Lakeland Bancorp Inc (LBAI) Reports Decline in Net Income and Earnings Per Share for Q4 and ...

-

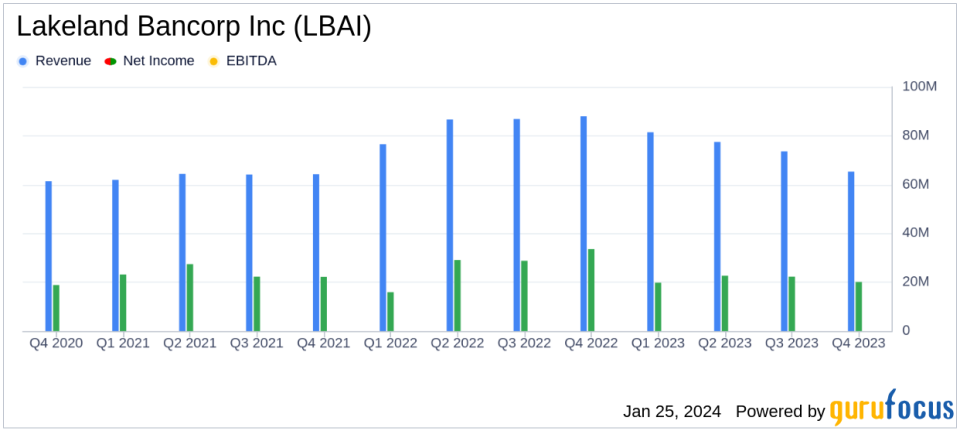

Net Income: Q4 net income decreased to $20.1 million from $33.6 million in Q4 2022; Full-year net income fell by 21% to $84.7 million.

-

Earnings Per Share (EPS): Diluted EPS for Q4 dropped to $0.30 from $0.51 in the prior year's quarter; Full-year diluted EPS declined to $1.29 from $1.63.

-

Net Interest Income: Q4 net interest income decreased by 20% to $65.3 million; Full-year net interest income decreased by 10% to $281.7 million.

-

Net Interest Margin: Q4 net interest margin fell to 2.52% from 3.28% in Q4 2022; Full-year net interest margin decreased by 47 basis points to 2.77%.

-

Noninterest Income: Decreased by $237,000 to $6.8 million in Q4; Full-year noninterest income decreased by $3.0 million to $25.1 million.

-

Asset Quality: Non-performing assets increased to 0.23% of total assets, compared to 0.16% at the end of 2022.

-

Merger Update: Merger deadline with Provident Financial Services, Inc. extended to March 31, 2024, to obtain necessary regulatory approvals.

Lakeland Bancorp Inc (NASDAQ:LBAI) released its 8-K filing on January 25, 2024, detailing its financial performance for the fourth quarter and full year ended December 31, 2023. The bank holding company, which offers a range of banking and investment services through its offices in New Jersey and New York, faced a challenging economic environment in 2023, impacting its financial results.

Performance and Challenges

LBAI reported a decrease in net income and EPS for both the fourth quarter and the full year of 2023. The company's President and CEO, Thomas Shara, acknowledged the economic challenges but highlighted a 6% loan growth and excellent asset quality, with negligible loan charge-offs for the year. The resilience of the deposit base during the banking crisis was also noted as a positive sign of the company's core deposit customer focus.

Financial Achievements and Industry Significance

The growth in loans, particularly in commercial real estate and residential mortgages, is a significant achievement for LBAI, reflecting the company's ability to expand its lending portfolio despite economic headwinds. This growth is crucial for banks as it drives interest income, which is a primary revenue source for the industry.

Income Statement and Balance Sheet Summary

The decrease in net interest income for both the quarter and the year was attributed to a decline in net interest margin, primarily due to increased market rates and customer shifts from lower-rate transaction accounts to higher-rate time deposits. The provision for credit losses also increased, reflecting a more cautious outlook on loan repayments amid economic uncertainty.