andreswd/E+ via Getty Images

andreswd/E+ via Getty Images

Back at the beginning of 2021, I shared a note on Kymera Therapeutics (NASDAQ:KYMR) with Seeking Alpha readers titled "Kymera Therapeutics Is A Protein Degrading Pioneer With A Triple-Figure Share Price In Waiting".

Looking back today, now that Kymera shares trade at a value of $39 (they were priced at $81 when I posted my note), it's clear I was over-optimistic, although my call was based on several factors which arguably still remain true today, and since I did not specify a time-line, perhaps Kymera can deliver the magical $100 per share price tag after all!

In this note, I will recap the investment thesis that got me excited about Kymera in the first place, update on progress over the last 3 years, and speculate about when, if ever, we will see some steady share price upside.

I provided a detailed overview of protein degradation and Kymera's approach to it in my last note, and since this has not fundamentally changed I will reproduce some of that here:

Kymera's technology targets the ubiquitin proteasome system, which acts like a cell's waste disposal unit, degrading proteins that have been marked for elimination by enzymes known as E3 ligases.

The Pegasus platform develops small molecules that are able to link the correct E3 ligases with specific disease causing protein targets, which are then bound to by E2 ligases carrying ubiquitin.

As the process repeats, a ubiquitin chain is formed, tagging the protein for destruction via the proteasome. The proteasome breaks the protein down into fragments, which can be reused in other cellular processes.

Instead of merely inhibiting the activities of proteins, as most small molecule drugs do, Kymera's technology allows for the protein to be removed altogether. The degrader molecules that Pegasus develops are further differentiated by their ability to bind to multiple sites on a protein, rather than just the active site, enabling them to be administered orally, and theoretically, to target and degrade entire signaling cascades that were once regarded as undruggable.

Kymera seems to have held onto most of its senior management team, led by Nello Mainolfi, with Jeremey Chadwick as Chief Operating Officer, and Jared Gollop as Chief Medical Officer, which is a positive for me, as it brings continuity and suggests management still believes in what it is trying to achieve.

Only Chief Science Officer Richard Chesworth has departed, returning to Third Rock Ventures, the VC firm that seeded Kymera. Kymera's IPO in August 2020 raised $173m, and a late stage seed round led by Third Rock raised $102m, backed by a number of biotech VC companies including Wellington Management, Blackrock, and Bain Capital, as well as the investment arms of Pfizer (PFE), Vertex (VRTX), and Eli Lilly (LLY).

In 2021, the company had partnerships in place with the 'Big Pharma" concerns GSK (GSK), Vertex, and Sanofi (SNY), however it seems the GSK and Vertex collaborations have expired, without any further development milestones having been paid, which helps to explain why Kymera's share price has hit lows of ~$15, in June 2022, and ~$11 in October last year.

On the plus side, Sanofi has taken up its option to keep developing Kymera's lead candidate, KT-474, which targets the protein IRAK4, and is being developed to treat autoimmune conditions including hidradenitis suppurativa ("HS"), atopic dermatitis ("AD"), rheumatoid arthritis ("RA"), asthma, and inflammatory bowel disease ("IBD"). It seems the company has turned down the opportunity to develop any further assets, however.

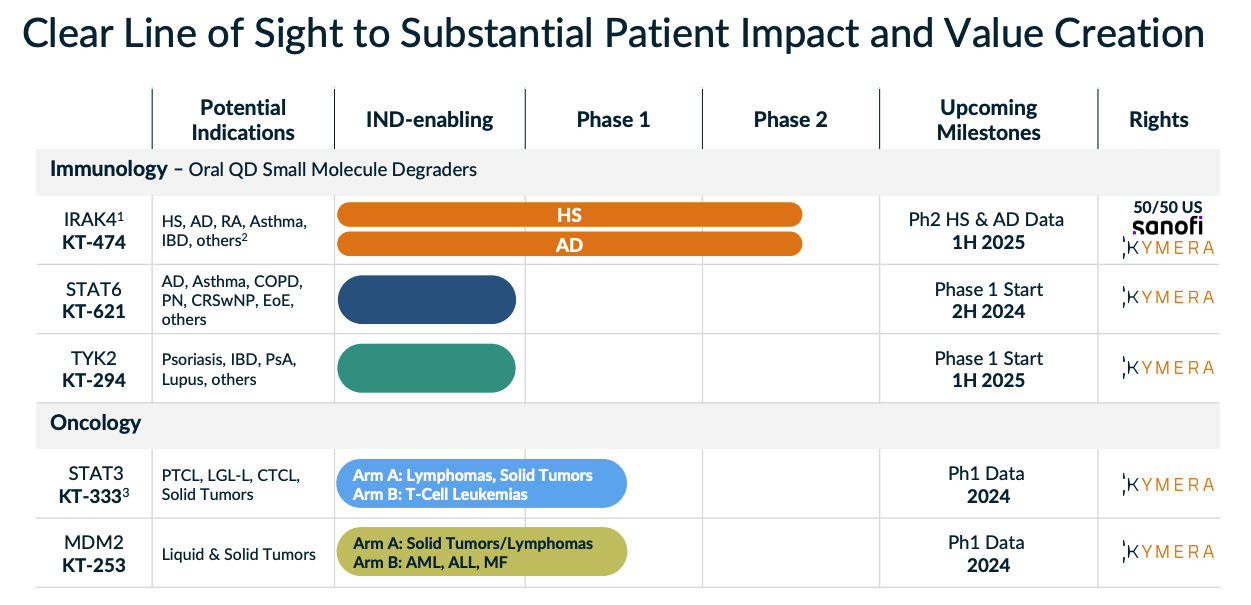

Kymera's two other preclinical candidates mentioned in my last post, KTX-120 and KT-413 - targeting Diffuse large B-cell lymphoma ("DLBCL"), and liquid and solid tumors, respectively, both appear to have been discontinued, although, as we can see below (slide taken from a February 2024 investor presentation), they have been replaced by two other oncological candidates, KT-333, targeting STAT3, and KT-253, targeting MDM2, although the company notes that "assessment of STAT3 opportunity is ongoing".

Kymera pipeline (investor presentation)

Back in 2021, I wrote:

Kymera's most advanced candidate - KT-474 - targets HS and AD. The treatment market for dermatological conditions is worth >$30bn, and currently dominated by Humira - the world's best-selling drug, which will earn its developer and marketer AbbVie (ABBV) revenues of ~$20bn in 2020.

Humira is scheduled to go off patent in the US in 2023, however (and has already done so in Europe), creating a massive market opportunity. KT-474 - for which Kymera hopes to file an Investigational New Drug ("IND") application, and initiate a Phase 1 trial in H121, ought to be pushing for an approval by 2023, provided its promising preclinical data is demonstrated in a real world setting.

How optimistic that seems now. Humira's US patent expiry did indeed occur in 2023, but Kymera was in no position to take advantage with KT-474, given topline data from two Phase 2 studies in HS and AD is not due until the first half of 2025. Instead, the likes of AbbVie's Skyrizi and Rinvoq, Sanofi and Regeneron's (REGN) Dupixent, Pfizer's Cibinqo, and a variety of topical creams have rushed to fill the void created by Humira's loss of exclusivity ("LOE").

Nevertheless, Kymera earned $55m when Sanofi opted to initiate these two studies, which both began enrolling in the fourth quarter of last year. In November last year, Kymera shared Phase 1 data in the respected journal Nature Medicine - highlights summarized as follows:

For HS, the analysis was performed for all patients (n = 12), including two patients with very severe disease who had progressed after prior biologics, as well as for those patients with moderate to severe disease (n = 10). Overall, both analyses yielded similar results, with responses for the group gradually evolving over the 28d of dosing before then being generally maintained or continuing to improve during the subsequent 2-week follow-up period. There was a 46.1–50.7% reduction in abscess and nodule ("AN") count (maximum 100% reduction) and an HS Clinical Response 50% ("HiSCR50") reduction rate of 42–50%, as well as an AN 0/1/2 rate of 42–50%.

There was a 48.8–55.2% reduction in Pain Numerical Rating Scale (NRS) and a 50–60% Pain NRS30 (at least a 30% reduction and one unit reduction from baseline) response rate. Pruritus is a substantial problem in patients with HS, and KT-474 also impacted this symptom with a 61.6–68.4% reduction in Peak Pruritus.

Patients with AD, like patients with HS, also showed a pattern of response characterized by evolution over the dosing period followed by maintenance or continued improvement during follow-up. There was a 37.1% reduction in Eczema Area and Severity Index (EASI) score (maximum 76% reduction), with validated Investigator Global Assessment for AD improving in two patients and remaining stable in the others. Pruritus is one of the primary symptoms affecting quality of life in patients with AD. Peak Pruritus declined by 62.9%, with a Peak Pruritus response rate of 71%

For context, AbbVie's JAK inhibitor Rinvoq achieved the following results in its pivotal Phase 2b study in AD:

A 75 percent improvement in disease (EASI 75) was achieved by 69/52/29 percent of patients receiving the 30/15/7.5 mg doses of upadacitinib (Rinvoq) respectively, compared to 10 percent for patients receiving placebo (p<0.001/0.001/0.05, respectively).

The Rinvoq data is taken after 16 weeks, whilst the KT-474 data is over 4 weeks, hence, perhaps it seems possible that KT-474 could emerge as a contender for approval in AD - and other autoimmune conditions - when Phase 2 data is made available in 2025.

Kymera's AD study will use % change in EASI as its primary endpoint, but the bar for "best-in-class" remains very high - remember, it seems nearly 70% of all Rinvoq patients experienced 75% improvement at 12 weeks - at 4 weeks, only a single KT-474 had achieved such a reduction.

In HS, I found the following information from a Novartis (NVS) press release announcing the approval of Cosentyx in the indication:

Results from the US Food and Drug Administration (FDA)-requested analyses at Week 16 showed that a significantly higher proportion of patients achieved HiSCR50 when treated with Cosentyx 300 mg dosed every two weeks (after standard weekly loading doses), compared with placebo in both the SUNSHINE and SUNRISE trials (44.5% vs 29.4% [*P<0.05] and 38.3% vs 26.1% [*P<0.05], respectively). A greater proportion of patients randomized to Cosentyx 300 mg dosed every four weeks (after standard weekly loading doses) achieved HiSCR50 compared with placebo in both SUNSHINE (41.3% vs 29.4%) and SUNRISE (42.5% vs 26.1% [*P<0.05]) trials.

Again, my reading of these results seems to suggest KT-474 may have a competitive efficacy profile, and Kymera also seems to believe this is the case.

In an interview with Dermatology Times, Kymera's CMO Gollop comments "the results we saw were comparable to the metrics one would associate with standard of care agents", and also underlines the fact that the studies, albeit small with no comparator arm, help to confirm that KT-474 does indeed degrade IRAK4, and that this is now a validated target.

Gollop also points to the oral administration of KT-474, a potential advantage over injectables such as Humira or Dupixent, while oral JAK inhibitors like Cibinqo or Rinvoq have been associated with an adverse safety profile.

There is no questioning the market opportunity for KT-474, if successful - an $8bn AD market, $16bn IBD market, and $28bn RA market for example - Kymera estimates the immune-inflammation market could be worth as much as $250bn globally - hence, these Phase 2 studies appear to be the stand out opportunity for the company.

According to Kymera, "STAT6 is the specific transcription factor required for IL-4 and IL-13 cytokine signalling", and "STAT6 regulated cytokines are clinically validated targets for allergic diseases".

Kymera cites the success of Sanofi's Dupixent, which blocks IL-4 / IL-13 signalling, as validation of its approach. Dupixent has been hugely successful, and some analysts believe the drug will break $20bn in peak annual sales across numerous autoimmune indications, such as chronic obstructive pulmonary disease ("COPD"), AD, and asthma.

According to a statement in Kymera's 10K, a two-week atopic dermatitis model in mice:

KT-621 robustly and dose dependently inhibited IgE elevation to levels that were comparable to dupilumab, in this preclinical study. Of note, the KT-621 dose that led to 90% STAT6 degradation produced similar activity in this preclinical model to an IL-4Rα saturating dose of dupilumab, indicating full IL-4 and IL-13 blockade by KT-621 in vivo.

Kymera shares many more examples of how KT-621 may prove superior to Dupixent (dupilumab) in its investor presentation, although if that were the case, it seems bizarre that Kymera's partner Sanofi, the developer of Dupixent, is not attempting to partner with Kymera on this asset.

Perhaps Kymera prefers to develop KT-621 itself, and has not given Sanofi the option - although, with so many drugs in development focused on IL-13, and other cytokines such as IL-17, perhaps there are doubts around whether Kymera's preclinical data can be reproduced in the clinic, and establish proof-of-concept.

Meanwhile, Kymera's KT-294 focuses on a slightly more established target in TYK2, a member of the janus kinase ("JAK") family, making it a potential rival to Rinvoq, or Johnson & Johnson (JNJ) Tremfya, two drugs making sales in the multi-billions. Kymera is once again discussing a "potential best-in-class" opportunity, in dermatology, gastroenetreology, rheumatology, and CNS, and arguing that only its degrader approach can deliver "biologics like activity", as other JAKs are unable to deliver "full pathway inhibition".

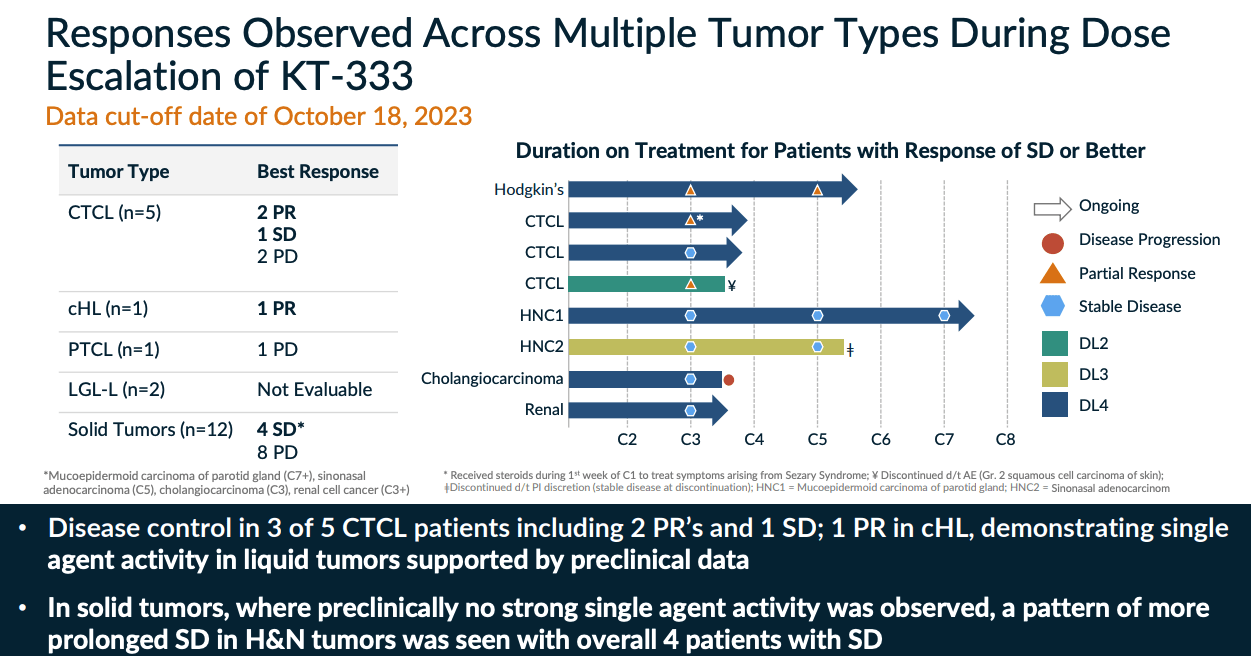

Finally, within oncology, STAT3 and MDM2 are the targets, and KT-333, which targets the former, has demonstrated some promising results in a Phase 1 study, as shown below:

KT-333 P1 data (investor presentation)

Once again, the degrader mechanism of action ("MoA") appears to work, and there is evidence to suggest the approach can help reduce tumor burdens, with an acceptable safety profile - Kymera has promised further data from this study this year, and from KT-253. Management updated on the Phase 1 study of the latter drug in its Q4 earnings press release, commenting:

The data demonstrated evidence of target engagement and p53 pathway activation, as well as initial antitumor activity and a lack of the traditional hematological toxicity seen with small molecule inhibitors.

The short answer is that, while acknowledging that there is significant risk attached to any investment in Kymera, I do still have faith in the company and its science, and, had I bought stock 6 months ago, when shares traded at $11, I would have realised a >125% return on investment.

Let's address the risks before we look at the positives. Early stage drugs that show impressive, "potential best-in-class" preclinical do have a nasty habit of being removed from biotech companies' pipelines overnight, as they ultimately prove ineffective / dangerous / unworkable for any number of reasons.

That has been the case with several of Kymera's assets, therefore, we may conclude that the science is not quite right and the company is attempting to squeeze a square peg into a round hole. Two of Kymera's partners have abandoned ship in the past couple of years, not seeing anything in Kymera's data that persuaded them to make milestone payments and take the project forward.

Kymera made a net loss of $(147m) in 2023, and $(155m) in 2022, and its accumulated deficit stands at >$500m. To date, no protein degrader drugs have been approved to treat any disease, and there is competition in the space from the likes of Arvinas (ARVN), C4 Therapeutics (CCCC), Foghorn Therapeutics (FHTX) and Nurix Therapeutics (NRIX). These companies' market caps are respectively $3bn, $600m, $276m, and $650m, meaning three of the four are much cheaper to invest in than Kymera, whose market cap stands at $2.5bn at the time of writing.

Nevertheless, for my money at least, Sanofi's decision to move forward with KT-474 has given Kymera - company and share price - significant upward momentum, and as discussed above, there is clinical evidence suggesting this drug, and the two oncology drugs, may be effective in a real-life setting, by leveraging Kymera's unique degrader approach.

With more Phase 1 data arriving this year, from the two oncology assets and Phase 2 KT-474 arriving early next year, Kymera, while not out of the woods yet, seems to have a fighting chance of establishing its technology as well worth investing in.

Positive Phase 2 data would offer genuine validation of the protein deg approach, generate further milestone payments, and perhaps, substantially increase the value of the KT-621 program, and even make Kymera an acquisition target for Big Pharma.

Kymera still has the same management team in place that it did back in 2020 when it completed its IPO, and given how heavily backed it was at that time, by a "who's who" of biotech investors, the company ought to have few problems finding additional funding if it needs.

Like Kymera, I am not prepared to give up on the protein deg story yet, and although a poor set of data, or the exit of Sanofi from the KT-474 program could derail the company's share price overnight, and this risk must be acknowledged, I believe the company may have now turned a corner, and therefore I am personally looking forward to the next set of data readouts, with optimism, not pessimism.