 50% more IFP in 2024 than we did in 2023.

Source: Lemonade Fourth Quarter 2023 Shareholder Letter.

The fact that Lemonade wants to spend more and not even achieve analysts' near-term growth expectations didn't go over well on Wall Street and was one of the most likely culprits for why the stock sank on February 28, 2023. The management realizes topline growth could be better and understands that for Lemonade to get its costs in line, the company needs to grow much larger and faster as the company today is subscale. The company plans for its "growth budget" increase to bring IFP up from the current quarter's 20% to 26% by the fourth quarter of 2024.

Lemonade Fourth Quarter 2024 Shareholder Letter

Lemonade's choice to invest in growth initiatives will temporarily reduce its adjusted EBITDA in 2024. In the past, increased spending for customer acquisition directly negatively impacted cash flow. But thanks to Synthetic Agents, Lemonade can now protect its cash flow from immediately dropping. Management recently expanded its Synthetic Agents program with General Catalyst, so the program likely had its intended effect in the short time the company has used it. However, while the General Catalyst deal prevents its cash flow from immediately dropping, GAAP accounting rules still require Lemonade to record the new $55 million in spending as an expense in 2024 EBITDA calculations. So, rising spending on customer acquisition comes at the cost of making it more difficult for the company to reduce adjusted EBITDA losses. If Adjusted EBITDA comes in higher than analysts expect over the next year, the stock may drop further. The company's fourth-quarter shareholder letter states:

The associated spend, and the resultant [IFP] growth, should boost our bottom line a couple of years hence, but it will weigh on our bottom line in the coming quarters. Threading that needle - doubling growth spend while shrinking Adjusted EBITDA losses - will be our central challenge in 2024. To be clear, as our guidance below shows, we believe we are up to this challenge: we expect our Adjusted EBITDA to improve in 2024, notwithstanding the immediate downforce created by accelerated growth. We expect to pull off this maneuver thanks to our systems continuing to drive down our loss ratio, while driving up our operational efficiencies. We anticipate that the contributions of these two forces will more than offset the additional ~$55m we plan to spend on growth in 2024.

Source: Lemonade Fourth Quarter Shareholder Letter.

If Lemonade's plan works, the company will restore its topline growth to its target of over 25%. At the same time, it will continue on the road to positive cash flow and EBITDA profitability. However, if its plan runs into problems, growth or profitability could disappoint within the next several quarters, leading to further selloffs in the near term.

One reason the company's first quarter and 2024 revenue growth forecasts disappointed analysts in the first place may be because the company's artificial intelligence, named LTV 9, predicted home and car insurance would not achieve the profitability the company desires with the current premium rates. In response, management has intentionally slowed the written premiums in those areas until regulators approve new higher rates, and it can write profitable business. Since home and auto policies have the highest average premium, IFP, GEP, and revenue are lower than desirable due to the company throttling growth in those insurance lines.

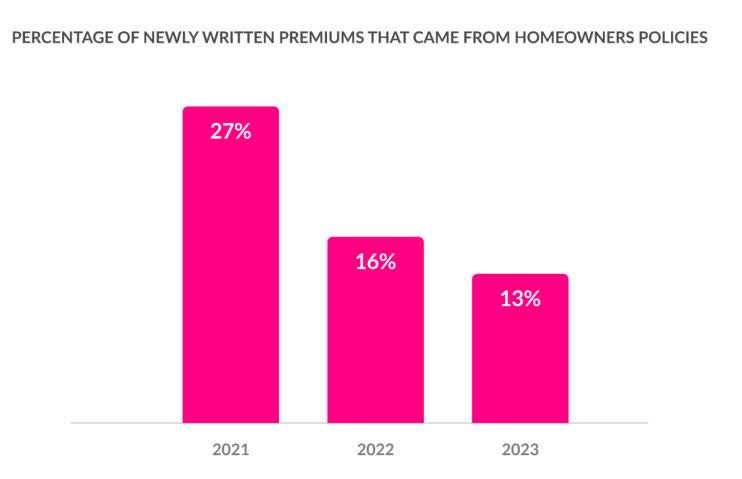

Management seems most concerned about the home insurance line of business. Home insurance profitability has been hurt recently due to the combined impact of more damage from storms, more claims, higher claims due to inflation in home repair exceeding the core CPI (Consumer Price Index) inflation rate, and the lag in getting new premium rates approved by regulators. As a result, management has pulled back drastically on writing home insurance policies. The following chart shows the extent of Lemonade's reduction of its newly written homeowner policies.

Lemonade's Fourth Quarter 2023 Shareholder Letter.

If management cuts back on home insurance and auto growth, where does it intend to spend its growth budget? One possible answer to that question comes from its LTV 9, which shows that renter's insurance and pet insurance will currently give Lemonade the most bang for the buck. The company wrote in its shareholder letter, "Our Renters business generates 12% higher LTVs than prior models predicted; that our Pet customers' LTV is very robust and little changed from prior models." In addition, although the company is cutting back on car and home insurance in areas where it is not profitable, it still writes car and home insurance in areas LTV 9 has identified as profitable. Another potential growth area to consider is that although management didn't explicitly mention that it plans to increase spending in its European subsidiaries, Europe may be where it will spend some of its customer acquisition growth budget.

Although the plan Lemonade outlined in its shareholder letter sounds nice on paper, where the rubber meets the road is perfect execution, and even that may not be enough. Many risks could trip the company up, from adverse weather to changes in the regulatory environment, privacy regulations, and more.

Lemonade is an early-stage company with an experimental business model. Even if the company's business model works out, Wall Street may be loath to give it a higher valuation until it proves its business model is viable. If you decide to invest in this company, don't expect the returns to happen immediately. This company's story could take several years to play out before investors see substantial price appreciation.

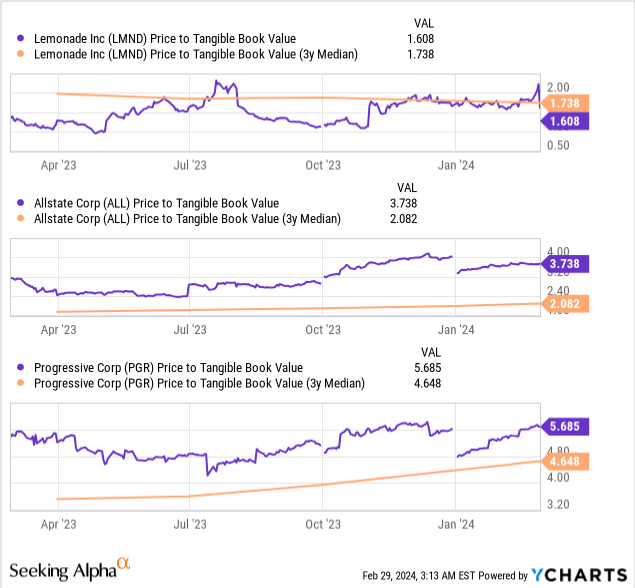

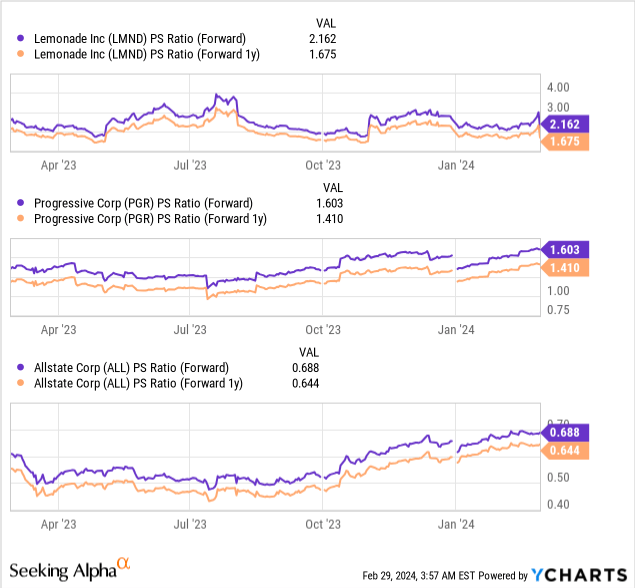

Lemonade is an exceedingly tricky to value because it lacks free cash flow and profitability. Since analysts can't reliably forecast the company's GAAP EPS, using forward price-to-earnings is out. Lemonade has a unique experimental insurance business model, and some people wonder whether the model can ever achieve profitability. Therefore, making comparisons to other mature, profitable insurance companies is challenging. The following chart compares Lemonade's price-to-tangible book (P/TB) to its three-year median P/TB and compares it to two mature insurance companies.

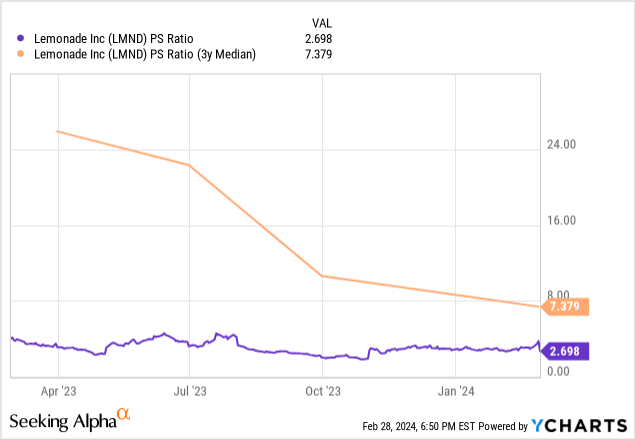

The company deserves to trade lower than Progressive (PGR) and Allstate (ALL) on a P/TB basis as those two companies are well-established and GAAP profitable on a net income basis. Lemonade's P/TB is slightly below its three-year P/TB median. If Lemonade traded at its three-year median, the stock price would be $16.89, which is 7.5% above its February 29 closing price of $15.70. The following chart compares Lemonade's price-to-sales (P/S) ratio of 2.698 to its three-year median P/S ratio. If Lemonade traded at its three-year median P/S ratio of 7.379, the stock would trade at $43.38 or $176% above its February 29 closing price.

The following compares Lemonade's forward (2024) P/S ratio and one-year forward (2025) P/S ratio with Progressive and Allstate.

The following table shows each of the above companies' expected revenue growth rates.

| Company | 2024 expected revenue growth rate | 2025 expected revenue growth rate |

| Lemonade | 18.27% | 26.98% |

| Progressive | 13.97% | 13.73% |

| Allstate | 7.55% | 6.80% |

Data Source: Seeking Alpha

On a forward P/S ratio basis, Lemonade deserves to trade higher than its more well-established competitors because it's growing faster. The big question is whether Lemonade can eventually turn its unprofitable topline growth into profitable growth. A large part of whether an investor considers Lemonade undervalued or overvalued is whether that investor believes management can achieve its goals of becoming consistently cash flow positive cash in the first half of 2025 and adjusted EBITDA turning positive in 2026. If Lemonade achieves its profitability goals, I believe it should trade around its three-year median P/S ratio, meaning my price target for 2026 is $43.38. However, suppose Lemonade fails to execute its profitability plans. In that case, the market may consider the stock vastly overvalued. Some believers in the company might start questioning its long-term viability, depending on how far it is from achieving its profitability goals.

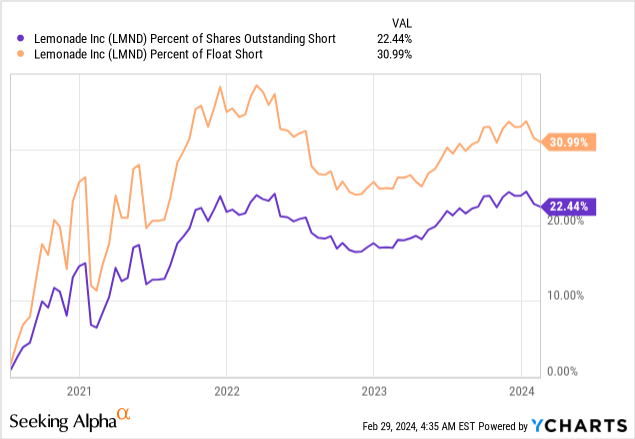

If you decide to invest, understand that it is a battleground stock with strong opinions for and against the company. If you're considering investing in Lemonade, it's crucial to realize that it's a controversial company, with solid opinions supporting and questioning its long-term viability. The company currently has 22.44% of its shares outstanding shorted, as shown in the image below.

Neither bulls nor bears know how the future will unfold for this company, and because of its uncertain future, consider the stock speculative. Even if you are bullish on the company, avoid "backing up the truck" and dumping your life savings into the stock. However, if you are an investor with a speculative mindset, the potential long-term upside may be worth a small percentage of your portfolio. I rate the stock a speculative buy.