kentoh/iStock via Getty Images

kentoh/iStock via Getty Images

By Catherine Wood

Last year began the journey back from what we believe will be deemed one of the biggest mistakes in monetary policy history, a journey that should continue to favor growth stocks generally and disruptive innovation specifically. While the rally in the US equity market during the last year rewarded a narrow subset of stocks, we believe it will broaden out during the next year as inflation and interest rates surprise on the low side of expectations.

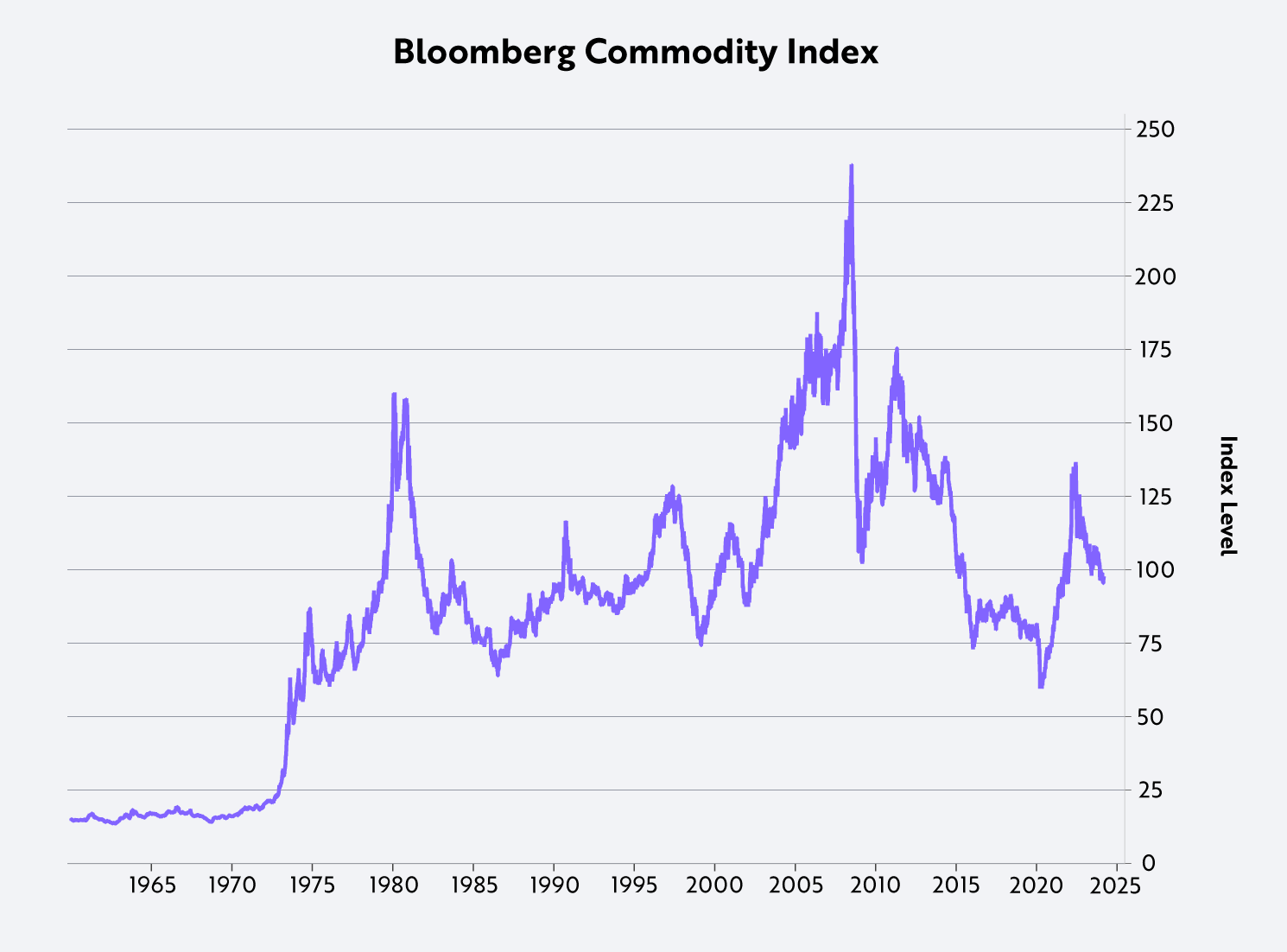

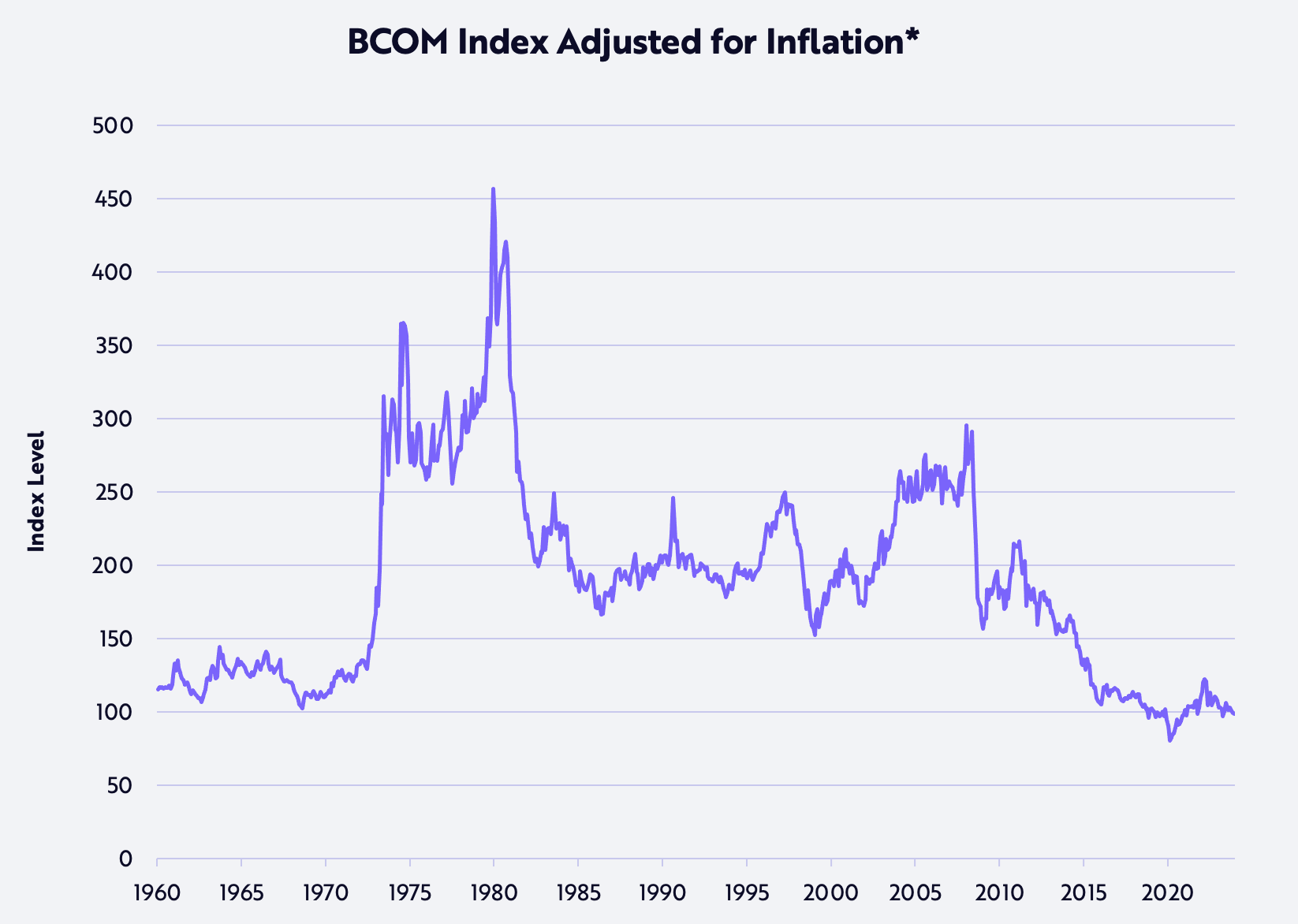

In little more than a year through July 2023, the U.S. Federal Reserve (the “Fed”) shocked the financial system with an unprecedented, and unexpected, 24-fold surge in the Fed funds rate[1] from 0.25% to 5.5%. Fed’s moves did arrest the price shock caused by COVID-related supply chain bottlenecks and pushed commodity prices, as measured by the Bloomberg Commodity Index (BCOM), back into the deflationary trend that has been in place since the Great Financial Crisis (GFC) in July 2008, as shown in the first chart below. Today, BCOM is trading at the same level as it was more than 40 years ago in the early eighties, suggesting that the Fed’s fears about inflation are misplaced. In our view, deflation should be the concern. Indeed, adjusted for inflation as measured by the Producer Price Index (PPI), BCOM is lower than its level when the US abandoned the gold-exchange standard in 1971, as shown in the second chart below.

| *Inflation = adjusted by the Producer Price All Commodities Index. Source: Bloomberg, data as of Feb 2024. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results. |

As it observed the deflationary strains on housing, autos, commercial real estate, and capital spending, the Fed paused its tightening moves last summer. At the same time, in the technology realm, ChatGPT began to dramatize the seemingly miraculous breakthroughs that are likely to tip the scales even further toward broad-based deflation. Although creative destruction—the transition from gas-powered vehicles to electric vehicles, for example—could obfuscate the boom associated with AI and other disruptive technologies evolving today, the waves of growth associated with the convergence among the 14 technologies involved in our five major platforms—robotics, energy storage, AI, blockchain technology, and multiomics sequencing—should start moving the needle on macro metrics increasingly and significantly during the next five to ten years.

Because the Fed still seems to be fighting the inflation war that we believe ended in 2008,[2] the equity market has been somewhat unsettled this year. Deflation would punish companies with leverage, and reward those with cash piles. In our view, the deflationary ramifications of current Fed policy already are surfacing through bankruptcies in commercial real estate, both office and multi-family, and could culminate in another round of regional bank failures. If the Fed were to lower interest rates in response, companies sacrificing short-term profitability to invest and potentially capitalize on technologically enabled super exponential growth opportunities should be prime beneficiaries.

After boosting profitability with higher prices during the supply-chain-related bottlenecks in 2021-22, and again as unit growth disappointed in 2023, corporations now seem to be losing pricing power, to the detriment of profit margins. As measured by Bloomberg, the S&P 500's (SP500, SPX) gross profit margin dropped from 34.8% on average during the past five years and 34.6% during the fourth quarter of 2022 to 33.5% during the fourth quarter of 2023. In our view, this setback will intensify until the Fed cuts interest rates significantly and unless companies harness innovation like artificial intelligence aggressively, not only to drive productivity growth but also to create new products and services that replace legacy solutions.

To limit the damage to margins in the interim, after hoarding employees in the aftermath of the severe labor shortages caused by COVID, companies are likely to lay them off during the next year and to lower the rate of wage gains, further allaying the Fed’s concern about underlying inflation. As a result, nominal consumption could weaken beyond the recent soft spots associated with housing, autos, and other big-ticket purchases, forcing more price cuts and margin compression.

Seemingly expecting continued pricing power, companies never disgorged inventories after purchasing managers double- and triple-ordered goods in response to shortages during 2021-22. In real terms, nonfarm inventory[3] accumulation swung ~$345 billion, from -$138 billion in the second quarter of 2021 to +$207 billion in the fourth quarter of 2021, and has yet to drop back into negative territory. Since then, the accumulation has continued apace, totaling another $913 billion. As a result, total inventory accumulation has hit 4% of real Gross Domestic Product (GDP) over the past two and a half years, a rate which typically has not declined until the onset of a recession.[4] If prices do fall and inventory losses mount, corporate gross margins will continue to suffer, potentially breaking down toward the 30.1% low hit in 2009.

After what we have characterized as a “rolling recession” in the last few years, the damage is not likely to cascade uncontrollably. Both in the US and the rest of the world, much of the damage has been done. Belying the “soft landing” thesis that dominated “Wall Street’s” narrative, the revenues of many global bellwethers actually dropped on a year-over-year basis during the fourth quarter: 3M (MMM, -1.8%), UPS (-7.8%), Kraft-Heinz (KHC, -7.1%), Exxon Mobil (XOM, -12.3%), Thermo Fisher (TMO, -4.9%), Home Depot (HD, -2.9%), Cisco (CSCO, -5.9%), Texas Instruments (TXN, -12.7%).[5] In other words, Europe, the UK, Japan, and China already are in or are bordering on recession. Meanwhile, the global weakness in commercial real estate is likely to hit several groups disproportionately: private equity, private credit, and other large investors who leveraged up while reaching for yield before and during COVID. Importantly, as prices and speculative excesses unwind, key decision makers at companies are likely to assess and reassess capital spending plans, including the boom in spending on artificial intelligence.

Roughly 30 years after America Online (AOL) first connected its proprietary email service to the internet in 1993, creating one of the most important "aha moments" in technology history, ChatGPT has captured the imagination of consumers, businesses, and the financial markets. Given lessons learned from internet history, the capital that has plowed into all-things-AI during the past year could get a reality check as companies become focused on the need to develop strategic plans for a breakthrough technology that is likely to separate winners from losers in the years ahead.

Based on ARK's analysis from both a business and investment point of view, management teams are facing a number of decision points: they will have to assess the competition among cloud providers and AI companies that the capital markets are funding, map workflows in extensive detail, and find/integrate data from far-flung divisions—all daunting and time-consuming tasks—before activating AI strategically and effectively. If the loss of pricing power does pressure corporate margins, as we anticipate, then management scrutiny will intensify, perhaps delaying the decision-making process, but also heightening the sense of strategic urgency.

Cisco Systems (CSCO) offers a good history lesson. I remember well the stock's behavior at a similar technology moment in time. In the three and a half years leading to March 9, 1994, CSCO soared ~31-fold from $0.07 to $2.24 split-adjusted, as its routers, switches, and other equipment dominated the buildout of the internet backbone globally. The capital markets began to fund competitors, even those with systems inferior to Cisco’s, which confused strategic planners in corporations and cast a short-term pall on spending. In the four months leading up to July 15, 1994, CSCO dropped 51% as companies—already worried about a potential recession—reassessed their spending commitments and deliberated. After the coast cleared, CSCO entered another ~73-fold run into the peak of the internet bubble during 2000.

Today, Nvidia (NVDA) is that company. Central to the AI age, NVDA has soared ~117-fold in the roughly nine years since February 8, 2015, when analysts were beginning to understand that breakthroughs in Deep Learning were accelerating the pace of AI change, to the benefit of GPUs (graphic processing units). NVDA also had appreciated 23-fold in the five years since its last inventory correction, one triggered by a crypto winter[6] that hit it in October 2018 and trounced the stock by 56% in three months.

The launch of ChatGPT in November of 2022 has fueled several quarters of unprecedented growth for Nvidia as cloud service providers, other consumer internet companies, and well-funded startups have scrambled—likely double- and triple-ordering GPUs in the process—to acquire Nvidia’s hardware and train AI models. Today, Nvidia is guiding expectations to a sequential deceleration in growth and, reportedly, the lead time for its GPUs has dropped from 8-11 months to 3-4 months, suggesting that supply is increasing relative to demand.[7] Without an explosion in software revenue to justify the overbuilding of GPU capacity,[8] we would not be surprised to see a pause in spending, compounding a correction in excess inventories, particularly among the cloud customers that account for more than half of Nvidia’s data center sales.[9] Longer term, unlike the history with Cisco, competition could intensify, not only because AMD is finding success but also because Nvidia’s customers—cloud service providers and companies like Tesla—are designing their own AI chips. That said, since 2019 futurists have collapsed the time to AGI[10] (Artificial General Intelligence) from 80 years to 8 years, so anything is possible!

Once the cyclical correction is complete, AI should continue to take off and catalyze other technologies—including robotics, energy storage, blockchains, and multiomics sequencing—creating convergences that we believe will lead not to exponential growth, but to super-exponential growth—already rapid growth rates that accelerate over time. In Big Ideas 2024, we have detailed the likely impact of these convergences on each of the technology platforms and on global economic growth between now and 2030. The upshot is that

real Gross Domestic Product (GDP) growth[11] is unlikely to decelerate from 3% on average during the past century to the consensus expectation of 2.6%, but instead should accelerate to 6-8%+ growth, an expectation we have found in no other economic forecast. Moreover, if the five innovation platforms—involving 14 different technologies—evolve as our research suggests during the next seven years, the equity market cap associated with them should scale ~40% at an annual rate, from $15-20 trillion today to ~$220 trillion in 2030.We are privileged to be researching disruptive innovation at the crossroads between the old world and the new world. Innovation solves problems, of which we have no shortage in 2024.

Cathie Wood,

ARK Invest CEO/CIO

FOOTNOTES

1“Fed funds rate" refers to the overnight lending rate among US banks as set by the Federal Open Market Committee.

2https://www.youtube.com/watch?v=hFg1TMACw4I ARK Investment Management. 2024. “In The Know With Cathie Wood: Big Ideas 2024—Episode 52,” see timestamp 50:12.

3“Nonfarm Inventory” refers to the change in real total private inventories that are taken into account within gross domestic product.

4Inventory data from Macrobond as of February 29, 2024.

5All revenue data from Bloomberg as of February 29, 2024.

6“Crypto Winter” refers to a bear market in which cryptocurrencies prices depreciated significantly. During the most recent crypto bear market, which occurred roughly between November 2021 and November 2022, bitcoin's price dropped ~ 77%.

7https://www.forbes.com/sites/petercohan/2024/02/21/nvidia-stock-soars-after-hours-on-265-revenue-growth/ Cohen, P. 2024. “Nvidia Stock Soars After-Hours On 265% Revenue Growth.” Forbes.

8https://www.sequoiacap.com/article/follow-the-gpus-perspective/ Cahn, D. 2023. “AI’s $200B Question.” Sequoia Capital.

9Specifically, Amazon Web Services (AWS), Microsoft Azure (Azure), and Google Cloud Platform (GCP).

10https://ark-invest.com/big-ideas-2024 ARK Investment Management. 2024. “Big Ideas 2024: Disrupting The Norm, Defining The Future,” slides 10-16. By General Artificial Intelligence, here we mean a unified system that can surpass a specific benchmark comprising (1) successfully passing an adversarial multi-modal two-hour Tuning test, (2) exceptional performance on knowledge and logic benchmarks at or exceeding human expert levels, and (3) the successful interpretation and execution of complex and intricate model car assembly instructions.

11https://ark-invest.com/newsletters/issue-404 Winton, B. 2024. “Technology Could Cause A Transformational Acceleration In Economic Growth.” ARK Disrupt Newsletter.

Important Information

Please note, companies that ARK believes are capitalizing on disruptive innovation and developing technologies to displace older technologies or create new markets may not in fact do so and/or may face political or legal attacks from competitors, industry groups, or local and national governments.

ARK aims to educate investors and to size the potential opportunity of Disruptive Innovation, noting that risks and uncertainties may impact our projections and research models. Investors should use the content presented for informational purposes only, and be aware of market risk, disruptive innovation risk, regulatory risk, and risks related to Deep Learning, Digital Wallets, Battery Technology, Autonomous Technologies, Drones, DNA Sequencing, CRISPR, Robotics, 3D Printing, Bitcoin, Blockchain Technology, etc.

The content of this material is for informational purposes only and is subject to change without notice. This material does not constitute, either explicitly or implicitly, any provision of services or products by ARK and investors are encouraged to consult counsel and/or other investment professionals as to whether a particular investment management service is suitable for their investment needs. All statements made regarding companies or securities are strictly beliefs and points of view held by ARK and are not endorsements by ARK of any company or security or recommendations by ARK to buy, sell or hold any security. Historical results are not indications of future results.

Certain of the statements contained in this material may be statements of future expectations and other forward-looking statements that are based on ARK's current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. The matters discussed in this material may also involve risks and uncertainties described from time to time in ARK's filings with the U.S. Securities and Exchange Commission. ARK assumes no obligation to update any forward-looking information contained in this material. Certain information was obtained from sources that ARK believes to be reliable; however, ARK does not guarantee the accuracy or completeness of any information obtained from any third party. ARK and its clients as well as its related persons may (but do not necessarily) have financial interests in securities or issuers that are discussed.

©2024, ARK Investment Management LLC. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK Investment Management LLC (“ARK”).

©2021-2026, ARK Investment Management LLC (“ARK” ® ”ARK Invest”). All content is original and has been researched and produced by ARK unless otherwise stated. No part of ARK’s original content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. The content is for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation in respect to any products or services for any persons who are prohibited from receiving such information under the laws applicable to their place of citizenship, domicile or residence.

Certain of the statements contained on this website may be statements of future expectations and other forward-looking statements that are based on ARK's current views and assumptions, and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. All content is subject to change without notice. All statements made regarding companies or securities or other financial information on this site or any sites relating to ARK are strictly beliefs and points of view held by ARK or the third party making such statement and are not endorsements by ARK of any company or security or recommendations by ARK to buy, sell or hold any security. The content presented does not constitute investment advice, should not be used as the basis for any investment decision, and does not purport to provide any legal, tax or accounting advice. Please remember that there are inherent risks involved with investing in the markets, and your investments may be worth more or less than your initial investment upon redemption. There is no guarantee that ARK's objectives will be achieved. Further, there is no assurance that any strategies, methods, sectors, or any investment programs herein were or will prove to be profitable, or that any investment recommendations or decisions we make in the future will be profitable for any investor or client. Professional money management is not suitable for all investors. For full disclosures, please go to our Terms & Conditions page.

The Adviser did not pay a fee to be considered for or granted the awards. The Adviser did not pay any fee to the grantor of the awards for the right to promote the Adviser's receipt of the awards nor was the Adviser required to be a member of an organization to be eligible for the awards. For full Award Disclosure please go to our Terms & Conditions page. Past performance is not indicative of future performance.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.