3d_kot/iStock via Getty Images

3d_kot/iStock via Getty Images

In the stock market, we have a term for stocks that generate dividend yields that are too good to be true…

We call them sucker yields.

I included the definition in my new book:

REITs for Dummies by Brad Thomas (Wiley)

Whenever I see a stock that yields 10% or higher, I become skeptical that the company can sustain its dividend.

We've seen this play out time and time again in the REIT sector...

How many sucker yields have you purchased and later regretted it?

That leads me to today's headline article:

Is Blackstone Mortgage's 12.3% Dividend Yield A Sucker Yield?

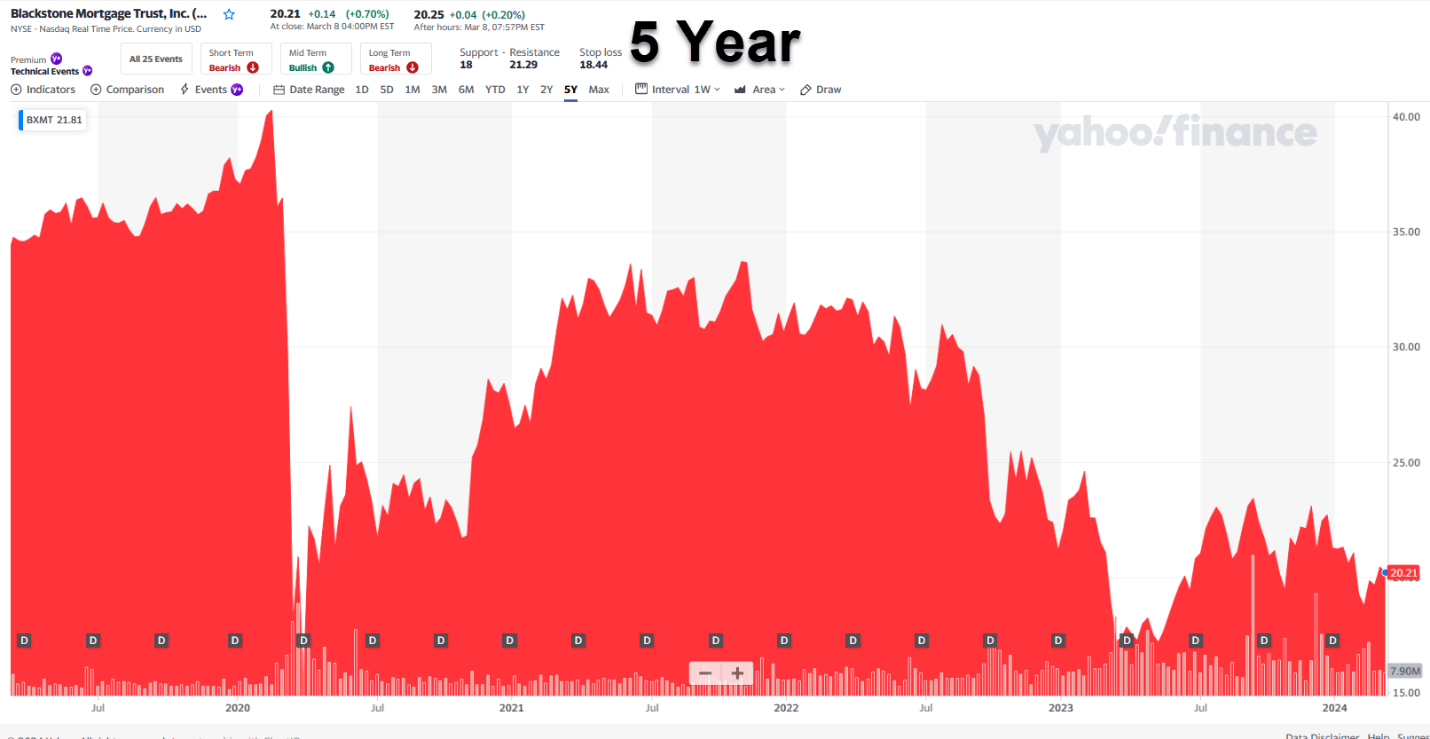

Yahoo Finance (5-Year)

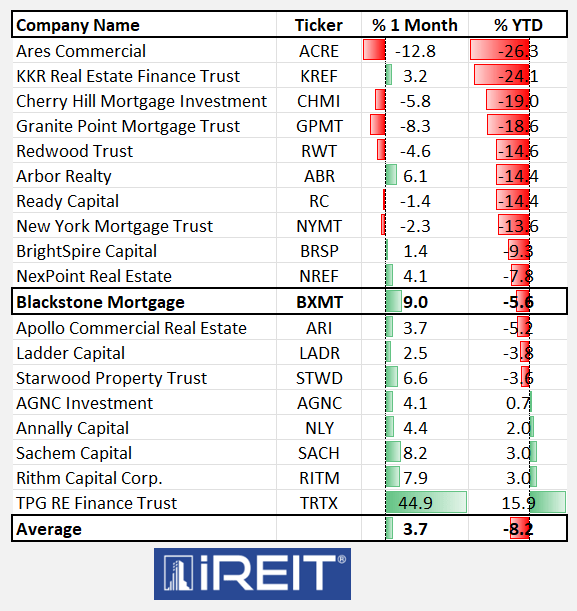

As you can see, Blackstone Mortgage Trust's (NYSE:BXMT) share price is near Covid-19 lows, suggesting something is "rotten in Denmark" (idiom that means something is seriously amiss).

However, it's not just BXMT that's stinky.

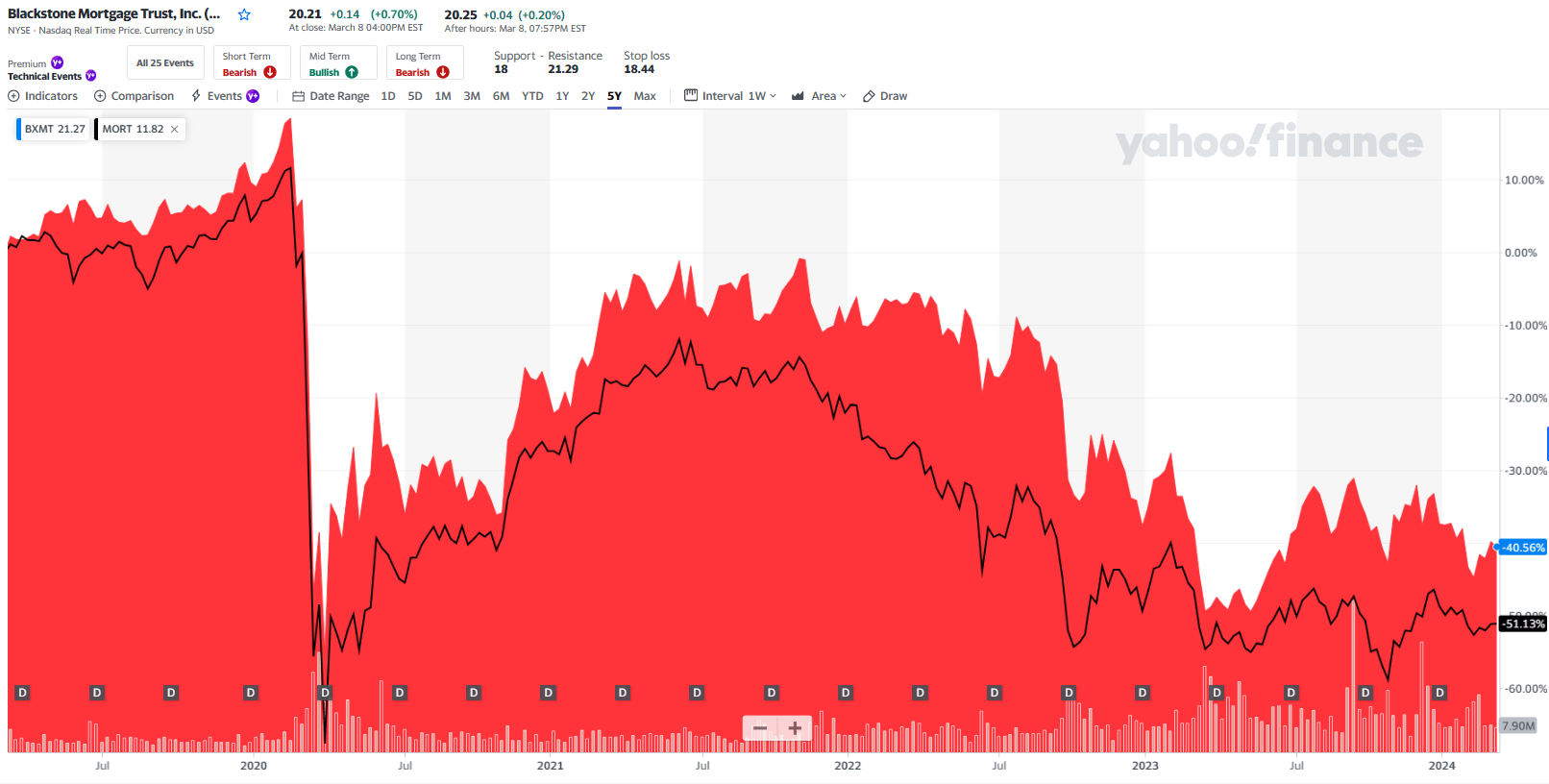

Just take a look at BXMT compared with the mortgage REIT ETF known as MORT.

Yahoo Finance (5-Year)

It's well known that commercial real estate ('CRE') fundamentals remain unstable and as rates stay higher for longer pressure will increase on mREIT portfolios.

And unlike residential mortgages, commercial mREIT loans tend to be floating rates.

As rates have risen from historic lows (and seem poised to stay "higher-for-longer"), properties have seen material declines in value, which impact borrowers' ability to refinance loans.

Although these distressed loans can be extended or modified to avoid a default, mREITs often require "rate caps" to be purchased at origination, which hedge against rate moves.

So as rates have risen sharply, these caps have helped keep interest costs low for borrowers.

However, as loans mature, the rate caps also mature, causing borrowers to buy new rate caps at expensive prices.

This creates a natural opportunity for borrowers to weigh the cost of adding equity into the property or to default and hand back the keys to the lender.

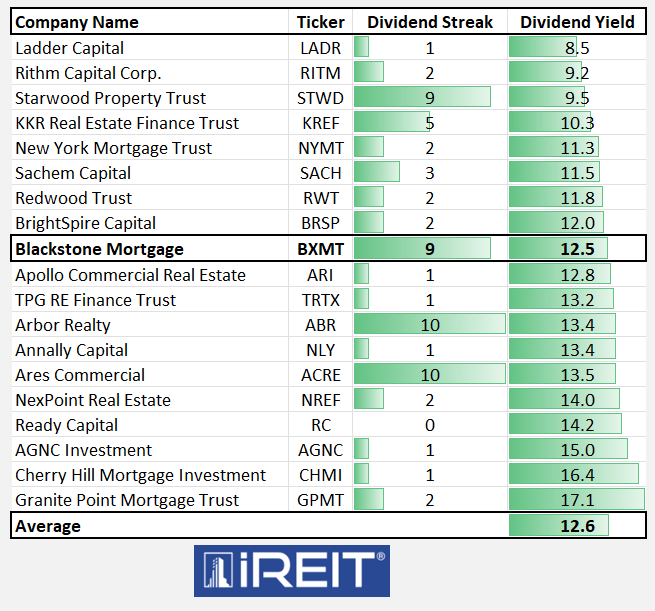

This brings me to BXMT's dividend yield, which is 12.3%.

Seeking Alpha (Dividend Yield)

BXMT is a commercial mREIT managed by its "big brother" asset manager, Blackstone Inc. (BX), the largest real estate private equity business in the world, with access to all the resources of the Blackstone Real Estate platform.

Blackstone is the largest global alternative asset manager with a 38-year investment record and $1 Trillion of assets under management that includes 60+ investing strategies.

BXMT IR

BXMT operates a simple business model that consists of a portfolio of 100% senior secured loans with a weighted average origination LTV of 64%, all collateralized by institutional-quality real estate across sectors and markets.

BXMT IR

BXMT originates loans that are sized and structured to capitalize value-added business plans that drive cash flow growth and long-term value creation.

The loans are repaid when sponsors sell or refinance assets, typically following the execution of a business plan, and sometimes when there's a default.

Generally, commercial mREIT loans face headwinds due to weak office property fundamentals (which make up ~30% of mREIT portfolios, on average) and higher-for-longer rates that weigh on valuations.

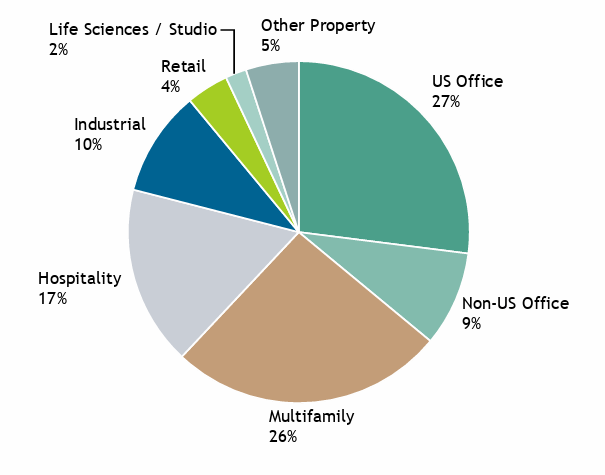

As shown below, BXMT has 35% exposure to the office sector, broken down as 27% US office exposure and 9% non-US office exposure.

BXMT IR

Higher-quality offices (trophy or Class A) have had better vacancy trends than lower-quality properties (Class B and below) and this has enabled BXMT to mitigate some of the headwinds.

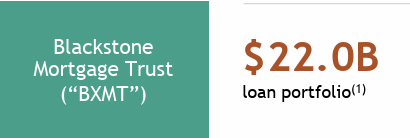

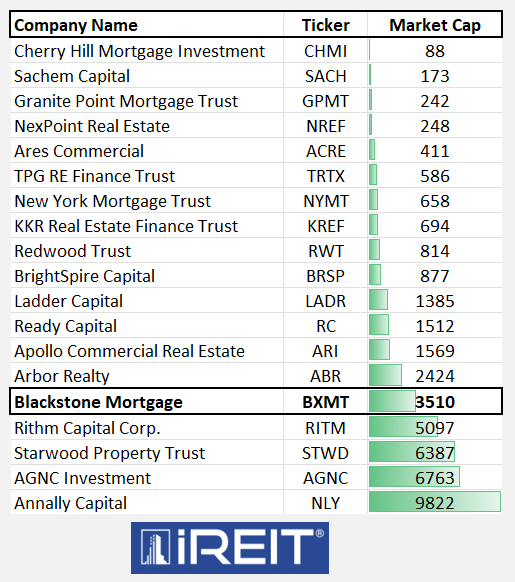

BXMT's $22.0B portfolio consists of 178 senior loans, collateralized by institutional quality real estate and diversified across sectors and markets; weighted-average origination LTV of 64%. BXMT's average loan size is around $120 million compared to these peers:

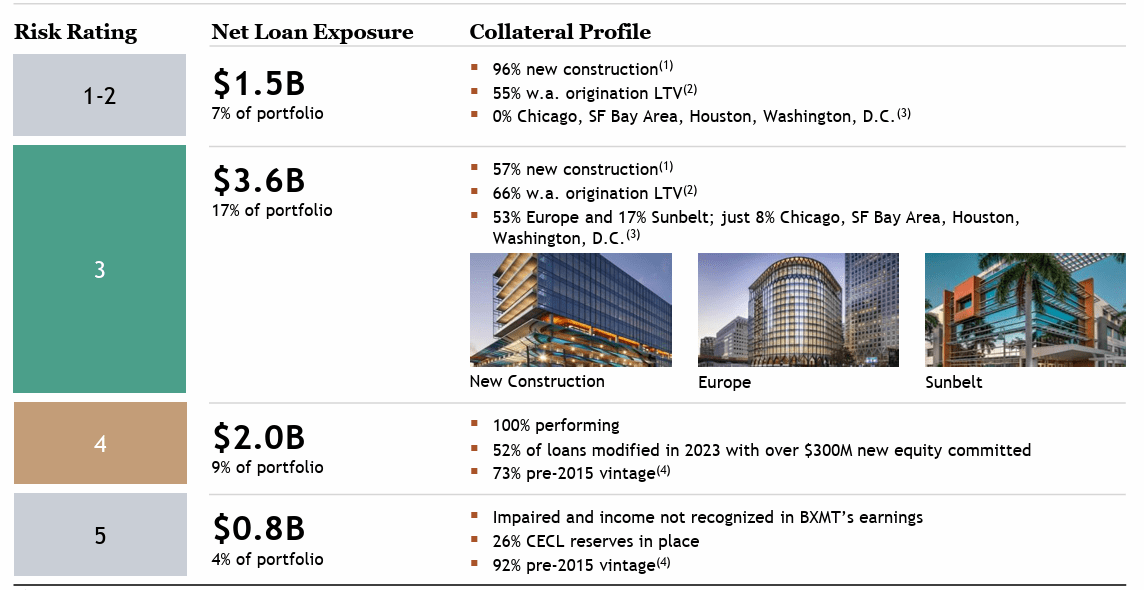

In terms of BXMT's office exposure, around 30% of the total office is either outperforming (risk rated 1-2) or already impaired (risk rated 5) with reserves reflected on BXMT's balance sheet.

Risk rated 3 loans are concentrated in newer-vintage assets and/or better markets; risk rated 4 loans are performing loans but concentrated in older-vintage assets and/or weaker markets.

BXMT IR

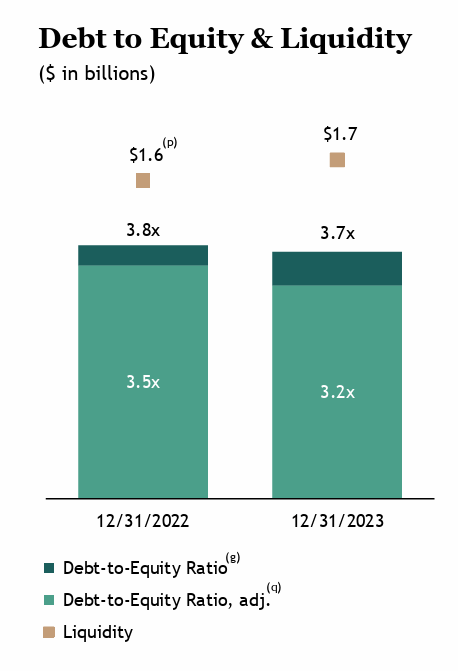

BXMT's diversified balance sheet is structured to withstand volatility with term-matched financings, substantial liquidity, and no capital markets mark-to-market provisions.

BXMT has maintained consistently strong liquidity over the year with $1.7B at year-end 2023 while reducing leverage to 3.7x from 3.8x in 2023.

BXMT IR

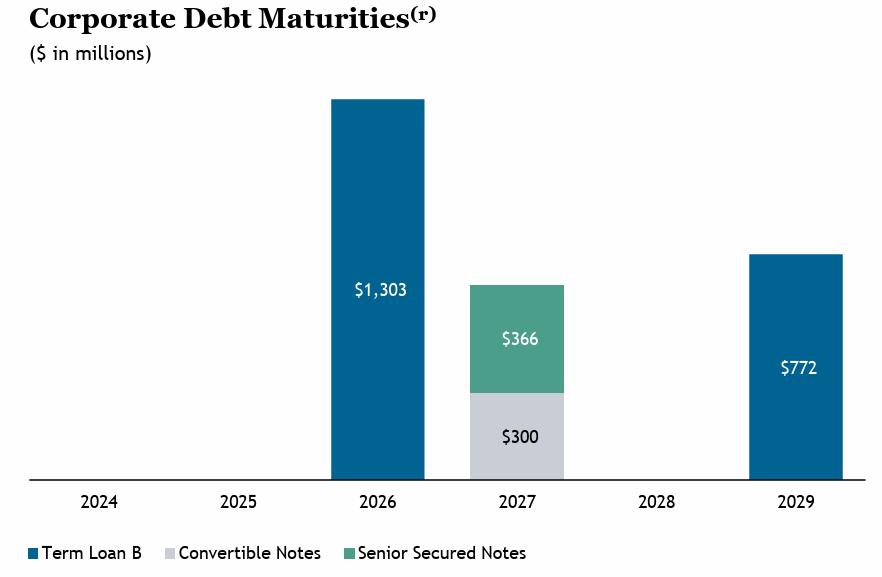

As shown below, there are no corporate debt maturities until 2026, and net future funding commitments of $1.2B are spread over a weighted-average term of 2.6 years, and approximately 90% are tied to leasing costs or capital expenditures.

BXMT IR

BXMT's dividend is $0.62 per share or $2.48 annually, which represents a current yield of 12.3%. The company has paid the dividend consistently for 34 quarters. On the latest earnings call, the CFO said:

As in the past, we will make decisions regarding our dividend with this long-term perspective in mind, rather than reacting to any short-term changes in earnings that we believe are temporal in nature.

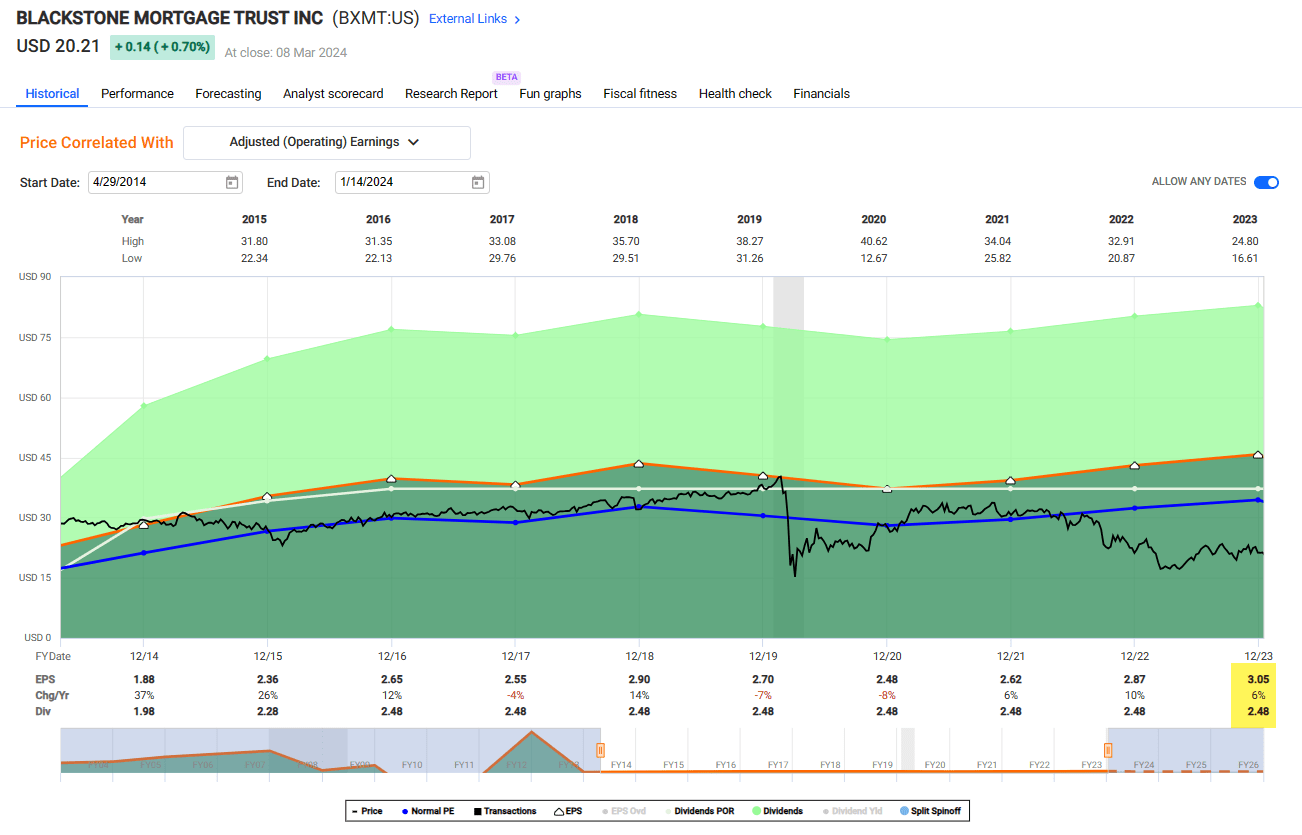

In Q4-23, BXMT generated distributable earnings of $.69 per share or $3.05 for YE 202 (highest annual earnings since BXMT was launched in 2013).

FAST Graphs

The $3.05 per share for 2023 covered the dividend of 123%.

This dividend of $2.48 per share of current income exceeded the $1.10 net reduction in book value from CECL reserve increases, while the company maintained record levels of liquidity and reduced leverage.

FAST Graphs

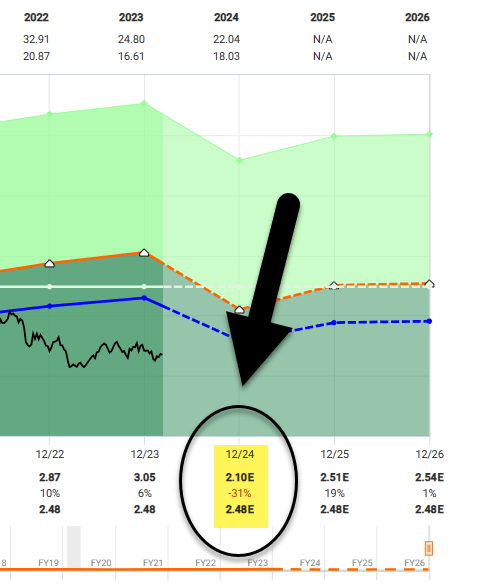

Now we can see where things start to look sketchy...

As shown above, analysts are forecasting negative EPS in 2024, down 31% from $3.05 in 2023 to $2.51 in 2025.

This represents a forward-looking payout ratio of 118%.

Keep in mind that the 2024 consensus number includes 8 analysts.

2025 suggests improvement in 2025, as 6 analysts forecast $2.51 of EPS, which translates to a payout ratio of 99%.

Commercial mREIT portfolios with 2024 maturities have higher risks, due to rate cap expirations; loans with later maturities should benefit as rates decline and fundamentals rebound.

Now, the good news is that 93% of BXMT's portfolio is performing.

Also, the company has virtually no exposure to New York City or San Francisco rent-regulated multifamily.

The bad news is that BXMT has $2.7 billion of loans on the watch list.

And these are big loans...

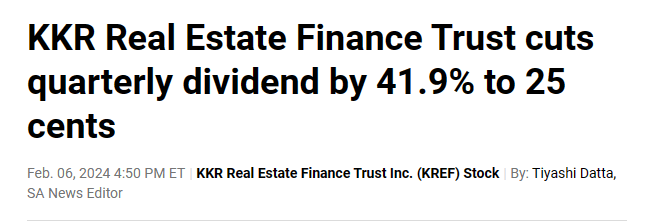

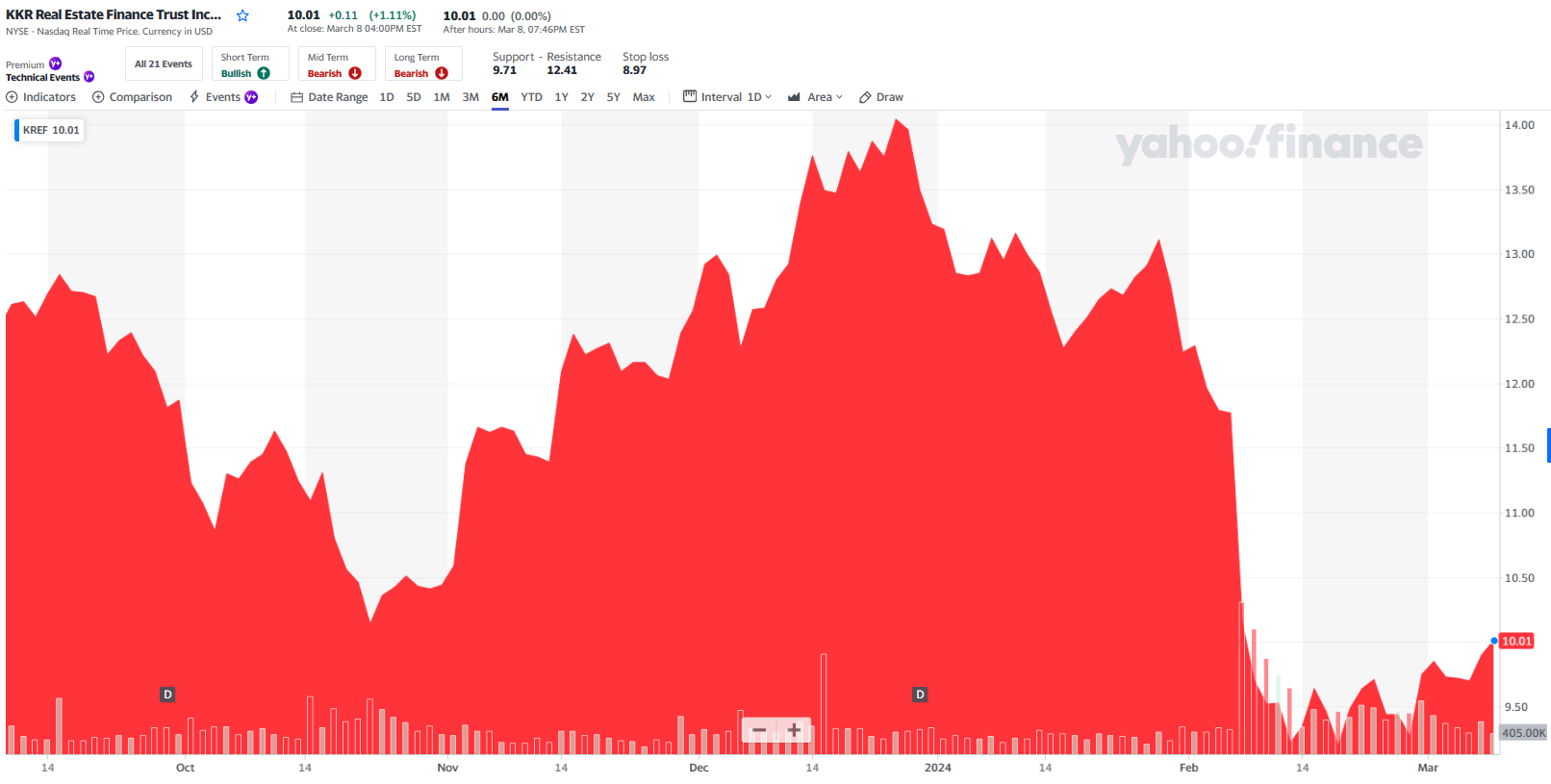

I consider KKR Real Estate's (KREF) recent dividend cut a harbinger of more bad news to come.

Seeking Alpha (KREF)

Perhaps BXMT can avoid a dividend cut...

Is the thrill of victory worth the agony of defeat?

Yahoo Finance (KREF)

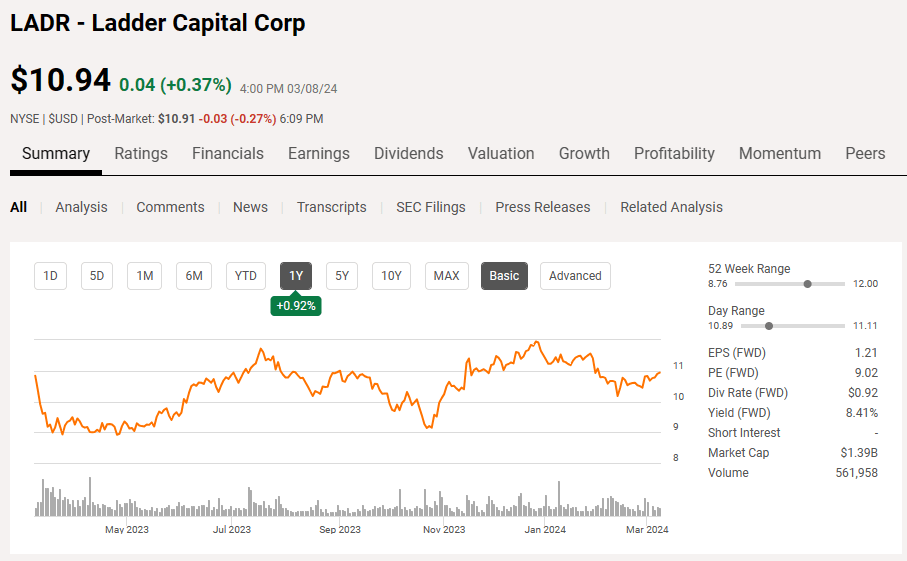

In a previous Seeking Alpha article I highlighted Ladder Capital (LADR), my favorite mREIT and not a "sucker yield".

LADR's borrowings under repurchase facilities were about 16% of total debt, which limits exposure to margin calls caused by weakening asset quality.

Ladder also has the highest percentage of unsecured debt among peers, at about 41% of total debt.

The company continues to maintain ample unencumbered assets.

As of the end of 2023, LADR had about $2 billion in unencumbered assets that it could use to raise liquidity if needed.

Two things I like most about LADR are (1) its strong inside ownership (management team and directors own over 11%) and smaller loan size (of around $20 million).

In this cycle, I would avoid BXMT and focus on LADR.

Seeking Alpha (LADR)

(I hope you're enjoying our new "data duel" feature. Let us know your feedback, please. Thank you)

iREIT® iREIT® iREIT® iREIT®

That's all folks!

PS: We moved BXMT to a Spec Buy and included it on the Dividend Watch List.