M. Suhail/iStock Editorial via Getty Images

M. Suhail/iStock Editorial via Getty Images

Shares of KeyCorp (NYSE:KEY) have been an underperformer over the past, alongside most of the regional banking sector, as the industry faced pressures in the wake of Silicon Valley Bank’s failure. I last wrote about Key in October 2022, before the regional banking crisis, rating the stock a “buy.” Since then, it has returned just 3%, significantly lagging the S&P 500, though KEY has outperformed most regional banks with a leading ETF (KRE) losing about 16% of its value since then. Importantly, I believe Key’s asset mix leaves it well-insulated from ongoing pressures in commercial real estate, making shares attractive today.

Seeking Alpha

In the company’s fourth quarter, Key earned $0.25 in adjusted earnings, excluding the impact of an FDIC special assessment to cover its cost of bailing out depositors in failed institutions, alongside restructuring costs as Key works to reduce operating expense. The bank has faced many of the same funding pressures as peers as the industry has scrambled to retain deposits. Key has acquitted itself during this period of stress, and I believe with its balance sheet position fairly stable, it is well positioned for 2024 and 2025.

In all of my analysis of regional banks, I have begun by emphasizing the importance of stable deposits, which are the lifeblood of a bank. Considering the fact the entire industry essentially trades as a discount valuation, investors can be “picky” about which value stocks they buy, and a solid deposit base is a good initial screening. Key passes this test.

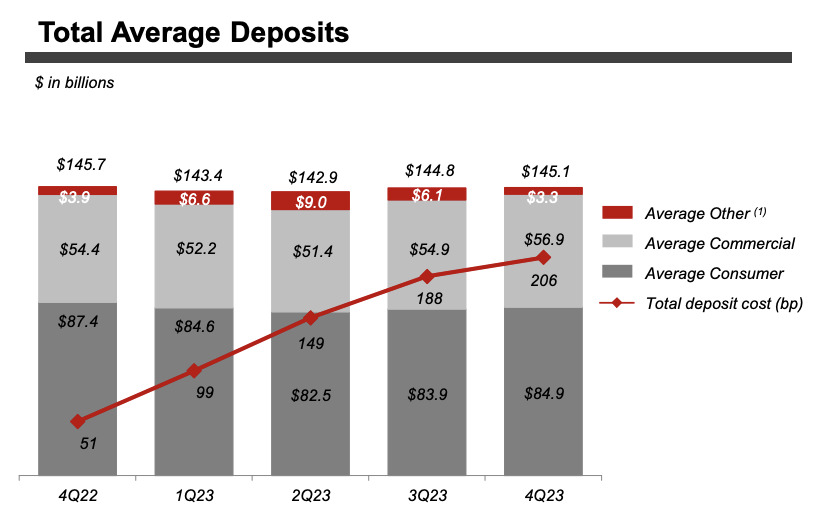

As you can see below, Key’s deposits fell by just 2% during the first half of 2023 and have subsequently recovered to essentially flat. Key has been aided by its focus on relationship banking, where it lends and provides treasury services to companies who deposit with them, creating a stickier deposit base. Additionally, 67% of deposits are insured or collateralized, making them less susceptible to a panic.

KeyCorp

Of course, like every bank, given the interest rate environment, the cost of deposits has increased substantially, from 0.51% a year ago to 2.06%. This has been due to both increased rates on interest-bearing deposits and a mix shift away from noninterest-bearing deposits. This mix shift is slowing as these transactional accounts near their lower functional limits. 22% of deposits are noninterest bearing, which was down 1% sequentially. We are seeing a deceleration in the rate of change in deposit yields. After rising about 50bp in Q1 and Q2, they rose 39bp in Q3, and just 18bp in Q4. Management sees pricing pressure on deposits easing, and barring further Fed rate increases, deposit yields should peak in Q1.

Because of higher funding costs, Key’s net interest margin (NIM) of 2.07% was down substantially from the 2.73% in Q4 2022 as loan yields did not rise as quickly and because of fixed rate securities. However, I was encouraged to see NIM expand by 6bp sequentially. Accordingly, net interest income of $928 million was up $5 million sequentially but down by $299 million from last year. I expect to see some further expansion of NIM in 2024. This is because Key’s asset mix optimization if taking hold. Given their conservative nature, in Q1 when deposits were flowing out of the industry, Key increased its wholesale funding to improve its liquidity, should it face pressure. While deposit costs have risen, they are cheap relative to market funding. Wholesale funding typically costs over 5.3%. Shifting away from this funding back to deposits at 2% has helped to relieve pressure on NIM. With its deposit base proving resilient, since the end of Q1, Key has paid down $11.5 billion of debt, helping to mitigate funding costs.

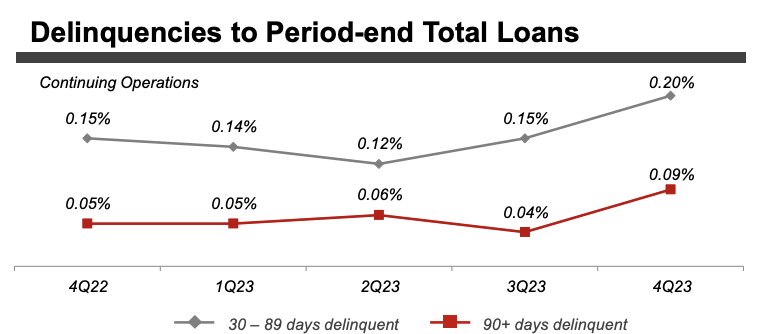

At the same time, Key has been pruning its assets to maximize its capital efficiency. Loans were down $3.7 billion to $113.9 billion in Q4 as it reduced business lending to non-relationship customers. Credit quality remains sturdy. While delinquencies have risen, just 0.29% of loans are more than 30 days delinquent, a very healthy level. Charge-offs continue to be muted at 0.26%. Key has also been conservative in reserving for future losses. Nonperforming loans are 51bps of its total portfolio, while allowances are 1.6%, proving more than 3x coverage of NPLs. I view 250% as a health level of reserve coverage to guard against further delinquencies. With 300+% coverage, KEY can afford to see a further tick-up in NPLs without having to boost reserves materially.

KeyCorp

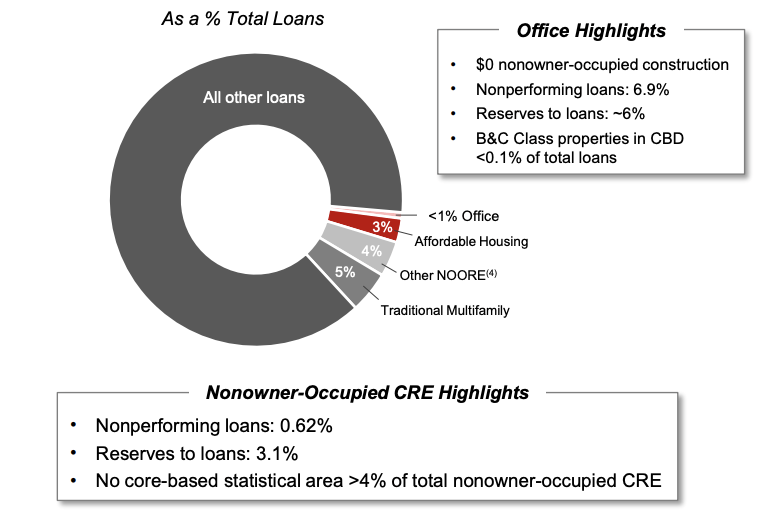

This conservative reserving is consistent with Key’s approach to its business, and it is fundamentally different than the reserve levels a bank like New York Community Bancorp (NYCB) carried. Additionally, Key’s loan book is very different. NYCB, like other banks, is seeing pressure in commercial real estate (CRE), including NYC multifamily. Well, as highlighted in a February investor update, KEY has no exposure to NYC-rent controlled apartments. Additionally, while many regional banks have CRE-focused loan books, Key is an exception. Key is primarily a business lender, with just ~13% of loans in CRE. Here it also has 5x reserve coverage of NPLs, meaning it has already braced itself for further weakness.

KeyCorp

If we see the CRE situation continue to worsen, KEY is likely to be a safe haven within the regional banking sector, given its small CRE portfolio, solid reserves, and less than 1% exposure to the most troubled asset class, office. Key is likely to face more losses in a traditional business cycle downturn, given its larger C&I loan book, but here, the outlook is brighter. Corporate profits are strong, and it appears increasingly likely that the Fed has engineered a soft landing.

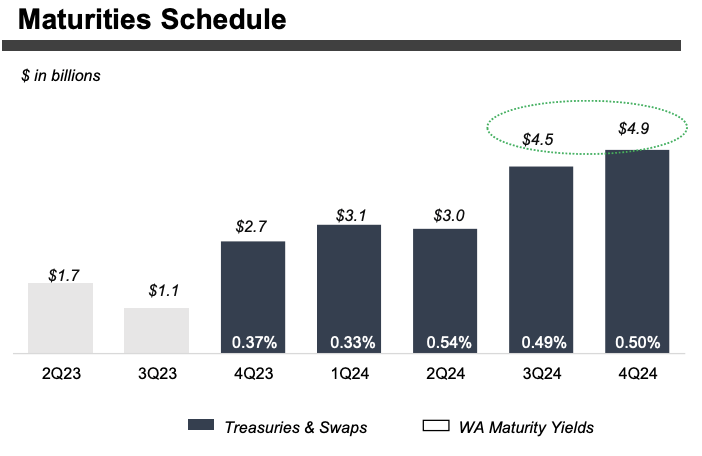

As with most banks, Key also has a portfolio of high-quality fixed income securities. It has been allowing the portfolio to shrink by not full reinvesting maturities. As such, it now totals $44.3 billion, down $2 billion sequentially and $5.9 billion from a year ago. I would expect to see this portfolio to continue to shrink in 2024. As you can see, there are substantial maturities of fixed rate swaps and treasuries, which can then be redeployed at higher rates, via either loans or other securities. These maturities will be an over $200 million tailwind for 2025’s net interest income, providing a $0.15-$0.17 tailwind to EPS.

KeyCorp

Now because Key owns bonds at lower yields, it has an unrealized loss that sits in accumulated other comprehensive income (AOCI). Key has a $5.2 billion loss in AOCI. If the forward curve plays out, this will decline to $4 billion at year-end 2024 and $3.4 billion at year-end 2025. If rates stay at current levels, this will still decline, though not quite as much, to $3.6 billion. This is because bonds at a loss gradually pull to par and pay back at $100. Key does not need to sell any bonds at a loss given its strong liquidity profile.

This AOCI loss is important, though because it will gradually be phased into Key’s capital calculations as it has over $100 billion in assets. This is why Key is carrying more capital than its 9-9.5% common tier 1 equity ratio (CET1) target. In Q4, Key’s capital rose to 10.0% from 9.1% a year ago and 9.8% in Q3. Key is building in a buffer for this gradual phase-in. Holding all else equal, Key’s capital position will be closer to 8% fully accounting for the AOCI loss at the end of 2025 (in practice this loss will only be phased-in gradually), and Key should retain over $1 billion in capital the next two years to bring capital back toward the low-end of its target. I would expect to see its headline capital ratio continue to build in 2024.

For this year, Key expects to hold loans flat to end of 2023 levels in 2024, meaning they will be 5-7% lower on average. Average deposits are expected to be flat to down 2%, as it allows its highest cost funding to roll off. This combination will push net interest income down 2-5% for the year. However, that is still up low-single digits from Q4 2023 levels with an exit rate up double-digits. There will then be further gains in 2025 as benefits from low-yielding securities maturing build. Additionally, increased capital market activity should boost fee revenue by at least 5% while it holds noninterest expense flat. Net charge-offs are expected to be 30-40bp.

Altogether, this implies about $1.20-$1.30 in 2024 EPS, and about $1.60-$1.85 in 2025 EPS as its net interest income continues to recover, given the tailwind of maturing securities and declining deposit yields after the Federal Reserve rate cuts eventually commence.

Of course, all investments have risk. In the case of Key, as with all banks, there are several. Key is less exposed to a real estate downturn, but a general recession that reduces corporate profits would impact its loan book more and likely force an increase in reserves. Given its strong reserve positioning today and a likely soft landing, I view this risk as manageable. Additionally, if we saw inflation rise and force the Fed to raise not cut rates, this would worsen Key's AOCI position and push out any potential buybacks beyond 2025 in all likelihood. I will also monitor Key's deposit base. I expect deposit costs to peak in Q1; if they remain elevated beyond that, its NIM recovery could take longer than I currently forecast.

Given all of this in my base case, I would expect shares to migrate to $17-18 over the next 12 months, or 9-10x 2025 earnings as we see the benefits each quarter of reinvestment and improved NIM trends. Most regional banks, like Citizens Financial (CFG), Huntington (HBAN), Comerica (CMA), Capital One (COF), and U.S. Bancorp (USB) are trading about 9.7-10.7x earnings. Ultimately, given the pressures the industry faced last year, I believe it prudent to assume limited multiple expansion, especially as many firms work through fixed security losses before they can materially turn on buybacks. As such, I expect KEY to have a ~10x multiple in my base case, and rising earnings are the primary driver of my price target, rather than multiple expansion,

Additionally, I would note that with so many regional banks facing CRE-losses, Key’s minimal exposure here could enable significant positive divergence in credit trends, increasing the attractiveness of shares. Combined with a 5.5% dividend yield, shares offer a 20% total return potential, and I view them as a buy.