bjdlzx

bjdlzx

Since I presented my 'Buy' thesis for Linde (NASDAQ:LIN) in my introductory article, the stock price has surged by more than 25%. The company released their Q4 FY23 result on February 6th, delivering 4% underlying revenue growth and 13.6% of adjusted profit growth. I reiterate 'Buy' rating for Linde with a fair value of $490 per share.

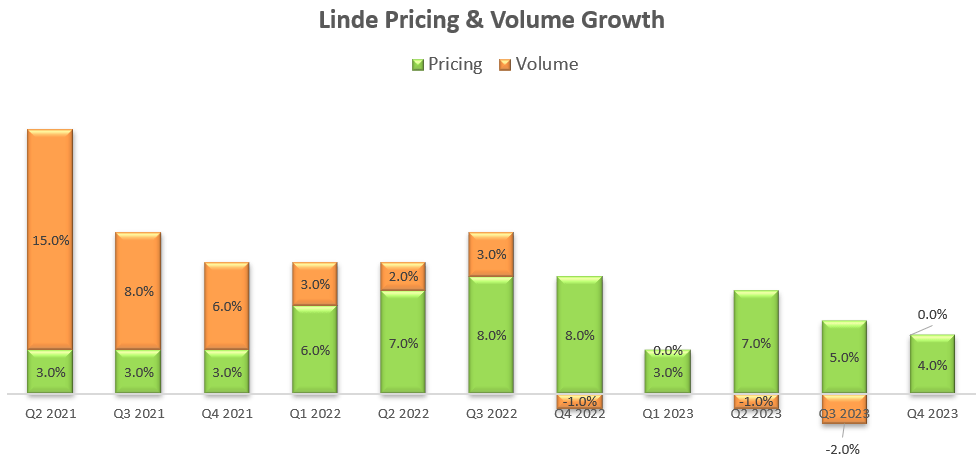

Linde's pricing has undergone a robust growth trajectory since the global pandemic, as evidenced by the chart below. In Q4 FY23, their core pricing was up 4% year-over-year with flattish volume growth.

Linde Quarterly Results

When the inflation was high, Linde did take the advantage to raise their pricing to offset their input costs. Interestingly, when the inflation cools down, Linde hasn't reduced their pricing. On the contrary, their management signalled that they would continue to take pricing actions throughout FY24, thereby enhancing margin expansion moving forward. While industrial gas is a highly competitive industry, Linde owns pipeline networks in many locations, and supply reliable industrial gas to their customers. Once these pipelines were established, customers would face significant hurdles to switch to an alternative gas supplier. Consequently, Linde has strong pricing power over some of their customers.

Additionally, Linde initiated their cost management program from FY20, undertaking measures such as location consolidations, business rationalization projects and process harmonization, as disclosed in their FY22 10-K. Linde starts to harvest from these cost management initiatives implemented in the previous years.

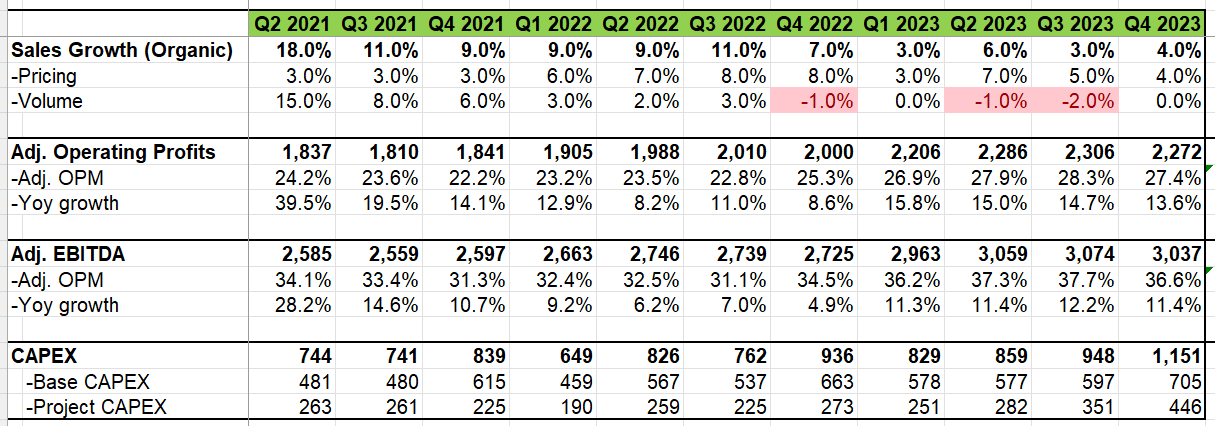

Lastly, as emphasized in my introductory article, Linde's cost passthrough contact model empowers them to pass some unpredictable costs to their customers, mitigating their margin volatility. As exhibited in the table below, Linde's operating profits surged by 13.6% in Q4 FY23, and their EBITDA increased by 11.4% year-over-year, quite remarkably!

Linde Quarterly Results

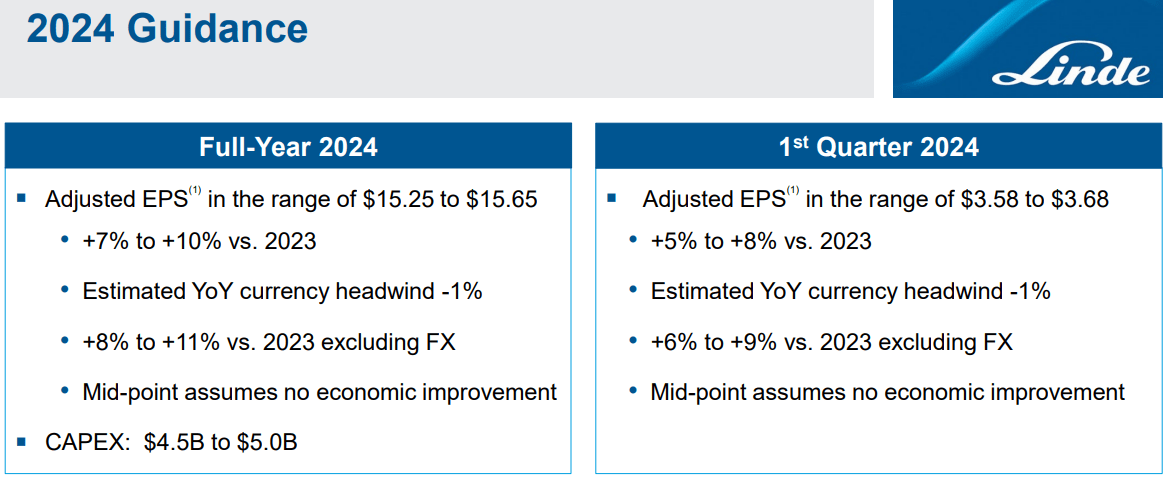

A significant takeaway from their FY24 guidance is the projection of 8%-11% of adjusted EPS growth on a constant currency basis. It's worth noting that their mid-point guidance doesn't assume any economic improvement in the industrial production.

Linde Investor Presentation

To estimate their FY24 growth, I consider the following moving pieces:

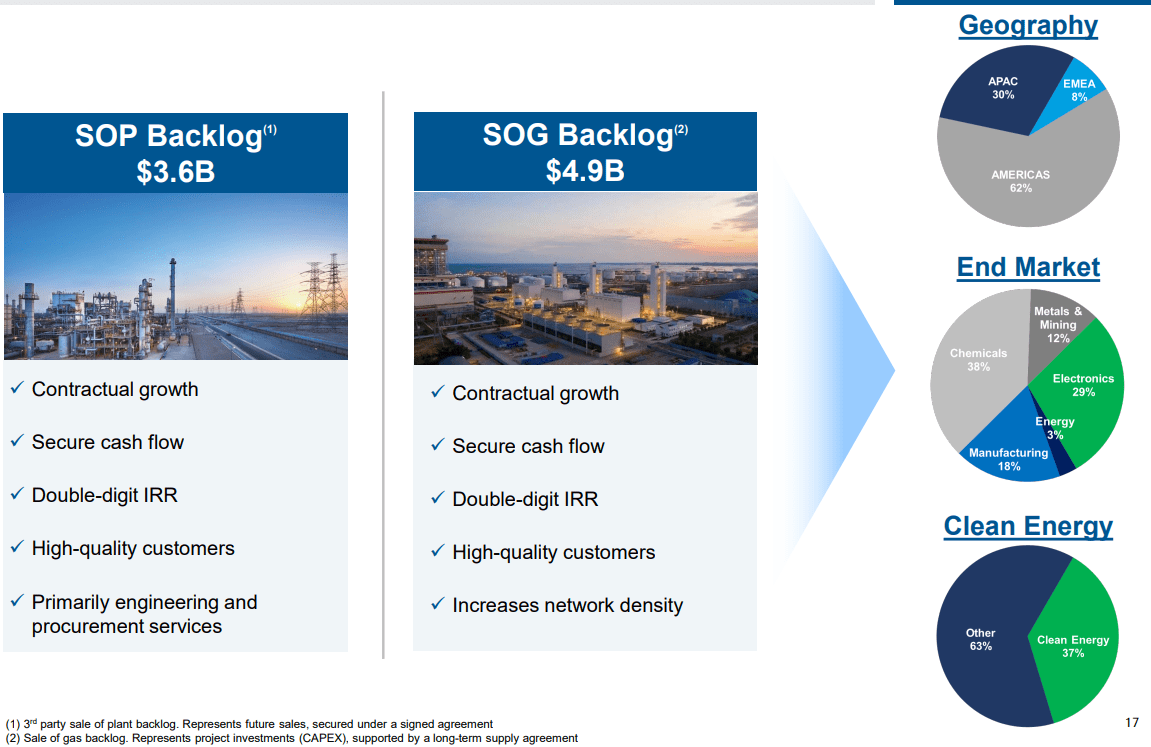

-High Quality Project Backlog: as shown in the slide below, Linde has an impressive $8.5 billion worth of high-quality project backlog, poised to gradually translate into the actual revenue. They define the high-quality project as double-digit IRR, secure cash flow and high-quality customers. More than 1/3 of these projects are clean energy related. As I mentioned in my previous coverage, Linde is benefiting from the mega trend of global decarbonization. During the earnings call, their management indicates they have been witnessing large project opportunities led mainly by decarbonization initiatives. They anticipate that the contribution from their high-quality project backlog will bolster EPS by 1%-2% in FY24.

Linde Investor Presentation

-Pricing Growth: As previously discussed, Linde possesses formidable pricing power, and their management is confident that they could continue to take pricing actions even in a low-inflationary environment.

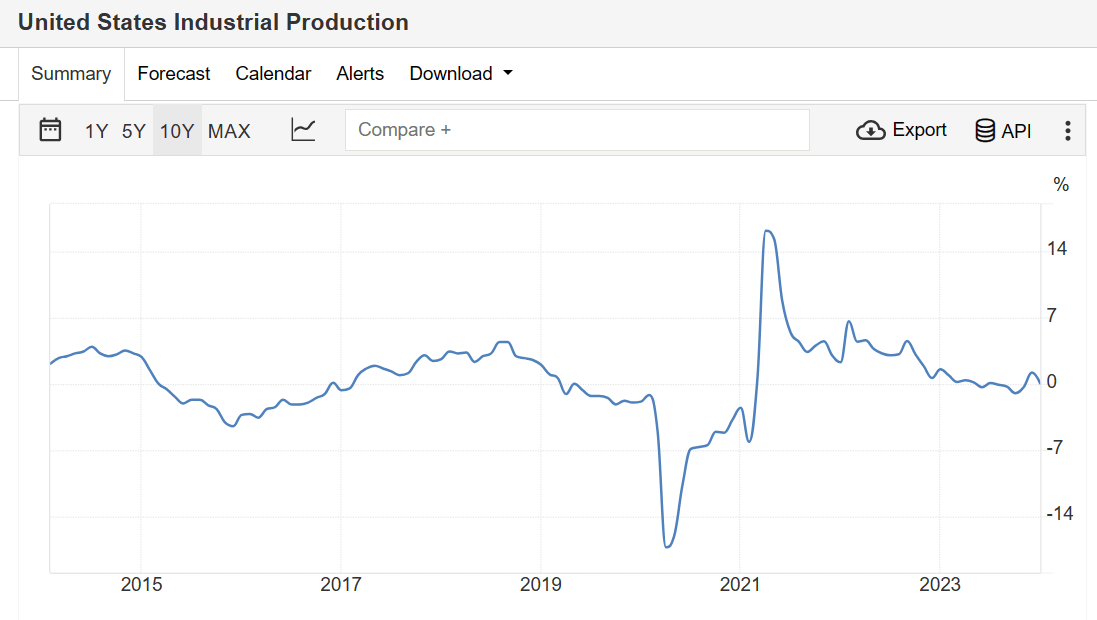

-Industrial Production Growth: As depicted in the chart below, the U.S. industrial production growth has been quite weak during the post-pandemic period, reflecting a reduction in consumer expenditure on physical goods. I don't foresee a significant recovery in overall industrial production growth for FY24. Consequently, the gas volume growth from existing customers is expected to remain subdued.

Trading Economics

-Shares Repurchase: Linde repurchased $3.9 billion own shares in FY23, $5.1 billion in FY22 and $4.6 billion in FY21. The shares repurchase reduced their shares outstanding by 2.3% in FY23 and boosted their EPS growth. Assuming Linde allocates 12% of total revenue toward shares repurchase, their shares reduction would be over 2% in FY24, as per my calculation.

So let's put all the pieces together: project backlog 1%-2%; plus pricing 5%; plus shares repurchase 2%. The EPS growth would be around 8%-9% even without any volume growth from existing customers.

For the revenue growth assumptions, I break down into 4 main components: pricing, volume, passthrough, and tuck-in acquisitions. I am applying the historical average to these parameters: 3% pricing growth, 2% volume growth, 2% passthrough and 0.1% acquisition growth. Consequently, the revenue growth is projected to be 7.1% in the model.

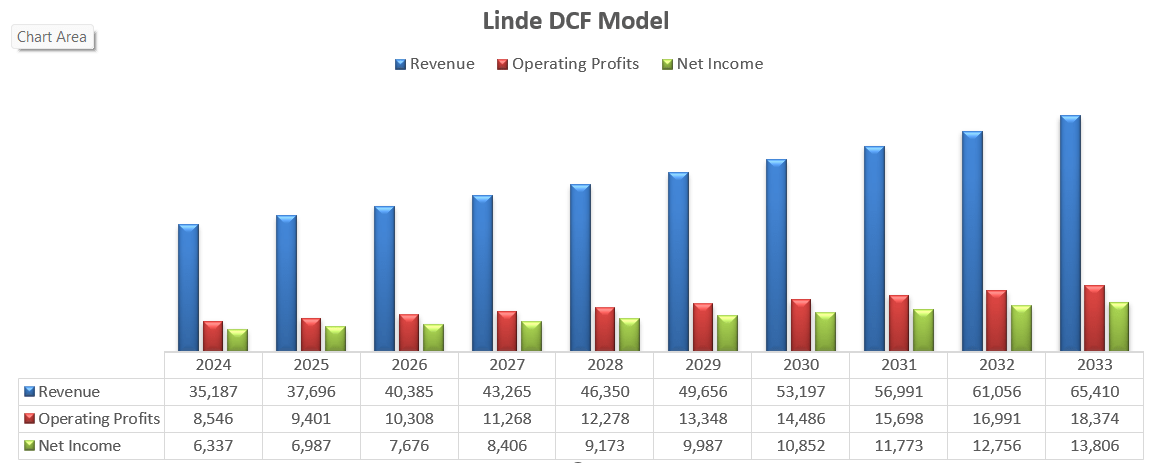

Their margin expansion is propelled by operating leverage, pricing increase, as well as the diminishing restructuring costs. Linde spent $2.4 billion towards restructuring (cost reduction program), and I anticipate their restructuring activities draw to a close, and the associated costs will diminish over time. I calculate their operating expenses will grow by 6.2% per year; therefore, their operating margin could potentially reach 28.1% by FY33.

Linde DCF Model

I am applying 10% WACC across all my models, and using a two-stage DCF model. With these parameters, the free cash flow to firm (FCFF) is estimated to be:

Linde DCF Model

On the balance sheet, Linde has $4.66 billion in cash and $19.3 billion in debt. Adjusted the net cash/debt position, the fair value of Linde is calculated to be $490 per share, and the current stock price is trading at 30x fwd. FCF.

Argentinian Peso Depreciation: As disclosed over the earnings call, the Argentinian Peso depreciated over 50%, and they recorded a charge of $10 million to the American profits and another $20 million to the interest expenses. Despite Linde's efforts to realign local prices in response to high inflation, it would take some time for a full recovery in the Argentinian market.

China: The market accounts for around 7% of group revenue and profits. The weak manufacturing activities have presented some growth challenges for Linde. During the earnings call, their management acknowledged the weakness of their China operations, and anticipated a mild recovery probably through the first half of FY24. It appears to me that their management lacks clear visibility in China, as the manufacturing activities in China could be affected by the government regulations, as well as the demands of physical goods in the developed countries.

Linde stands well positioned to capitalize on the global trend towards decarbonization. I favor their cost passthrough business model and their capability to deliver double-digit earnings growth. I reiterate 'Buy' rating for Linde with a fair value of $490 per share.