sergeyryzhov

sergeyryzhov

Note:

I have covered Kornit Digital Ltd. (NASDAQ:KRNT) previously, so investors should view this as an update to my earlier articles on the company.

On Wednesday, leading digital textile printing solutions provider Kornit Digital Ltd. or "Kornit" reported fourth quarter and full year 2023 results largely in line with management's projections:

Company Press Releases

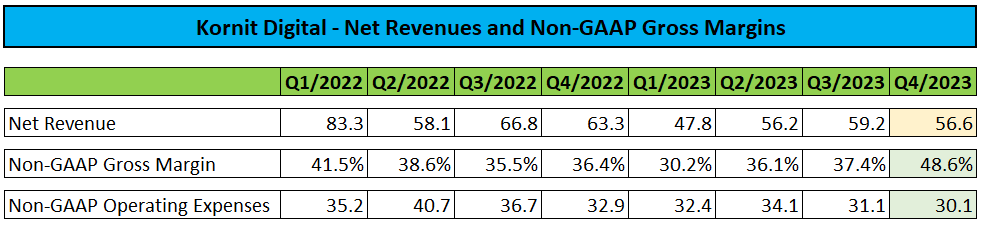

While revenues came in at the lower end of the provided range, profitability actually exceeded the company's expectations, albeit just slightly.

System sales continue to be impacted by macroeconomic and industry-specific headwinds:

Company Presentation

On the flip side, healthy demand for consumables and ongoing cost-cutting efforts resulted in non-GAAP gross margins reaching new two-year highs:

Company Press Releases

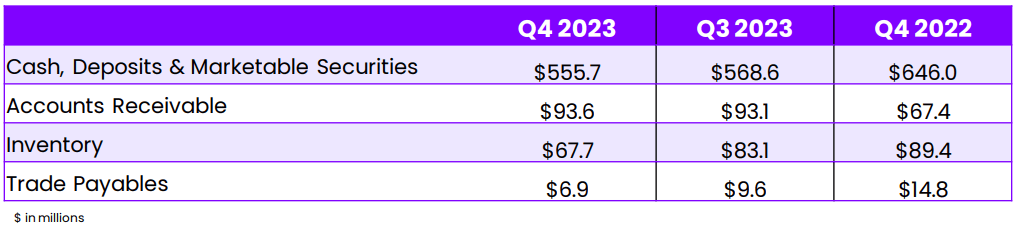

In combination with non-GAAP operating expenses dropping to new multi-year lows and a sizeable reduction in inventories, Kornit managed to generate $2.6 million in cash flow from operations in Q4.

Company Presentation

During the quarter, the company repurchased another 1.1 million shares for $19.0 million, thus resulting in the company's cash position decreasing by $12.9 million sequentially. The remaining balance under Kornit's $75 million share repurchase program calculates to approximately $19.2 million. On the conference call, management stated its intent to continue share repurchases in the current quarter.

Unfortunately, business headwinds are expected to persist for the time being, thus resulting in only modest growth expectations for this year and the decision to double down on cost savings initiatives:

In the fourth quarter, we took decisive actions to advance these cost savings initiatives which resulted in a $19.1 million restructuring charge. This charge supports our strategy to align our cost structure with our revenue expectations and to enable operating leverage as we return to growth. Included in this restructuring is a meaningful workforce reduction, a consolidation of facilities and a phasing out of our legacy platforms. We expect this restructuring plan to save approximately $20 million in operating expenses during 2024 versus the full-year 2023. (...)

As a result, management expects to generate positive cash flow from generations in 2024:

As we discussed on our last earnings call, the consumer environment remains uncertain, which with regard to system sales impacts our customers' purchasing appetite and thus our visibility.

Additionally, we continue to expect to face a challenging macro environment in 2024, similar to what we faced in 2023. While we will work proactively with our customers, invest in our product portfolio and improve our operating model, we acknowledge that these macroeconomic headwinds will weigh on our ability to convert leads and plan confidently.

With that said, we continue to expect modest growth and modest profitability in 2024 on a full year basis. We are also expecting to deliver positive cash from operations in 2024 on a full year basis.

However, management does not expect the seasonally weak first quarter to show meaningful year-over-year sales progress, but the above-discussed restructuring measures should benefit the company's adjusted EBITDA margin:

We currently expect revenues for the first quarter of 2024 to be between $43 million and $48 million and adjusted EBITDA margin to be in the negative 16% to negative 26% range.

Last month, Kornit announced the commercial availability of its new Apollo direct-to-garment digital textile printing solution.

Kornit Digital

While 2024 is anticipated to be more of a ramp year, management expects Apollo sales to accelerate in 2025.

In addition, Kornit is piloting a new sales approach for the Apollo, which essentially appears to be a lease model with required minimum consumption levels:

This will create more predictability and visibility both for us and for our customers that are using it. It will create shorter sales cycles and improve our opportunity to address screen as a whole. This business model is going to generate around $1 million per unit per year and this is kind of the minimum. We expect it even to do more than this $1 million. The machine is able to bring much more than that.

While there's nothing wrong with generating recurring, high-margin sales, the new approach will result in lower upfront revenue recognition and some related pressure on cash flows.

However, with the lease/subscription offering currently limited to the new Apollo system, I do not expect a major impact on Kornit's financial statements this year.

In fact, I strongly support the decision to leverage the company's very strong cash position in order to attract new customers to Kornit's ecosystem and generate a sticky, high-margin recurring revenue stream.

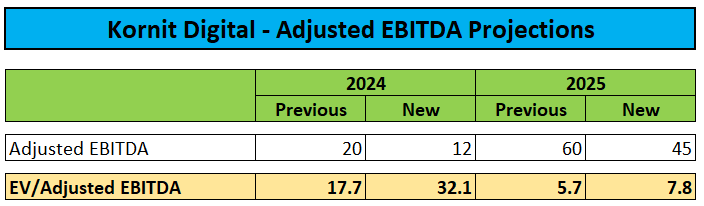

The ongoing business headwinds anticipated by management have caused me to lower my adjusted EBITDA estimates for both 2024 and 2025:

Author's Estimates

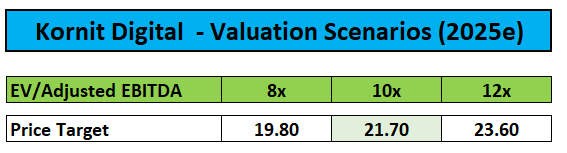

Based on my revised estimates, the company is trading at close to 8x my 2025 EV/Adjusted EBITDA estimate, which is still below the corporate average in the machinery sector.

Assigning an EV/Adjusted EBITDA multiple of 10x would yield a $21.70 price target for the shares, or approximately 15% upside from current levels:

Author's Estimates

While Kornit Digital's near-term prospects remain muted, the company is expanding its product portfolio and piloting a new sales approach, which could result in further margin accretion over time.

In addition, Kornit has doubled down on its cost reduction efforts, which should help the company to deliver positive operating cash flow and modest profitability this year even without meaningful sales growth.

Due to ongoing business headwinds, I have reduced my adjusted EBITDA estimates for both 2024 and 2025, thus resulting in a lower price target for the shares.

Given the limited upside following Wednesday's 12% rally, I would prefer to wait for a pullback before potentially entering a position in Kornit Digital's shares.