tenten/iStock via Getty Images

tenten/iStock via Getty Images

Krystal Biotech (NASDAQ:KRYS) continues to make improvements with their Vyjuvek launch for the treatment of dystrophic epidermolysis bullosa (DEB). In my last update, I highlighted Q3 earnings and believed that, despite small numbers, the launch appeared to be going well. Subsequently, the stock was rated a "Strong Buy." The company announced Q4 earnings on Monday, prompting a reevaluation of Krystal's stock.

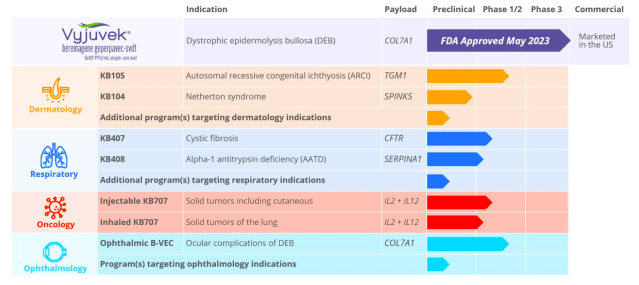

When a drug is new to the market, I like to stay on top of the most recent and relevant treatment recommendations. This helps me project the trajectory of drug launches. Glancing at current recommendations (per UpToDate), Krystal's Vyjuvek is one of two "novel topical wound therapies" utilized for DEB. The other, oleogel-S10 (birch triterpenes), is approved only in the EU. Vyjuvek, unlike oleogel-S10 (a herbal medicine), targets the underlying cause of the condition by delivering a functioning COL7A1 gene to skin cells.

Krystal's Q4 report builds on the momentum it established in the previous quarter. In Q4 and FY2023, Vyjuvek's net product revenue in the US was $42.1 million and $50.7 million, respectively. Gross margins were a sparkling 93%. Krystal also stated that patient compliance remains high, at 96% at the end of the year. This suggests that patients are having good experiences with Vyjuvek.

Surprisingly, given the company's R&D efforts outside of Vyjuvek (see pipeline below), Krystal reported a net income of $8.69 million for the quarter, compared to a loss of $32 million for the same period in 2022.

Krystal Biotech

This indicates that the corporation is very frugal in its activities, which is respectable in this industry. Surprisingly, SG&A spending remained relatively flat year over year. This emphasizes patient and prescriber demand over big marketing expenditures.

To wrap things up, Vyjuvek's trajectory, to date, is very positive. Estimates for Vyjuvek's peak annual revenue range from $700 million to $900 million. I believe this can be reasonably achieved. If so, Krystal, valued at $3.89 billion in market capitalization (at writing), does not appear expensive considering Vyjuvek will benefit from years of market exclusivity and DEB treatment options are sorely limited.

Turning to Krystal's balance sheet, the aggregation of 'cash and cash equivalents', 'short-term investments', and 'long-term investments' totals approximately $593.1 million, with $358.3 million in cash and cash equivalents, $173.9 million in short-term investments, and $61.9 million in long-term investments. When comparing assets to debts, notable liabilities include accounts payable ($4.1 million), the current portion of lease liability ($1.5 million), and accrued expenses and other current liabilities ($27.5 million), totaling current liabilities of $33.1 million. The current ratio, calculated as total current assets divided by total current liabilities, stands at approximately 17.8, indicating a strong liquidity position.

The company's net cash used in operating activities was $88.8 million over the last year, which, when annualized, suggests a monthly cash burn of approximately $7.4 million. This calculation provides a cash runway of roughly 80 months, assuming constant burn rates and no additional cash inflows. It's crucial to note that these values and estimates are based on past data and may not fully predict future performance.

Given the significant cash reserves and the company's current burn rate, the likelihood of requiring additional financing in the next twelve months seems low. However, this assessment depends on the company maintaining its current operational efficiency and cash burn rate.

Glancing at cash flows suggests Krystal is actively managing its capital, balancing between investing in its future and maintaining a robust balance sheet, as evidenced by its strategic investments and financing activities.

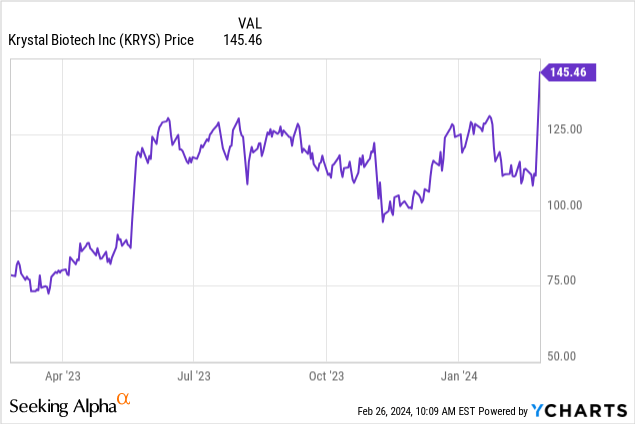

According to Seeking Alpha data, analysts are projecting significant growth for Krystal, expecting revenue to surge to $381.11 million by 2025. Prior to Monday, stock momentum revealed underperformance relative to SPY over most timeframes, except for a notable +42.29% increase over the past year.

Per Fintel, short interest stands at 2,029,257 shares (9%), indicating a high level of investor skepticism or speculative interest. Institutional ownership is dominant at 88.26%, with a notable increase in positions by 105 holders, totaling 3,181,382 shares, compared to 22 sold-out positions, shedding 236,338 shares. Significant institutions include Avoro Capital Advisors, Fmr, and Redmile Group. Insider activity over the past three and twelve months shows a net sell of 102,500 and 642,979 shares, respectively, suggesting cautious or profit-taking behavior from insiders.

Given these dynamics, the sentiment around KRYS could be characterized as "adequate," reflecting solid growth prospects tempered by cautious insider and institutional actions.

Today's market response following Q4 (stock is up over 30% intraday) tells you all you need to know. Vyjuvek launch is going exceptionally well and Krystal is already making a profit. Importantly, Vyjuvek serves as a validator for their platform, so other clinical assets could, too, become successful drugs. Krystal remains a "Strong Buy" at these prices. In fact, my confidence has increased since my last update.

Looking ahead, there are some risks to look out for. Drug launches for rare diseases are notoriously difficult to project, and hiccups can especially occur in the early stages. If next quarter, for example, falls below projections, Krystal's stock could fall. Moreover, any failure in clinical trials in the pipeline outside Vyjuvek could place pressure on Krystal's stock.

As of right now, it seems reasonable to maintain optimism about Krystal and believe the Vyjuvek launch will continue to be successful.