PM Images

PM Images

It's interesting how the landscape around oil and gas has changed. Several years ago, the discussion regarding renewable energy controlled the narrative, but today, fossil fuels seem less demonized. I am pro-renewables as I believe we will need to generate more energy across the board to meet the future global demand, but I am still focusing on investing in traditional oil and gas companies. As an income investor, I love the large yields energy companies deliver, and the midstream space, due to its tax structure, throws off some of the largest yields an investor can find. Enterprise Products Partners (NYSE:EPD) is often referred to as the gold standard, as its operational track record speaks for itself. Since I started writing articles on Seeking Alpha, I have been bullish on EPD, and if you look at my track record, I didn't flip-flop when the oil and gas industry was decimated during the pandemic. EPD has continued to climb back to its pre-pandemic levels, and I believe it's going higher. All the data I look at indicates that we will need more energy in the future, and traditional sources of energy aren't going to disappear over the next several decades. EPD has established a 25-year track record of delivering distribution increases to its unit holders, and I think EPD will become even more popular as the Fed gets closer to a rate-cutting cycle. I am still long EPD and feel it can generate ongoing reliable income in addition to capital appreciation for investors in the future.

Seeking Alpha

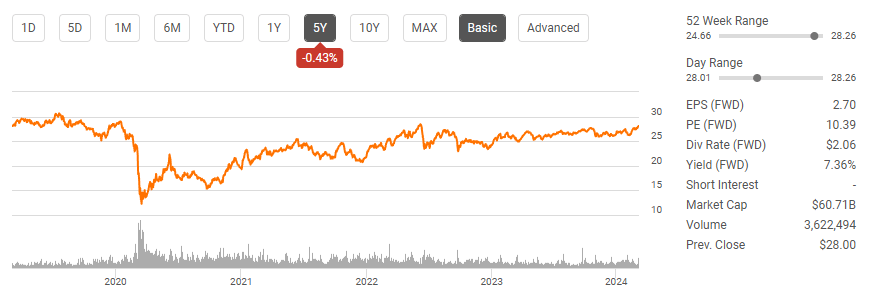

I wrote my last article on November 1st, 2023, on EPD (can be read here). Since then, units of EPD have appreciated by 8.2%, which has trailed the S&P 500's appreciation by 21.7%. When EPD's distribution is taken into account, its total return is 10.27%. In my last article, I discussed the energy landscape and why the acquisition of Pioneer Natural Resources (PXD) by Exxon Mobil (XOM) was bullish for EPD. Now that EPD has reported its 2023 fiscal year results, I wanted to follow up with a new article to discuss why I am excited for EPD in 2024 and how the new information regarding OPEC+ could be bullish for EPD. I am still long EPD and feel it could continue back into the $30s throughout 2024.

Seeking Alpha

EPD is a publicly traded partnership that is taxed as a partnership for U.S. tax purposes under the Internal Revenue Code Section 7704(b). For EPD's K-1 tax package, click here, and to read more about the K-1 tax package, please click here. Before investing in EPD or any other partnership that issues a K-1 tax package, I would recommend reading about how it could impact your taxes and discussing the implications with your tax professional.

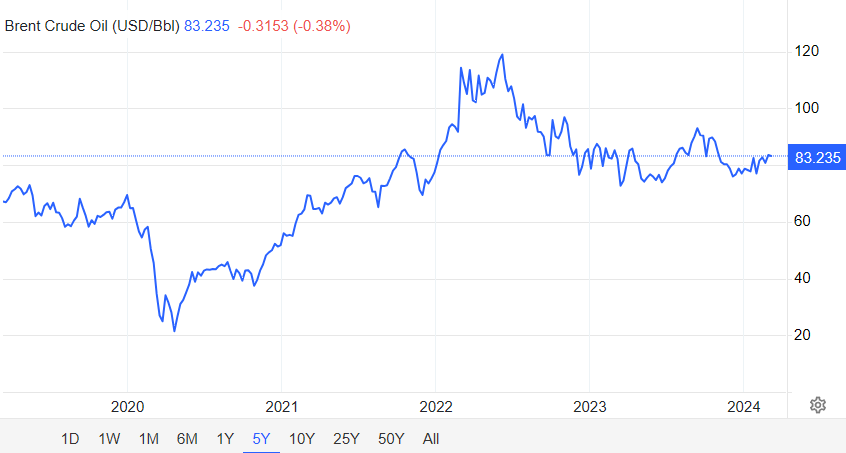

The Organization of the Petroleum Exporting Countries (OPEC) announced on 3/4/24 that several countries in the OPEX+ group would be extending additional voluntary cuts of 2.2 million bpd in Q2 2024. The decision was made to support the stability and balance of the oil markets. Saudi Arabia is leading the charge with an additional 1 million BPD of cuts, while the Russian Federation will reach 471,000 bpd of cuts during Q2. It certainly looks as if OPEC+ is trying to keep the price of Brent above $80 per barrel.

Trading Economics

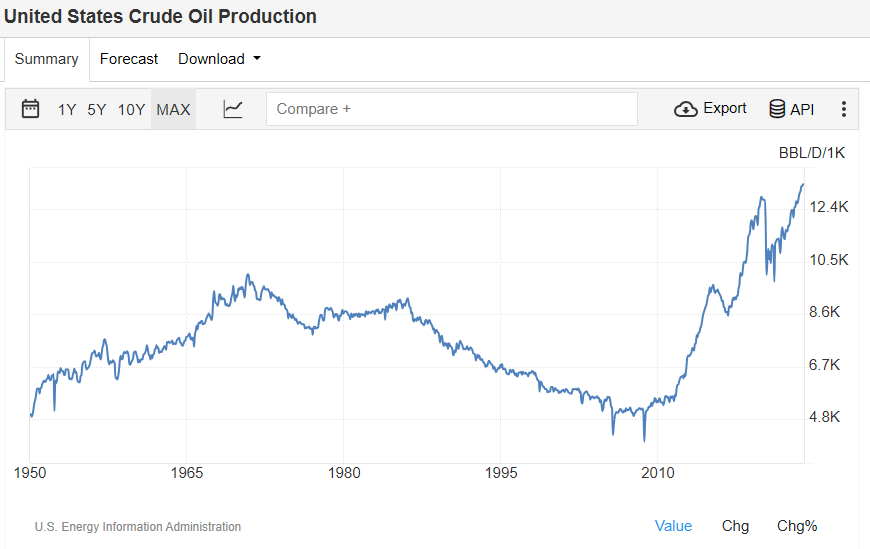

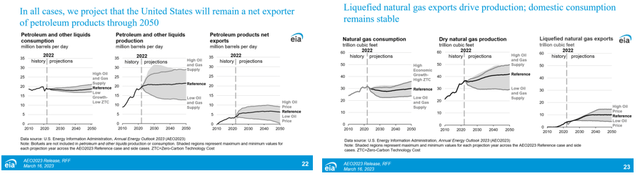

Despite how some may feel about the fossil fuel industry, production is soaring in the U.S. Domestic oil production is at all-time highs, and roughly 400,000 additional bpd are being produced from the 2019 peaks. The most recent data indicates that from July through December, the U.S. exceeded 13 million bpd of oil production, while the amount of money generated from oil exports reached an all-time high in 2023. The projections from the Energy Information Agency's (EIA) Annual Energy Outlook look more realistic these days, considering where U.S. production is. The EIA continues to project that petroleum and other liquid production will slightly increase from now through 2050, and dry natural gas production will increase by roughly 20% through 2050. As OPEC+ tightens the spicket, I believe domestic upstream production companies will be incentivized to produce more as higher prices are likely to stay here for longer.

Trading Economics EIA

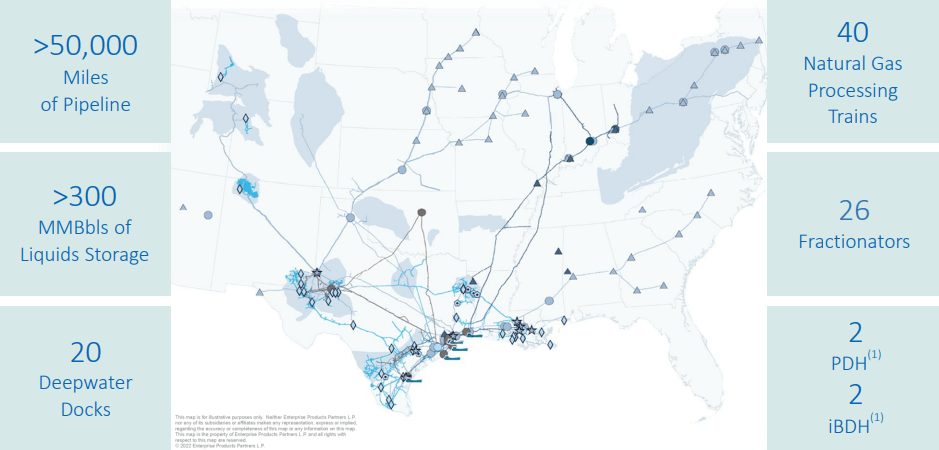

I believe the current energy landscape is beneficial for midstream operators, especially EPD. During Q4, EPD transported 12.7 million bpd, which was an increase of 1.2 million bpd YoY, while exporting 2.3 million bpd of liquid hydrocarbons. In 2023, EPD increased the amount of NGL, crude, refined products, and petrochemical pipeline volume by 8.22% YoY (600,000 bpd). The amount of natural gas pipeline volume that ran through EPD's system increased by 7.07% (1.3 million bpd), and their marine terminal volumes increased by 19.05% (400,000 bpd). To support the growing demand for transportation, EPD completed $3.5 billion of construction projects and placed 2 natural gas processing plants in the Permian into service in addition to their 12th Natural Gas Liquids (NGL) fractionator. EPD is starting 2024 off with $6.8 billion of organic growth projects underway and will look to bring their Texas Western Products pipeline system and 2 additional processing plants in the Permian online. EPD continues to fuel its growth organically and is expected to spend $3.75 billion in 2024 and $3 billion in 2025 to bring 11 projects online to strengthen its NGL, petrochemical, natural gas, and refined product segments.

Enterprise Products Partners

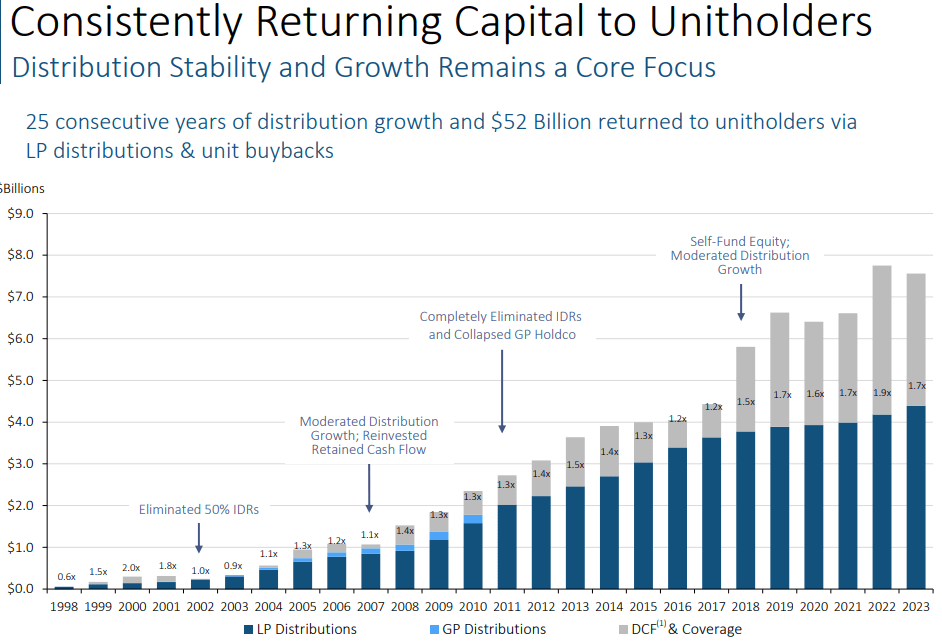

It doesn't matter if a financial crisis occurred if the price of oil collapsed, or if a pandemic wreaked havoc on the global economy, EPD has grown its distribution annually for the past 25 years. Going back to 1998, EPD has established an ongoing track record of growing its operational distributable cash flow, and adjusted cash flow from operations. In 2023, each unit of EPD generated $3.70 in Adjusted CFFO and 3.44 in operational DCF. Since 2013, EPD has increased the amount of operational DCF each unit produced by 74.62% ($1.47), and its Adjusted CFFO by 74.52% ($1.58). This has allowed EPD to maintain a distribution coverage ratio that exceeds 1.5x for the past 5 years. Today, EPD is trading at 8.17 times its operational distributed cash flow, which looks like a bargain. As production continues to increase and the global economy needs more energy, EPD should benefit from an endless stream of fossil fuels running through its system. EPD collects fees for delivering the raw materials that the economy runs on, and the combination of increased volume and fee increases should lead to larger cash flows generated by EPD's infrastructure.

Enterprise Products Partners

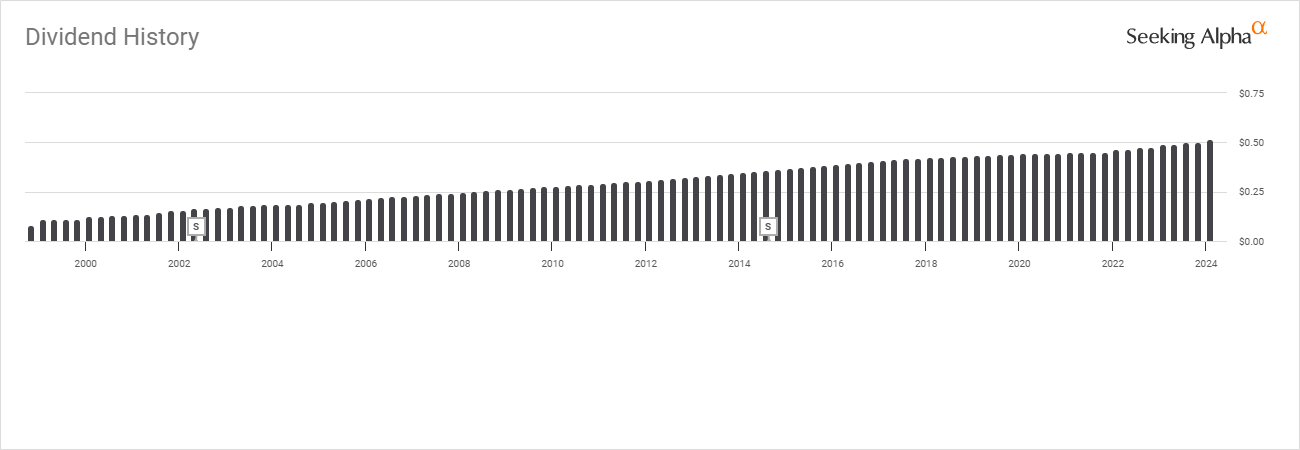

From an income generation perspective, EPD has established a strong track record and produces quarterly distributions that investors can rely on. Today, units of EPD pay a distribution of $2.06, which is a 7.36% yield. Over the past 5-years, the distribution has had a 3.05% growth rate, and the distribution has increased on an annual basis for 25 consecutive years. Since EPD's inception, the split-adjusted amount of income its distributions have produced is $31.14, as the quarterly distribution has grown by 544% from $0.08 to $0.52. Looking at a more recent snapshot, units of EPD have been relatively flat over the past 5-years, having declined by -0.43%. Units were $28.22, and for every unit purchased 5 years ago, they generated $9.28 of income, which is a 32.87% yield on cost. This also doesn't include the impacts of reinvesting the quarterly distributions. EPD is in a position to continue generating reliable income while providing investors with ongoing increases on an annual basis. Its operational efficiency has allowed it to remain a favorite in the midstream sector, and this is a major reason why over 139,000 investors follow EPD on Seeking Alpha.

Seeking Alpha

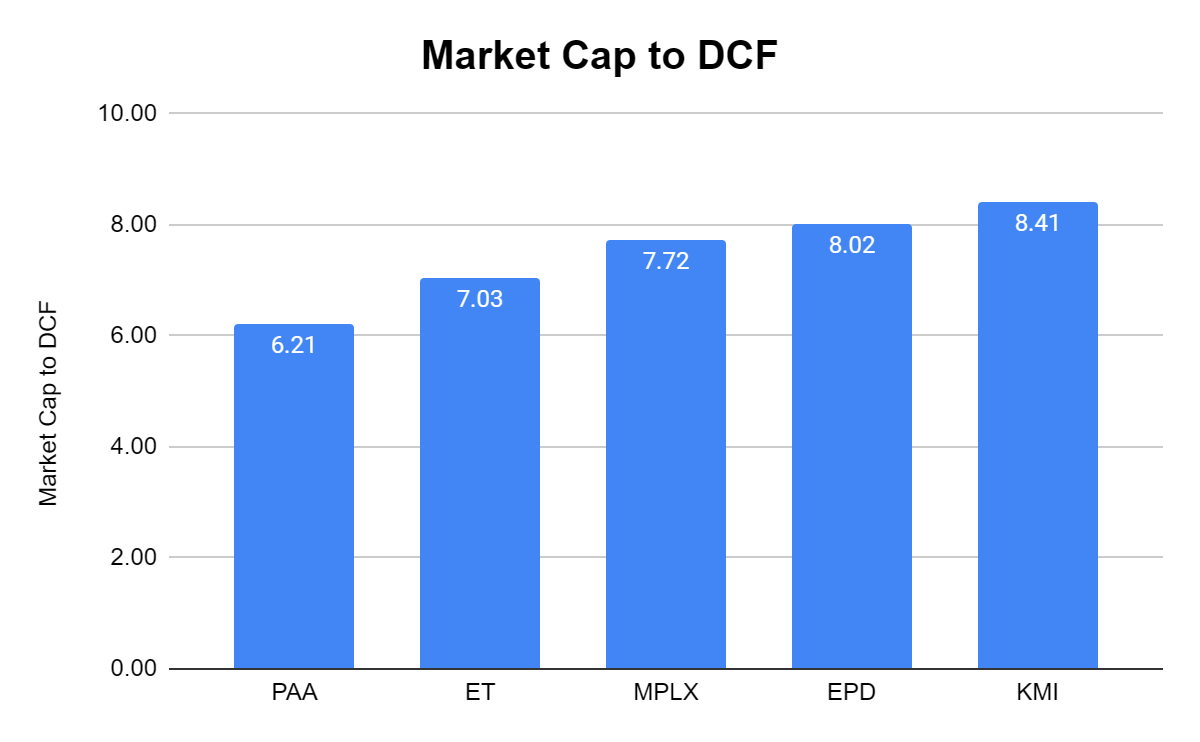

I compared EPD to Plains All American (PAA), Kinder Morgan (KMI), MPLX LP (MPLX), and Energy Transfer (ET). I put KMI in here because it's one of the largest pipeline companies in the U.S. even though it doesn't have an MLP corporate structure. Sometimes, it's not just about paying a rock bottom valuation for a company but getting a great company for a good valuation. EPD may not be the cheapest valued energy infrastructure company, but its units are enticing.

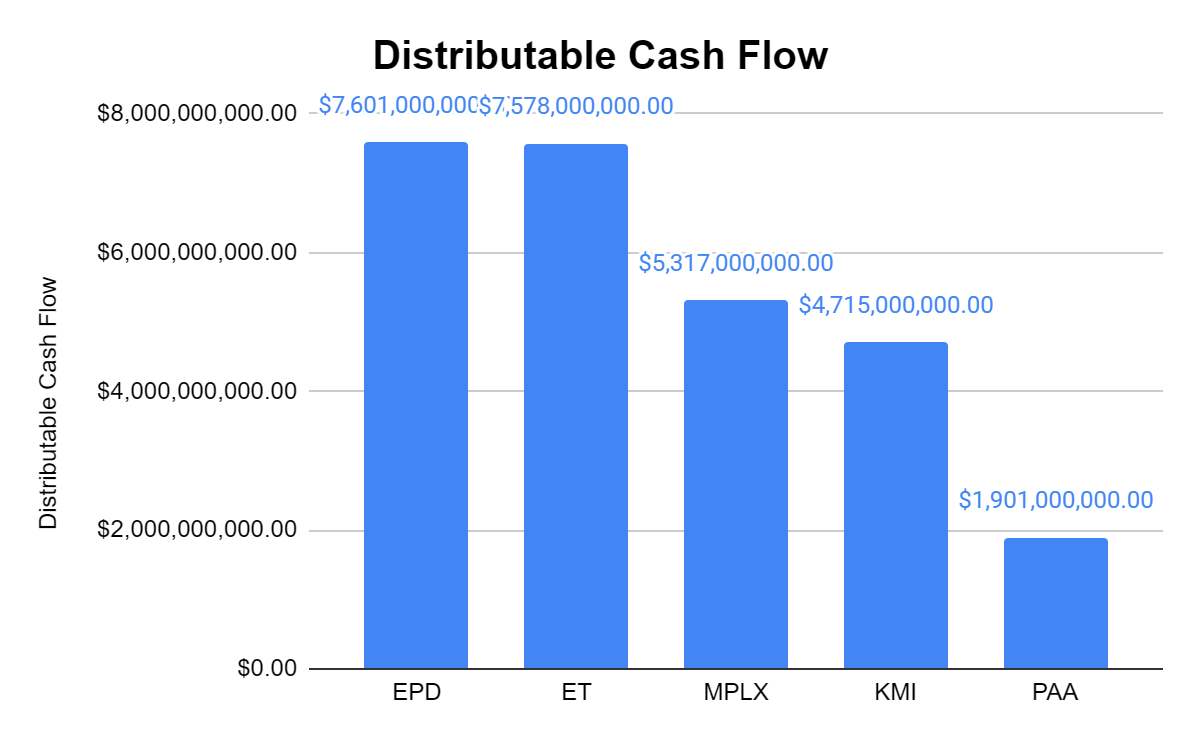

I was very surprised when I noticed that EPD passed ET in the amount of distributable cash flow (DCF) generated throughout 2023. EPD and ET generate significantly more DCF than their peers, and this is what I buy when I invest in energy infrastructure companies. The peer group trades at a 7.48x market cap to DCF average, and EPD trades at 8.02 times its DCF. I am willing to pay a premium for EPD, and trading slightly above the peer group average is fair to me.

Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha

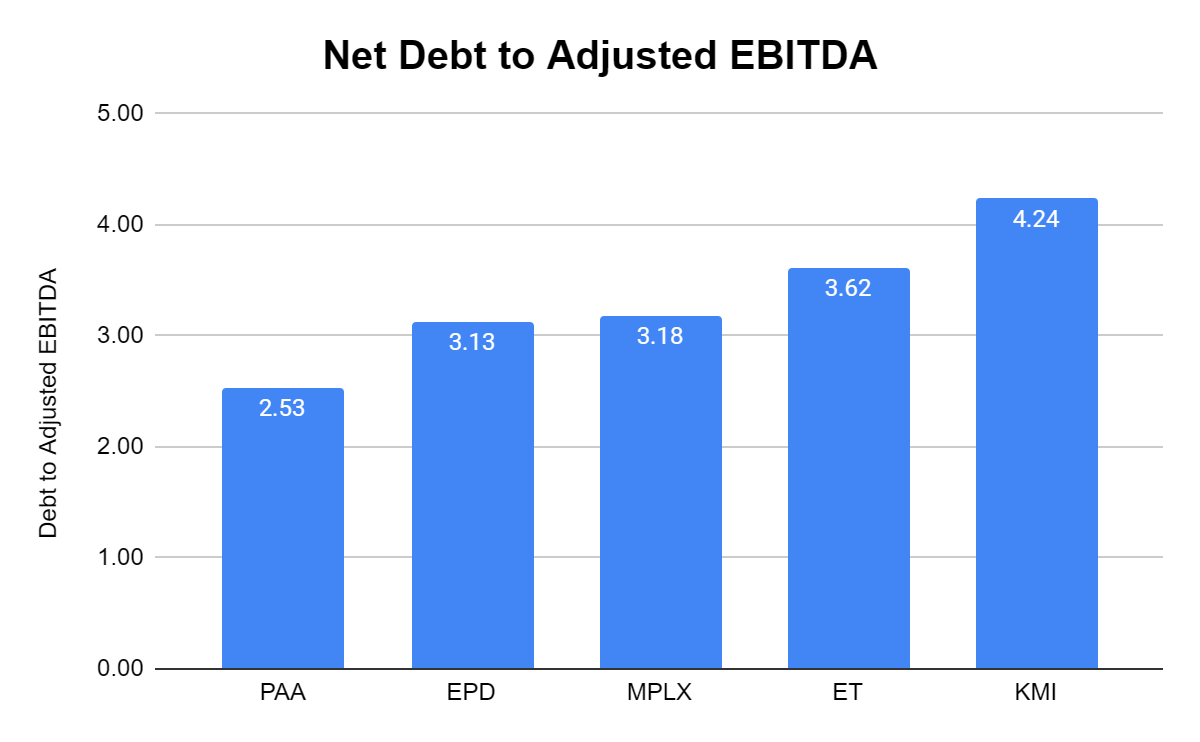

EPD has the 2nd lowest net debt to Adjusted EBITDA ratio at 3.13x, which is important to me because it validates EPD's organic growth. EPD has a slightly lower net debt to Adjusted EBITDA ratio than the peer group average of 3.34x, and the current ratio is well under what I would consider excessive or high.

Steven Fiorillo, Seeking Alpha

The recent cuts disclosed by OPEC+ could be bullish for EPD, as American producers will likely increase production to capitalize on higher oil prices and meet the demand for American energy. The U.S. continues to increase its oil production as a whole, and by the end of 2023, the number of barrels produced domestically was at an all-time high. I am bullish on midstream operators in general but feel that EPD will continue to climb higher while increasing its distribution. EPD has many capital growth projects coming online over the next 2 years, increasing its capacity and allowing more producers to increase their contracted volumes through EPD's infrastructure. As a fee-based business, the current setup looks strong for EPD, and I wouldn't be surprised if units exceed and stay above $30 in 2024.