~UserGI15994093/iStock via Getty Images

~UserGI15994093/iStock via Getty Images

Kratos Defense (NASDAQ:KTOS) stock jumped following the presentation of its fourth quarter results. The stock has now climbed nearly 80% in a year and 50% since I marked KTOS expensive compared to peers with its 50x EV/EBITDA which likely was driven by investors looking for investment opportunities in companies with an unmanned aerial vehicles portfolio. In September 2023, I changed my rating on Kratos stock from Hold to Buy recognizing the stretched valuation as well as the strategic strength of its product portfolio. Since marking the stock a buy, it has continued to outperform the market with a 38% return compared to a 12.5% return for the broader markets.

In this report, I will analyze the most recent earnings as well as the guidance and I will assess whether there is any need to alter my rating or price target.

Kratos Defense & Security Solutions

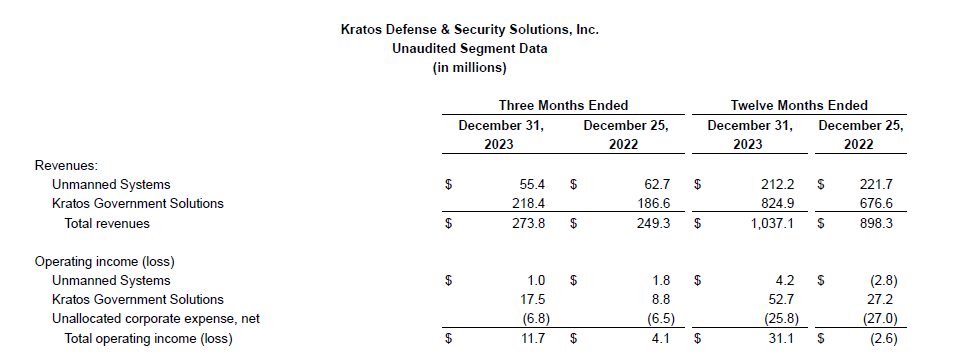

During the fourth quarter, Kratos booked revenues of $273.8 million or nearly 10% growth. Unmanned Systems revenues declined 12% to $55.4 million, but this was more than offset by 17% growth to $218.4 million in the KGS segment. Despite positive contributions of $6.4 million to the revenues from the acquisition of Sierra Technical Services, Unmanned Systems revenues declined due to lower tactical drone revenues. KGS revenues increased by strength across its entire product portfolio. For the full year, the company reported revenues of $1,037.1 million, marking a strong 15.5% increase. Unmanned Systems revenues declined 4.3%, once again reflecting lower tactical drone activity partially offset by inorganic growth from the acquisition of Sierra Technical Services. KGS revenues increased nearly 22%, which was driven by demand strength in all of the company’s areas of expertise.

Operating income for the quarter increased from $4.1 million to $11.7 million while adjusted EBITDA grew from $19.2 million to $29.1 million reflecting a margin of 10.6% compared to 7.7% same quarter last year. Adjusted margins for the Unmanned Systems business remained stable despite lower revenues. Kratos had guided for fourth quarter revenues of $237 million to $257 million, operating income of $4 million to $7 million and Adjusted EBITDA of $19 million to $23 million. So, the fourth quarter came in significantly stronger than projected and that was driven by some milestones that were expected to be reached in Q1 2024 being reached a quarter earlier. For the full year, operating income increased from a $2.6 million loss to a $31.1 million profit which compared favorably to the guidance of $25 million to $28 million. Adjusted EBITDA came in at $95.4 million compared to $70.7 million a year earlier with margins expanding from 7.9% to 9.2%. Free cash flow came in at $12.8 million whereas a cash flow usage of $20 million to $25 million was expected. The strong cash flow performance was driven by customer milestone payments that came in a quarter earlier than expected.

Overall, Kratos’ financial results showed strong performance and primarily put on display the appeal of the product portfolio of Kratos Governmental Services.

Kratos Defense & Security Solutions

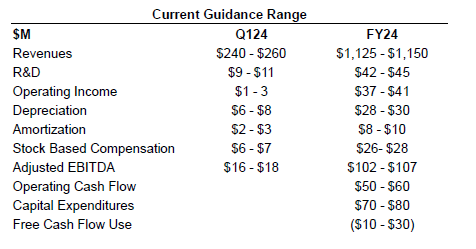

For the full year, Kratos expects 8.5% to 11% revenue growth with adjusted EBITDA of $102 million to $107 million indicating margins of 9.1% to 9.3%. Compared to last year, adjusted EBITDA is set to rise 7% to 12.5% on stable margins. Free cash flow is expected to be negative $10 million to negative $30 million. This is partially driven by the absence of some customer milestone payments that already have occurred in Q4 2023. Capex remains elevated as Kratos is self funding production of Valkyrie drones ahead of contract award and anticipated demand and sales. Furthermore, the company is expanding a production facility in Israel in line with customer demand which will increase capex by $10 million to $13 million. Other capex drivers include the establishment of a Material Production Center of Excellence and expansion of the global satellite sensor network. Kratos entered 2024 with a $1.2 billion backlog and $11 billion in contract opportunities. Kratos sees a set of growth drivers in 2024 that include turbojet, turbofan, and rocket engines for unmanned aerial drones, loitering munitions, cruise missiles, hypersonic systems, supersonic platforms and space. I like the fact that the growth drivers are not one or two platforms, but multiple areas where growth can be realized demonstrating the diverse and attractive product portfolio.

Kratos expects Q3 and Q4 to be significantly stronger as defense contractors are currently operating under a Continuing Resolution Act or CRA since the US Government budget was not passed by the first of October 2023. Under the CRA, no new contracts or modifications to contracts is permitted. The CRA expires by early March and Kratos expects the CRA will be resolved at that time at which point government contract officers can get to work on new contracts and contract modifications.

The Aerospace Forum

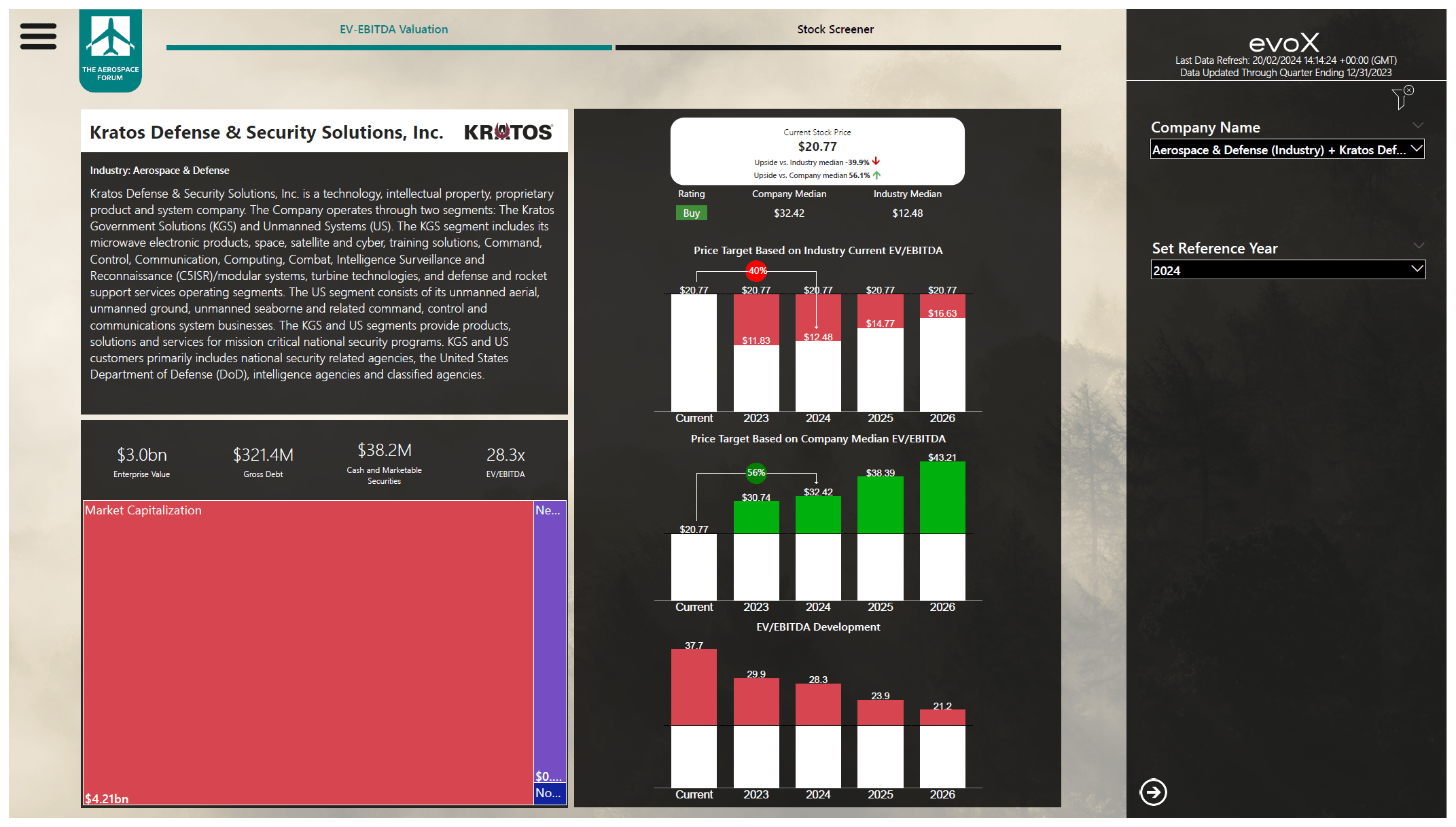

Kratos stock can be quite challenging to put a price target on because the stock is currently trading at an EV/EBITDA multiple that's significantly higher than that of peers. The reason most likely is that there aren’t that many companies with significant exposure to hypersonic motors, rocket motors and unmanned aerial vehicles. So, I can see why Kratos stock has a richer valuation. I don’t believe that Kratos stock will be trading in line with peers unless there is a major correction on the stock market. After implementing the Kratos balance sheet as well as forward projections for debt reductions, free cash flow and EBITDA the stock price target would imply 56% upside with a price target of roughly $32.40. If we average the industry multiple with the company median the price target would be $22.45 which would imply around 9% to 10% upside. As a result, I am maintaining my buy rating as I believe Kratos has an attractive and in-demand portfolio, its elevated CapEx levels support growth of the company and on the longer term the EV/EBITDA is tapering. I previously had a $22.35 price target for 2024, so with the most recent results and projections in place there is a minor bump in the price target.

Kratos posted strong fourth quarter and full year earnings and 2024 is shaping up to be a great year for the defense contractor as well with a $1.2 billion backlog and $11 billion in contract opportunities. With exposure to hypersonics, rocket motors, turbofans, drones and aerial target drones I believe Kratos has an extremely attractive position in the defense landscape with future opportunities for pairing fighter jets with drones such as the Kratos XQ-58 Valkyrie. As a result, I'm maintaining my buy rating for KTOS stock noting that in case the EV/EBITDA levels remain significantly elevated there is upside beyond the price target that I have put.