sasha85ru/iStock via Getty Images

sasha85ru/iStock via Getty Images

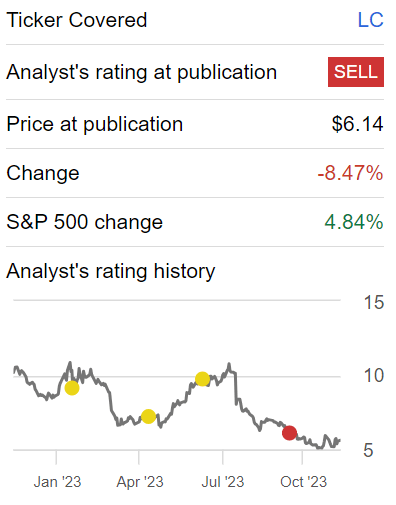

LendingClub Corporation's (NYSE:LC) Q3 results saw the company's key performance indicators continue to worsen. Notably, not only are its revenue growth rates leaving a lot to be desired, but more importantly, its Return on Asset metrics are clearly progressing in the wrong direction.

I remain steadfast in my stance that this stock should be avoided.

In my previous analysis prior to LendingClub's Q3 results, I said,

LC's revenue growth rates are on a downward trajectory, leaving investors to wonder when stability will return. Betting on a turnaround can be a daunting task, as it relies on mean reversion, which may take longer than investors are willing to wait.

Author's work on LC

In the ensuing months, the stock has continued to slide lower. I declare that investors should avoid buying the dip in this stock.

I'll first note some bullish aspects, before turning our focus to discuss bearish elements.

LendingClub used its earnings call to describe LendingClub's strategic response to the shifting investor landscape, particularly with bank investors temporarily on the sidelines.

The introduction of the structured certificates program, a two-tier private securitization, has proven successful, attracting strong interest and doubling in size from Q2 to Q3. This program provides a unique avenue for low-friction, low-cost financing for buyers, positioning LendingClub as a robust choice for marketplace investors.

Also, the company's focus on prime originations and the anticipation of a historic refinance opportunity in credit cards, coupled with innovations such as incorporating loan servicing into its banking mobile app and testing a line of credit products, underlines a proactive approach to meeting consumer needs.

Moving on, despite its optimistic prospects, LendingClub highlights a challenging investor side of the marketplace, with bank investors temporarily retreating to fortify capital and liquidity levels. This shift poses constraints on LendingClub's capacity to attract investment, particularly in the short term.

What's more, the reduction in headcount to align with market conditions and ongoing expense management efforts are indicative of the tough decisions required to maintain resilience in the face of dynamic challenges.

With that backdrop in mind, let's now turn to discuss its financials and outlook.

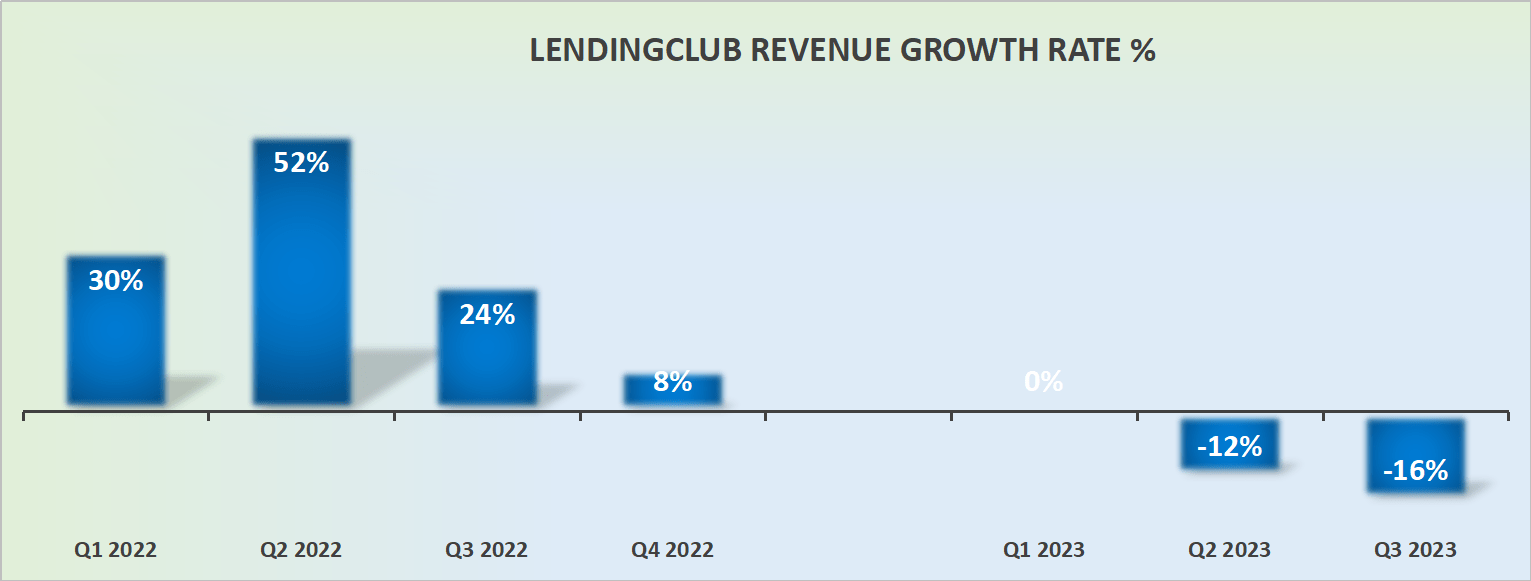

LC revenue growth rates

LendingClub's Q3 results saw its revenues shrink by 16% y/y. That being said, that was the last strong quarterly comparison revenue that LendingClub had to report against.

Not only will Q4 provide a much lower base to compare against the prior year, but the whole of 2024 will leave LendingClub with much easier comparable revenue growth rates.

Consequently, it's highly possible that without much progress, simply remaining with the revenue line at the present level, LendingClub will be able to deliver around 5% to 10% y/y revenue growth rates.

Given that backdrop, it's easy to imagine LendingClub's management team in 2024 will put out the narrative that its fundamentals prospects have improved and that the business has succeeded in striving for the right balance between growth and profitability, even though, I declare that this is mostly to do with the unimpressive and lackluster progress LendingClub has delivered this year.

SA premium

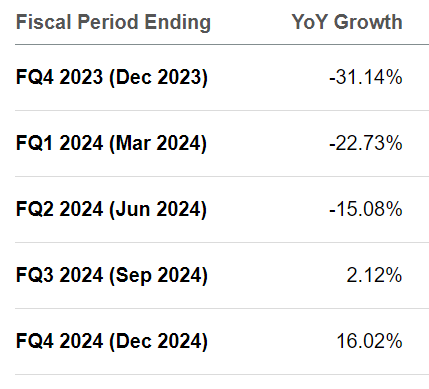

All that being, we should note that my estimates are meaningfully higher than what analysts presently expect to see LendingClub delivering. This means that if LendingClub does deliver 5% to 10% top-line growth next year, investors would be quick to salute. But is that enough to get investors to back this stock?

LC Q3 2023

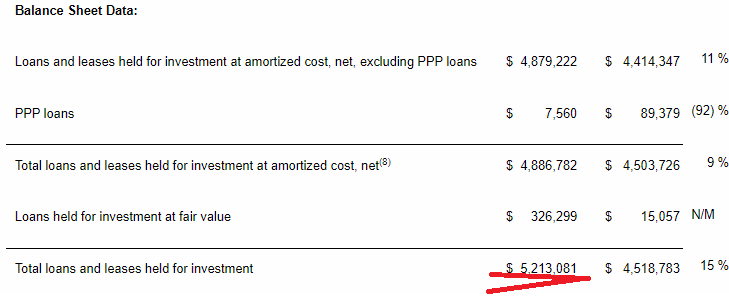

LendingClub's Q3 results show that the loans on its balance sheet have increased by 15% y/y, even though, as we've just discussed, its top line is shrinking.

For a bank, that's not a good position to be. You can see its poor fundamental performance reflected in its return on asset figures, below:

LC Q3 2023

For a bank, its ROA provides insight into the efficiency and profitability of a bank's operations. A declining ROA may signal that a bank is taking excessive risks with its assets, potentially leading to lower profitability or even losses.

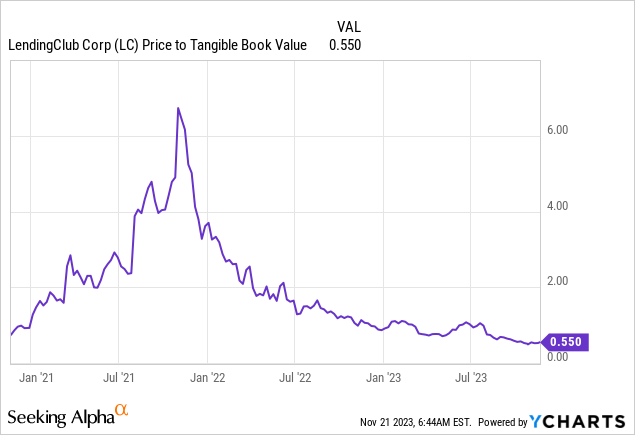

A few people reached out to me on the back of my previous analysis stating that I failed to understand just how undervalued the stock is right now. And yes, I'll admit that looking back there was a time when investors were more than willing to pay 2x LendingClub's tangible book value.

But the key aspect to keep in mind is that there's only value in this name if management can convincingly demonstrate that it's capable of growing its underlying prospects without having to overleverage its balance sheet.

And as we've discussed so far, that doesn't appear to be taking place.

In a comprehensive evaluation of LendingClub's recent performance and strategic outlook, it becomes increasingly apparent that caution is paramount for investors.

Despite the allure of an undervalued stock, the prevailing challenges, including declining key performance indicators, a questionable balance sheet, and uncertainties in the near-term prospects, underscore the inherent risks.

As the market adage warns, "cheap stocks can always get cheaper," prompting a resounding recommendation to avoid investment in LendingClub at this juncture.

The complexity of its current landscape and the ongoing struggle to demonstrate sustainable profitable growth calls for caution on this investment. Ultimately, I argue that there are better investments elsewhere than LendingClub Corporation stock.