stocknshares

stocknshares

I have to say, I'm in an incredibly good mood while I'm writing this. It doesn't have anything to do with the market, just the fact that it's officially spring in the Northern Hemisphere, which - I think - is the best time of the year.

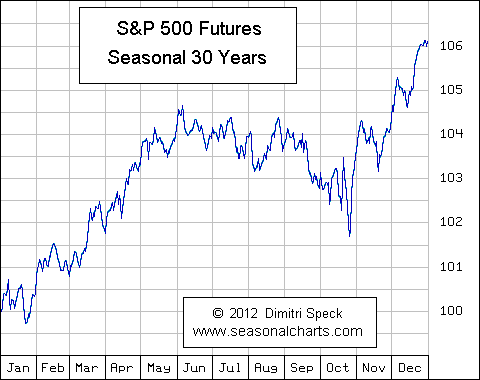

As it turns out, I'm not the only one who enjoys spring, as the seasonal pattern of the S&P 500 shows that March, April, and May tend to be very good months to be long stocks. That's based on 30 years' worth of data.

Seasonal Charts

With that said, the main message of this article isn't to make the case that now is the best time to buy stocks. I just wanted to start this article by mentioning how glad I am that spring is just around the corner.

It also means we're very close to the start of the MLB (baseball) season, which I like to follow for a wide range of reasons - but more on that in a future article.

On a more serious note, this article will be about a macroeconomic update and stock picks.

We'll discuss inflation risks, potential market valuation headwinds, and three stocks that I like in this market.

After writing an article titled "30,000 Followers Special - Here's How I Would Invest $30,000 In Today's Market," I got a huge amount of requests to write a similar article.

However, people wanted a better utilization of $30,000. In my prior article, I gave nine picks that would have brought the average investment size to just $3,333 ($30K/9).

In this article, I'll give you three picks that I like.

So, with all of that being said, let's get to it!

A lot has changed over the past two years.

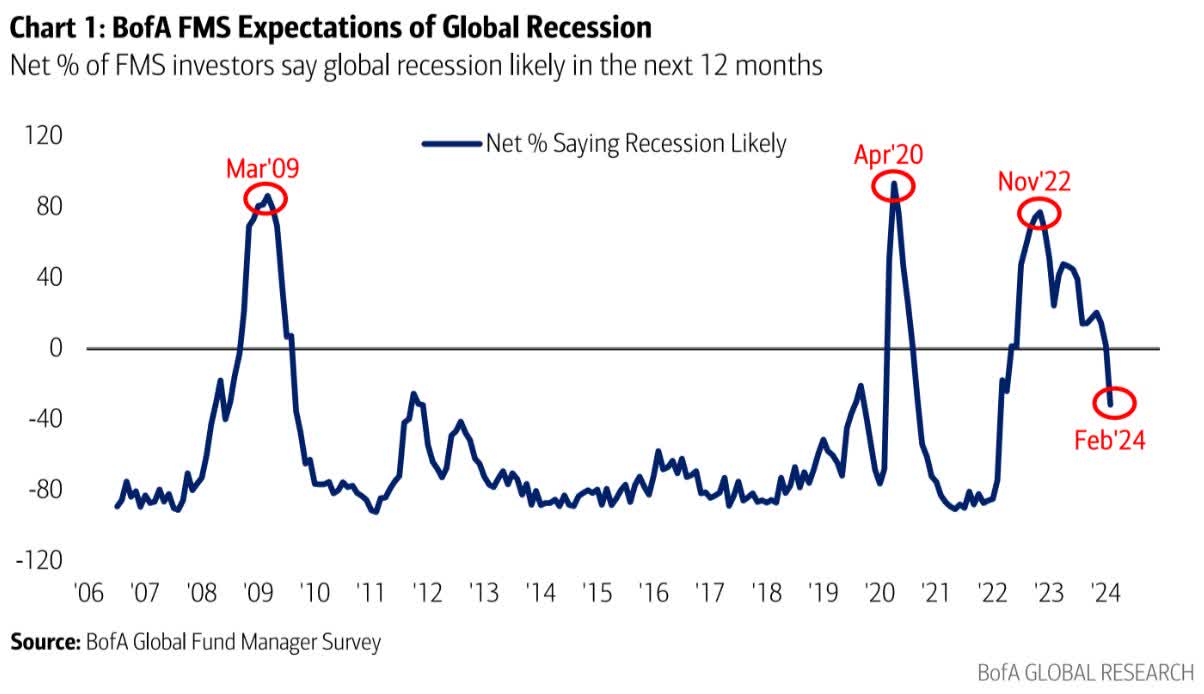

I just found a chart from last month that showed that in November 2022, close to 80% of fund managers interviewed by Bank of America (BAC) believed that a recession was likely.

That number remained elevated through the first half of last year before falling inflation, and a more dovish interpretation of Fed comments led managers to believe that a recession could be avoided.

Bank of America

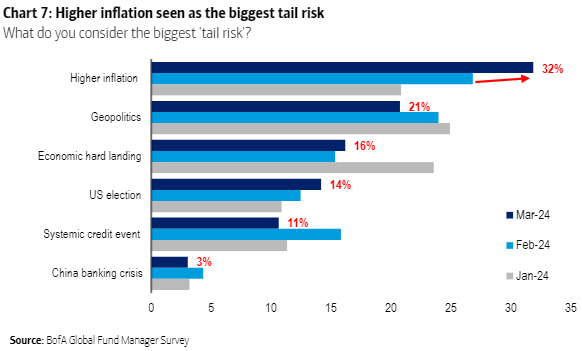

In fact, the latest numbers show that the market is now worried about other things.

Using data presented by Bloomberg's John Authers, we see that global fund managers are now increasingly worried about higher inflation rather than geopolitical issues or economic slowdowns.

Bank of America

This also makes it harder for the Fed to cut rates.

Although it is tough to find empirical research that suggests that the Fed is driven by sentiment, all of this continues to support my "higher-for-longer" thesis.

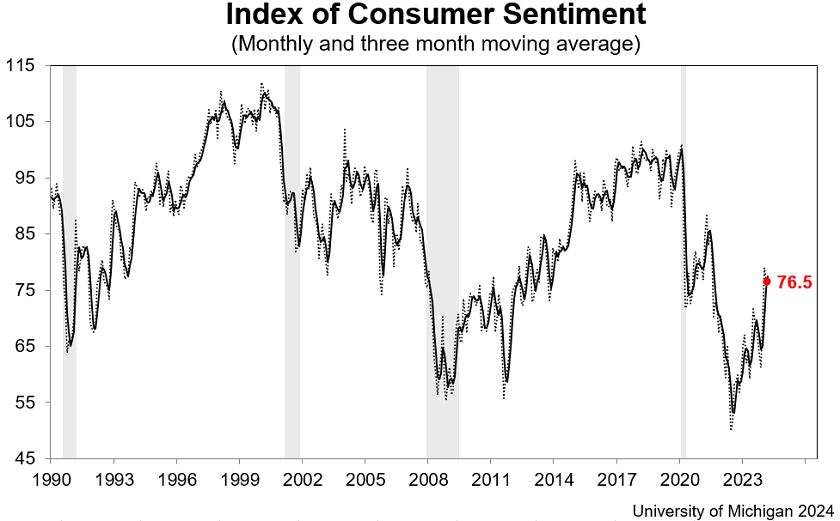

With that in mind, most readers will recall that I often talk about a weakening economy.

I have been talking about a slowing economy since 2022. That's based on two important observations.

Bloomberg

University of Michigan

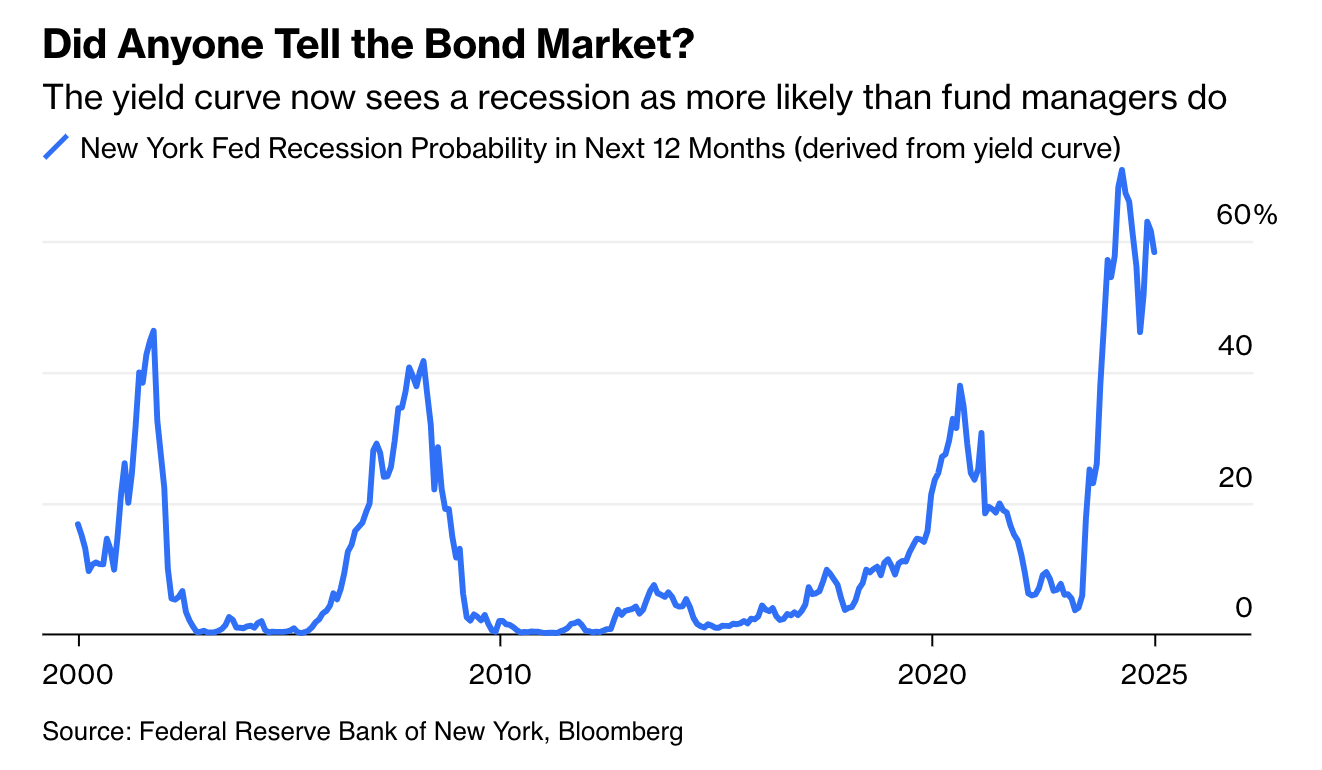

As it turns out, the bond market supports my thesis that everything is, in fact, not that great.

The New York Fed's recession indicator, which is based on the yield curve, shows a 60% recession probability.

Bloomberg

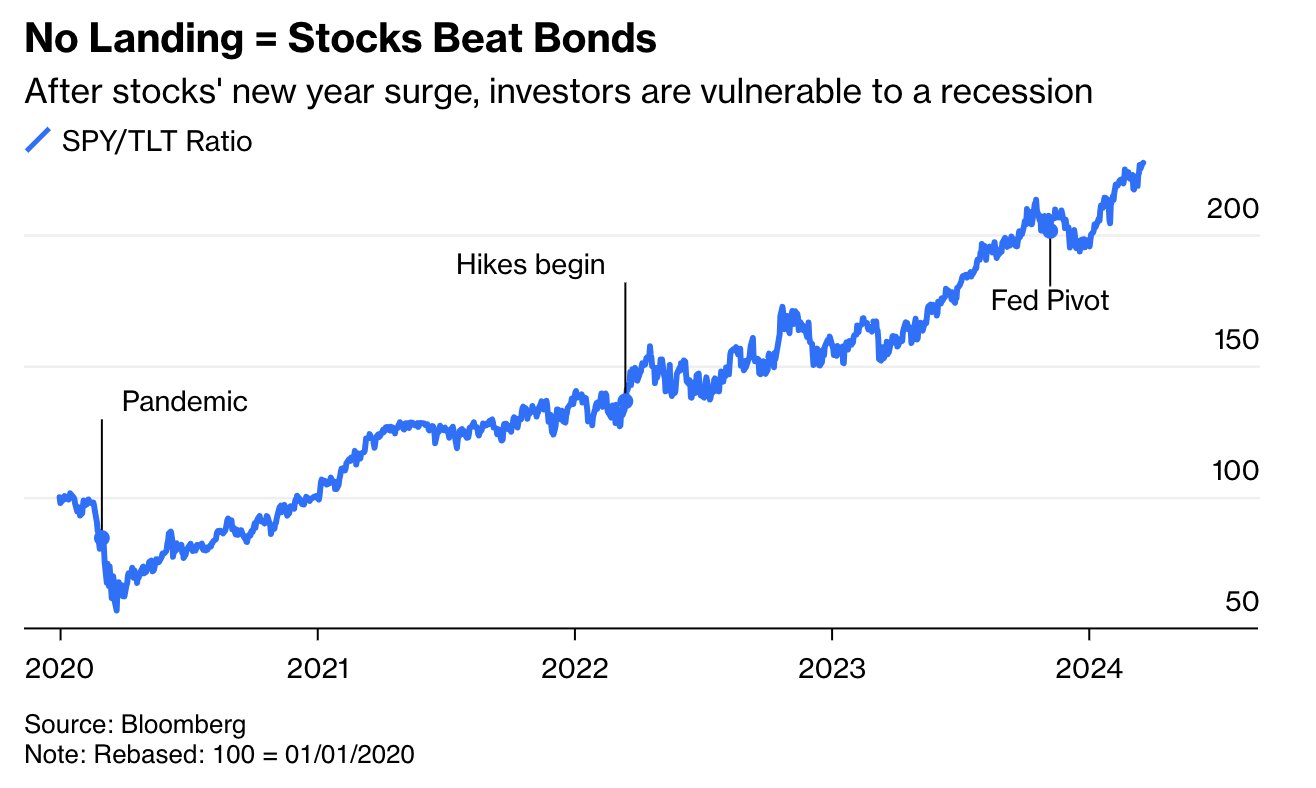

This means that the market is now betting that the bond market is wrong.

Or, to put it differently, the market is actively betting against a recession.

Don't get me wrong. I am not saying that a recession will happen. I am also not saying that stocks are wrong. Like everyone else, I cannot predict the future.

To me, it's all about the risk/reward.

Given the super strong relative performance of stocks compared to bonds (see the chart below), I believe we are in a situation where expectations are simply too upbeat to chase the market and high-flying stocks.

Bloomberg

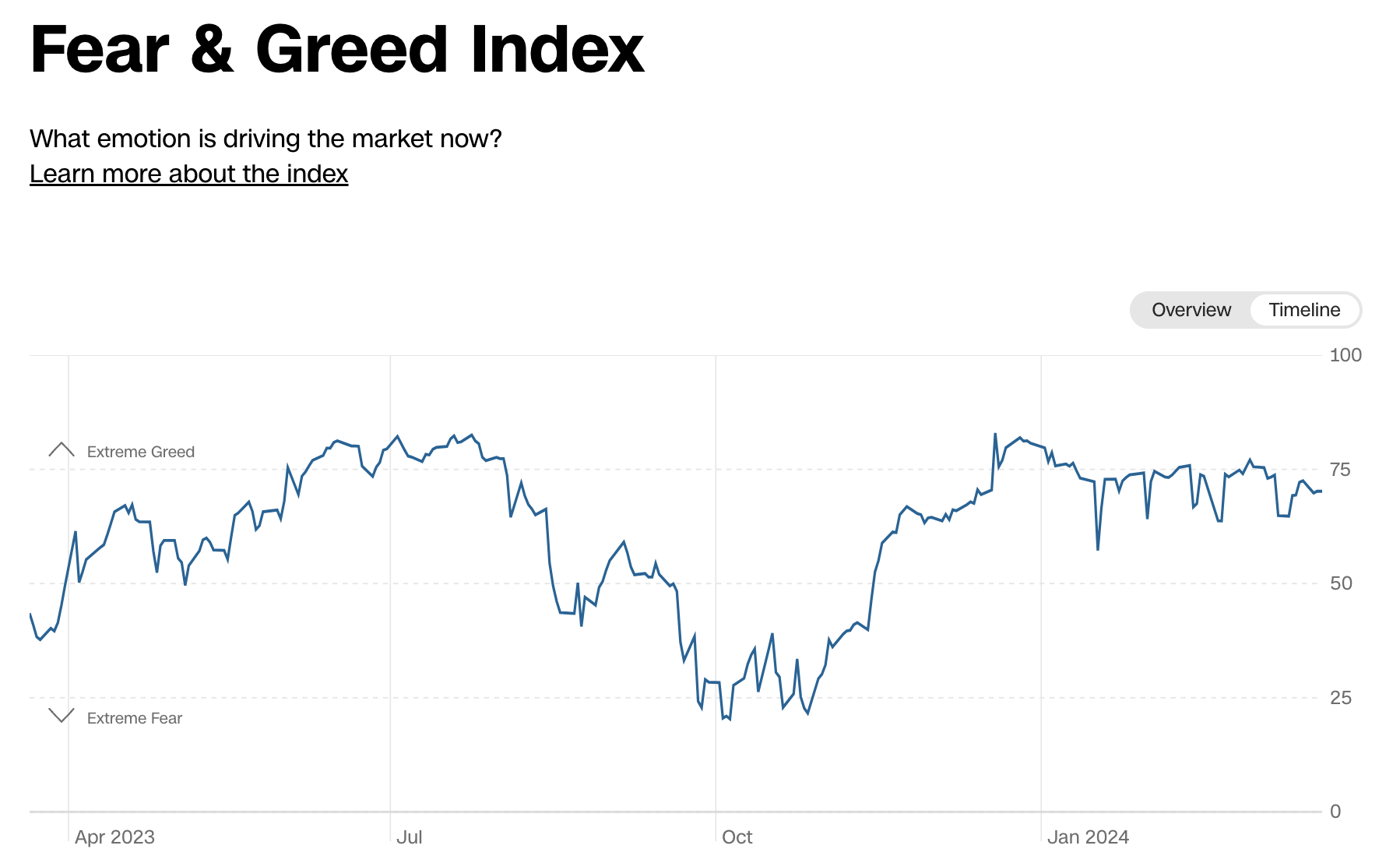

On top of that, the CNN Fear and Greed Index continues to indicate that sentiment is close to "extreme greed."

Usually, these periods last longer than one might expect. However, to me, it's a clear sign to be very careful when it comes to chasing hot stocks.

CNN Money

With that said, let's move over to the picks.

Generally speaking, I'm careful in this market. Although I have gradually reinvested my dividends and aggressively invested in oil and gas over the past few weeks, I try to keep an elevated cash position.

That's based on my view that market sentiment and valuations are too high. I also believe that the market is too dovish when it comes to inflation and interest rates.

However, if I had to buy stocks in this market, three fantastic companies come to mind.

This may be one of my all-time favorite REITs. A company I wanted to buy for many years. However, I never got the chance, as it always traded at prices I wasn't willing to pay - excluding the opportunities that I missed for various reasons.

Equity LifeStyle Properties has a very defensive business model, secular tailwinds, consistent dividend growth, and other benefits.

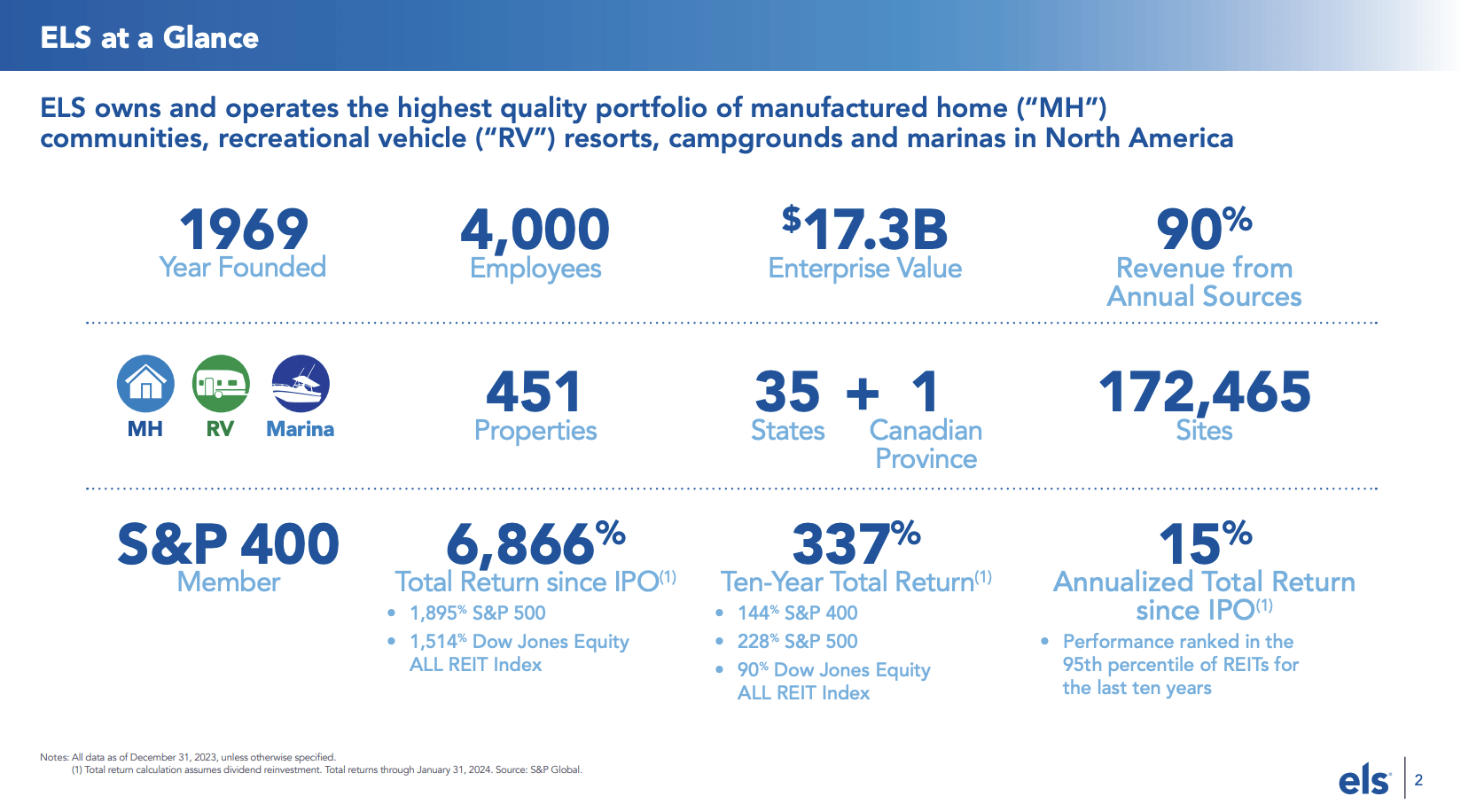

Founded in 1969, ELS is America's largest owner of manufactured housing ("MH"), RV communities, and marinas.

It operates more than 450 properties in 35 states and one Canadian Province.

These properties include more than 172,000 sites. Even better, 90% of total revenue comes from recurring annual sources.

Equity LifeStyle Properties

While this may be a boring business model - compared to fancy tech stocks - ELS has returned close to 340% in the ten years ending January 31, 2024. This has beaten the S&P 500 by more than 100 points!

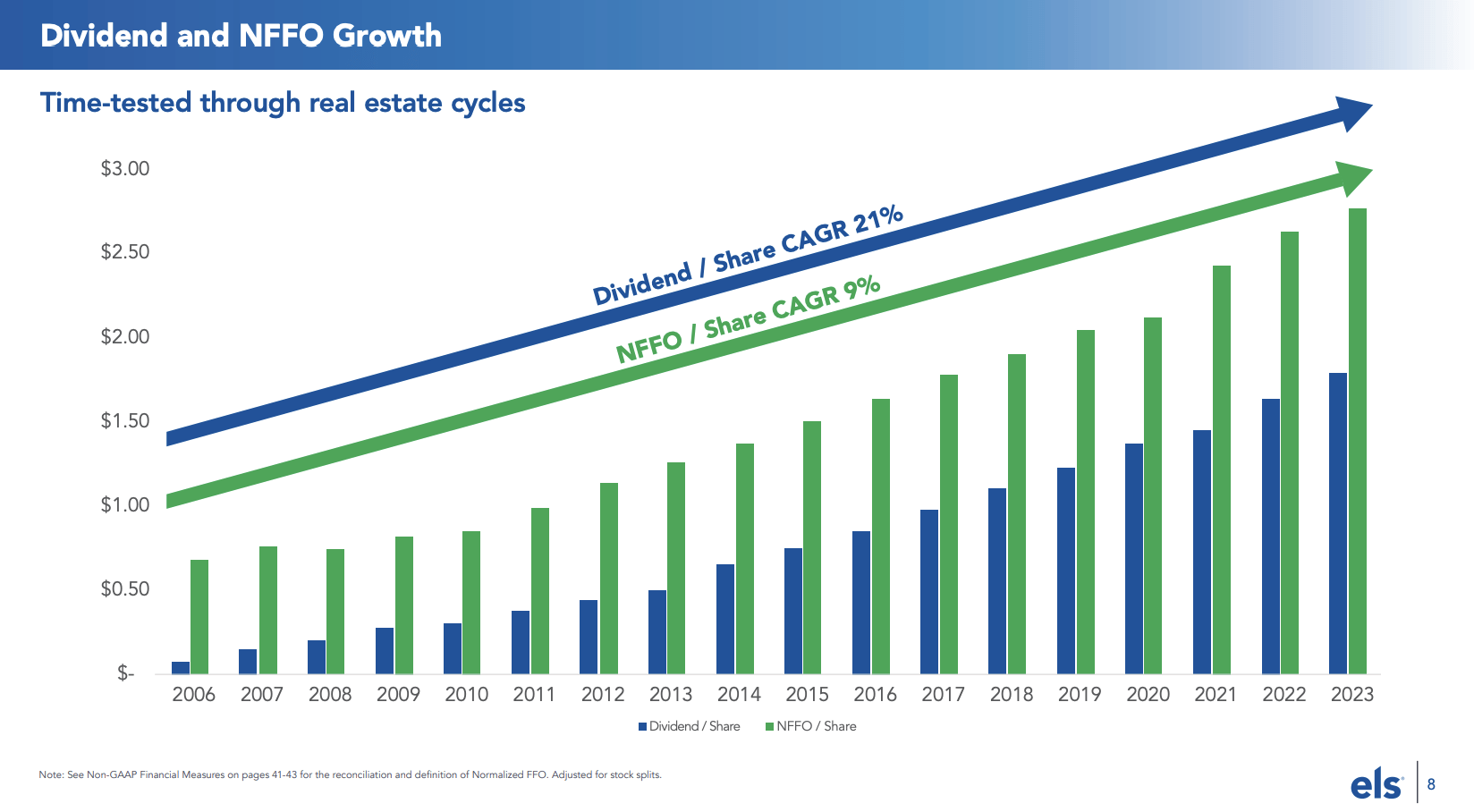

The company has compounded its dividend by 21% per year since 2006, supported by strong secular growth.

Equity LifeStyle Properties

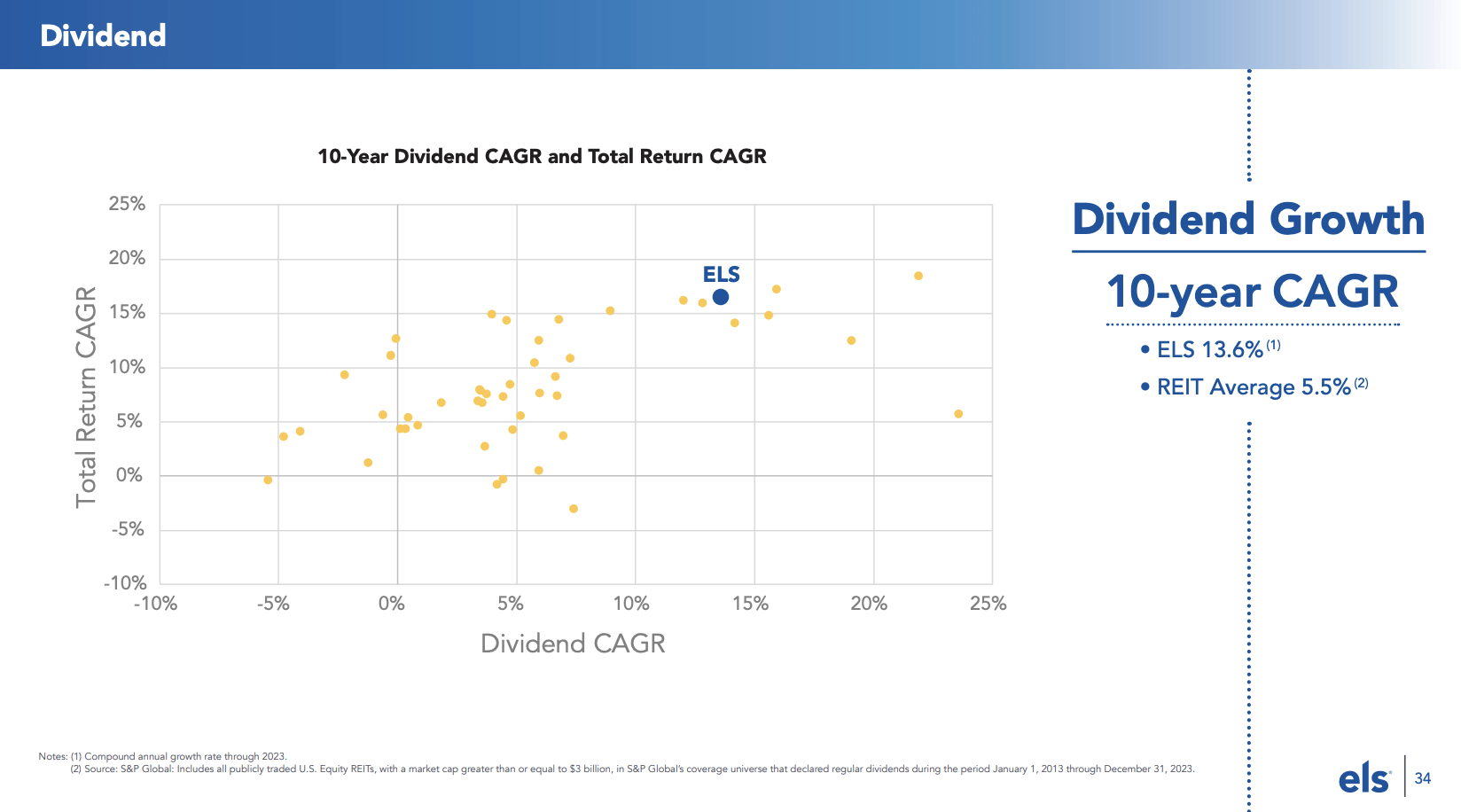

Over the past ten years, annual dividend growth has averaged 13.6%, which beats the REIT average by a wide margin.

The company currently yields 3%, protected by a 77% 2024E AFFO (adjusted funds from operations) payout ratio.

Equity LifeStyle Properties

The reason I liked ELS for many years is secular growth from two main drivers:

Equity LifeStyle Properties

It also has a healthy balance sheet, which matters a lot in this environment.

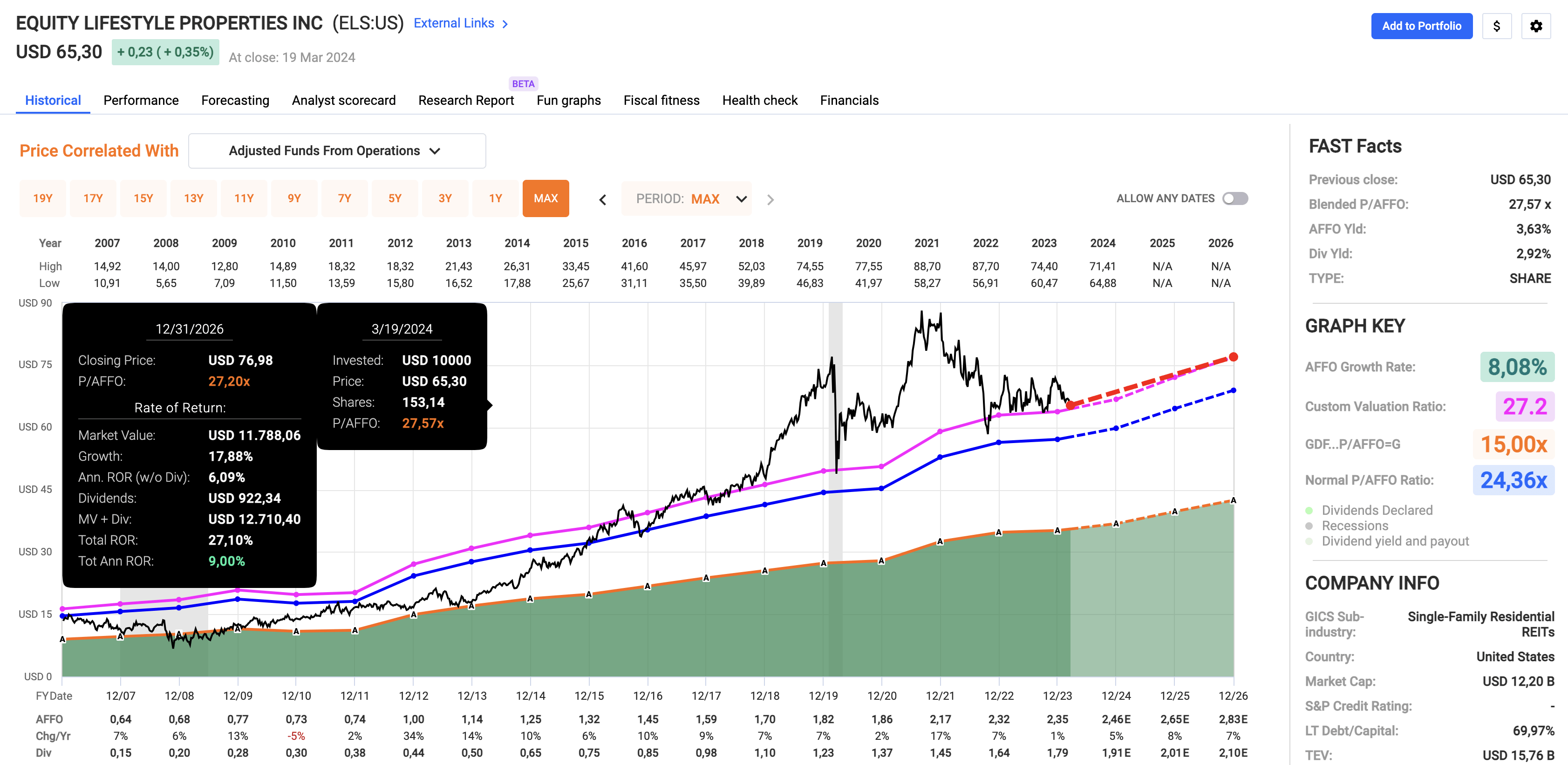

Valuation-wise, ELS is trading at a blended P/AFFO ratio of 27.7x. This is roughly in line with its 10-year normalized AFFO multiple of 27.2x (the pink line in the chart below).

FAST Graphs

This year, AFFO is expected to grow by 5%, potentially followed by 8% growth in 2025 and 7% growth in 2026.

Including its dividend, the 27.2x normalized AFFO multiple implies a 9% annual return through 2026.

Although this is purely theoretical, I believe ELS is attractively valued - especially compared to the broader market.

Hence, I view ELS as a Buy and hope to add it to my portfolio this year.

Unlike ELS, CME Group is a company I have owned for a while.

It's a company very close to my heart, as it has everything I'm looking for in a dividend (growth) stock.

The company operates some of the biggest exchanges in the world, including CME (where it gets its name), CBOT, NYMEX, and COMEX.

This means that whenever people trade S&P 500 futures, corn, soybeans, gold, copper, WTI crude oil, and various interest-rate futures or options, CME makes money.

Even better, because it has a fantastic business model in place and a stellar balance sheet with a double-A rating (one of the best ratings on the market), it distributes roughly 100% of its free cash flow to shareholders.

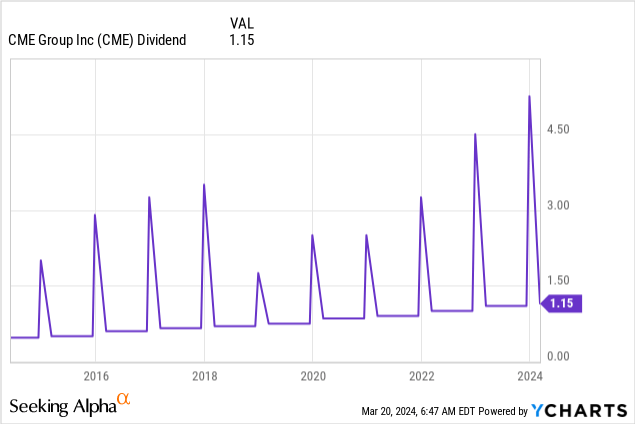

It usually pays four regular quarterly dividends and one special dividend in January.

Last year, the company paid $9.65 in total dividends. That's an annualized yield of 4.5% based on the current stock price.

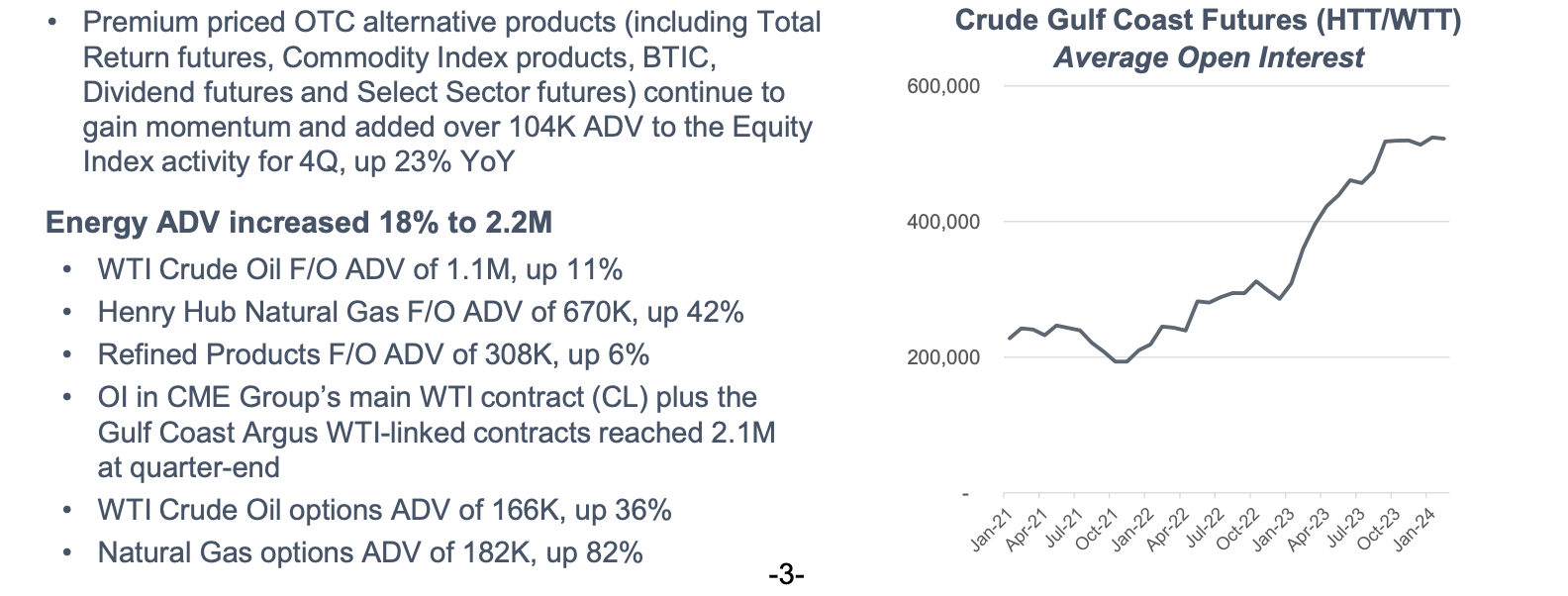

Moreover, this year, I expect the total dividend to come in even higher, as the company has tremendous success in bringing new products to market. It has the right future/derivative for every market segment, including metals, agriculture, indices, rates, crypto, and specialized contracts like Argus Gulf Coast contracts.

Especially energy contracts are doing very well, supported by geopolitical uncertainty.

CME Group

Moreover, because of CME's products, it benefits from volatility.

As a result, every "recent" recession has resulted in higher revenues!

While CME's stock price still suffers during sell-offs, investors usually hold stock in a rock-solid company that has bounced back rapidly after sell-offs, backed by secular growth and the benefits that come with elevated volatility.

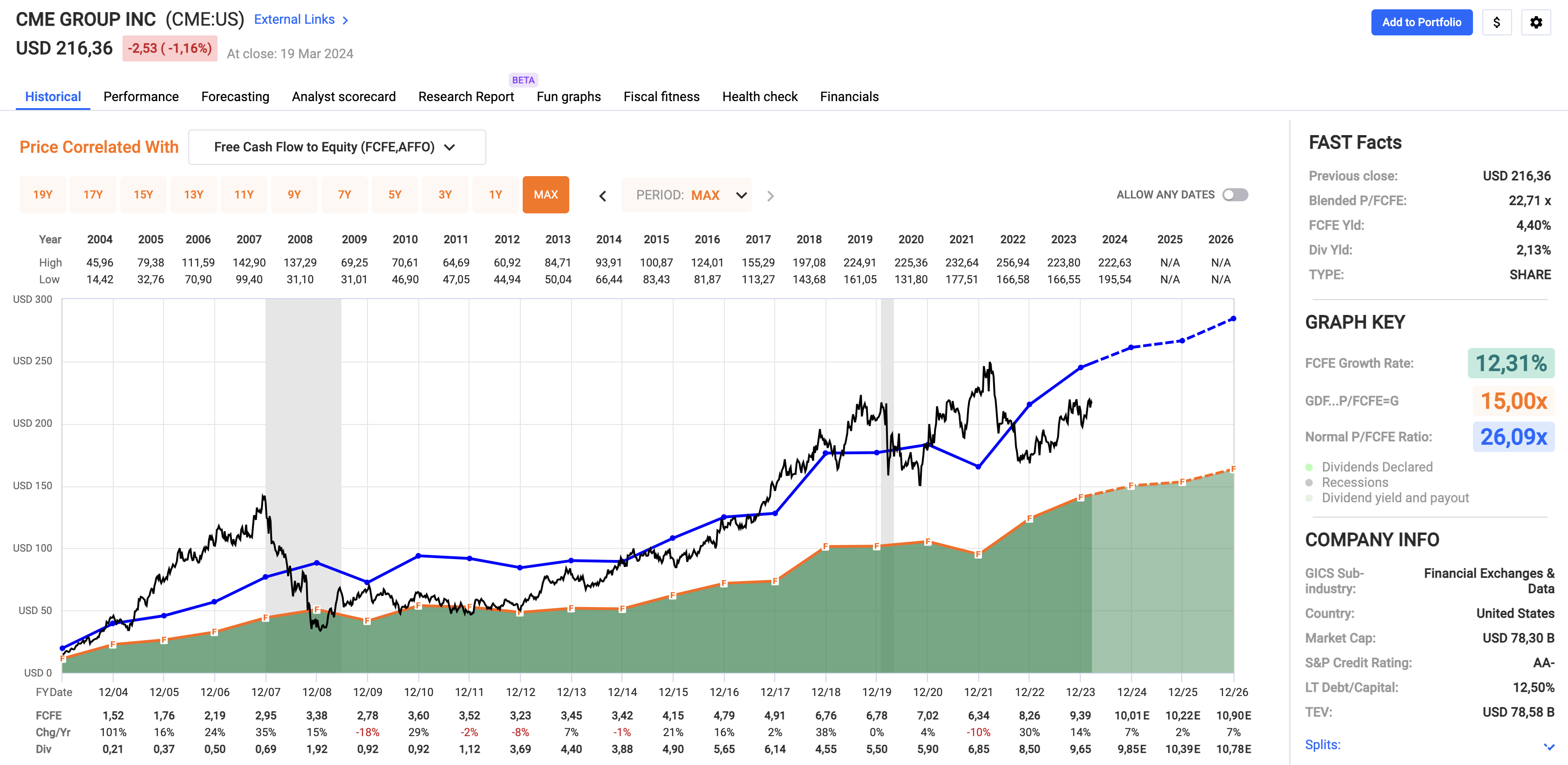

Valuation-wise, we're dealing with a stock that is trading at 22.7x FCFE (free cash flow to equity). That's below its normalized multiple of 26.1x.

FAST Graphs

The company is also expected to consistently grow per-share FCFE by 7% in 2024 and 2026 and 2% growth in 2025.

Needless to say, these numbers are subject to change.

Nonetheless, it's hard to not give the stock a fair stock price target of at least $284 based on these numbers. That's 32% above the current price.

Since 2004, CME has returned 15.5% per year, including its dividend.

Depending on my funds, I'm always looking to buy this one on weakness.

I started this year by throwing a lot of money at energy stocks.

Last year was all about defense contractors.

As a result, I have invested roughly a quarter of my entire net worth in defense contractors. One of my biggest positions is L3Harris Technologies, a stock I have liked since the 2019 merger between L3 and Harris.

My most recent article on this stock was written on February 11, when I explained why it's one of my favorite dividend growth stocks.

Unlike Lockheed Martin (LMT), LHX is not dependent on major programs like the F-35. While this jet is very important for LHX, it is a highly diversified supplier of everything related to defense aerospace.

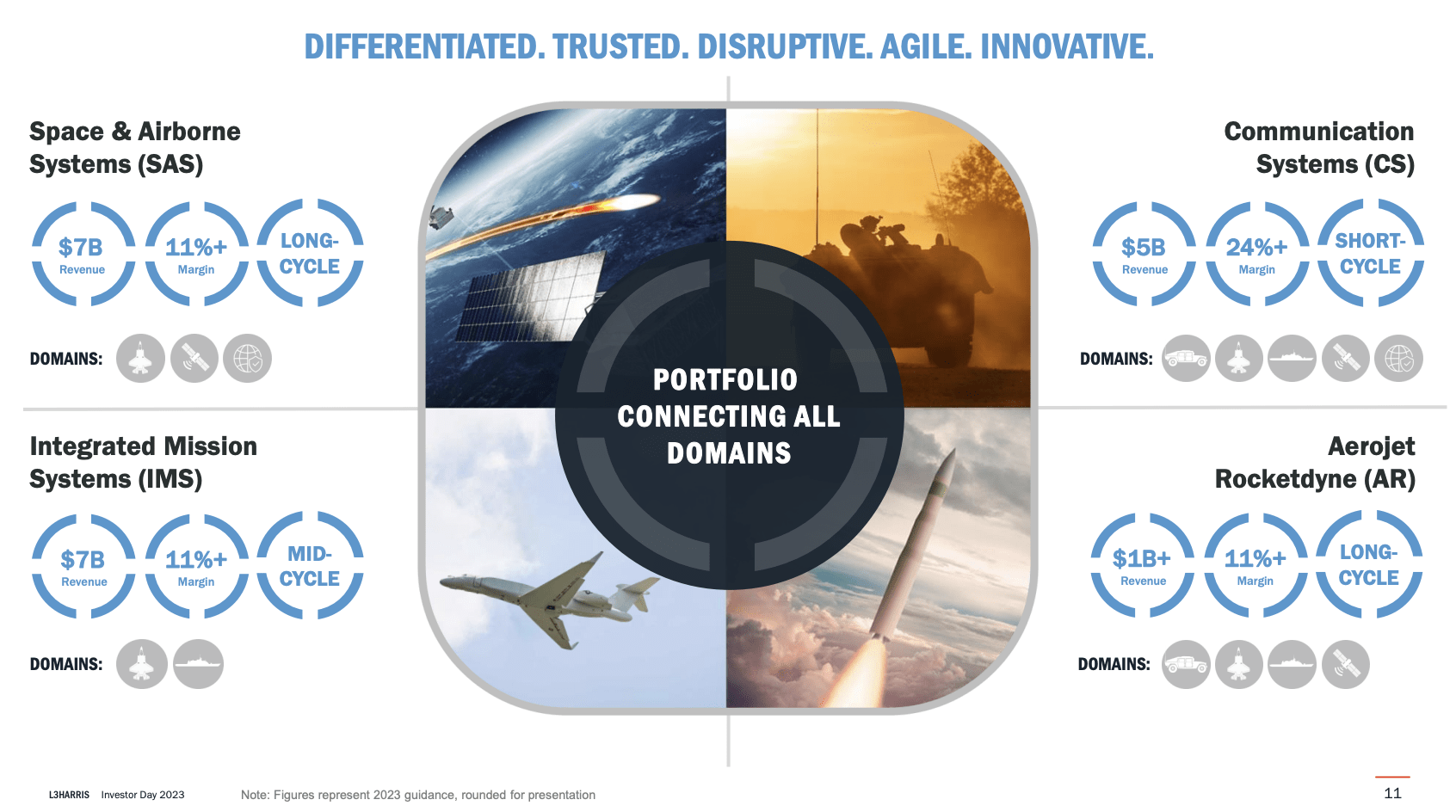

It has products in every major segment, including space, missiles, and communication.

L3Harris Technologies

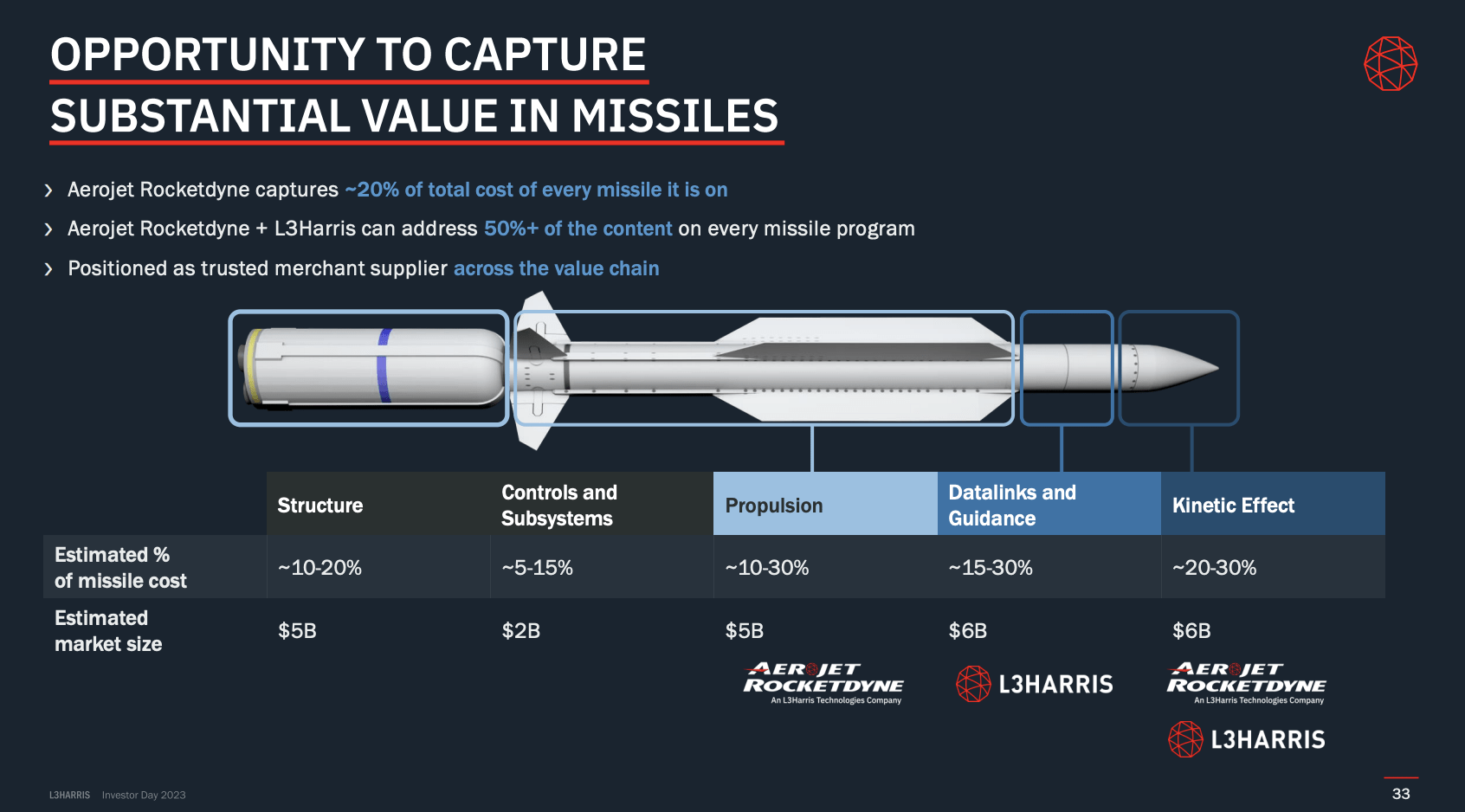

For example, after buying Aerojet Rocketdyne (one of my all-time favorite M&A deals), the company now has parts in 75% of all domestic missile programs!

L3Harris Technologies

The only reason why LHX is cheap is because it took on more debt to finance a number of M&A projects.

Moreover, like its peers, it suffered from supply chain issues and elevated inflation in certain areas.

It also did not help that Washington D.C. added a lot of budget uncertainty in recent years.

Now, LHX is in a great spot to boost growth, driven by elevated defense spending growth in NATO (ex-U.S.) nations who have some catching up to do, consistent growth in the U.S., secular growth in space operations, and merger synergies.

Moreover, the stock currently yields 2.2%. Dividend growth has fallen to the low-single-digit range. That's due to the company's focus on debt reduction.

The good news is that going forward, shareholders are in a fantastic spot to benefit from accelerating distributions.

This is what I wrote in my prior article:

That said, the good news is that LHX is very close to achieving its target leverage ratio.

Analysts expect the company to lower net debt to $11.3 billion at the end of 2024. This would translate to a net leverage ratio of 2.9x.

In other words, 2024 is likely the last year with subdued dividend growth and buybacks.

So, what does that mean for shareholders?

As the company expects to return 100% of its FCF to shareholders, there are many reasons to be upbeat about what may come in 2025.

Analysts expect the company to boost free cash flow from $2.0 billion in 2023 to $2.2 billion in 2024. This implies a 5.5% free cash flow yield, given its $40 billion market cap.

It also remains attractively valued.

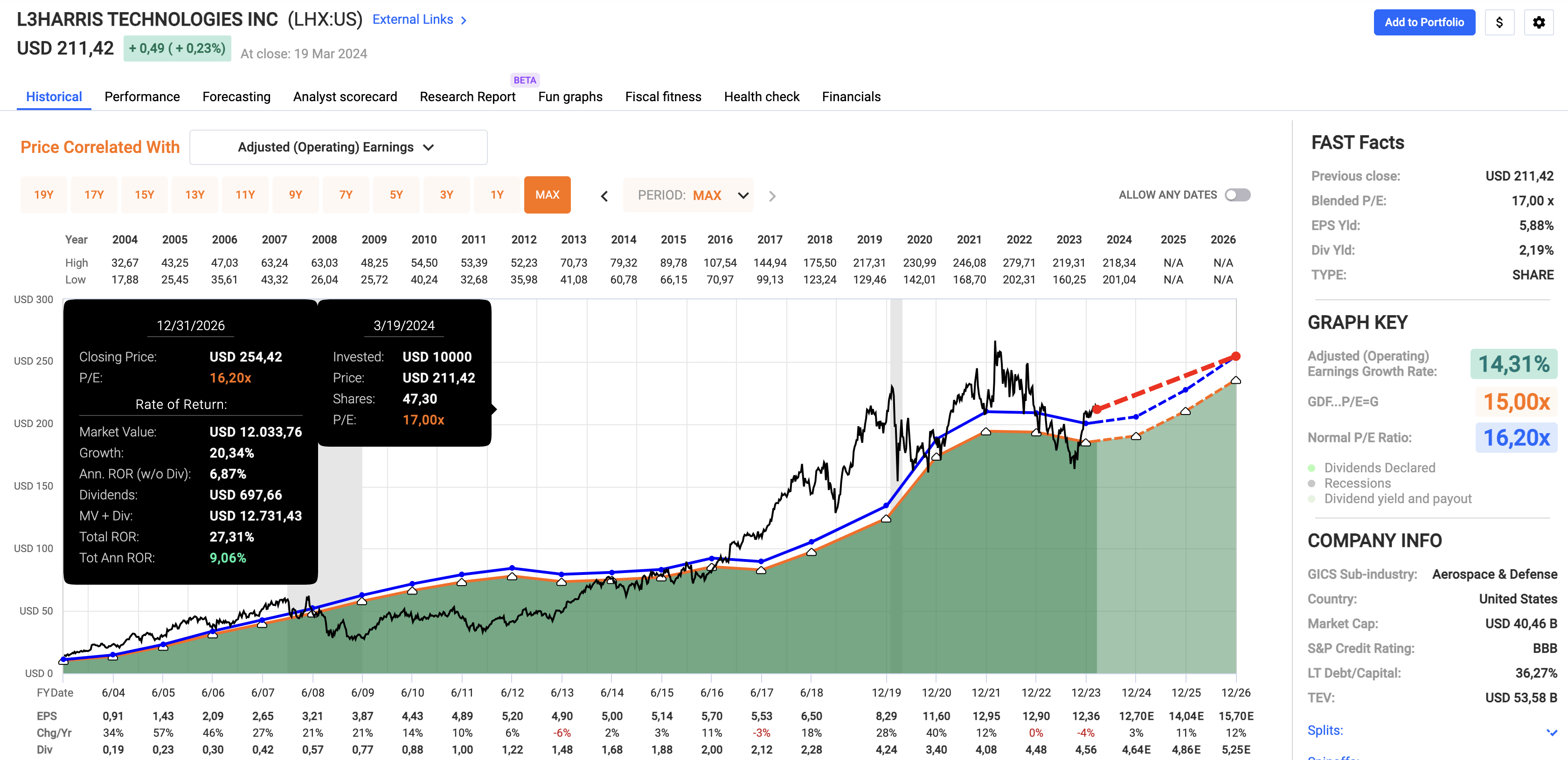

LHX trades at a blended P/E ratio of 17.0x. Its normalized P/E ratio is 16.2x.

FAST Graphs

Although it trades at a small premium, EPS growth is expected to accelerate.

This year, analysts are looking at 3% EPS growth, potentially followed by 11% growth in 2025 and 12% growth in 2026.

I expect these growth rates to persist, indicating a 10-12% annual return potential.

All things considered, given its valuation, anti-cyclical demand, shareholder distribution potential, and dominant position in the defense supply chain, I'm a buyer on any corrections.

The company is also a holding of all family accounts that I advise.

If we combine these three picks, we get a $30,000 portfolio consisting of three $10,000 investments.

However, before anyone makes the case that I'm wrong about the volatility profiles of these stocks, please be aware that we are comparing three stocks to a basket of 500 stocks.

Furthermore, the Sharpe Ratio of the $30,000 portfolio is 0.96. That's above the market's 0.67. This indicates a much more favorable risk/reward.

Even better, over the past five years, the portfolio's standard deviation has dropped to 17.9%. That's below the S&P 500 standard deviation of 18.4%.

While past performance does not guarantee anything, I am very upbeat about the likelihood that ELS, CME, and LHX will continue to beat the S&P 500, especially in light of the value they bring to the table in a time of uncertainty and a lofty valued stock market.

As we welcome spring, I'm reminded of the promising seasonal patterns in the stock market.

However, it's crucial to remain cautious amidst growing concerns of inflation and market valuation.

In light of challenges and opportunities, I've identified three robust stock picks: Equity LifeStyle Properties, CME Group, and L3Harris Technologies.

These companies offer stability, growth potential, and resilient business models in uncertain times.

By strategically diversifying investments and focusing on quality over hype, I aim to navigate the market's challenges and achieve long-term outperformance.

What do you think of my thesis? Please let me know in the comments down below!