Sakorn Sukkasemsakorn/iStock via Getty Images

Sakorn Sukkasemsakorn/iStock via Getty Images

Quaker Chemical Corporation (NYSE:KWR) recently delivered better than expected EPS, 3.97% dividend growth, announced earnings growth for 2024, and continues to deliver investments in clean energy. With a well-diversified business model offering many products to clients in many sectors, KWR recently reported ongoing restructuring efforts, which will most likely bring further FCF margin and Adjusted EBITDA margin growth. In addition, I believe that we may see new stock demand coming thanks to the new stock repurchase agreement. There are several risks with regard to business cycles, inflation, and the effects of competition. However, KWR does trade quite cheaply right now.

Created in 1918, Quaker presents itself as a chemical company. Clients purchase different compounds and liquids including metalworking fluids, lubricants, cleaners, forging fluids, and hydraulic fluids. I believe that the number of different products and industries served is an asset for the company. I would expect lower net sales growth volatility than peers targeting more niche markets.

Source: Company's Website

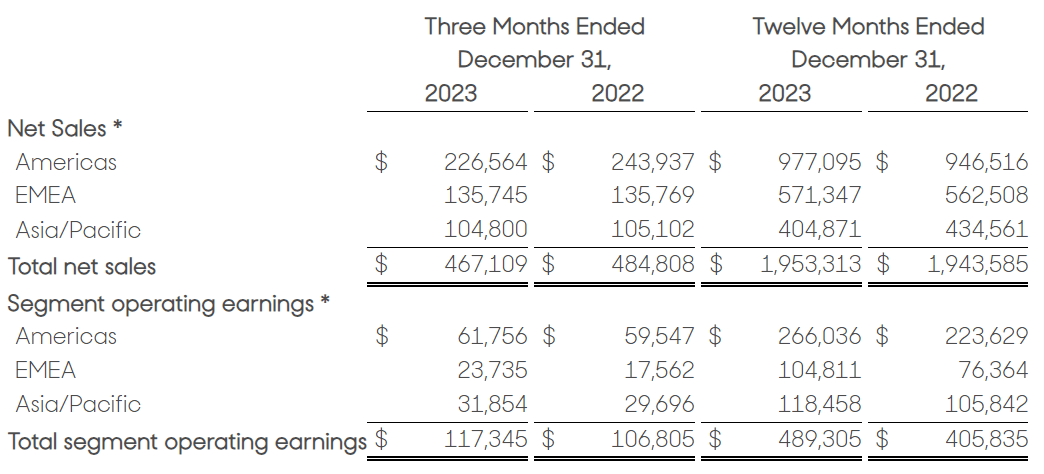

The business model appears quite diversified with activity in the Americas, EMEA, and Asia. Note that Quaker makes most of its revenue in the Americas, but other regions also represent a significant part of the total amount of sales. Geographic diversification will most likely have a beneficial effect on net sales volatility in the coming years. If the business model does not work in some areas, it may work in others.

Source: Quarterly Report

Quaker operates a global business model, where a significant portion of sales is made directly through employees and Fluidcare programs, complemented by sales through distributors and agents. Its employees collaborate closely with customers, identifying needs and offering solutions using existing products or innovative formulations. As part of Fluidcare, the company manages sales of third-party products, recognizing revenue on a gross or net basis depending on its role. Management provided more explanation about other ongoing programs on the company's website.

Source: Company's Website - Products

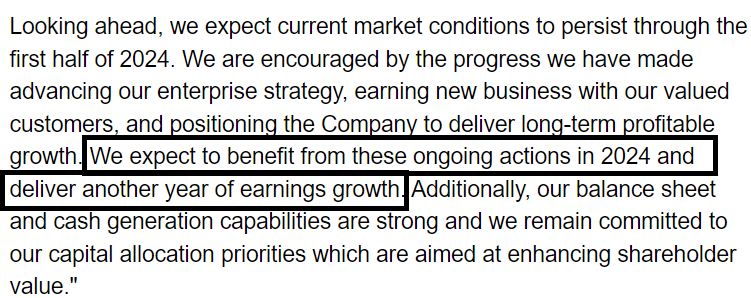

I believe that it is a great time for reviewing the company's business model, mainly after having a look at the recent earnings, which included better than expected EPS Non-GAAP figures. In addition, the guidance given for 2024 included beneficial words about future earnings growth.

Source: Quarterly Report

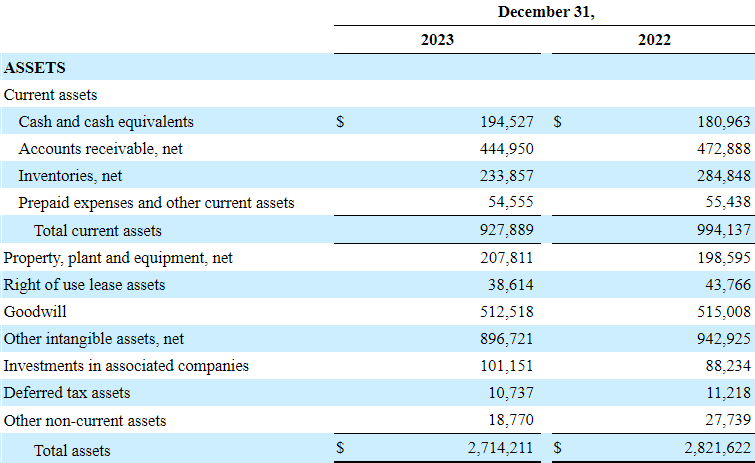

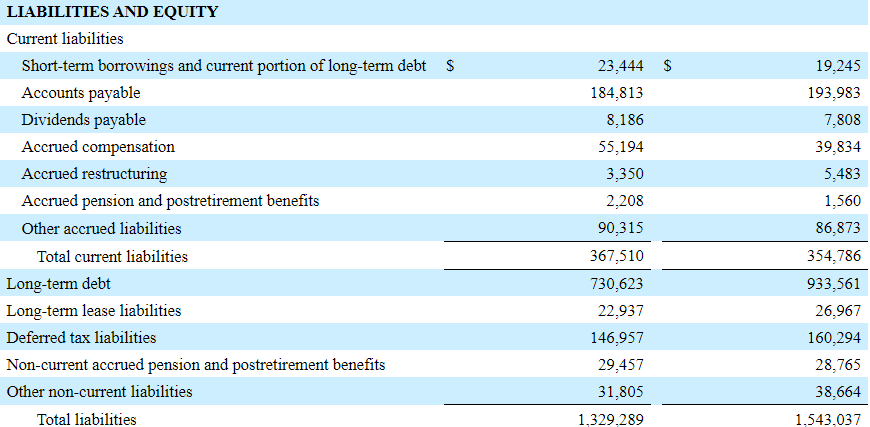

With an asset/liability ratio larger than 1x and a current ratio also larger than 1x, I believe that the balance sheet appears quite solid. Quaker reports a significant amount of cash in hand, close to $194 million, which management can use for R&D and inorganic growth. Given the goodwill accumulated worth close to $512 million, I think that new acquisitions could be announced.

Source: 10-k

The total amount of debt is not small. Long-term debt stands at close to $730 million, which is significantly smaller than that in 2022. I believe that lower debt level in the coming years could enhance the current EV/FCF ratio.

Source: 10-k

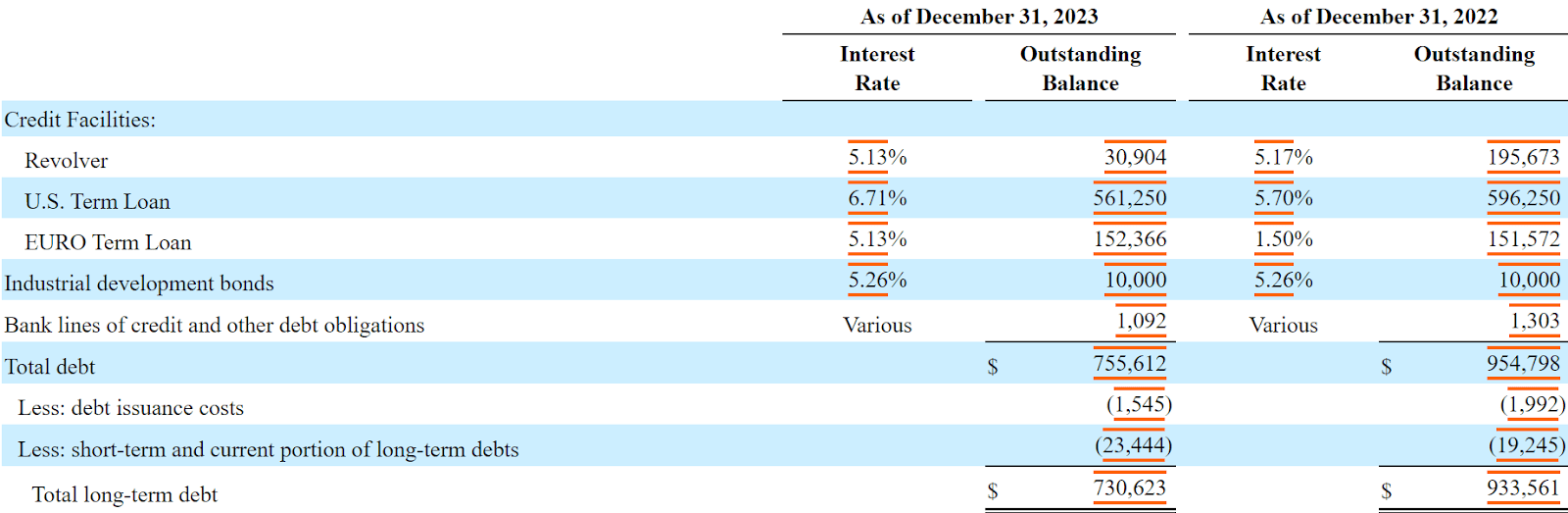

I did have a look at the contractual obligations reported by Quaker. In June 2022, Quaker and its subsidiary Quaker BV amended their credit facility, establishing a new $150 million Euro term loan, a $600 million U.S. term loan, and a $500 million revolver. The credit line was extended until June 2027, and eliminated the collateral requirement for large foreign subsidiaries. LIBOR has been replaced with SOFR. As shown in the table below, the interest rate applicable to the company's credit facilities stands at close to 5% to close to 7%. I used these figures for the calculation of the WACC in my different case scenarios.

Source: 10-k

The company appears to be successful in implementing value-based pricing initiatives mainly in the Americas region, where operating earnings increased in 2023. Clients seem to accept increases in the price of certain products, and inflation does not seem a problem for Quaker in the Americas. Under my base case scenario, I assumed that the company's pricing strategies will continue to bring net earnings growth.

This segment's operating earnings were $223.6 million, an increase of $47.4 million or 27% compared to 2021 primarily driven by higher margins as the Company's ongoing value-based pricing initiatives offset the ongoing inflationary pressures on the business. Source: 10-k

Quaker invests a significant amount of dollars in research and development that is expected to bring not only new formulae and compounds, but also chemical improvements or new products. As a result, I believe that the company may receive more attention from customers, and demand for existing products or new products may bring net sales growth.

The Company maintains approximately thirty separate laboratory facilities worldwide that are primarily devoted to applied research and development. In addition, the Company maintains quality control labs at each of its manufacturing facilities. Quaker research and development is directed primarily toward applied technology since the nature of the Company's business requires continual modification and improvement of formulations to provide specialty chemicals to satisfy customer requirements. Source: 10-k

Quaker incorporated sustainability into its business strategy. With a larger number of long-term environmental and social goals aligned with the UN sustainable development goals, the company recently launched green chemistry guides, and made relevant investments in renewable energy. In this regard, the agreement with Constellation is worth noting.

Given the total amount of investments in clean energy, I believe that the company could receive significant demand for its stock. As soon as more investors have a look at the type of clean investments made by Quaker, I would expect more attention from the investment community.

For every dollar invested in fossil fuels, about 1.7 dollars are now going into clean energy. Five years ago, this ratio was one-to-one. One shining example is investment in solar, which is set to overtake the amount of investment going into oil production for the first time. Source: iea

Very recently, Quaker launched a new stock repurchase agreement to buy close to $150 million shares. I believe that the repurchase of shares and the action of new investors acquiring shares of the company may accelerate the demand for the stock and enhance the stock price. I included this assumption in my base case scenario.

On February 28, 2024, the Board approved a new share repurchase program, authorizing the Company to repurchase up to an aggregate of $150 million of the Company's outstanding common stock. Source: 10-k

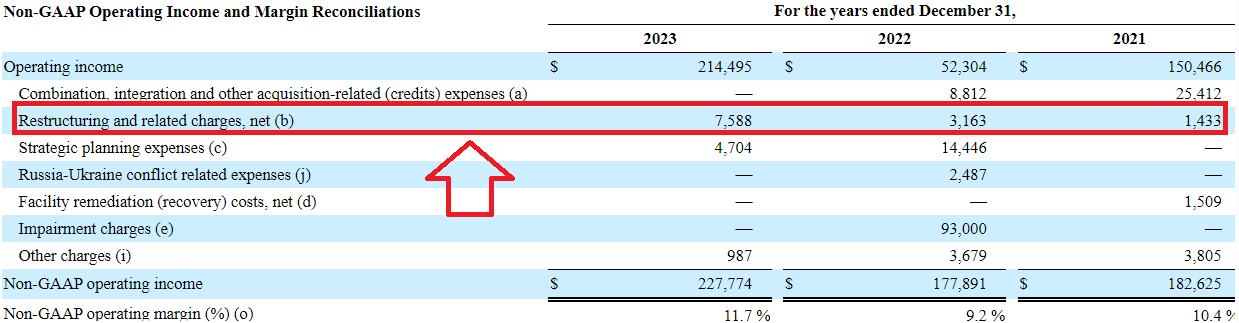

In 2021, 2022, and 2023, restructuring charges accelerated significantly from about $1.4 million in 2021 to $7.5 million in 2023. From 2021 to 2023, the Adjusted EBITDA margin increased substantially, and I believe that restructuring efforts made will most likely continue to have a positive effect on the EBITDA margin and the FCF margin.

Source: 10-k

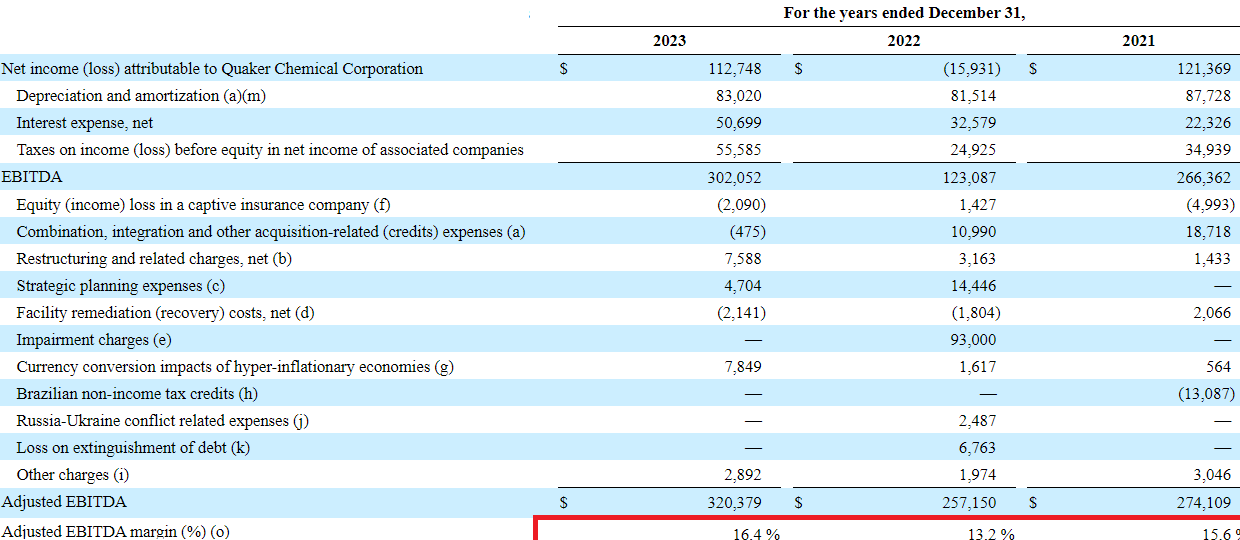

In the table below given in the last 10-k, Quaker noted increases in the Adjusted EBITDA margin from 15% to more than 16.3%. EBITDA also increased from $266 million in 2021 to $302 million in 2023.

Source: 10-k

In this regard, it is worth noting the strategic planning expenses executed in the last three years. According to the company's corporate documents, strategic planning is expected to enhance optimization processes.

Strategic planning expenses include certain consultant and advisory expenses for the company's long-term strategic planning, as well as process optimization and the next phase of the Company's long-term integration to further optimize its footprint, processes and other functions. Source: 10-k

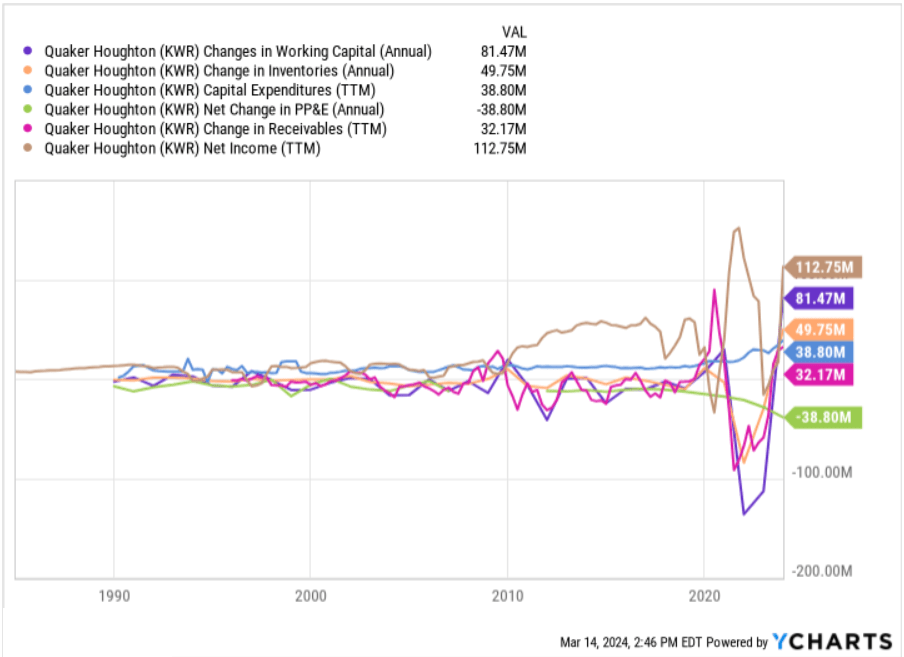

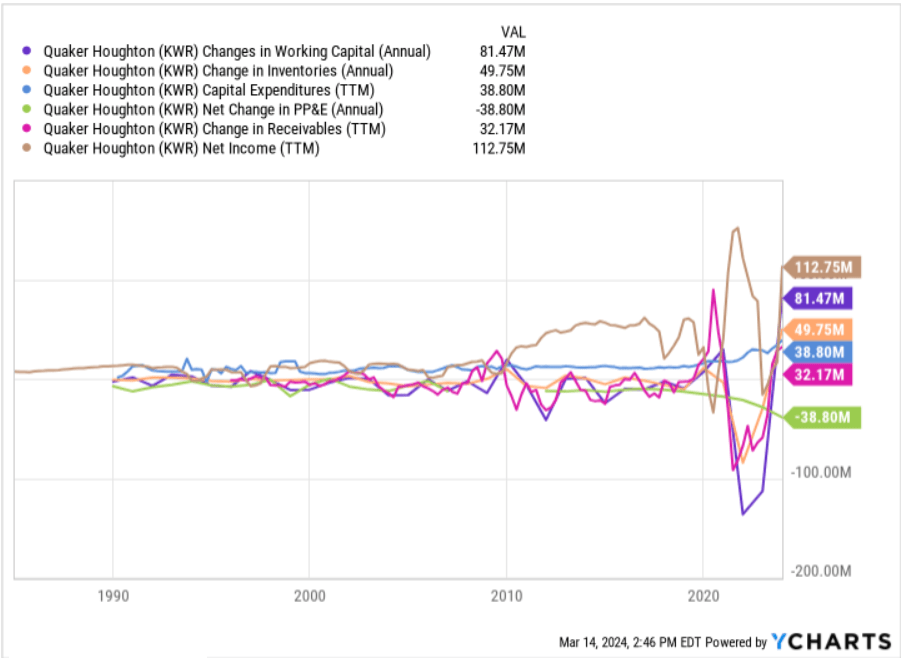

For the assessment of the base case scenario, I took a look at previous net sales growth, cost of sales, restructuring charges, and net income growth. In addition, I included some of my previous assumptions.

Source: YCharts

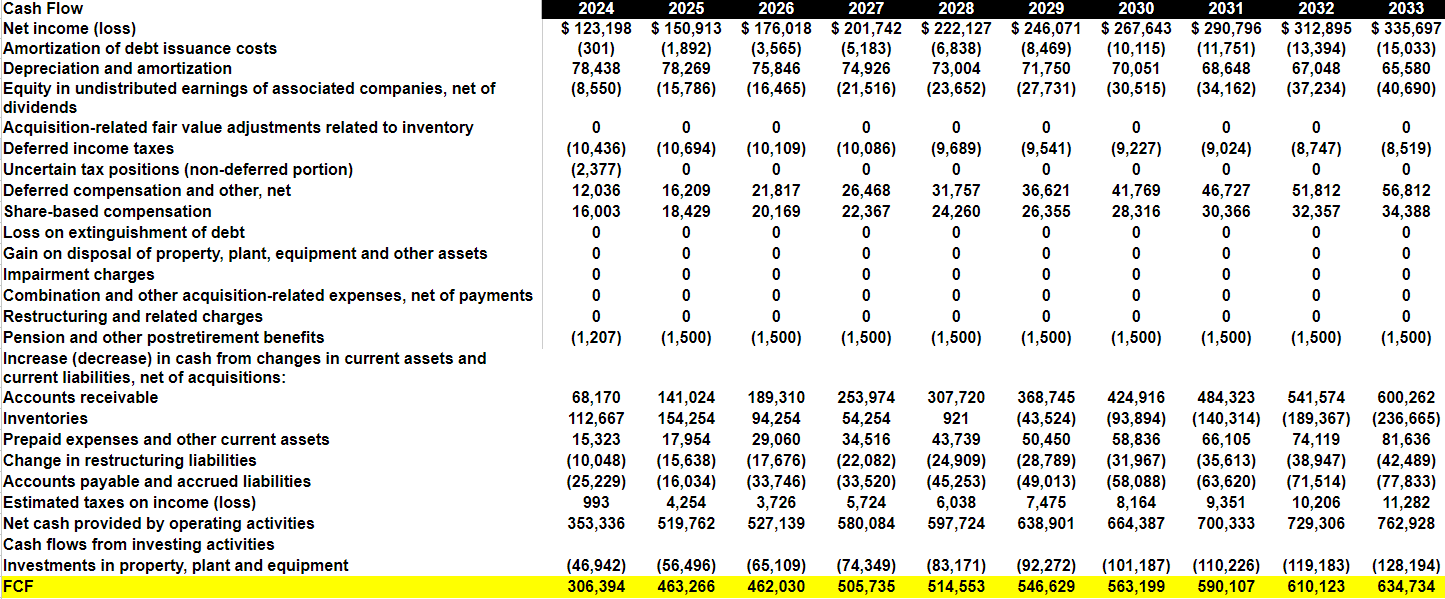

I included 2033 net sales of about $2768 million, with COGS worth $1444 million, which implied gross profit of $1323 million. In addition, I took into account selling, general, and administrative expenses of $800 million and integration and other acquisition-related expenses of about -$115 million. Finally, my results included operating income of about $637 million and net income of $335 million.

Source: My Expectations

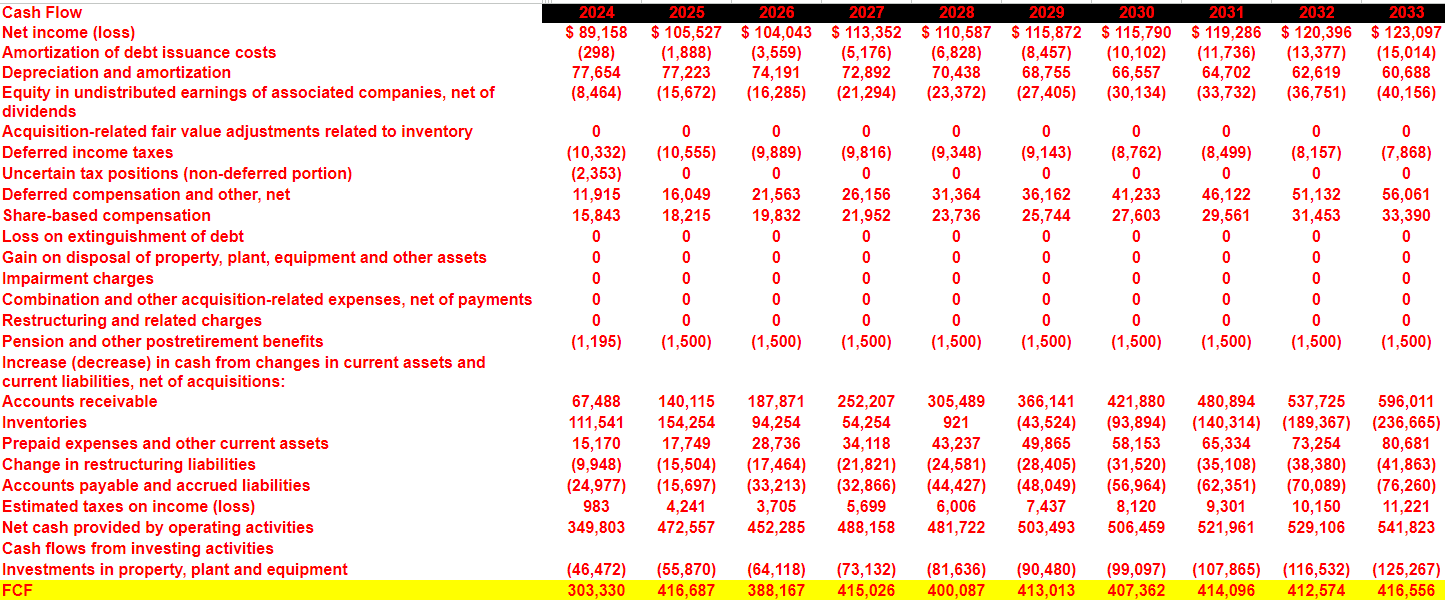

My cash flow expectations include 2033 amortization of debt issuance costs worth -$16 million, depreciation and amortization of about $65 million, and deferred income taxes of close to -$9 million.

Additionally, my cash flow expectations include 2033 share-based compensation of about $34 million, pension and other postretirement benefits worth -$2 million, and changes in accounts receivable of $600 million. Besides, taking into account 2033 inventories of -$237 million, changes in account prepaid expenses and other current assets of $81 million, and changes in restructuring liabilities of -$43 million, I also assumed changes in accounts payable and accrued liabilities of -$78 million.

My results also included 2033 CFO of $762 million. Moreover, with property, plant, and equipment of -$129 million, I obtained 2033 FCF of $634 million.

Source: My Expectations

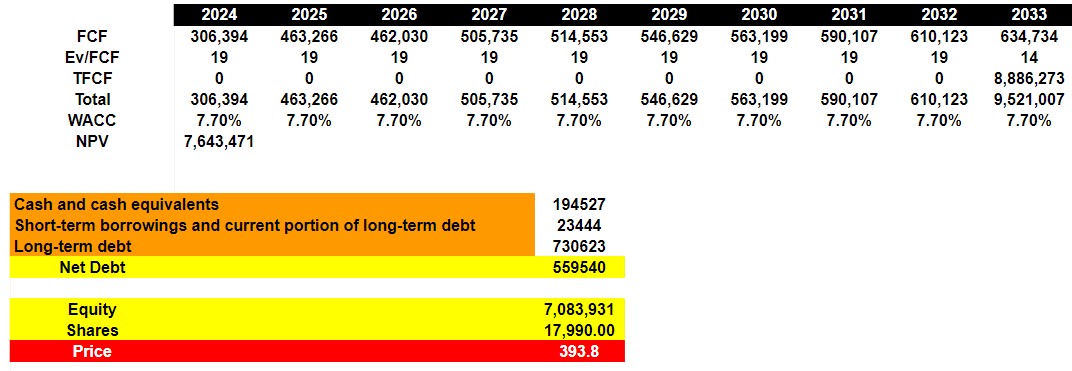

With the previous assumptions, I included an exit multiple of 14x FCF, which I think is quite conservative. Now, with a WACC of 7.7%, the implied enterprise value would be $7.6 billion. Subtracting net debt of 0.5 billion, the implied equity would be about $7 billion, and the fair price would be close to $393 per share.

Source: My Expectations

I included 2033 net sales of $2250 million, with cost of goods sold of $1361 million and gross profit close to $889 million. In addition, taking into account selling, general, and administrative expenses of $767 million, no impairment charges, and no restructuring charges, I obtained operating income close to $233 million as well as 2033 net income of $123 million.

Source: My Expectations

For the assessment of the cash flow statement, I took into account changes in working capital, changes in accounts payable, changes in inventory as well as capex, and other items included in previous annual reports.

Source: YCharts

My assumptions included 2033 amortization of debt issuance costs worth -$16 million, with 2033 depreciation and amortization of close to $60 million and equity in undistributed earnings of associated companies, net of dividends close to $-41 million.

Additionally, I included deferred compensation of $56 million, with share-based compensation of about $33 million along with pension and other postretirement benefits of about -$2 million.

Besides, I also assumed the following cash from changes in current assets and current liabilities. First, 2033 changes in accounts receivable would stand at close to $596 million, with changes in inventories of about -$237 million and prepaid expenses and other current assets worth $80 million.

Finally, I assumed accounts payable and accrued liabilities of about -$77 million and estimated taxes on income of about $11 million, which implied CFO of about $541 million. If we also take into account investments in property, plant, and equipment close to -$126 million, 2033 FCF would be about $416 million.

Source: My Expectations

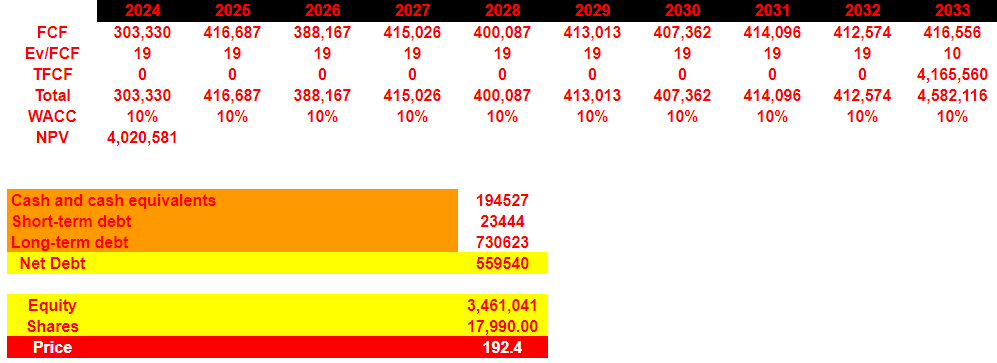

Under this case scenario I included a WACC of 10%, and Ev/FCF multiple of 10x, which implied a fair price of $192.

Source: My Expectations

In my opinion, Quaker faces risks associated with the business cycles of clients in sectors such as steel, automotive, and aerospace. In addition, reliance on global customer demand could expose the company to economic uncertainties and production constraints. Difficulties in differentiating and providing effective technical services also represent significant risks.

Quaker is situated in a competitive industry, alongside companies of similar and varied size. Although the precise position in each sector is difficult to determine, the company estimates its global leadership in industrial process fluids, standing out in the automotive and industrial markets as well as the production of steel and aluminum sheets. The competition presents diversity in product portfolios and technical services. The competitive key lies in supplying products and services that satisfy customer needs at an appropriate price and value, highlighting the importance of innovation and technical excellence.

Quaker presents a solid global business model with a significant number of products, serving various key industries. Diversification appears to be a key aspect that I believe will most likely bring new investors in. I also believe that recent successful pricing strategies in the Americas could bring new beneficial surprises in the coming years. If we also take into account ongoing restructuring efforts, the recently announced repurchase program, and investments in clean energy, the company appears to be a buy. There are some risks from dependence on business cycles, intense competition, and the need for differentiation, but I believe that Quaker appears cheap at its current price mark.