Clara Bastian

Clara Bastian

Back in college, I was enrolled in the Reserve Officers' Training Corps, or ROTC. It's a great program that offers basic military training and leadership skills.

That and marching. Lots and lots of marching.

In order to march properly. And, yes, there's a right and a wrong way to do so - you have to have the right rhythm in your head. That's why we used military cadences like this one to keep a uniform (and uniformed) beat:

Calling all the cows down to the farm

Calling all the cows to the barn

We'll have a little butter, and we'll have a little cream

We'll have a little milk and a little margarine.

How did those lyrics come to be? I guess a former farmer thought it up since most of us don't spend much time thinking about cows.

Though maybe we should.

According to Drink-Milk.com, they can have it made in the shade. They're "habitual animals" that "thrive on routines." This is why "dairy farmers work hard to make sure their cows" have predictable schedules.

5:00 a.m. is morning milking, which takes less than 10 minutes per cow, it turns out. Two hours later, they have their first feeding time, and two hours after that, they're busy "relaxing in the barn."

Those barns, it should be noted, are constructed and kept just so. These critters are pampered at every turn.

It'd be nice to get even half the consideration they do. Wouldn't it?

Brad Tomas (ROTC)

Once again relying on Drink-Milk.com, we learn that dairy cows:

I'm sure there are some minute-to-minute deviations, but dairy farmers work hard to keep those hourly schedules. Winter, spring, summer, or fall. Rain or shine. Weekdays or weekends. Sick or healthy.

These men and women get up every day to make it happen for their animals so their animals can make it happen for them. It doesn't sound like an easy life. But all of us lactose-tolerant individuals who love our non-black coffee, our milkshakes and ice cream, our cheeseburgers, yogurts, and/or cereals thank them for their efforts.

Or at least, we really, really should. Again, I know most of us probably take them for granted, if we're going to be perfectly honest.

This again, isn't that the beauty of modern life? We pay for goods that we can't make or don't want to make. Learning about the process behind them might be interesting - as evidenced by successful shows like "How It's Made," which ran from 2001 to 2019.

Its first episode explored aluminum foil production, snowboards, contact lenses, and bread. Its second highlighted compact discs, mozzarella cheese, pantyhoses, and fluorescent tubes. And its third studied toothpicks, acrylic bathtubs, helicopters, and beer.

Really neat stuff!

But overall, we want to have our products and use them with as little hassle as possible. We want it and we get it with an admitted increased amount of money down.

All of which makes me wonder why we don't expect the same thing from investing.

Let me clarify that when I say "we don't expect" ease and reliability from our investments, I don't mean me.

I actually very much expect steady "production" from the assets I hold in my portfolio. That's why, as I explained in a recent article, I only check them once a week on average.

Oh, I do my research on these companies to begin with. And I stay on top of their reports.

As a result, I'm confident my money will appreciate, both in long-term stock price and faithful dividend payments. There are very few surprises along the way, especially with my prized real estate investment trusts, or REITs.

Having been on the other side of the commercial real estate equation as a developer and landlord, I can tell you how much more relaxing it is to pay people to run the show. I get to sit back and watch while someone else grows my money.

Sometimes rather literally, as is the case with farming REITs.

That's why I brought up cows before. Because I've got my money-focused mind on food production at its most basic.

Admittedly, neither of the two publicly traded U.S. farming REITs concentrate on cows. One of them is heavily involved in traditional grains, the other is much more fruit and nut intensive.

I also should point out that they don't actually run these farms. They own the properties and then rent them out to people who will work the land.

Yet, this is still an intensely important part of the food production process. Farming is an expensive and involved business to be in, and REITs can give them infusions of cash that help them survive and thrive.

And, in the process, they offer reliable dividend payments I don't want to overlook.

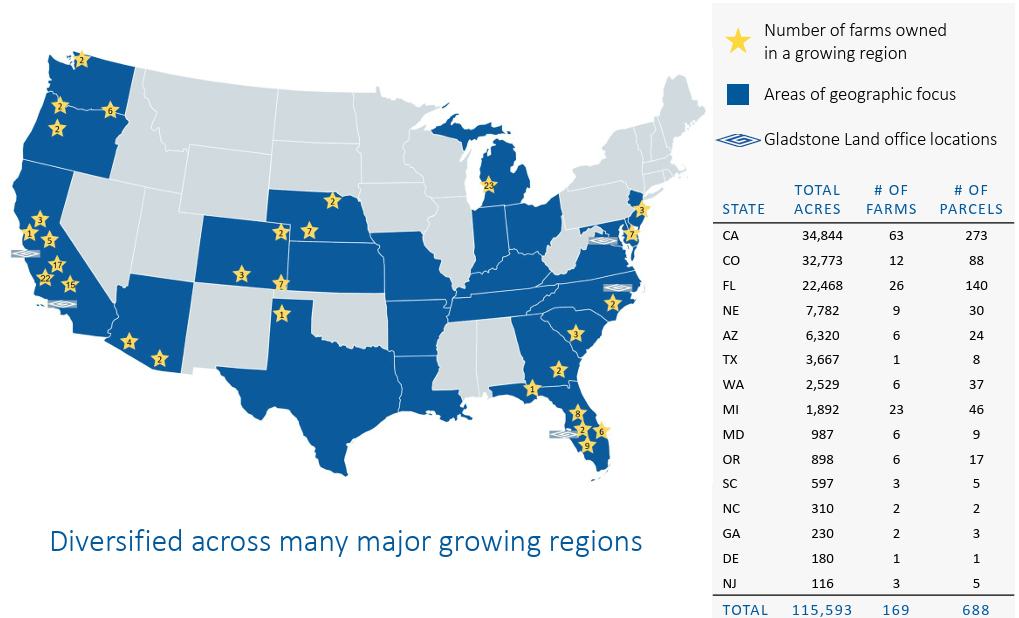

LAND is an externally managed (one of four public companies managed by the advisor) farming REIT that owns 169 farms with approximately 116,000 total acres in 15 states and more than 45,000 acre-feet of banked water in California, valued at approximately $1.6 billion.

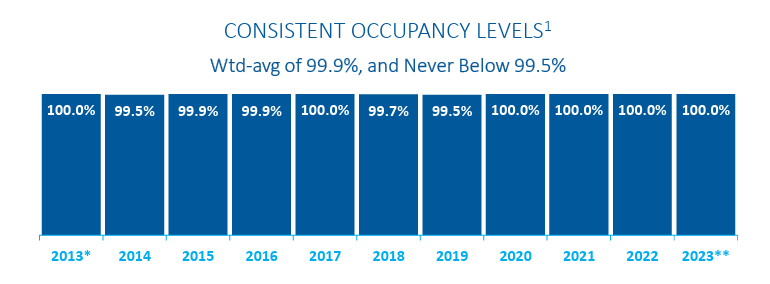

LAND's acreage is currently 99.9% leased.

LAND IR

One key differentiator for LAND (vs. the peer we will discuss next) is that the REIT focuses on acquiring annual fresh produce (most fruits and vegetables) and certain permanent crops (blueberries, nuts, etc.).

In some ways, specialty crops are superior to commodity crops (i.e. corn, wheat, and soy) due to higher profitability and rental income (200 to 300 bps higher cap rates for specialty crops vs. row crops).

Also, specialty crops generate higher rental income, they have lower price volatility, and they're less reliant on the government. That means the real estate is typically closer to major urban areas, which means they have much higher development potential (i.e. the "incubator" effect).

LAND IR

LAND's capital structure consists of fixed-rate debt ($562 million), term preferred stock ($57.4 million), preferred equity ($297 million), and common stock ($510 million).

As of Q4-23, total liquidity was over $200 million (including $60 million in cash). In addition, LAND has over $130 million of unpledged properties.

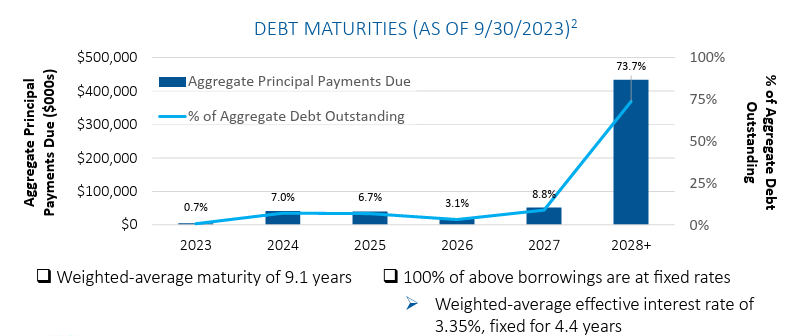

The fixed rate loans have a weighted average rate of 3.34% and a term of 4.2 years. Regarding upcoming debt maturities, LAND has about $35 million coming due over the next 12 months.

LAND IR

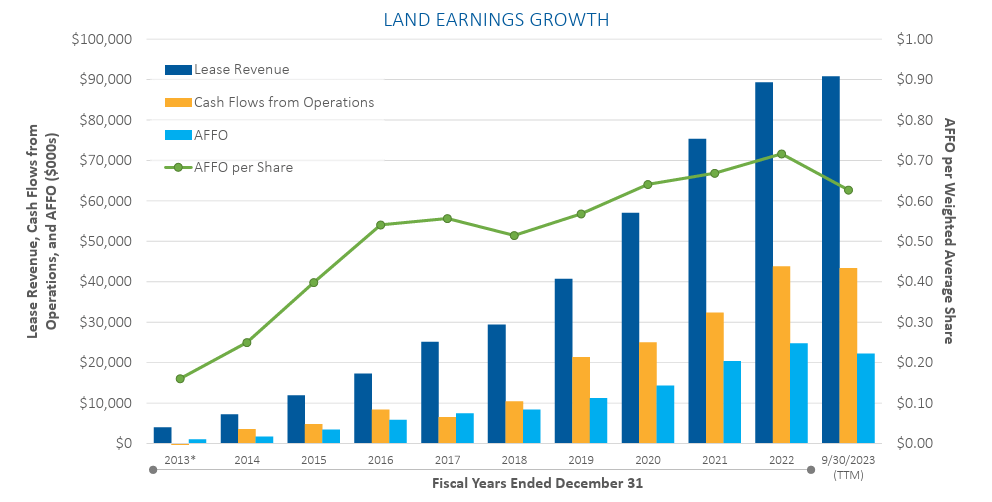

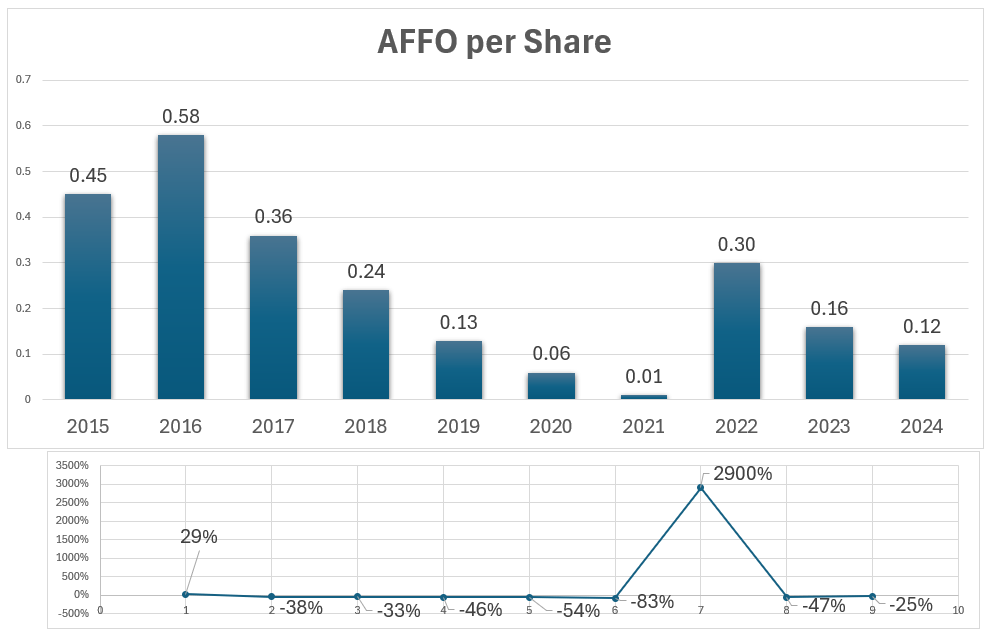

LAND has maintained consistent revenue and earnings as shown below. However, there has been modest growth (just 2.2% CAGR AFFO per share growth and 1.1% CAGR dividend growth over the last seven years).

LAND IR

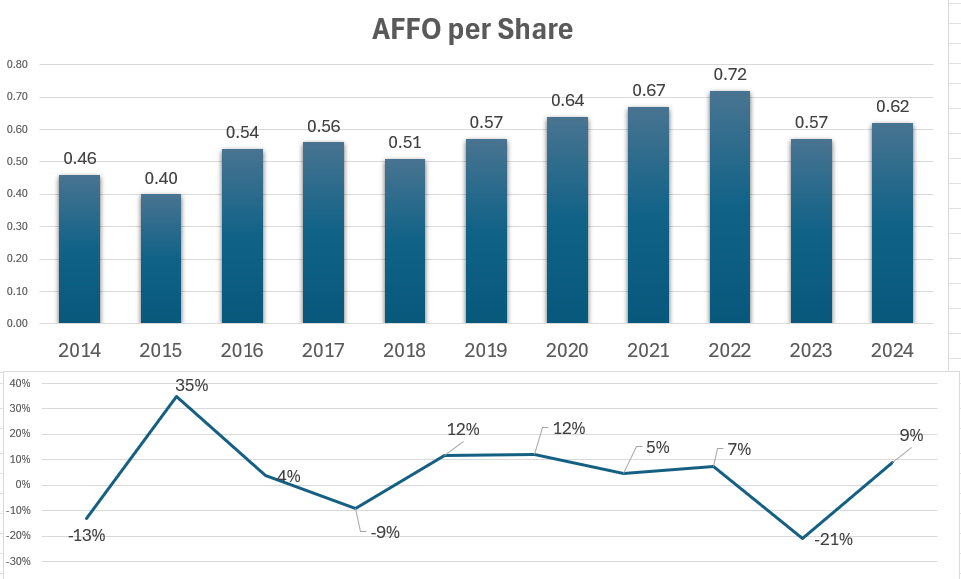

Here's a better representation:

iREIT®

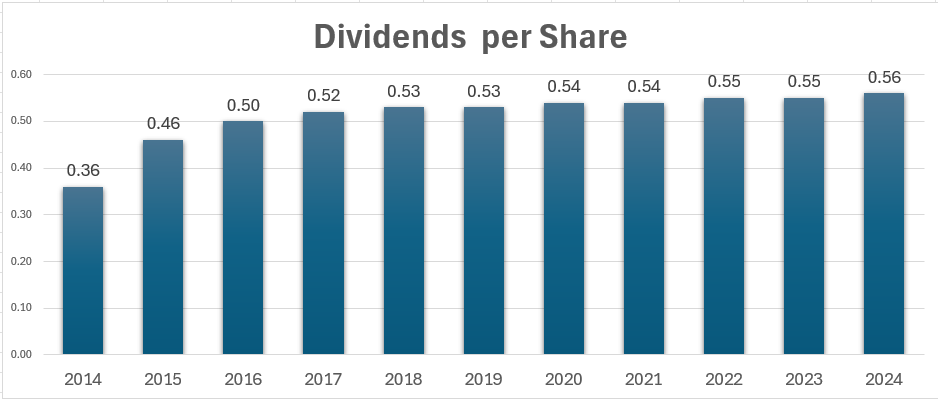

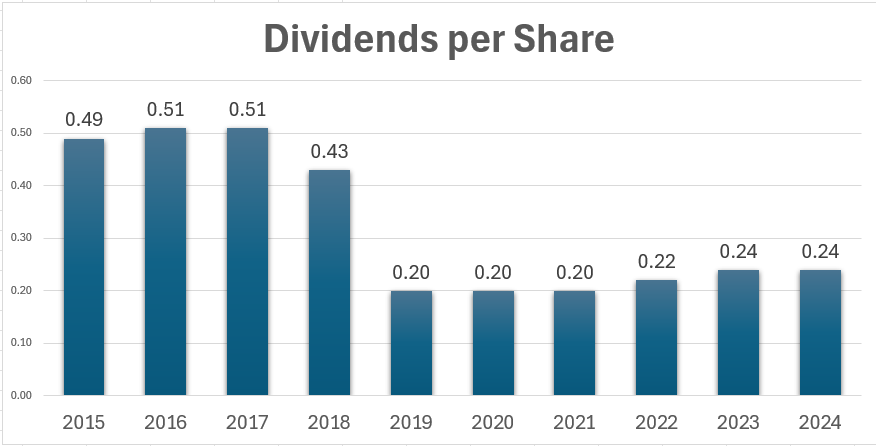

This choppy earnings stream has led to flat and/or very modest dividend growth:

iREIT®

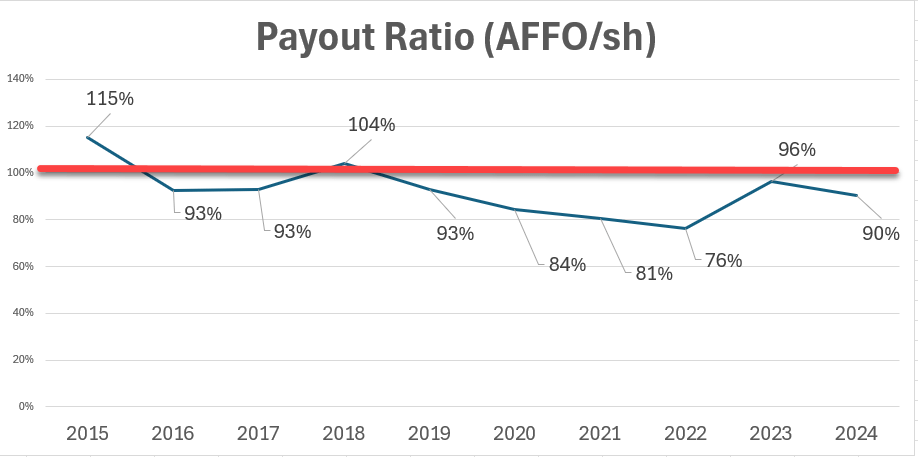

As viewed below, LAND has a higher payout ratio than most REITs, but that's expected given the fact that the company has lower capex requirements, and the portfolio maintains very high occupancy.

iREIT®

As you can see (above) LAND's payout ratio was elevated in 2023, however based on analyst consensus numbers, LAND should easily cover its dividend in 2024 and possibly increase it by a small margin.

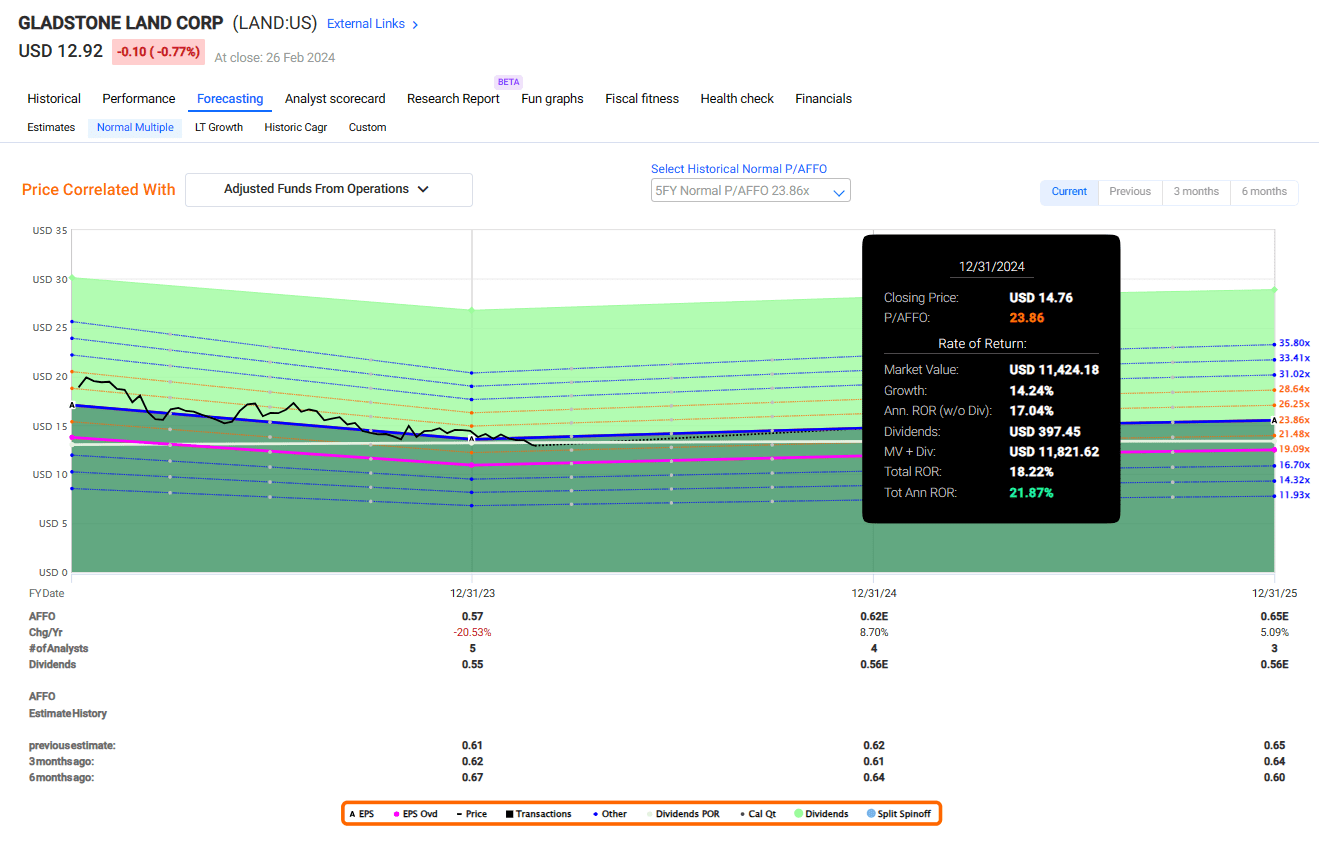

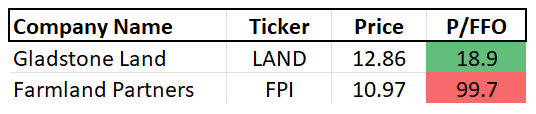

LAND is no bargain today, shares trade at $12.92 per share. But we do like the price for a long-term investor. Shares trade at 22.4x P/AFFO vs. the normal multiple of 24.2x. The dividend yield is 4.3%, and as mentioned, earnings should cover the distribution in 2024.

I'm not a huge fan of certain "mega loser states" that include California, Oregon or New York, and LAND has 63 farms in California. However, many of the farms are in East Coast markets (like my home state of South Carolina).

Thus, LAND could be a good fit with potential annual returns of 20% or higher. I also like the insider ownership - management owns 9% of the common shares. We maintain a Spec Buy.

FAST Graphs

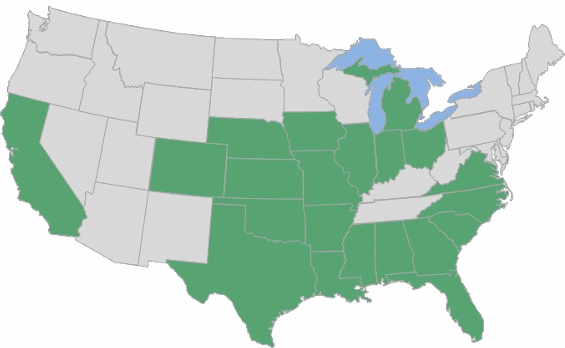

FPI is an internally managed REIT that owns and/or manages 178,000 acres (approximately 7.8 billion square feet) spread across 20 states. The portfolio includes more than 100 tenants with more than 26 types of crops. The portfolio has 100% occupancy.

Around 90% of the portfolio (70% of total value) is leased to row crop farmers, which means the crops are planted (or replanted) every year.

They're rotated to maximize soil health and market opportunities. These crops tend to be commodity products like corn, soybeans, wheat, rice, cotton. Representative states include Arizona, Colorado, Florida, Georgia, Illinois, Indiana, Kansas, Louisiana, Michigan, Missouri, Mississippi, North Carolina, Nebraska, Oklahoma, South Carolina, Texas, and Virginia.

The other 10% of the portfolio (30% of value) is leased to specialized products like tree nuts, citrus, avocados. Representative states include Alaska, California, Florida, Georgia, and Michigan.

FPI IR

FPI's capital structure consists of fixed-rate debt ($286 million), floating rate debt ($137 million) and common stock ($544 million). As of Q3-23, the company's weighted average cost of debt was 4.94%.

At the end of Q3-23, total debt was $22.8 million and the company had $157 million undrawn in its credit facility.

In addition to internal management and the focus on row crops, FPI is notable for having been the focus of a short thesis by an analyst called Rota Fortunae. FPI's problems commenced before the short thesis. The company was not growing, and the dividend was becoming less safe.

iREIT®

As seen below, FPI cut its dividend substantially in 2019 and has since been clawing it back. Note that the company paid out a special dividend of $.21 per share in December that's not reflected in the chart below.

iREIT®

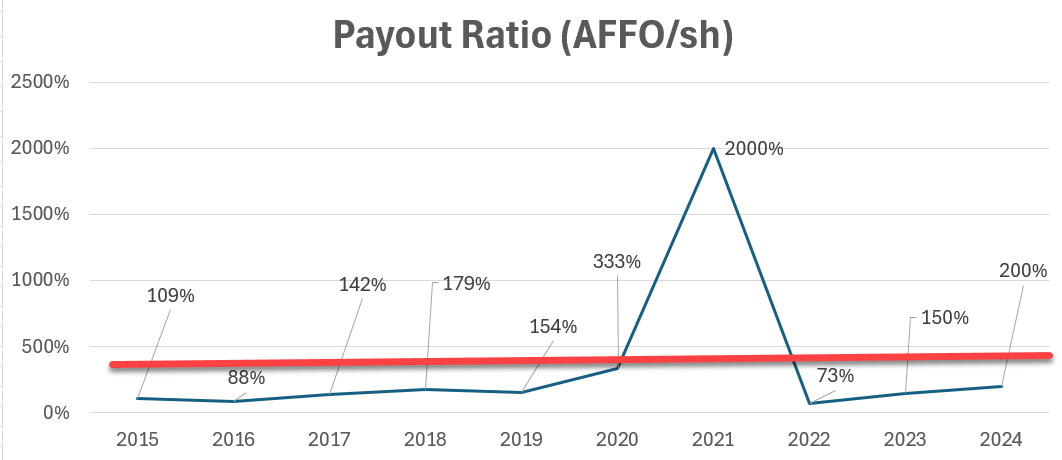

One concern with FPI is the fact that the company has consistently maintained a payout ratio of more than 100%.

iREIT®

Analysts forecast another negative year of growth for FPI in 2024 with a rebound in 2025.

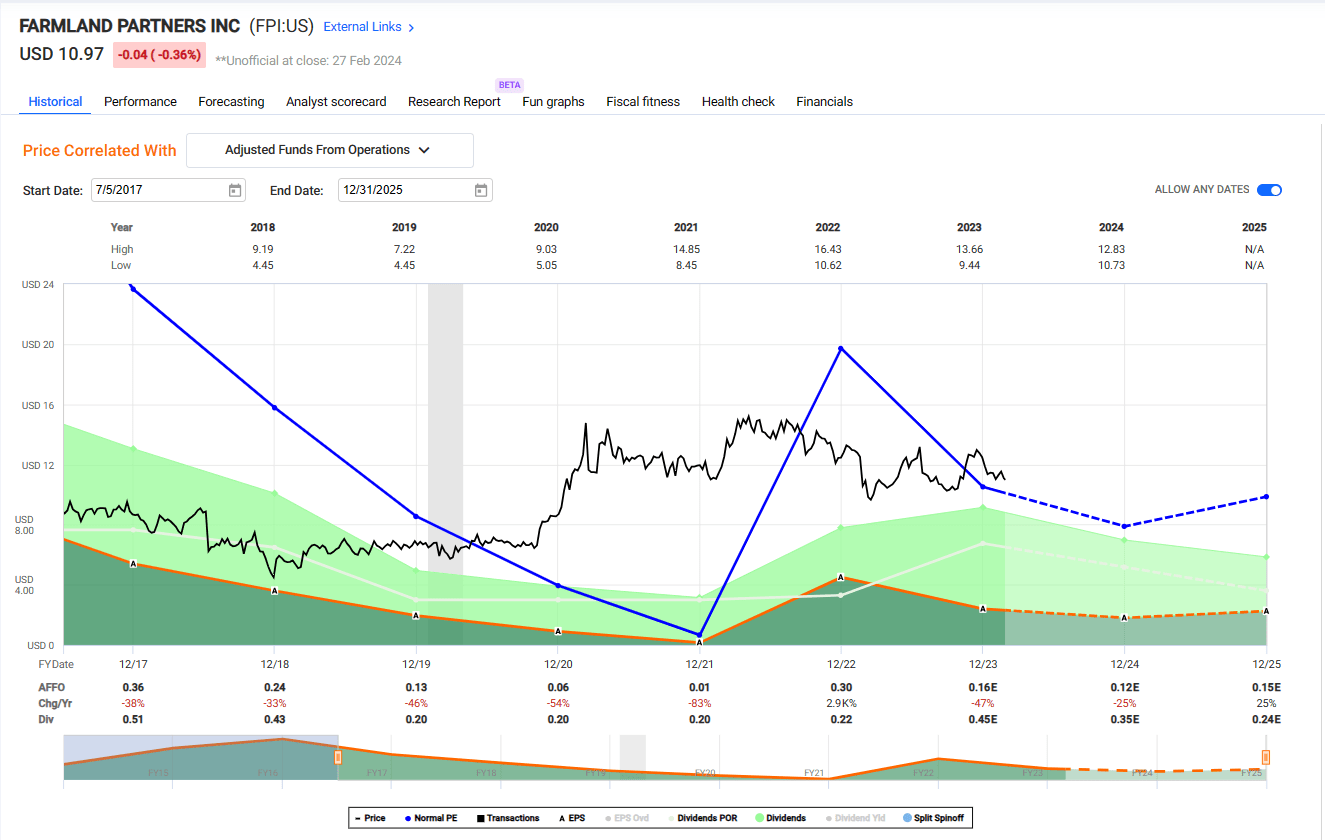

The company has not maintained stability since its IPO, yet shares trade at $10.97 per share or 71.4x P/AFFO. The dividend yield is 2.19%. On the positive side, management is well entrenched as insiders own around 10% of shares.

I do like the recent expansion into net lease investments via four agricultural equipment dealerships in Ohio under the John Deere brand. The accounting treatment classifies these acquisitions as financing transactions, so they appear on the balance sheet as loans and on the income statement as interest income.

Perhaps FPI should also expand into cannabis, just a thought. We maintain a Hold.

FAST Graphs

I'm not "digging" any of these farming REITs right now, but another way to play it is Federal Agricultural Mortgage Corp. (AGM) as the company recently rolled out a more than 27% increase in the dividend with a payout ratio is just over 28%. As I explained earlier:

"The company only holds a mid-single digit share of the $324 billion agricultural mortgage market. Management views demand for renewable power generation and storage, along with investments in rural fiber and broadband, as areas that could sour growth."

Now we're talking (and shouting):

"We'll have a little butter, and we'll have a little cream,

We'll have a little milk and a little margarine."

Happy Farm Investing!

iREIT® iREIT® iREIT® iREIT® iREIT®

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.