xxwp/iStock via Getty Images

xxwp/iStock via Getty Images

Kura Sushi (NASDAQ:KRUS) recently shared its fourth-quarter earnings on November 9th. Following this report, their stock took a bit of a hit, dropping by 10%. This isn't a new trend though; since reaching its high point in July, the stock has actually fallen back by a whole 50%. It looks like a big part of this downturn is due to the market feeling pretty pessimistic about the restaurant industry as we head into 2024.

In July, we kept our buy recommendation intact, but the stock fell by 45%. The restaurant biz got stuck in a major funk last 6 months. With all the gloom and doom, investors started fleeing any restaurant stock that looked overpriced. High-flying stocks got brought back down to earth real quick.

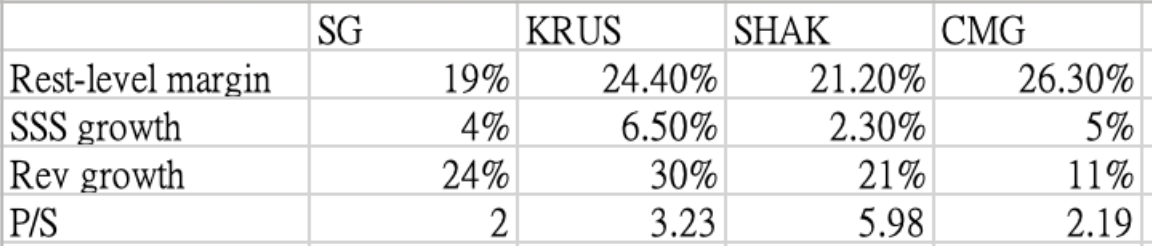

But we think the negativity has gone too far when it comes to our sushi fave, Kura Sushi. In the fourth quarter, their profit margins at the restaurant level hit 24.4%. That's comparable with the restaurant leader Chipotle (NYSE:CMG). In fact, Kura only has a tiny sliver so far of the $29 billion U.S. Japanese restaurant market. We're talking less than 1% market share. So there's still a ton of growth potential ahead. Based on their affordable pricing, we think they've got plenty of room to expand.

The recent sell-off seems overblown to us. Kura's growth story is far from over. We're sticking with a buy rating and staying bullish on this name. The market gloom won't last forever, and Kura will keep on growing. We just need to remember that not every restaurant stock is created equal. This one still has some major growth opportunities on the horizon.

Restaurant stocks have been struggling these past few months.

Seeking Alpha

As we talked about in our last article on Sweetgreen, the bear market has been ruthless towards highly-priced restaurant stocks, especially those facing concerns about hitting a growth plateau. Sweetgreen got slammed because investors worried their expansion was tapped out and growth would stall.

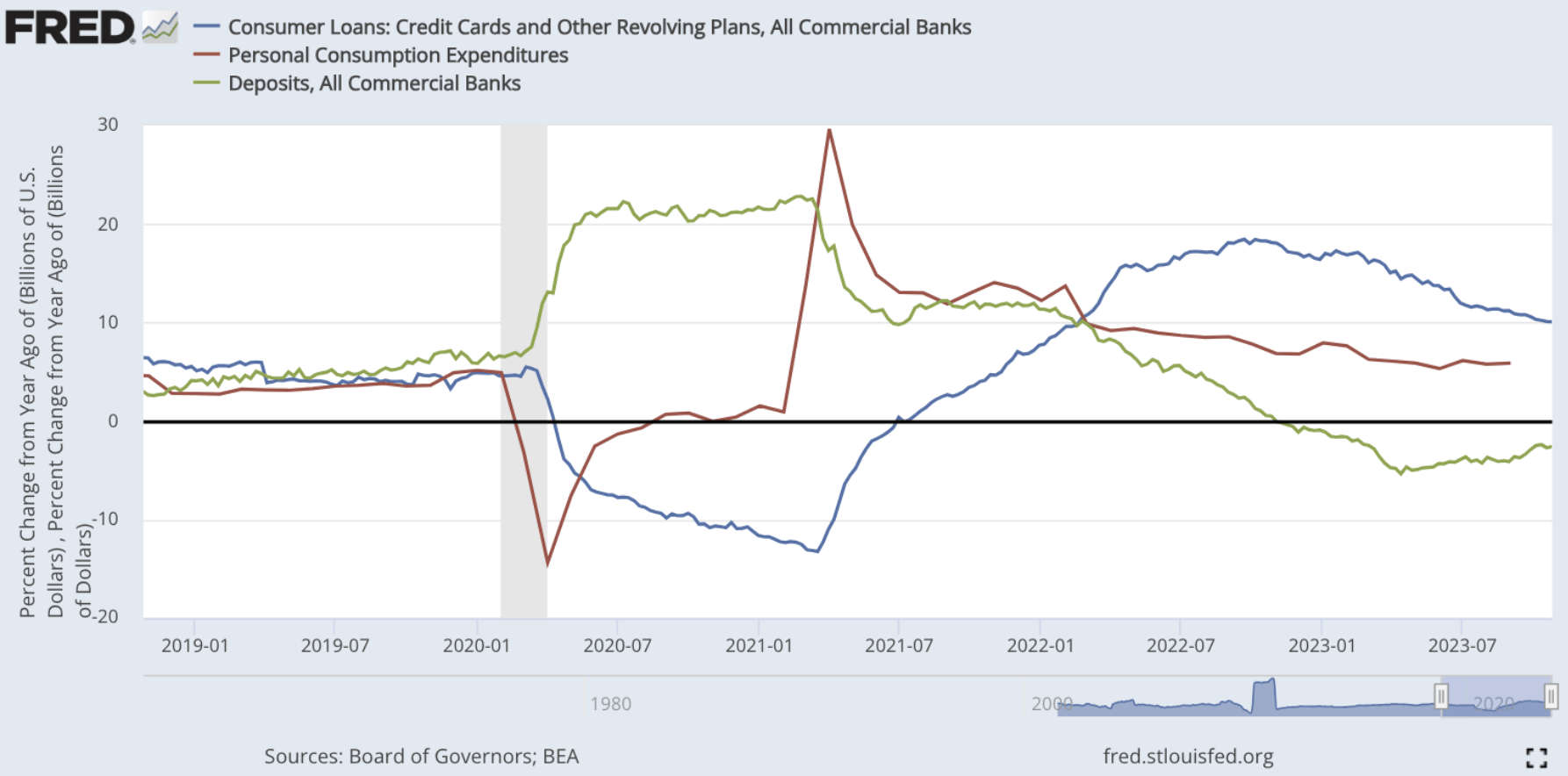

We view this negative sentiment as having a negative impact on the high valuations of high-growth restaurant companies. Restaurant companies are still experiencing strong growth in their financial results this year. However, as the chart below suggests, the growth rate of consumer spending (red line) has been gradually trending down over the course of 2023. Further, US consumer credit card balances (blue line) have also slowed down as banks have started to slow lending in response to negative deposit growth (green line). This softening consumer environment is likely to slow down the growth of restaurant companies.

FED

Kura's stock is declining to nearly reach its $50 per share resistance level.

Seeking Alpha

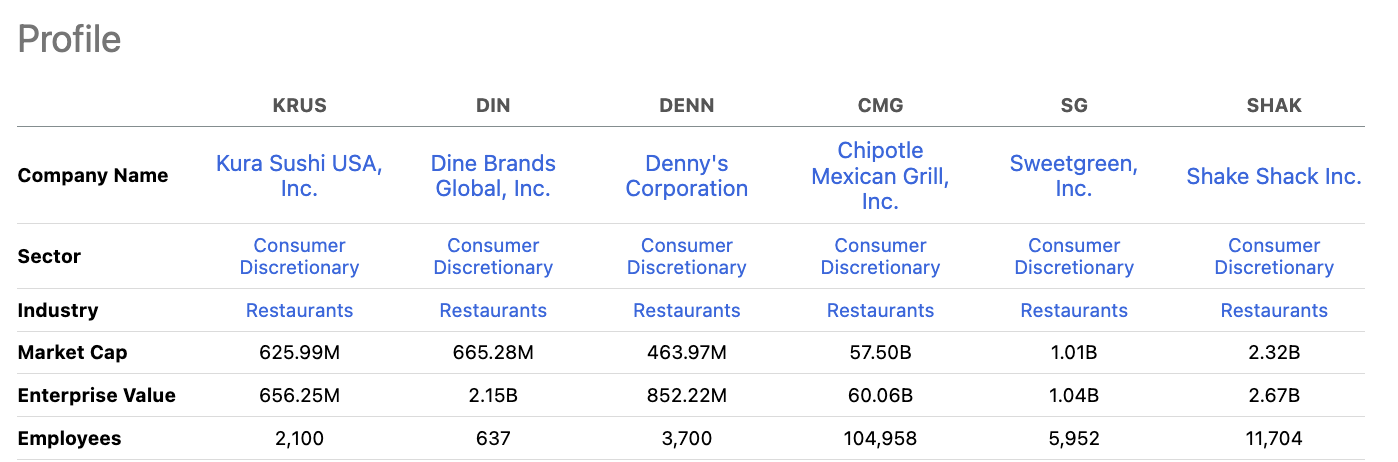

We believe that Kura's comparatively high P/S ratio when compared to its high-growth peers, like Sweetgreen and Chipotle, is probably going to be the reason for the stock's correction.

Companies reports, LEL

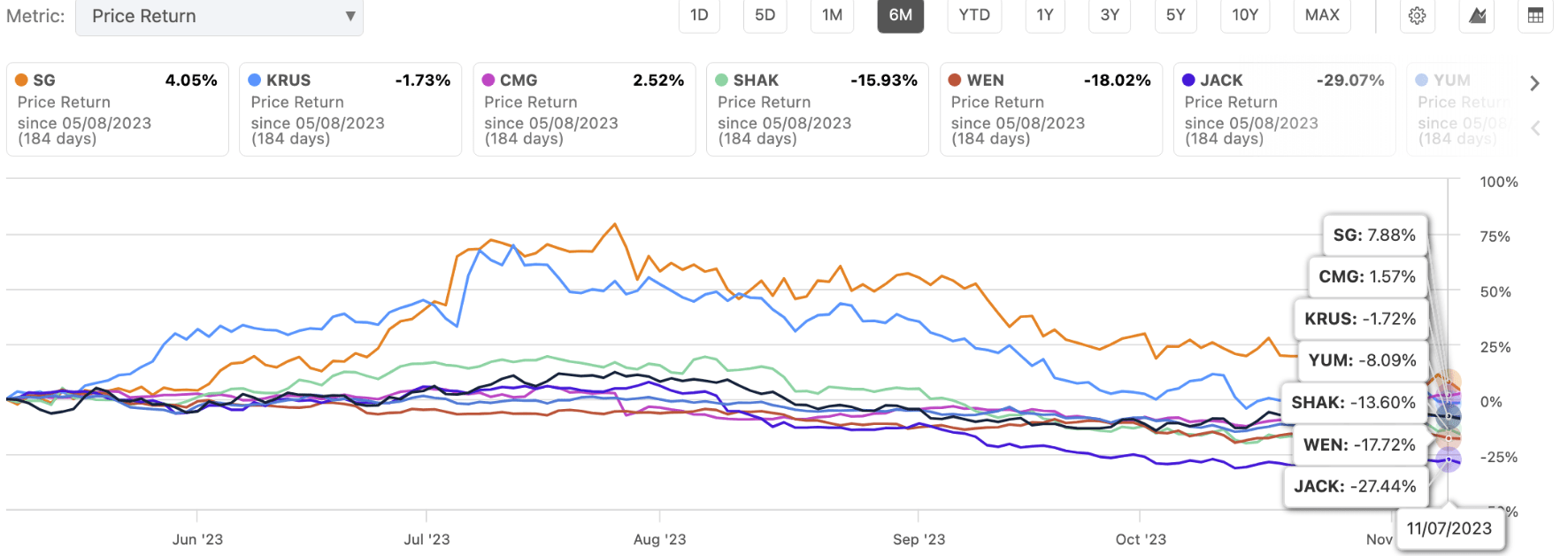

Kurs ranked in the bottom of 6-month stock return in this group, returning -1.7%, while Chipotle and Sweetgreen are still in the black, and Shack Shake has the highest stock return, returning -13%. Kura's stock may therefore decline further if the market keeps reducing the restaurant group's valuation.

The P/S ratio of the company's stock was still above 3x, indicating that the management was still projecting a 30% growth in revenues by 2024. This partially explains its high value.

Fiscal Year 2024 Outlook

Total sales between $238 million and $243 million;

General and administrative expenses as a percentage of sales to be approximately 14.5%; and

11 to 13 new restaurants, with average net capital expenditures per unit of approximately $2.5 million.

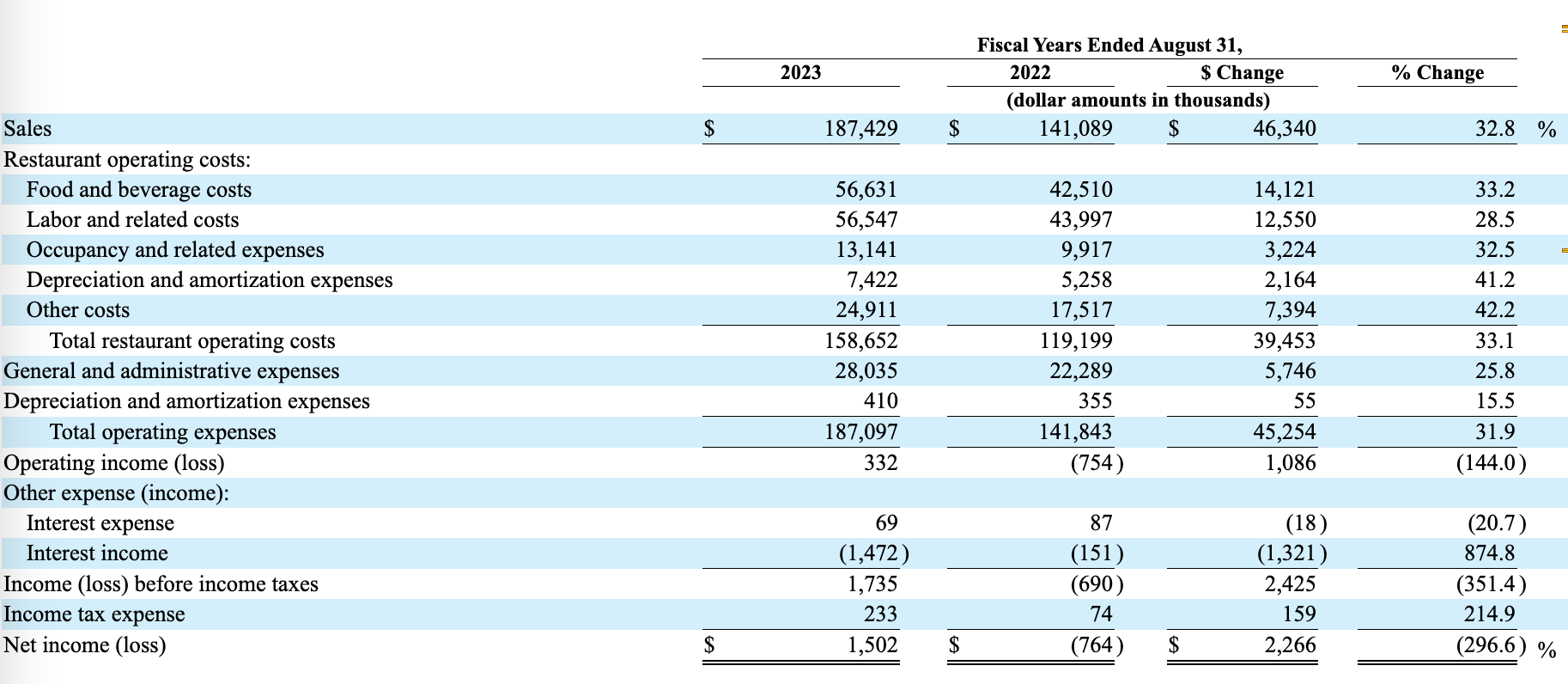

The company also maintains a strong restaurant-level profit margin at 24.4%. The company has only 54 locations in the US and doesn't have strong economies of scale as Chipotle. However, it was able to achieve a similar level of margin and thus is very impressive. One of the reasons is that the company received strong support from its parent company Kura Japan, a top 3 sushi chain restaurant in Japan. Leveraging the strong bargaining power of its parent, the company is able to save on materials purchase costs. By using tech and its supply chain leverage, Kura managed to actually lower food and labor costs last year.

KRUS

The company posted 32% sales growth last year even with high inflation nipping at their heels. It is because their prices are still pretty easy on the wallet. A plate of their Bluefin Toro sushi goes for just $3.70. And you can get beef Ojyu for $11.40.

KRUS

For eating out, that's still affordable. So while other restaurants jacked up menu prices to keep up with rising costs, Kura Sushi kept prices affordable. Customers clearly appreciated that, with sales growth staying strong. Their reasonable price points should keep customers rolling in, which gives investors more confidence in this growth story.

Looking at the numbers, Kura has a large upside to grow. The Japanese restaurant market in the US is worth $29 billion. Kura currently only has a market share of 0.7%. Even as sushi demand slipped a bit in the US last year, Kura put the pedal to the metal and grew sales by 120%.

The company's growth rate has slowed to 32% in 2023. This is likely due to the larger base in 2023 compared to previous years. However, the company still expects 30% growth in 2024, so we don't think Kura's growth story is over. Looking at absolute numbers, Kura remains very small compared to industry peers, with ample room for expansion in the U.S. market. The recent stock pullback has created a buying opportunity for investors, in our view.

Seeking Alpha

In our previous article, we mentioned Kura was expanding into Texas where supply chains and consumer preferences differ from coastal regions, creating uncertainty around performance. However, management said some Texas restaurants outperformed while some underperformed versus California, suggesting a more neutral outcome. This indicates Kura may be more open to building new stores in middle America, a positive for investors.

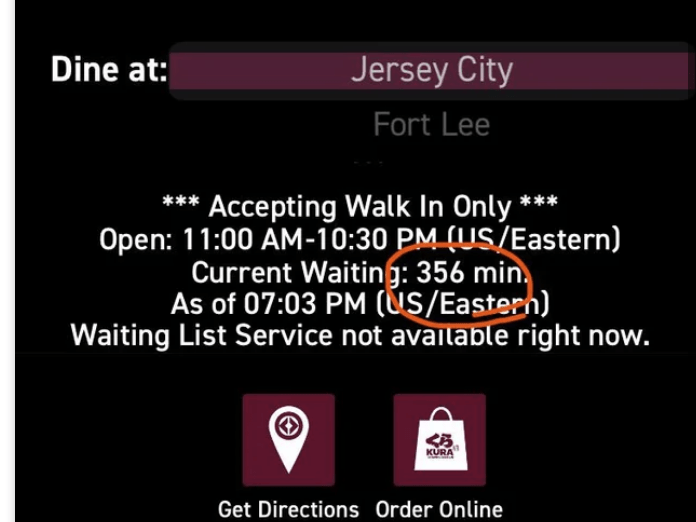

One value proposition Kura is working on is reducing customer wait times. They built an app allowing customers to view estimated wait times at each location.

KRUS

This improves customer experience and likely better converts diners since wait times can be an issue, especially for dine-in.

But we do know and the information we do have is that wait times are more accurate. And we do know that the over quoting or the underquoting of people by 0.5 hour or more has decreased substantially to where we – some restaurants could have been in the 20% to 25% range of people being misquoted by half an hour or more on their wait times.

While macro risks could cause restaurant stocks to underperform, we think Kura's relatively small market share means it hasn't plateaued. We continue to see long-term potential thanks to a strong value proposition, industry-leading unit economics, robust parent company support, and early robot server deployment. The recent pullback has created a buying opportunity in our view, and we remain bullish on the stock.