Joe Raedle

Joe Raedle

Over the past year, Carvana Co. (NYSE:CVNA) has outperformed the market with the stock up 1050% over that period against a 31.8% increase in the S&P 500. The bullish sentiment surrounding Carvana is due to the company restructuring the majority of its debt which gives it more time to deal with it. That said, Carvana is extremely overvalued at its current valuation, in my opinion, due to the rising delinquency rates among auto loan borrowers.

In addition, the improvement in Carvana’s financial performance last year is overstated in my opinion since it sacrificed growth for profitability. However, I don’t believe the company’s improvement justifies its current valuation as this improvement was only due to a one-time gain on debt extinguishment, inventory drawdown, and selling more loans than originated, all unsustainable factors. As such, I’m rating Carvana as a strong sell with a price target of $17.06 per share, implying 78% downside from current levels.

Auto loan delinquency rates reached 7.7% in 2023, their highest level since 2010. At the same time, auto loans that are 90+ days delinquent increased to 2.66% in Q4 2023 compared to 2.22% in Q4 2022.

With that in mind, it should be noted that a fundamental part of Carvana’s business model depends on the health of the auto loan market. When Carvana makes a car loan to a buyer, it packages it with other loans and sells the debt to investors as Asset Backed Securities (ABS). Other auto lenders also sell the loans to investors. However, a key difference between these auto lenders and Carvana is that they keep the debt on their books, while Carvana doesn’t retain the debt and book gains on cash sales.

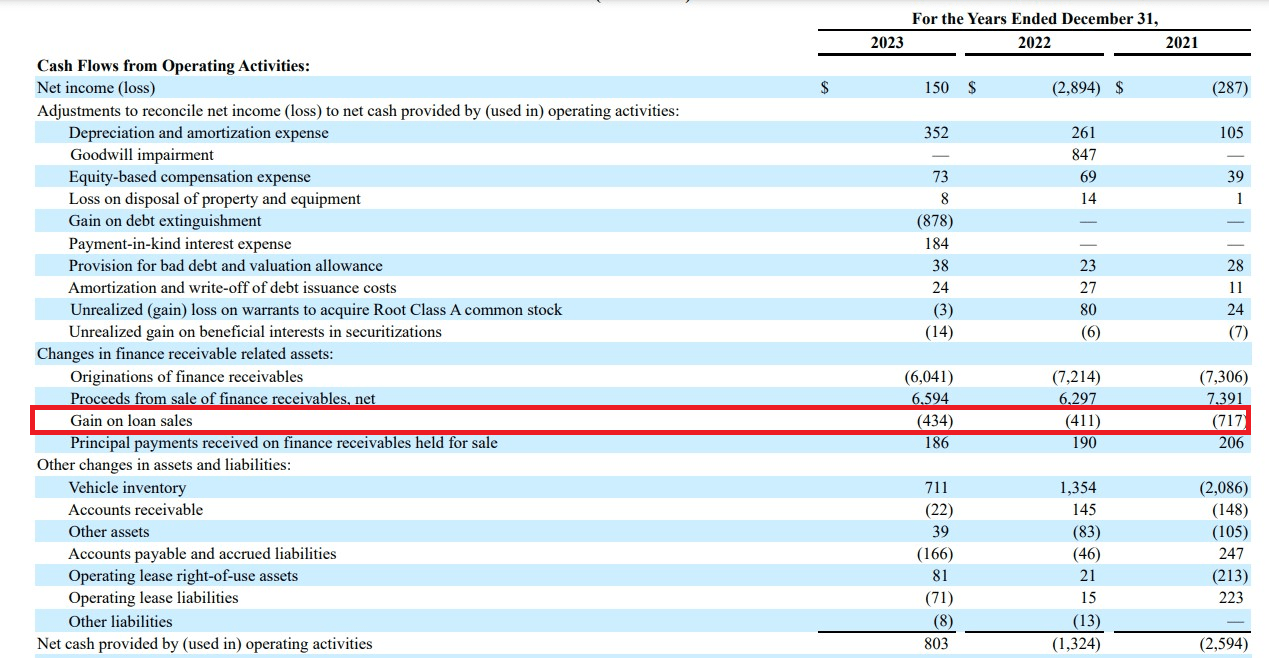

This leaves Carvana vulnerable to changes in the debt market conditions since if its loans start to sour, investors will not be willing to pay the same premium on these loans. As is, Carvana gained $434 million from loan sales in 2023.

10-K Filing

Based on this, I expect Carvana to suffer this year from the ongoing weakness in the auto loan ABS market. The high auto loan delinquency rates are impacting auto lenders as Ally Financial’s, Carvana’s main financing partner, net charge offs represented 1.77% of its loan portfolio in 2023 compared to 1.16% in 2022.

A recent report by S&P global shows that collateral performance slumped in 2023 due to record-high delinquencies and historically-low recoveries in the prime and subprime segments, with most subprime issuers recording losses exceeding 2016’s levels. The firm expects these losses to continue rising this year, with possible downgrades to the subprime segment.

Considering that Carvana is in an agreement with Ally to finance up to $4 billion in auto loans until January 2025, the current weakness in auto loans’ performance could result in Ally buying higher quality loans from Carvana while keeping its distance from subprime loans. As a result, Carvana may report losses on its subprime loans which will negatively impact its gross profit per unit (GPU).

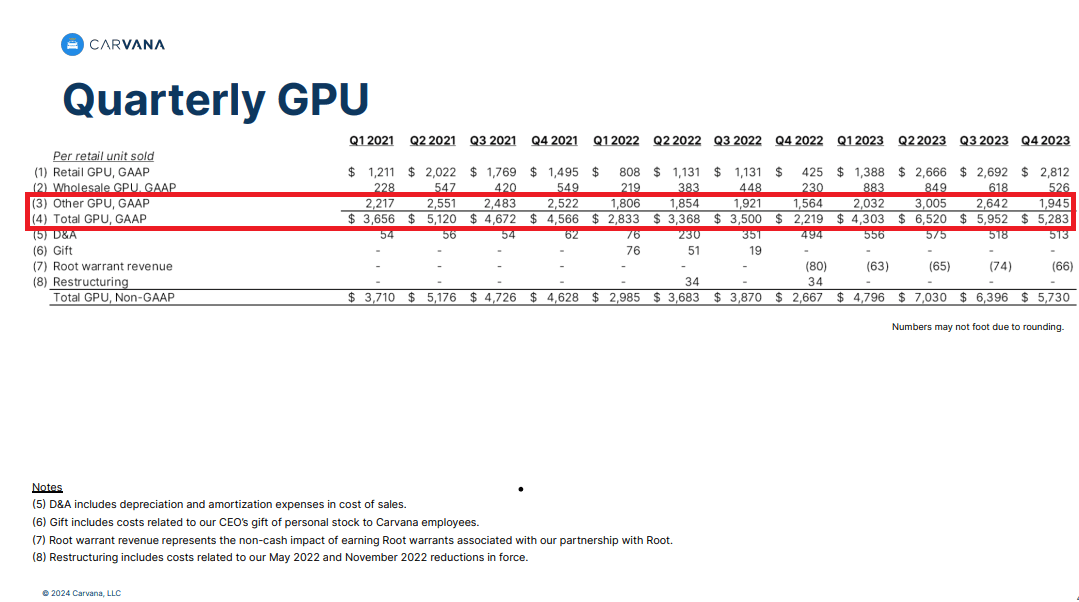

GPU is Carvana’s preferred earnings measure since it determines how much money it makes from each car it sells. In Q4, 37% of Carvana’s GPU came from the sale of auto loans. This is less than in previous quarters as auto loan sales represented 47%, 46%, and 44% of total GPU in Q1, Q2, and Q3 2023, respectively. This could be a sign that there is low demand for Carvana’s auto loans.

Carvana's Q4 2023 Presentation

Knowing the current weakness in the auto loan market, Carvana’s weak performance in 2023 adds to my bearish sentiment on the stock. In 2023, Carvana reported net income of $150 million, $803 million in operating cash flow, and $716 million in free cash flow. Given Carvana’s past performance, these figures should signal that the company is moving in the right direction. However, these results are simply unsustainable in my opinion as they were impacted by a one-time event which is the $878 million gain on debt extinguishment, PIK interest payments, inventory drawdown, and selling more car loans than originated.

In terms of Carvana’s $150 million net income, it was only due to the $878 million gain on debt extinguishment recorded in Q3 2023 as without this one-time benefit, the company would have reported a loss of $728 million.

Revenue | $10,771,000,000 |

CoR | $9,047,000,000 |

Gross Profit | $1,724,000,000 |

SG&A | $1,796,000,000 |

Interest Expense | $632,000,000 |

Other Income | -$1,000,000 |

EBIT | -$703,000,000 |

Income Tax | $25,000,000 |

Net Loss | -$728,000,000 |

In fact, Carvana’s Q4 performance shows that it’s still way off from reaching profitability as it reported a net loss of $200 million during the quarter. This raises serious doubt over the company’s future prospects since it still can’t be profitable even after cutting ad spend by 30% as mentioned in the Q4 2023 earnings call and reducing headcount by more than 4,000 employees.

Moving on to cash flow generation, Carvana reported free cash flow of $716 million in 2023. I don't expect the company to replicate this in the coming quarters as the generated free cash flow was only possible due to inventory drawdown. As is, Carvana’s inventory declined 38% YoY from $1.8 billion to $1.1 billion in 2023. This means that the company sold inventory without replacing them which is why the inventory reduction of $726 million was mainly responsible for the reported $716 million free cash flow figure.

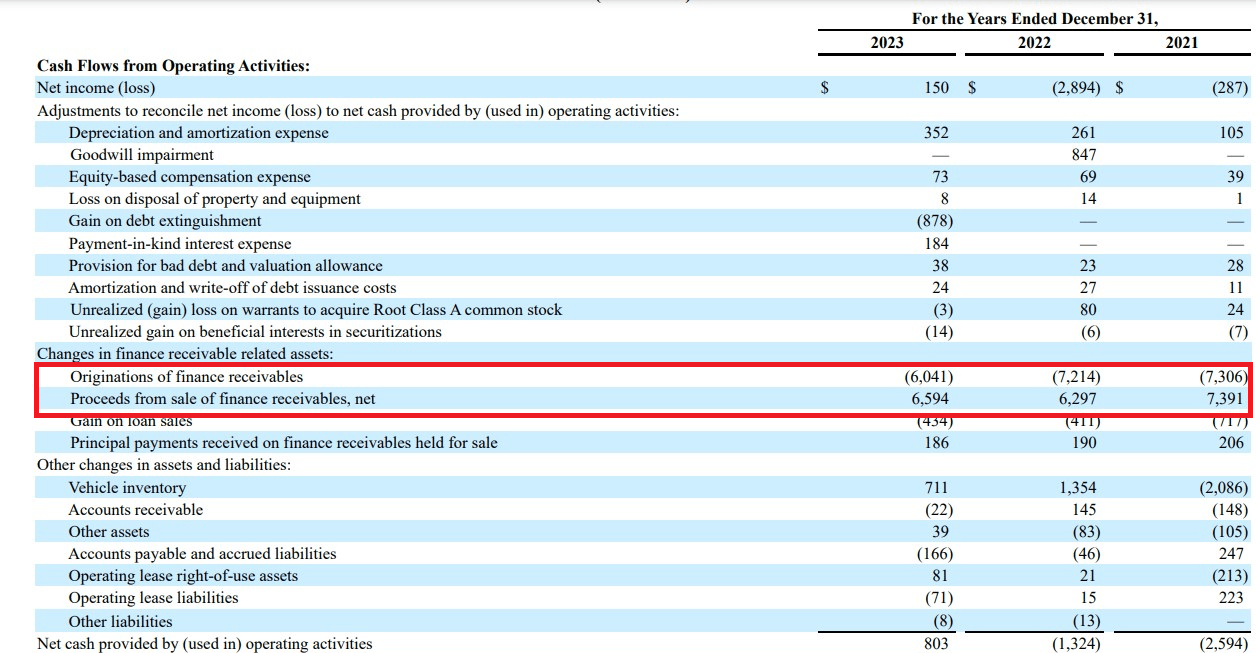

Carvana also reported $803 million in operating cash flow, which I also believe to be unsustainable. As mentioned earlier, Carvana mainly sold existing inventory in 2023 without replacing them. In addition, the company sold more loans than it originated in 2023 which is the opposite of previous years when the company sold loans equivalent or less than it originated. This caused Carvana’s receivables held for sale to decline YoY from $1.3 billion to $807 million.

10-K Filing

The inventory reduction and selling loans more than originated represented a $1.2 billion tailwind to operating cash flow in 2023 and excluding both changes, Carvana’s operating cash flow would have been -$435 million.

Having said that, Carvana’s performance in Q4 provides a snapshot into what to expect it to deliver in the coming quarters. In Q4 2023, Carvana’s inventory increased by $66 million. At the same time, the company originated $1.5 billion in loans and sold $1.3 billion of loans, in line with historical levels. As a result, the company’s operating cash flow in Q4 2023 was -$239 million.

In light of the Q4 results, I don’t expect Carvana to replicate its financial performance in 2024 as it will have to replace its inventory eventually in order for buyers to find the vehicles they want, or else, it risks losing market share to other used car retailers or local dealers. When that happens, Carvana will have to burn cash at a high rate, in my opinion, as shown in its Q4 performance which could force it to raise capital either through dilution or adding more debt to its balance sheet to fund its operations, without taking into consideration the interest payments on its existing debt.

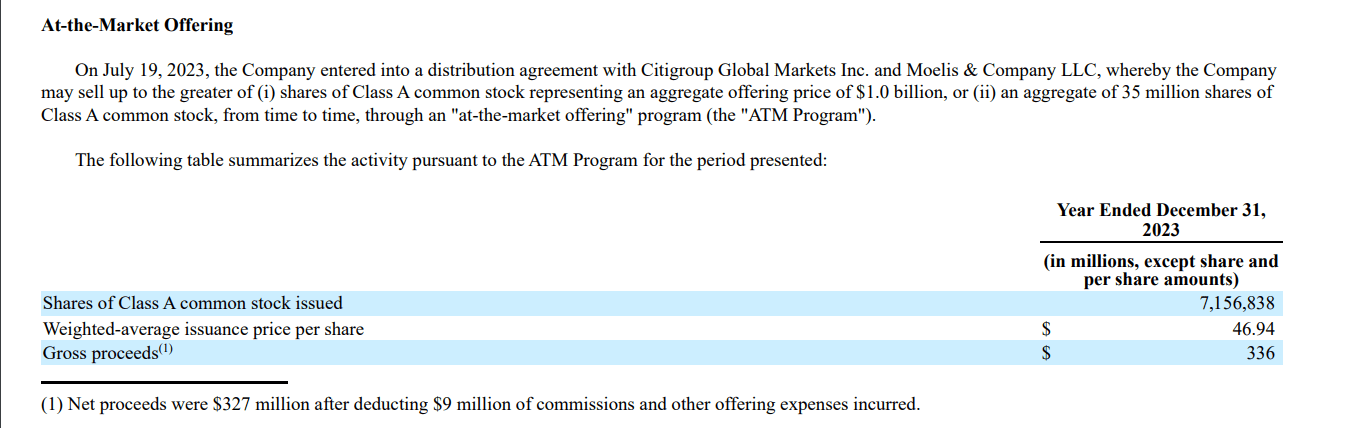

As is, the company is already authorized to issue 27.8 million shares under its ATM program required under its debt exchange transaction since it issued 7.1 million shares under the program per the 10-K filing.

10-K Filing

From a valuation standpoint, Carvana is extremely overvalued in my opinion at its current market cap of $15.9 billion. Currently, Carvana is trading at a 50.69 EV/EBITDA ratio, while CarMax (KMX) and Copart (CPRT) are trading at multiples of 31.48 and 29.41, respectively. While the average ratio of both CarMax and Copart is 30.45, Carvana should trade near the industry average of 10.96, in my opinion, due to its shrinking revenues and its future need to replace inventory which will impact its cash flow generation. As such, my price target for Carvana is $17.06 per share, implying 78% downside from current levels.

The main risk to my bearish thesis on Carvana is the stock reputation as a popular meme stock which makes it prone to short squeezes. According to Fintel data, Carvana’s short interest is 38.56%. Therefore, the stock could go on strong runs on any positive news shared by the company, especially in its upcoming Q1 2024 earnings call.

With auto loan delinquencies at their highest level since 2010, I’m bearish on Carvana due to its dependency on auto loan sales, which represent a significant portion of its GPU. Moreover, Carvana’s performance in 2023 is unsustainable, in my opinion, as its generated free cash flow was only due to selling inventory without replacing them and selling more loans than originated. As such, I expect Carvana’s free cash flow to turn negative soon as it replaces its inventory to maintain its market share in the used car market.

Given that the company isn’t anticipating any one-time benefits similar to 2023’s gain on debt extinguishment, I find it hard for Carvana to replicate its 2023 performance in the foreseeable future. Therefore, I’m rating Carvana as a strong sell with a price target of $17.06 per share, representing 78% downside from its current valuation.