grandriver/E+ via Getty Images

grandriver/E+ via Getty Images

Liberty Energy Inc. (NYSE:LBRT) is a founder-led company with a competitive service that should lead to cash flow and earnings growth. At only 6.7x fwd. P/E, LBRT is trading at quite an attractive valuation while executing value-add share buybacks. To make things better, it looks good on Seeking Alpha quant ranking with a buy rating and the company pays a dividend. With a respectable dividend yield of ~1%, I find LBRT to be a compelling investment opportunity.

This article explores why LBRT should merit consideration in an investment portfolio. The article will analyze the LBRT business model, balance sheet, ROIC (return on invested capital) profile, and other key factors that will drive an investment. The article will also review the risks involved in a potential investment in LBRT as well as provide an estimate of fair value for the company.

Long story short, I'm estimating the fair value of LBRT to be in the $28-$31 range, offering more than 40% return opportunity compared to where the shares currently trade. Without further ado, let's dive in.

Liberty Energy provides hydraulic and technology services to onshore oil and natural gas companies, mainly focusing on hydraulic fracturing (a.k.a. fracking) and complementary services. LBRT serves independent and integrated E&P (exploration and production) companies and operates in the most active shale basins in North America.

Company Presentation

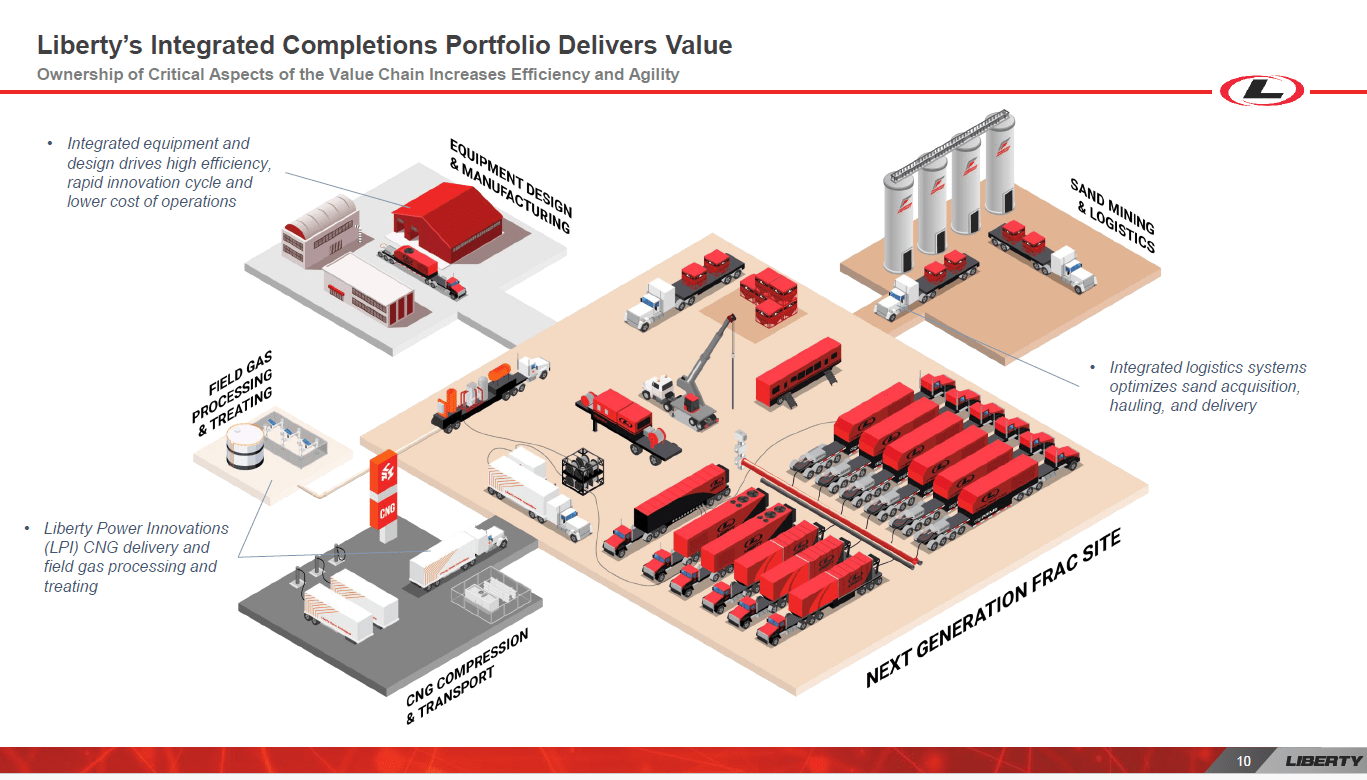

LBRT's competitive advantage are its fracking fleets. They operate more efficiently and produce less emissions than other fracking fleets. This is achieved by using fleets that are powered by natural gas, as opposed to Diesel. In addition, Liberty Energy's vertical integration strategy allows them to better serve E&P companies while reducing overall emissions.

Company Presentation

One of the compelling attributes of LBRT is that it's still run by its founder, which I generally view as a positive attribute when searching for an investment. Founders tend to act like owners, especially when they have significant ownership in the company's share (a.k.a. "skin in the game").

Chris Wright, the Chairman and CEO, owns ~1.8% of shares outstanding (approximately 3.2 million shares) as of proxy 2023. While he sold some shares during 2023, he still owns ~2.9 million shares, a stake worth ~$60 million. That's a good chunk of wealth tied to the stock and its performance, which should align him with other shareholders.

Insider ownership alone is not a good reason to be bullish. What's interesting and compelling about LBRT is that the CEO's incentives are designed to reward value creation for shareholders. After looking at the executive compensation package, the three key metrics that drive executive bonuses are:

Here's why these are good incentives that encourage value creation.

The adjusted pre-tax EPS provides a strong incentive to grow on a per-share basis, while the focus on ROCE provides an incentive to make smart capital allocation decisions. While the method of calculation for these numbers is a bit generous, it still provides enough incentives to create value for shareholders. For long-term incentives, comparative ROCE is the key metric.

Adjusted pre-tax EPS is calculated as Adjusted EBITDA minus D&A and interest expense, on a per share basis. ROCE is calculated as Adjusted EBITDA minus D&A, divided by Debt plus Equity employed. Their calculation is a bit generous because Adjusted EBITDA adds back stock-based compensation, fleet start-up cost, and transaction expenses.

As a final kicker, LBRT could be an M&A target. Before Liberty, Chris Wood founded a company called Pinnacle Technologies, which was ultimately sold to Halliburton (HAL) in 2008. It's hard to say if LBRT will have a similar exit, but the history is there.

One important reason to invest in LBRT is the ROIC (return on invested capital) profile it offers. LBRT has most of its capital invested is in fracking equipment and fracking fleets, while it generates returns from operating these fleets for customers.

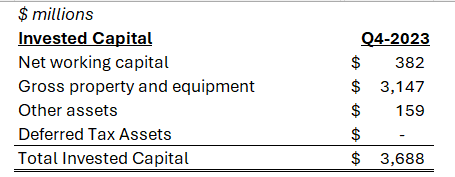

As I see it, invested capital base of LBRT is as follows:

Author Calculations

As mentioned earlier, LBRT's definition of return on invested capital is a bit too generous. My calculation is slightly different, as I'll be using NOPAT (net operating profit after tax) instead of Adjusted EBITDA.

NOPAT for LBRT is $576 million in 2023, derived from GAAP operating income of $761 million and a tax rate of 24%. Using NOPAT, the ROIC was a respectable 16.1% in 2023, a rate of return that should create value for the company. LBRT generates returns above its WACC and appears to be creating value in the process.

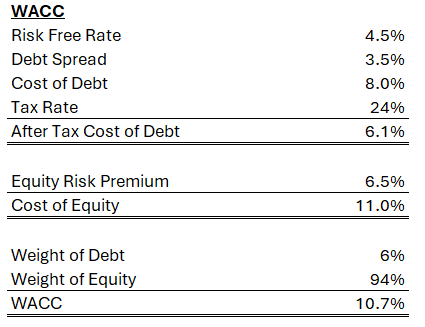

A fair cost of capital for LBRT is somewhere in the 10-11% range, with ~11% more likely to be a good return hurdle. I arrive at 10.7% return hurdle using the following inputs:

Author Calculations

In addition to its fracking fleets, Liberty Energy also has investments in start-up energy companies. These are smaller investments but may have potential to pay off big over the long run. Some of these investments are:

Overall, LBRT is still a fracking company with most assets tied to fracking fleets. That said, these venture capital-like investments in other energy companies not only demonstrates management forward-thinking mindset, but also provide a few call options on some cool technology. If any one of these companies turns into a home-run investment, these hidden assets could drive significant value in the future.

LBRT is conservatively capitalized with a strong balance sheet, which in turn limits the risk profile of the equity and provides some margin of safety. Lots of fracking companies have gone bust before. With a history of bankruptcies in this industry, having a strong balance sheet is critical.

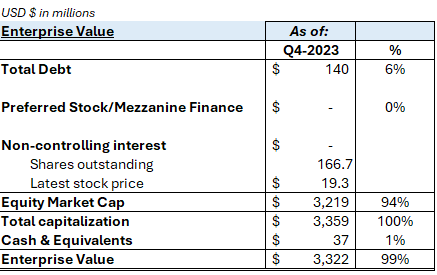

As of Q4-2023, LBRT total debt is $140 million, which is down from $223 million in Q3. Net debt is $103 million, which is low for a company with an enterprise value of about $3.3 billion. Debt makes up only 6% of the capital stack. With no preferred equity outstanding, common equity makes up the remaining 94%. The capital structure is shown below.

Company Filings; Author Calculations

With Net Debt to EBITDA ratio at only 0.1x, the balance sheet gives LBRT flexibility to return capital to shareholders through dividends and buybacks, as the balance sheet is not burdened by a big debt load.

LBRT will continue to invest in the business to capture demand for low-emission fracking solutions. LBRT has been investing in vertical integration of its operations, as well as differentiated technology to maintain a strong product. As explained above, these investments are generating ROIC of ~16%, which is quite attractive.

Stock buybacks are a priority for LBRT, which should create value as the stock trades at an attractive valuation (more on valuation later). LBRT repurchased ~12% of shares outstanding since starting the buyback program, as the executive team believes the shares are below intrinsic value. LBRT does not disclose their internal view of intrinsic value.

My estimate of intrinsic value is well above the stock price, so stock buybacks should be a good use of capital. In addition to buybacks, it is important to note that LBRT just increased its dividend by 40% in the last quarter.

My valuation analysis will focus on how the stock trades on a multiple of free cash flow and earnings, as well as attempting to determine intrinsic value in perpetuity. LBRT currently trades at compelling valuation.

In 2023, LBRT produced ~$411 million in free cash flow. The executive team expects 2024 to be another strong year of free cash flow generation.

On an EV/FCF basis, using the EV laid out above, LBRT trades at 8.1x TTM free cash flow, or free cash flow yield of about 12%. This is why buybacks are a great use of capital, as the company can retire shares at higher yields than its cost of capital.

Consensus EPS estimates for 2024 and 2025 are $2.90 and $3.22, respectively. For reference, LBRT reported EPS of $3.15 in 2023.

At the current stock price, P/E ratio is only 6.7x for 2024 and 6.0x for 2025. Those ratios look too low for a company generating excess returns above its cost of capital. For reference, the S&P 500 trailing P/E ratio is about 22x.

Mr. Market is basically saying LBRT is worth a much lower multiple than the S&P500. While I would generally agree with that, I view 6x P/E as too low.

I think a fairer multiple for LBRT should be closer to 9x given its cost of capital and risk profile. Using a normalized EPS estimate of $3.10 and applying a 9x fair multiple, fair value for LBRT should be closer to $28.

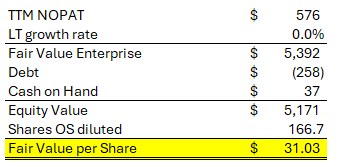

Another way to think about valuation for LBRT is capitalizing the NOPAT into perpetuity. Taking NOPAT of $576 million at zero growth, then applying a WACC of 10.7% as the return hurdle, intrinsic value for the enterprise is ~$5.3 billion. Subtracting debt and tax liability, while adding cash gets to an equity value of $5.2 billion, or per share value of ~$31.

Author Calculations

Investing in any equity is risky, and LBRT is no different. Below are some of the biggest risks I see in LBRT.

Oil prices and natural gas prices are key factors driving demand for LBRT services, and thus driving revenues and profits. Oil prices have been relatively stable over the past year, with a high of ~$94 and a low of ~$67. Over the past 5 years, oil prices have been quite volatile, with a high of $119 and a low of $21. Natural Gas prices have ranged from $3.86 to $1.85 over the past year and are currently trading at 1-year low. It is extremely difficult to predict these commodity prices, and this is most likely a key reason for the lower P/E multiple Mr. Market ascribes to LBRT.

E&P companies' willingness to spend on low emissions. LBRT provides oilfield services to some of the largest E&P companies. As such, LBRT is sensitive to the spending plans of E&P companies. While it seems like every company is now looking at lowering overall emissions, it is no guarantee this trend will continue.

The tax receivable agreement. LBRT has an agreement to pass through some tax benefits to previous owners of the business (before the IPO), which creates a liability on the balance sheet. While this liability does not look high at $118 million, it is uncertain how it may change. The calculation of intrinsic value is reduced by this liability.

Government regulation is also an important risk. Fracking is not an environmentally friendly activity, and the government can impose higher taxes and/or higher burdens for companies in this business. Climate change is real. Although LBRT seems to be focused on lowering emissions, it still supports oil and gas companies, which are not necessarily environmentally friendly companies.

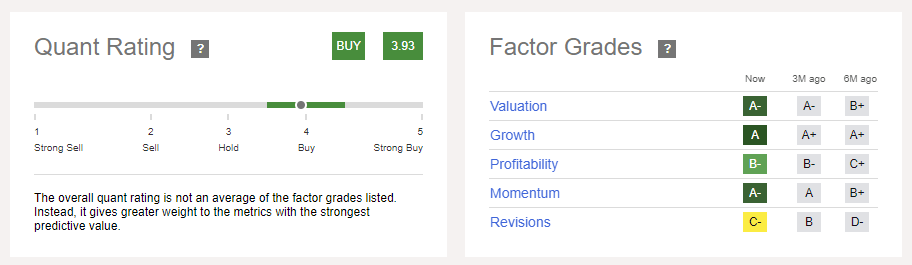

LBRT currently has a buy rating on Seeking Alpha's quant rating, which adds a nice validation to the fundamental analysis discussed above. As of this writing, Seeking Alpha gives LBRT a 3.93 score, with the best marks on valuation, growth, profitability, and momentum.

Seeking Alpha

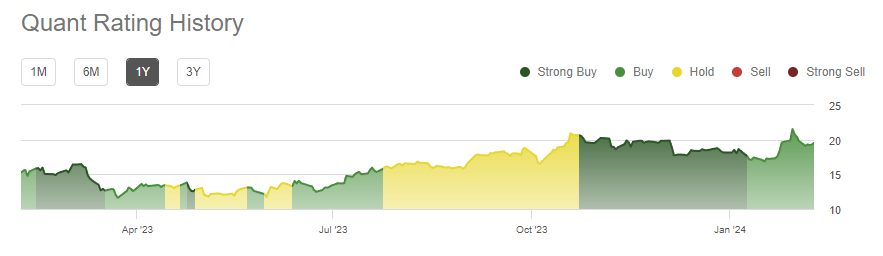

Historically, LBRT has not always been a buy rating on Seeking Alpha's quant rating. But I would note that it had the same buy rating around June 2023, when the stock was trading in the $12 to $13 range. Since then, the stock has performed quite well, rising all the way up to $21 by January 2024.

I find the setup today is similar to that in June, with the biggest question mark is where the stock will be 6 months or 1 year from now. My bet? The stock will be higher.

Seeking Alpha

LBRT looks like a compelling investment for the next 2-3 years, perhaps longer. The growth outlook for the business isn't extraordinary, but the balance sheet is rock solid and valuation is highly compelling. In addition, the company is run by founders who are highly incentivized to create value for shareholders.

LBRT is trading at ~8x trailing FCF, or ~12% free cash flow yield, which is a compelling valuation for a business that generates ROIC of ~16%. On a P/E basis, LBRT is trading at only 6.7x 2024 EPS, much lower than the S&P 500 P/E of 22x.

My fair value estimate for LBRT is in the $28 to $31 range, and with the stock trading at $19.5 as of this writing, the return potential looks compelling at 44% to 59% from stock price only. And there is an additional 1% coming from the dividend, which was just raised by 40% in the last quarter.