brightstars

brightstars

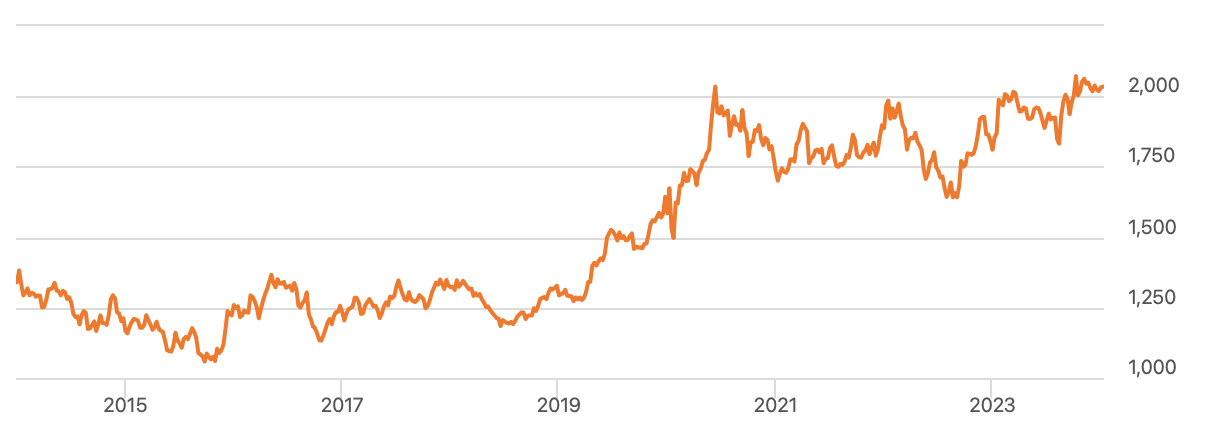

Gold has been one of the most detested assets over the last ten years. And why not? With tech stocks, cryptocurrencies, and other assets appreciating by hundreds or thousands of percent, gold's price has essentially gone nowhere over the last decade, appreciating by only around 50%.

Spot Gold Price: 10-Year Chart

Spot gold (seekingalpha.com )

However, there are specific reasons for gold's "recent" underperformance, and things will likely change. As the Fed transitions to a more accessible monetary stance, bond yields should decrease, improving sentiment and increasing demand for gold.

Also, the Fed could stop its QT program relatively soon. This dynamic should open the door for new rounds of QE in future years. Falling interest rates combined with the potential for future QE stimuli provide an ideal environment for gold, other precious metals, and many materials in general.

Additionally, gold's "depressed last decade" was due to a massive run-up in the early and mid-2000s. First, gold needed significant time to digest the gains. And second, there were expectations that the Fed would wind down its balance sheet. However, nothing could be further from the truth, as the Fed's balance sheet could continue to balloon perpetually, enabling higher inflation levels to become more permanent in future years.

Therefore, gold, silver, copper, lithium, and other essential compound prices could appreciate considerably in future years. Moreover, high-quality stocks could be the best way to play the upcoming bull market in gold and other commodities. My three favorite gold stocks are Barrick Gold (GOLD), Agnico Eagle Mines (AEM), and Kinross Gold (KGC).

I expect gold to break out to new ATHs in H2, and it could close the year in the $2,200-2,500 range, roughly 10-25% higher from here. Such a breakout in gold could enable top metal miners to appreciate rapidly, with a potential 25-50% or more upside in the next twelve months.

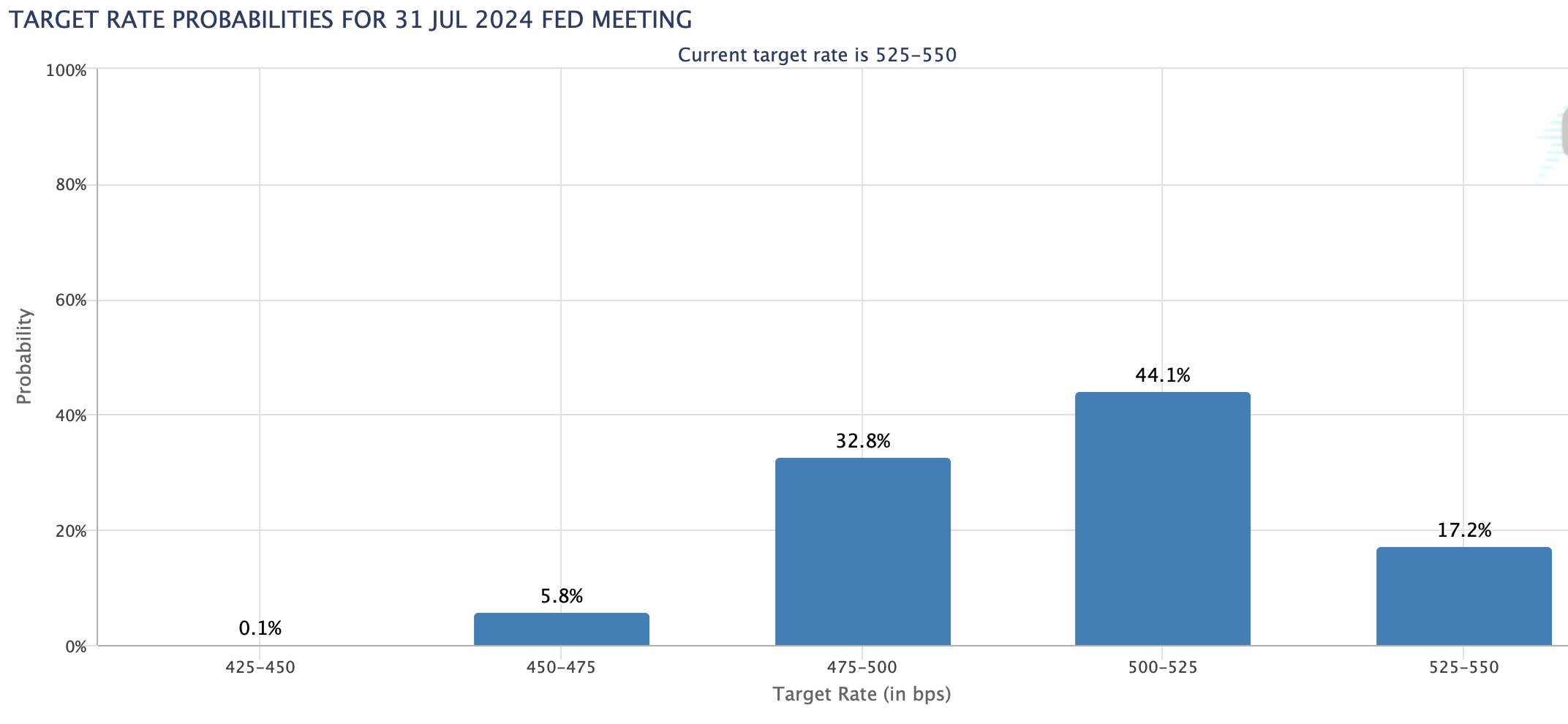

Rate probabilities (CMEGroup.com)

The probability of at least one rate cut by the July FOC meeting is around 83%. Also, the odds have tilted away from a rate cut sooner due to a potentially transitory uptick in some inflation readings. Therefore, the odds of a rate cut occurring sooner than the July meeting should increase if future inflation readings come in better than expected. However, unless we see significant signs of resurging inflation, I expect the first rate cut soon.

Also, once the easing cycle gets going, it can last years, and the destination could be a zero-rate policy. The servicing payments on government and other forms of debt are incredibly high now and likely unsustainable. Moreover, the economy could begin buckling under the pressure of high-interest rates. The path of least resistance is lower, and the Fed could tolerate higher inflation levels as the easing cycle advances.

The Fed's quantitative tightening "QT" program should end soon, likely later this year. This dynamic should lower treasury yields and other key bond rates, providing a favorable backdrop for gold. Additionally, the Fed can introduce future QE programs to backstop bad debt, purchase federal and municipal bonds, and essentially buy anything else it needs. At its core, the Fed is a "printing press" (monopoly on U.S. fiat money creation) that could perpetually balloon the money supply.

As the Fed eases monetary policy, treasury, bonds, and other major yields should decline. This dynamic is highly favorable for gold as it competes with bonds in the "safe haven" space. Therefore, lower yields, especially when inflation-adjusted, should push more investors to increase exposure to gold.

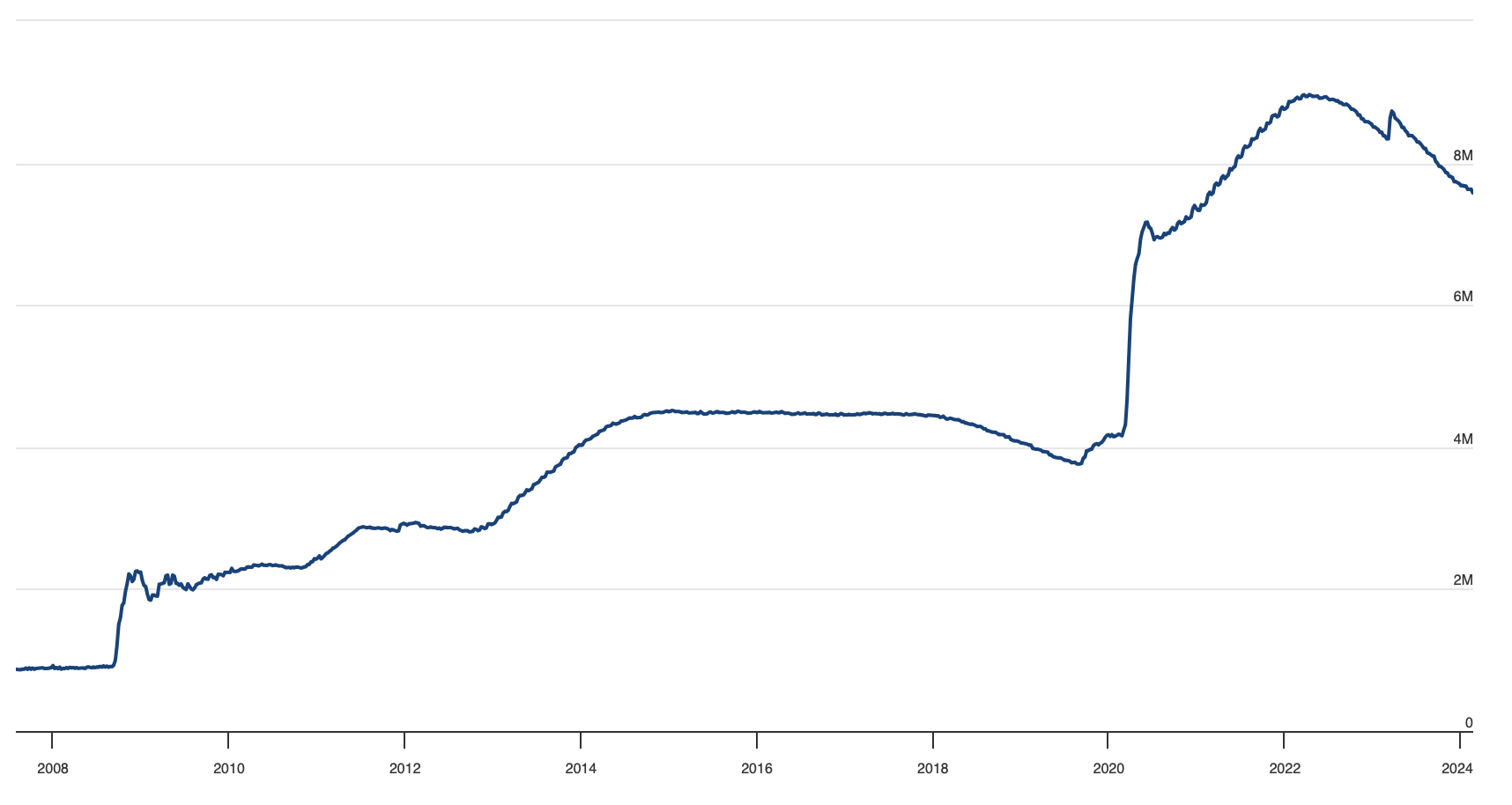

Fed's balance sheet (federalreserve.gov)

The Fed's balance sheet has skyrocketed from under $1T in the mid-2000s to around $7.6T. These extraordinary asset increases cannot be unwound "simply." The Fed can sometimes gradually decrease its balance sheet, but the trend is higher and higher. Therefore, we should return to monetary expansion after this transitory reduction phase.

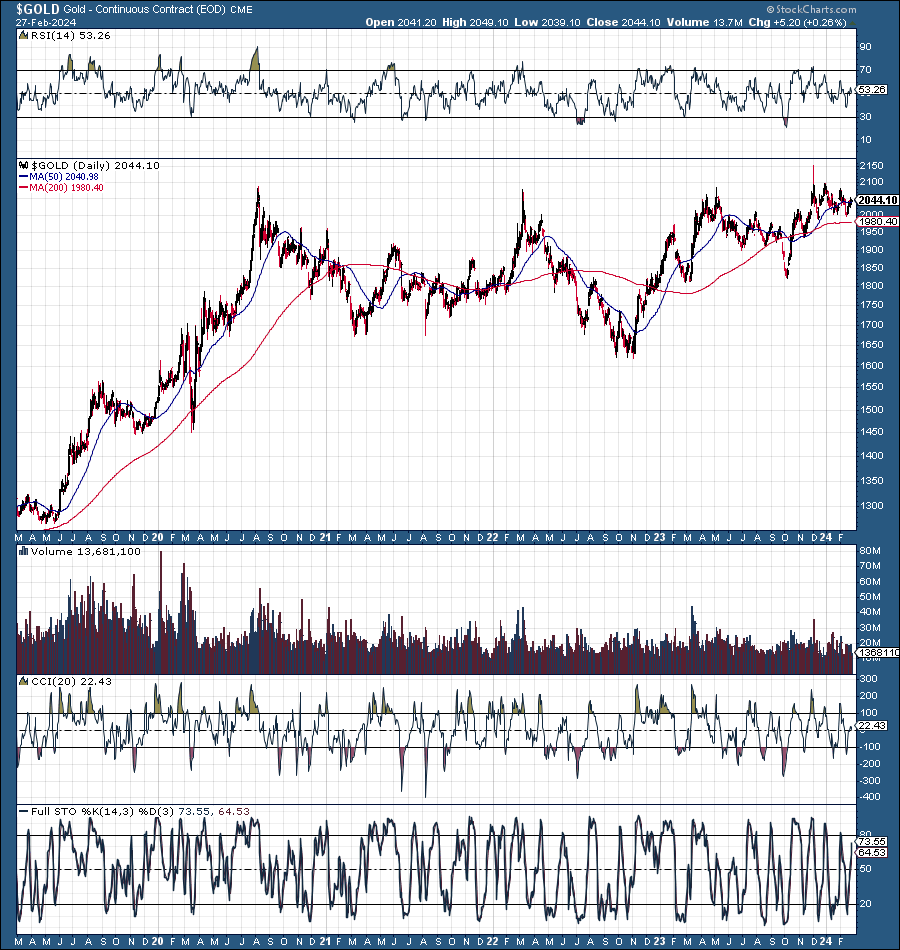

Gold (StockCharts.com )

Gold has consolidated for about four years and could break out to new ATHs soon. We have a very solid uptrend from the lows before 2020. We also see a highly bullish long-term inverse head and shoulders pattern with the neckline around $2,100 (roughly the ATH) about to get breached. Critical near-term support remains around the $2,000-1,980 level, with stopouts below, just in case (for day and swing traders). Despite the possibility of near-trade volatility, gold should go much higher in the intermediate and long term.

Many high-quality gold stocks have gotten battered lately and are oversold, undervalued, and underappreciated. As Benjamin Graham continuously teaches us, the market is a weighing machine, not a voting machine, in the long run. Therefore, the top gold mining companies should get revalued much higher as gold continues moving higher in future years.

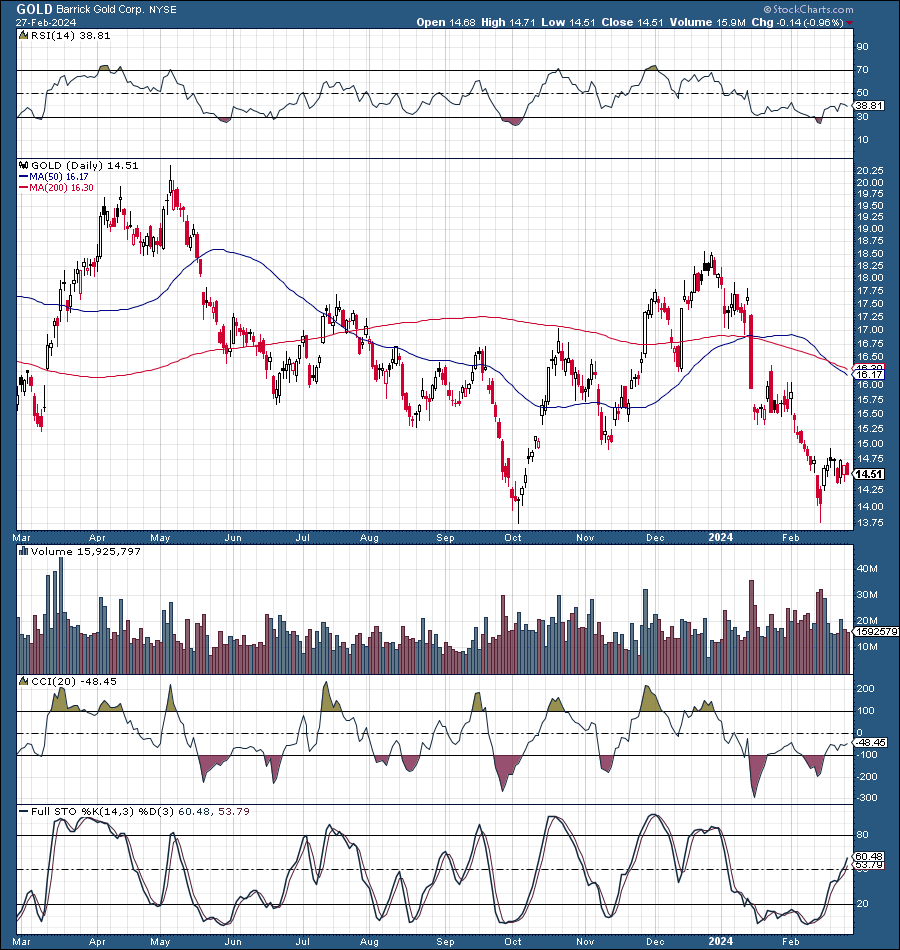

GOLD (StockCharts.com )

Barrick's stock price has crumbled, declining by 33% from its 52-week high (peak to trough). We also see a possible double bottom around critical support at $14, and the downside risk is probably minimal from here. We see technical indicators improving, and the stock could move much higher in future months and years.

Fundamentally - Barrick looks excellent, as it is positioned exceptionally well as one of the most significant gold producers globally.

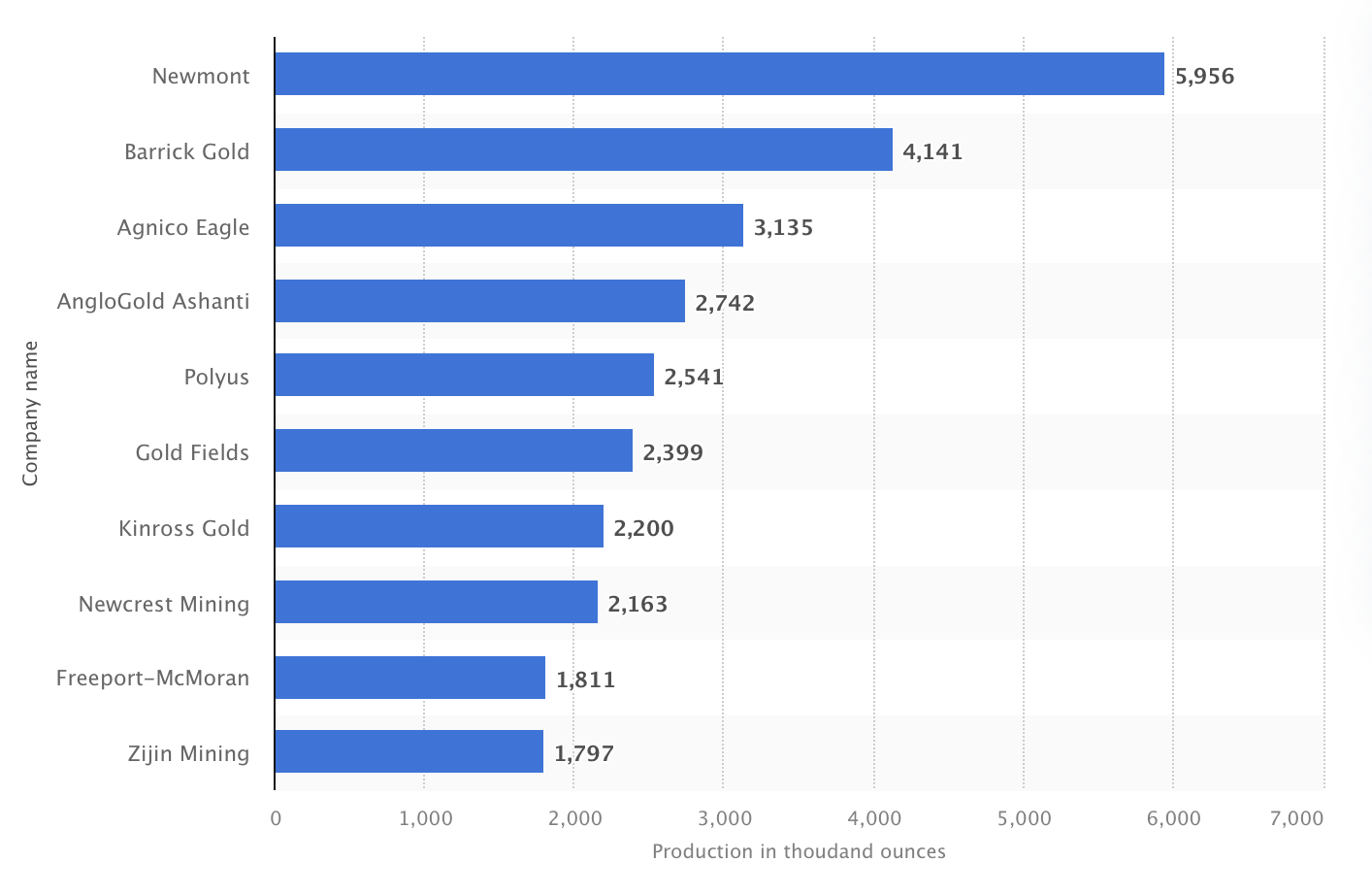

Gold production (Statista.com)

Production-wise, Barrick was second only to Newmont (NEM) in 2022. Barrick has made significant acquisitions in recent years and should capitalize as we move forward. Barrick also pays a 2.8% dividend, trading at only 13 times next year's consensus EPS estimates.

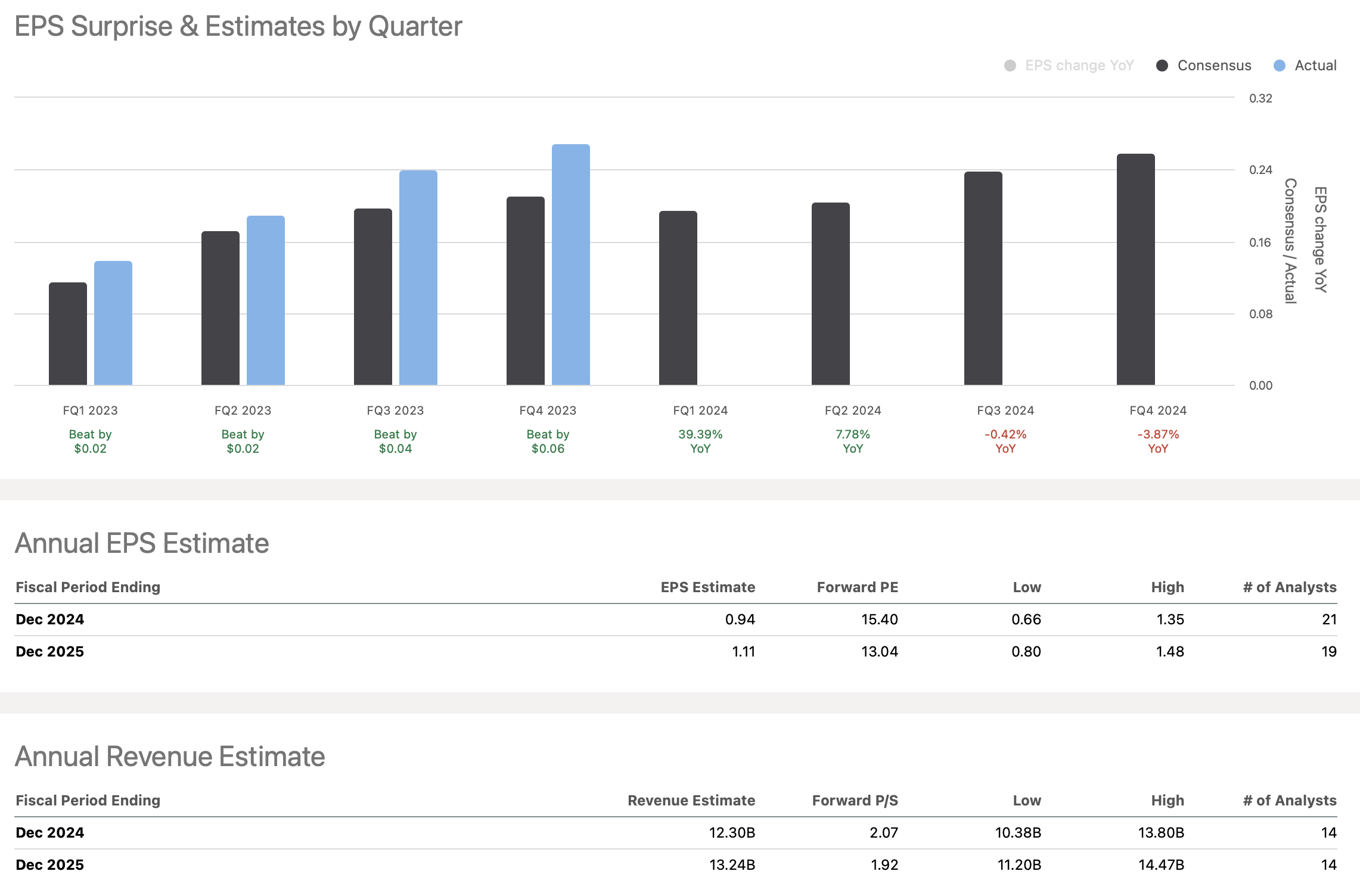

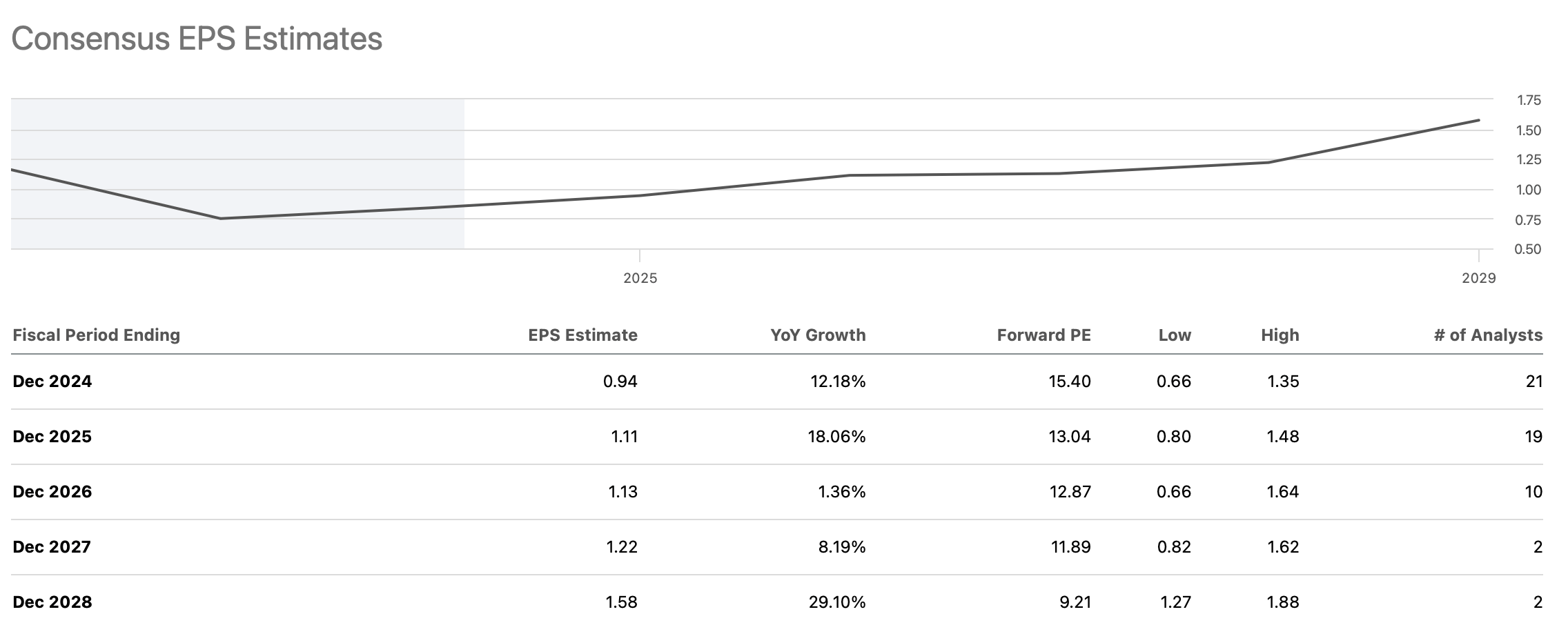

Estimates (seekingalpha.com)

Barrick's sales and EPS estimates seem predicated on stagnant or lower gold prices, which could be the opposite of what we will see. Gold's price should break out to new ATHs, moving higher in 2024-2025 and likely beyond as the Fed continues to ease.

EPS estimates (seekingalpha.com )

Due to higher-than-expected gold prices, Barrick is likely to surpass futures estimates, and future revisions should lead to a higher P/E multiple and a much higher stock price. Moreover, this dynamic is not Barrick Gold specific, as it concerns most major miners with ultra-low sales and earnings estimates that will likely get surpassed.

Barrick - 2024 year-end price target range: $18-24 (25-75% upside potential).

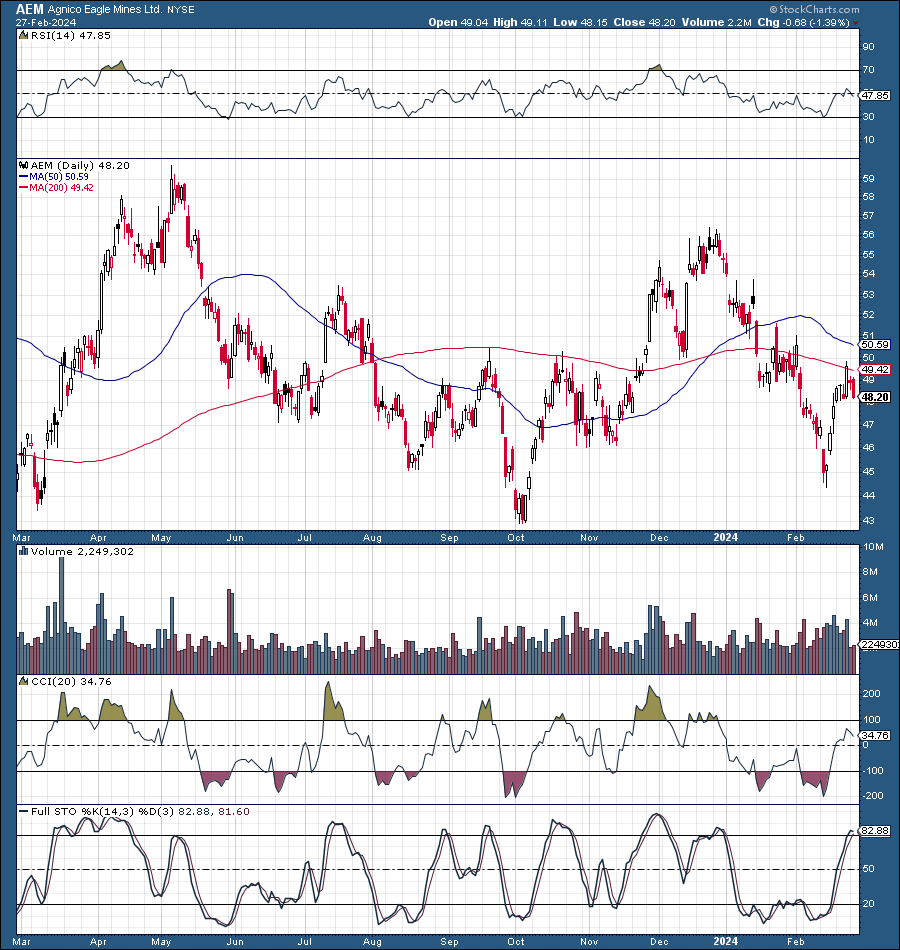

AEM (StockCharts.com )

Agnico Eagle Mines "AEM" has also formed a highly bullish long-term inverse head and shoulders pattern, suggesting that the low was put in around the $43-44 range. Moreover, this level represents crucial support now, and there is likely minimal downside threat ahead. On the upside, there is plenty of potential to break out above the $50-60 resistance zone in the next 6-12 months.

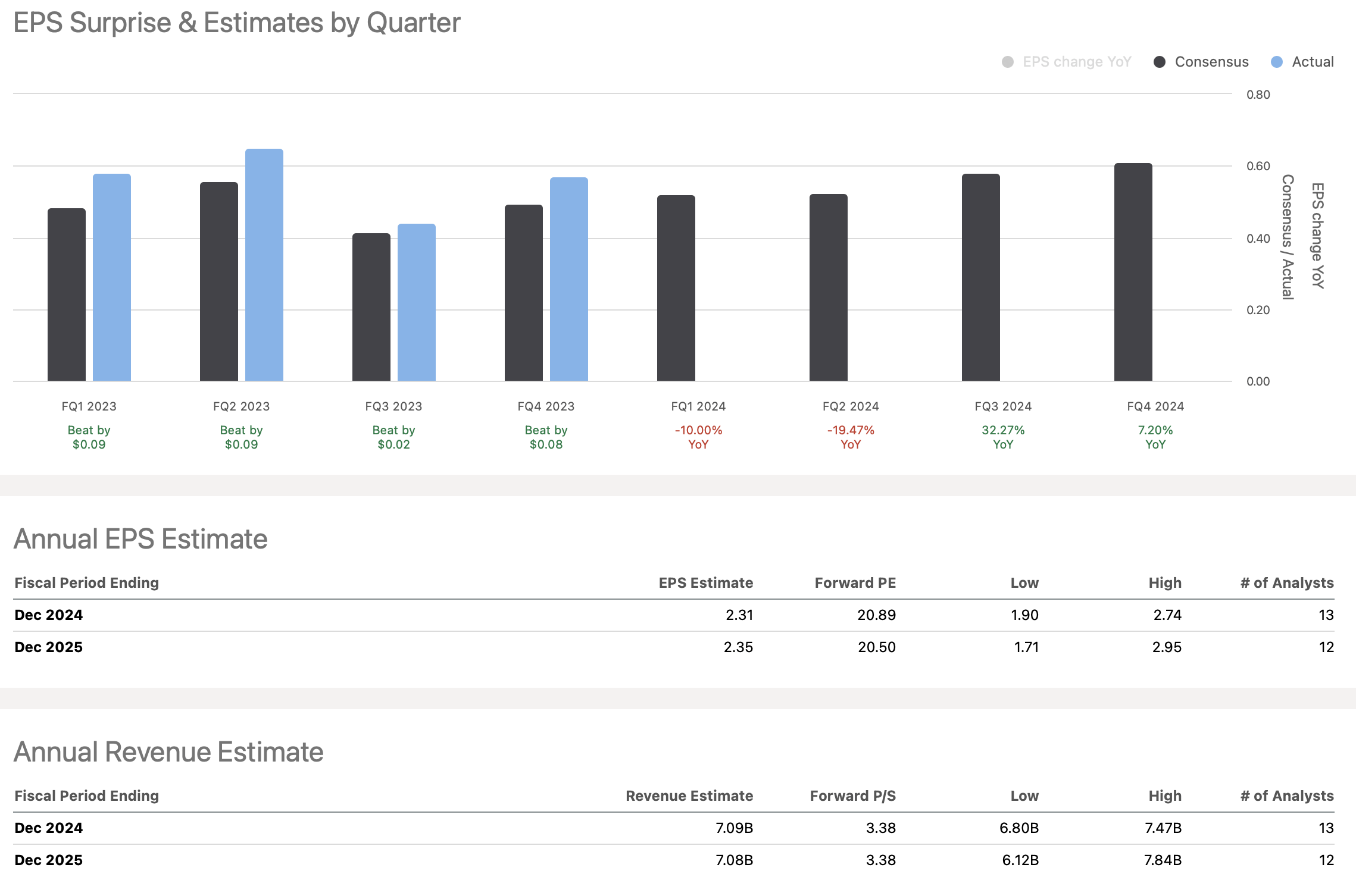

Fundamentally - AEM suffers from a similar problem plaguing Barrick and other high-quality gold mining companies. Despite outperforming recent estimates, forward projections seem ultra-low and would likely require the gold price to decrease.

Estimates (seekingalpha.com)

However, I have a different thesis based on gold prices increasing from here. Therefore, AEM's sales and EPS could be considerably higher than consensus estimates imply. Instead of the projected $2.35 lowballed consensus figure, AEM could earn around $3 next year, consistent with higher-end and, in my view, more realistic EPS projections.

$3 in EPS implies that AEM could be trading at 16 times next year's earnings, which is cheap for a company in AEM's position. AEM has significant growth prospects and is the third most considerable gold miner globally. Agnico also made wise acquisitions, building a healthy, long runway for growth.

Agnico - 2024 year-end price target range: $60-75 (25-55% upside potential).

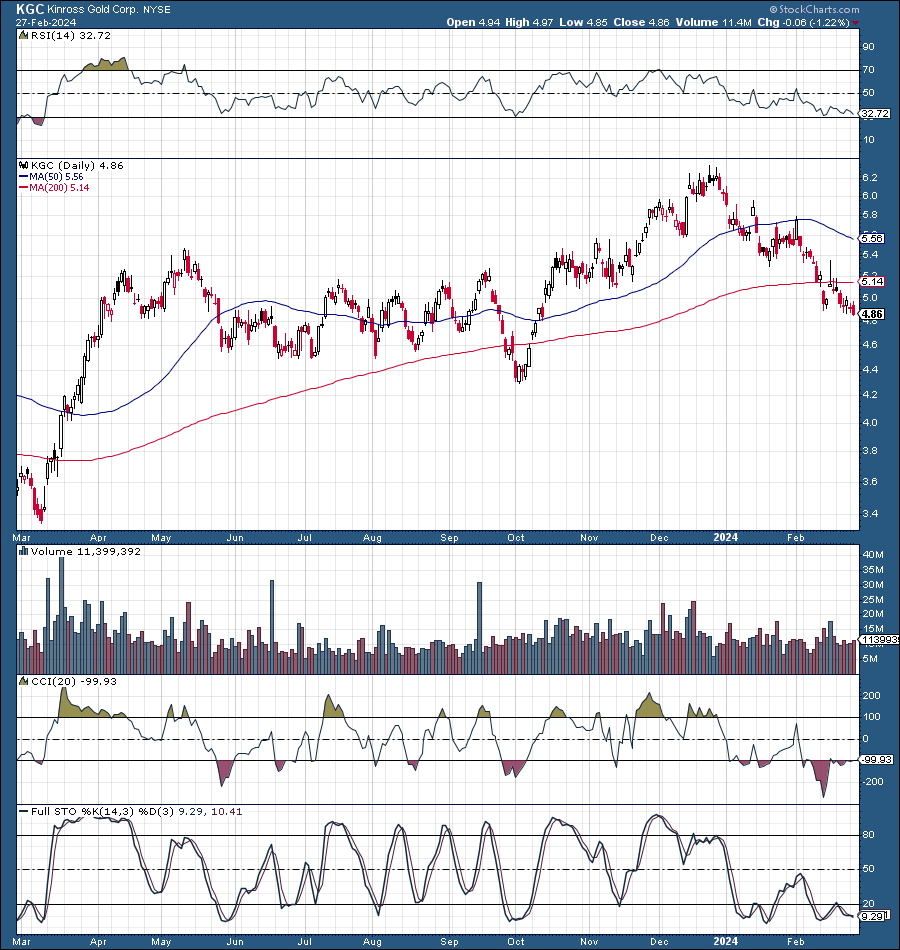

KGC (StockCharts.com)

Kinross has had a considerable correction, (dropping by 25%) since its recent highs. The stock has become oversold and is set up nicely for a solid rally into the year's second half. The recent selloff has been a badly needed correction that the market required to reset valuations, creating substantial long-term buying opportunities here. The CCI dipped to its lowest level in over a year, and other technical indicators illustrate improving momentum for KGC.

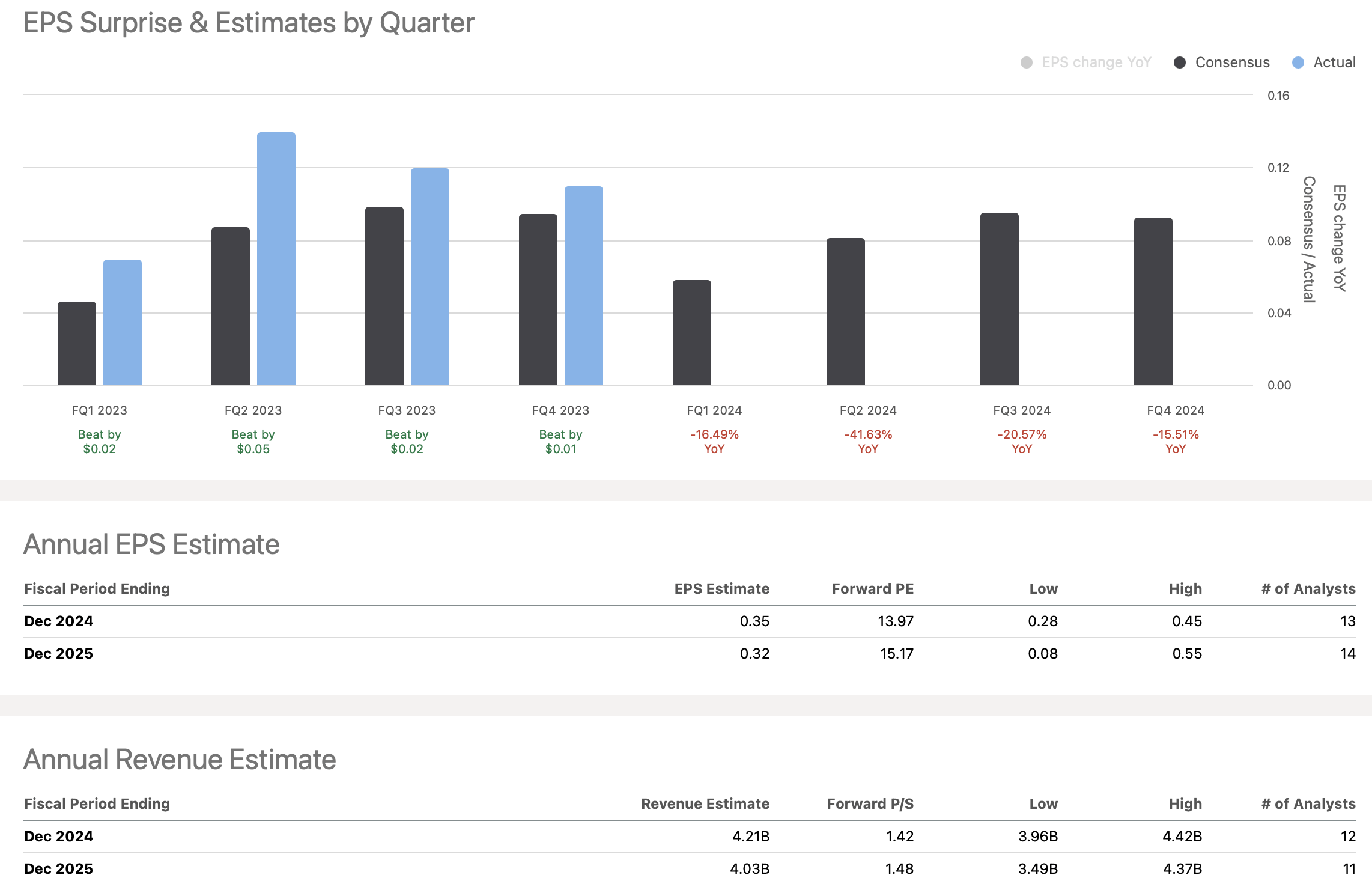

Fundamentally - Kinross is the seventh most significant gold miner globally. Kinross trades at a low multiple, 14 times this year's consensus EPS. Kinross has also surprised consensus EPS, which is considerably higher than expected in recent quarters.

Estimates (seekingalpha.com)

Despite its substantial beat rate, Kinross forward estimates remain depressed. We continuously see this dynamic of lowballed earnings with quality gold miners, likely because many estimates are still predicated on stagnant or a lower gold price ahead.

Nonetheless, Kinross's share price could appreciate considerably as gold heads higher in 2024 and 2025 due to monetary loosening. Many analysts may boost their sales, EPS estimates, and price targets, leading to multiple expansions and a much higher share price for Kinross stock.

Kinross - 2024 year-end price target range: $6.50-8.50 (35-77% upside potential).