gynane

gynane

KB Home (NYSE:KBH), while demonstrating some recent resilience in the face of fluctuating mortgage rates, may soon find itself navigating a more turbulent housing market. Amidst the flurry of builder incentives and signs of buyer reemergence, a crucial question lingers: has the market truly found its bottom, or is the recent uptick merely a prelude to a looming supply glut? As investors consider KB Home, it's vital to examine whether the company is adequately positioned to weather a potential period of oversupply and the pricing pressure it could bring.

I last covered KB Home in March 2018 in my article, KB Home: Increased Risks, in which I argued that the company's valuation was stretched after a material run-up in the stock price, and the stock was volatile but essentially flat for the following four years from March 2018 through October 2022.

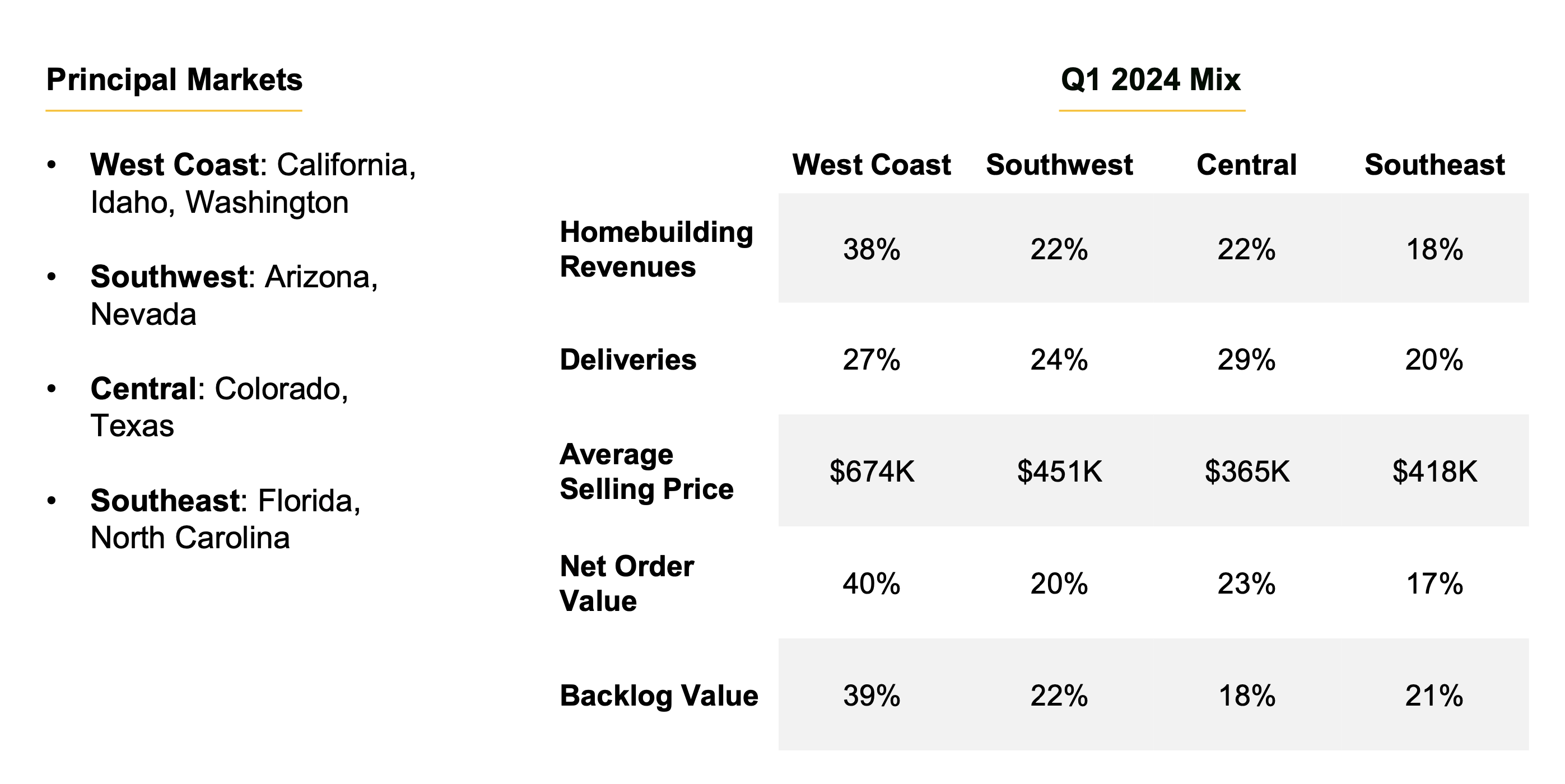

KB Home is a major player among national homebuilders in the United States. With over six decades of experience, the company operates in 47 markets across nine states.

KB Home

KB Home distinguishes itself through its emphasis on customization. Buyers are granted a significant degree of flexibility in selecting homesites, elevations, floor plans, and design features. This tailored approach caters to diverse preferences while maintaining a commitment to affordability.

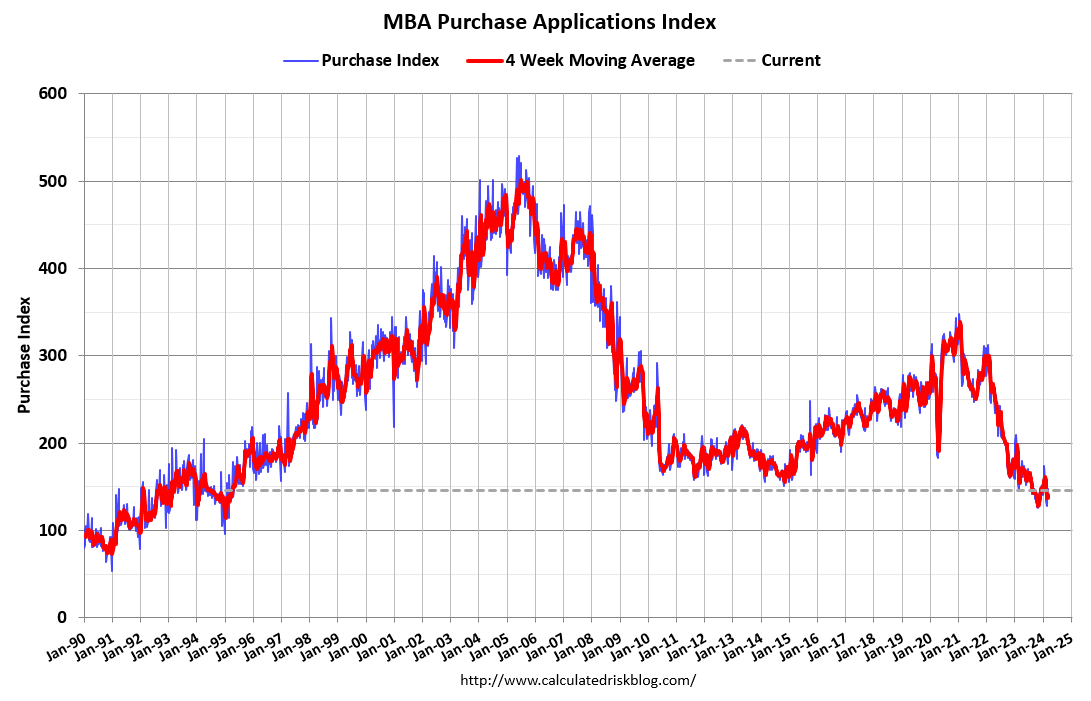

High mortgage rates pose a significant challenge to KB Home and the broader housing market. With rates fluctuating and affordability stretched, potential buyers are becoming more hesitant to move forward with purchases. The following graph illustrates the weekly Purchase Mortgage Applications index, which is at a three-decade low.

Calculated Risk Blog

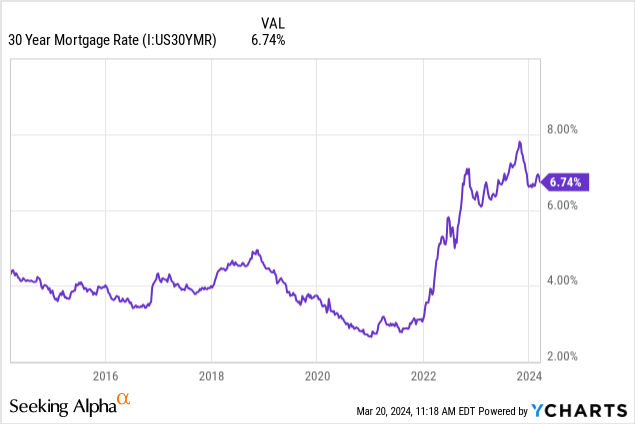

The following graph illustrates the recent surge in 30-year mortgage rates, which is the primary reason why housing demand, as measured by the weekly purchase mortgage applications index, is near a three-decade low:

Buyers' hesitation leads to reduced demand, forcing builders like KB Home to either compete more aggressively on price or face the prospect of unsold inventory accumulating. Additionally, the easing employment market casts a shadow over the housing sector, as I discussed in my recent article, Employment Market Is Weakening, and I recommend reading it.

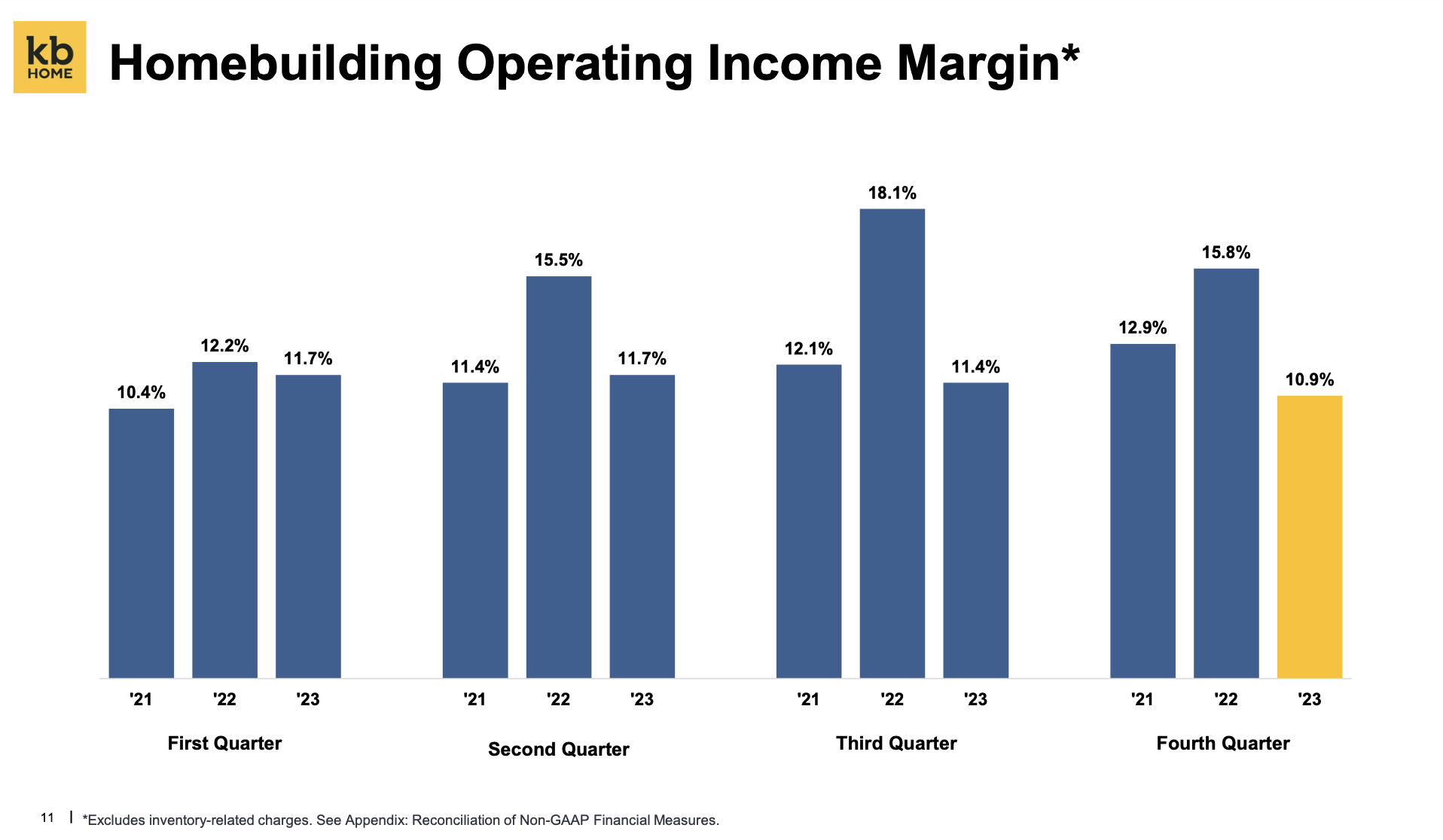

KB Home's financial performance in recent years highlights a somewhat concerning trend, as the company's quarterly operating income margin as of Q4 2023 had declined to the bottom of its range in the last three years, and Q1 2024 results show similar trend, as I discuss further along in this article:

KB Home

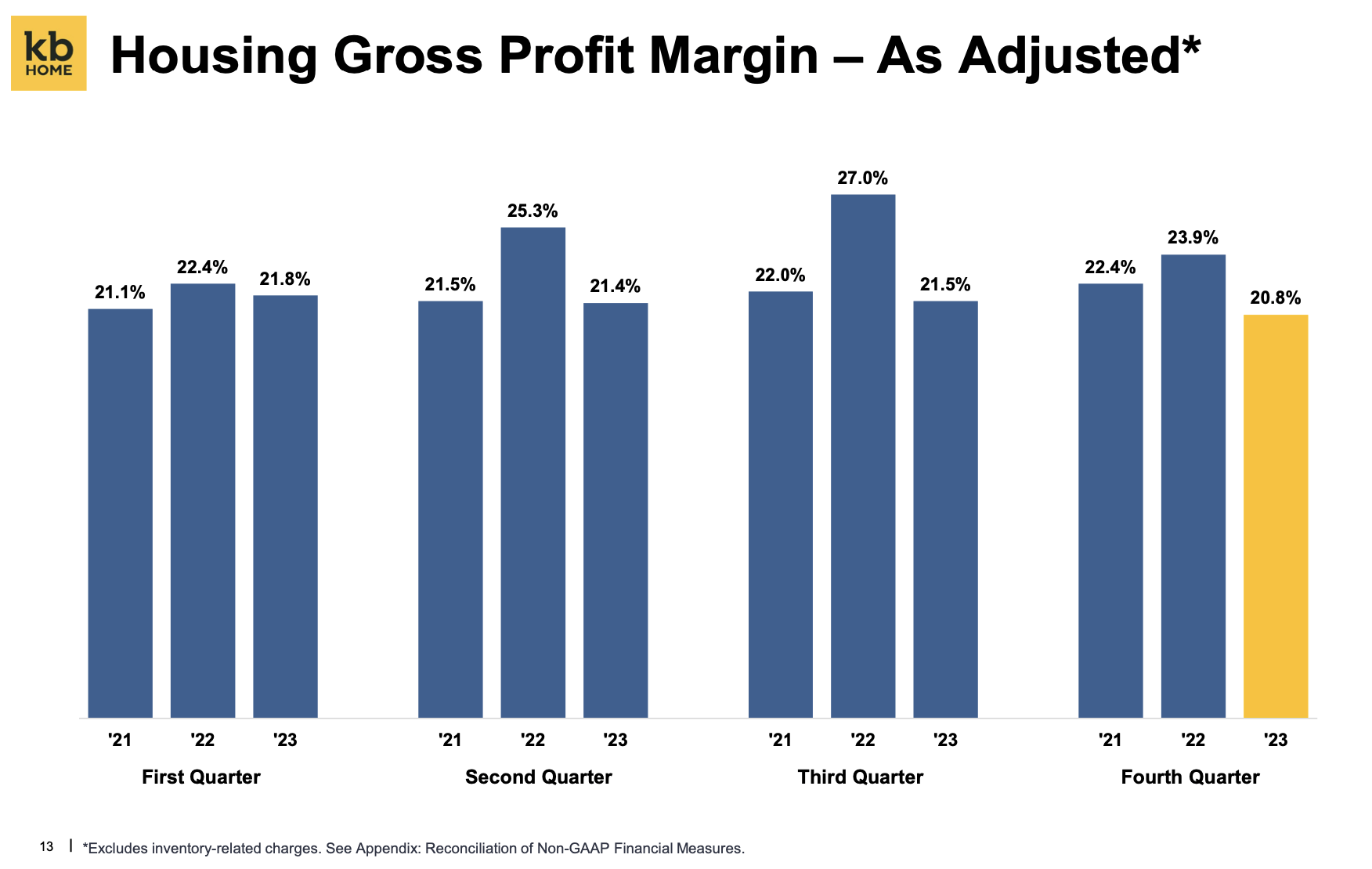

Furthermore, the company's gross margin, adjusted to exclude inventory-related charges, was 20.8 percent in the fourth quarter of 2023, lower than every other quarter in the last three years, as the following graph illustrates:

KB Home

This indicates potential difficulties in maintaining profitability amidst challenging market conditions. Management noted that the 3.1 percent year-over-year drop in adjusted gross profit margin was due to price decreases and other homebuyer concessions, as well as higher construction costs.

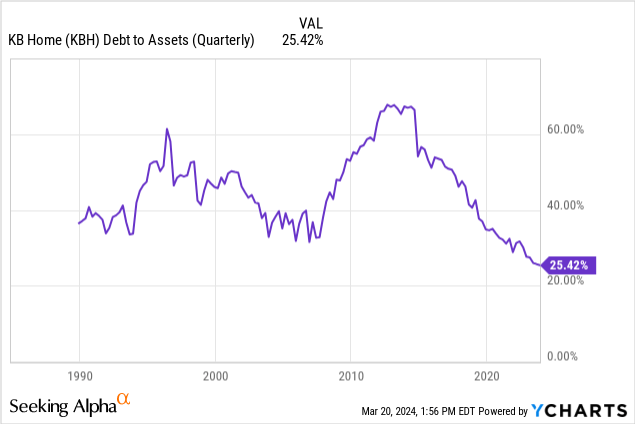

In contrast to the company's somewhat deteriorating income statement, KB Home's balance sheet has improved consistently since the acute housing crisis of early 2000s, and its balance sheet leverage as measured by Debt to Assets ratio is at the lowest level in the company's publicly traded history:

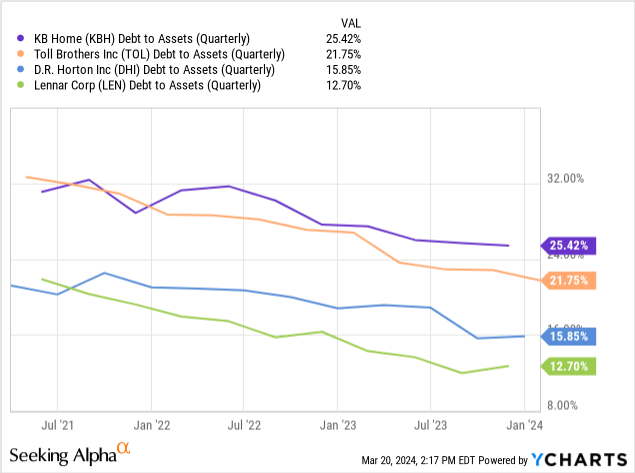

Having said that, however, the company's balance sheet leverage has not improved as much as those of its larger peers, such as Toll Brothers (TOL), D.R. Horton (DHI), and Lennar (LEN), as the following graph illustrates:

In light of the above financial analysis, let's review the company's valuation.

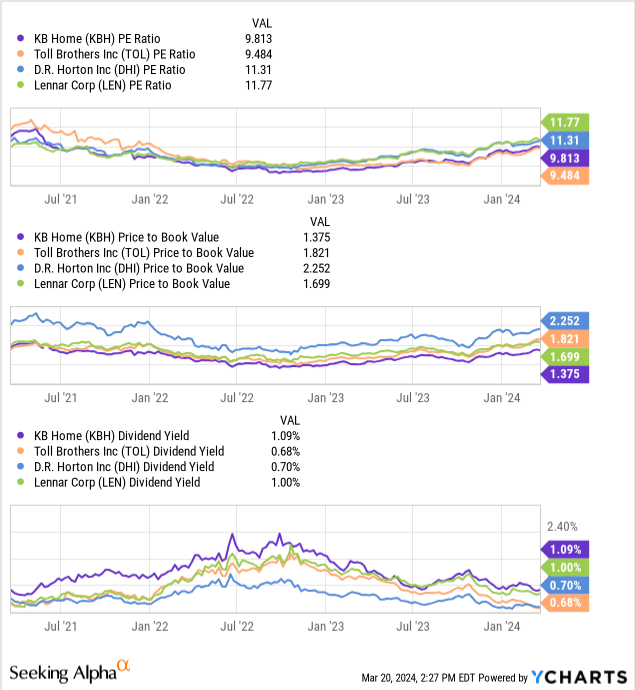

The following graph compares KB Home's select valuation metrics to peers:

My two key takeaways from the above graphs:

KB Home's dividend yield is slightly higher than those of its peers, but despite the company's declining profit margins, I deem the company's dividend yield safe, due primarily to its healthy balance sheet and positive free cash flow.

KB Home announced results for the three-month period ended February 29, 2024 on Wednesday (comparisons are year-over-year):

Most relevant to the discussion in this article is the company's guidance of operating income margin for 2024:

I note that the company is not forecasting a material increase in its operating margin for 2024, and even if the company achieves its guidance, its operating income margin would still be near the bottom of its three-year range.

Further, a bright spot in the company's Q1 2024 results is the 55 percent jump in net orders in the quarter, and if that continues throughout the quarter, it could ease my concern around the 17 percent year-over-year drop in backlog.

KB Home faces a mixed outlook. While demonstrating resilience in a volatile market, the specter of potential oversupply, coupled with stubborn mortgage rates and a softening labor market, casts uncertainty over its near-term prospects. The company's recent margin compression further highlights the challenges in maintaining profitability within the current environment.

Despite a seemingly attractive valuation compared to some peers, I believe the headwinds in the housing market will translate into volatile times for the company in the near term. I rate the stock HOLD due to its favorable valuation multiples, but I would wait for lower prices for an initial position.