Schon/Moment via Getty Images

Schon/Moment via Getty Images

Lennox International, Inc. (NYSE:LII) is a Texas-based company that designs, manufactures, and supplies climate control products for heating, ventilation, air conditioning (HVAC), and refrigeration markets in the US, Canada, and other countries.

Lennox closed the previous year with good results. It sustained revenue growth and became more viable amid its continued expansion. Also, it maintained decent liquidity levels despite its high borrowing level. It showed enough capacity to cover a larger operating capacity and distribute dividends.

However, investors must beware of its current valuation. The stock price has substantially increased in the past year, making it expensive. Several price metrics show overvaluation, so giving the company a hold rating should be logical.

Lennox navigated a challenging market landscape in 2023. It also had to account for the negative spillovers of the residential property sector. Yet, its transformation strategy and enhanced efficiency allowed it to maintain decent topline growth.

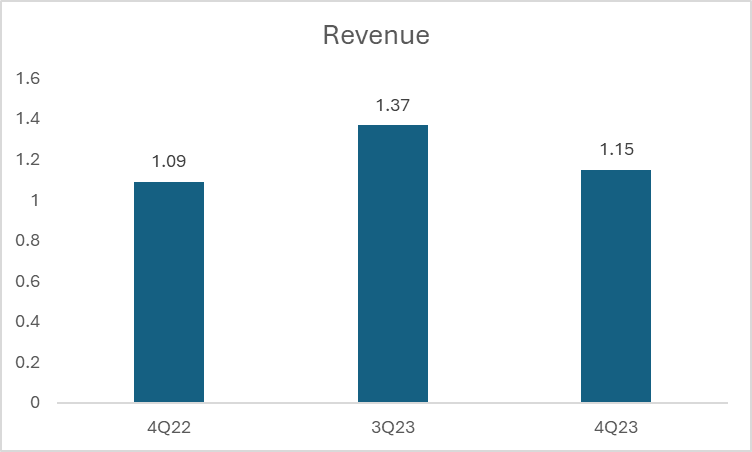

Its operating revenue reached $4.98B, a 5.5% YoY growth. Its Building Climate Solutions became the primary revenue growth driver after increasing by 17% YoY. It comprised 30% of the total sales compared to 27%, showing a substantial increase relative to the two other segments. Its Home Comfort Solutions remained the primary revenue component, with $3.22B or 64% of the total sales. Yet, it only rose by 0.8% and offset the impact of the Building Climate Solutions segment. Also, sales growth was much smaller than in 2021 at 18% and in 2022 at 15%. We can attribute it to the challenges faced by the residential property market. But with the effective pricing strategy, LII offset the volume drop.

If we concentrate on 4Q23, the year-over-year growth rate was slightly higher at 5.6%. The growth rate of revenue components was slightly better than the whole year. It was lower than in 3Q23, leading to a 16% QoQ decrease. But historically, the second and third quarters of every year had the highest sales, mainly driven by seasonality. Meanwhile, investors must note the 20% drop in sales volume through the 2-step distribution channel. This was primarily due to the high inventory destocking. Thankfully, its sales volume through its direct-to-contractor channel increased, showing stable consumer demand.

Revenue (LII 4Q23 Earnings Release)

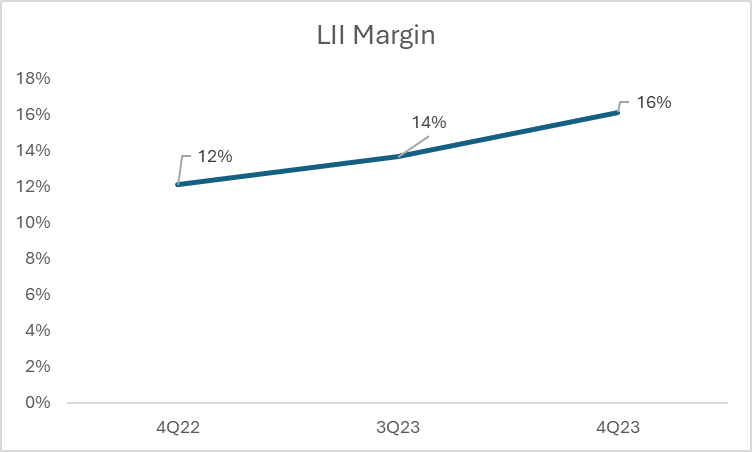

On a lighter note, topline growth was boosted by LII's enhanced operating efficiency. Its revenue growth outpaced the increase in the operating costs and expenses. It was most visible in the Building Climate Solutions segment, having the highest contribution to the operating income. As such, the operating margin in 4Q23 reached 16% compared to 12% in 4Q22 and 14% in 3Q23. It was also better than in 2021 and 2022, with margins of 14% and 13%, respectively.

Operating Margin (LII 4Q23 Earnings Release)

During the second half of 2023, LII capitalized on expansion. It acquired AES to expand its HVAC services in the light commercial market. As such, the company must ensure adequate resources to sustain a larger operating capacity. And since a substantial part of its production involves machinery and large equipment, LII is a capital-intensive company. It's no wonder it has relied heavily on borrowings over the years.

Despite this, LII maintained decent liquidity and efficient asset management. We can see it in its stable cash and receivables. Cash increased by 15% from $52.6M in 4Q22 to $60.7M in 4Q23. Meanwhile, it paid a portion of its borrowings. The total borrowings were $1.52B, equivalent to 54% of the total assets. But it was much lower than in the same quarter last year with $1.74B. This was an ideal trend, considering it recently acquired a company to expand its business.

Even better, the topline growth of LII remained decent enough to help repay its borrowings. It had a Net Debt/ EBITDA Ratio of only 1.66x versus 2.28x last year. With that, the company can pay all its borrowings in less than two years, even if it doesn't have to.

Lastly, its book value improved, given its positive equity, which used to be a deficit in previous years.

At this point, we must have realized that while LII sales kept increasing, the growth drop was substantial. Again, we are pointing out the negative spillovers of the residential property market. It may continue to pose downside risks this fiscal year.

First, the US housing inventory remained low. It has improved in the past year but remained slower than expected. We can attribute it to the caution that property builders have practiced over the past decade. Indeed, the scars of the real estate bubble have remained evident. The previous year started with over 7M housing shortages. In August 2023, it dropped between 5.5M and 6.8M housing units. Yet, the shortage of affordable housing was still high at 7.2M units. As of December 2023, the US was short of 4M units. This means the housing inventory was 4.9% higher than in 2022 but 36% lower than pre-pandemic levels.

We can't expect prices to just drop to an affordable level. The property market will not crash since excessive demand is the primary price driver. As long as inventory remains low, upward pressures on housing prices will remain. As of 4Q23, the median sales price of houses in the US was $417,700.

Given all this, many Americans will either join the competing renters to pay a relatively lower price or temporarily live in an RV. These have negative spillovers on LII. Higher home prices mean lower purchasing power, and renting a home or an RV can lower the demand in its residential home segment. In turn, LII may have lower flexibility to increase prices to offset the lower volume. There is a risk of lower sales in the segment, which can impact the stock price performance.

These are some external forces that can mitigate risks in FY24.

The US inflation has been on a roller coaster ride since the pandemic. It peaked and set a new all-time high at 9.1% in 2022. But since 2023, we have seen a substantial decrease in revenue. There were some upticks during the third quarter, but they remained manageable. Thankfully, the US avoided the anticipated recession.

Currently, US inflation is only 3.1%, compared to January 2023 at 6.4%. More interestingly, it shows the normalization of consumption after the spending splurge during the holiday season. In the subsequent months, we can expect the continued inflation deceleration. The same goes for Canada, with inflation of only 2.9% versus 5.2% in January 2023. In addition, the Fed eyes to cut interest rates thrice this year as inflation approaches the 2% target band.

If all these materialize this year, LII can support its growth potential. Lower inflation means higher capacity to enhance its production level and adjust pricing strategies to address the residential market challenges. These can lead to lower input costs and higher operating profit. Also, lower inflation means higher purchasing power and demand for its products. It can boost its building segment as more companies implement RTOs and buildings see higher occupancy rates.

Most importantly, interest rate cuts will be good for its liquidity since the company will incur lower borrowing costs. It will also lower the US mortgage rates, making housing units more affordable. This may have positive spillovers in the residential market segment of LII. Policymakers may have to be more careful, though, since housing inventory remains low. Otherwise, there may be an offsetting impact between mortgage rates and demand.

Its capitalization on expansion will be fruitful, given the improving macroeconomic landscape. Acquiring AES was pivotal in 4Q23 growth as it increased LII's market presence in the US. It also helped increase the production level, especially in the building segment. Given the lower inflation and potential rate cuts, there may be more demand for HVAC products and services. So, LII may have to adjust its production volume to cater to the market. With AES, LII is one step ahead of the market. It can produce more and faster amid the sustained inflation deceleration, which can generate economies of scale in the long run. In turn, it can adjust prices to a desirable level to maintain or increase the demand while deriving more income.

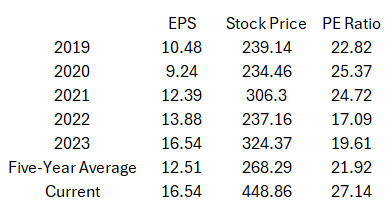

LII has continuously rebounded and increased in the past year. It returned to the $300 level after bouncing back from the 2022 lows. Now, it is valued at $448.68, 79% higher than its price on the same day last year. It is also the first time that Lennox exceeded the $400 mark since it started trading.

However, this sharp price increase makes it challenging to get an ideal entry point for a buy position. Also, it appears too high and unreasonable for its fundamentals. If we value the price in terms of earnings, we will derive a PE Ratio of 27.14x, which is much higher than the S&P 400's 18.14x. We can even compare it to its five-year PE Ratio. The PE Ratio of LII is unusually high relative to the values in the past five years. It is also much higher than the five-year average PE Ratio of 21.92x. If we use the average ratio to derive the stock price, the value will only be $352.56. Using the PE Ratio, the stock price shows a downside risk of 21%.

PE Ratio (Data: Yahoo Finance, Author Computation)

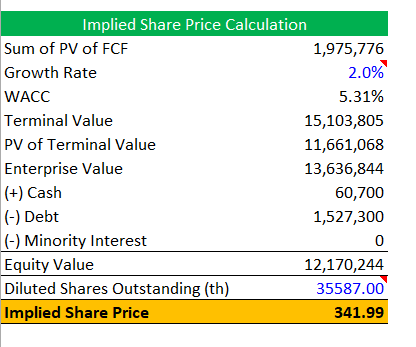

We can also use the DCF Model for a more precise valuation. It is also applicable to LII since it is a capital-intensive company.

DCF Model (Author Computation)

The DCF Model also shows downside risks, given the potential overvaluation of the stock price. The growth of 2% seems logical and conservative to me. This is in line with the Fed's target inflation level of 2%. It is also a safe percentage since sales growth has slowed recently. When increased to 2.5% and 3%, the implied share price increases to $395.95 and $440.84. Either way, the stock price remains overvalued. Meanwhile, I got the WACC using the CAPM method.

Lennox International, Inc. maintains a solid performance with decent topline growth and liquidity. However, buying the stock comes at a high price with some downside risks. It appears expensive now, so it is difficult to get an entry point to buy. Hence, I am recommending it as a hold.