Chung Sung-Jun/Getty Images News

Chung Sung-Jun/Getty Images News

KB Financial Group (NYSE:KB) has set itself apart from Korea's other big banks in recent years - not only by diversifying into fee-related, non-bank businesses but also higher-growth Southeast Asian markets. The result is a diversified earnings base that has delivered steady growth despite a slower Korean economic backdrop. Recent Q4 reporting was more of the same, as despite the bank taking some big one-off provisions, strong non-bank profits kept the group bottom line well insulated. Also, positive was that new management has been consistent in its shareholder return focus, setting out a clear path to even higher payouts in 2024.

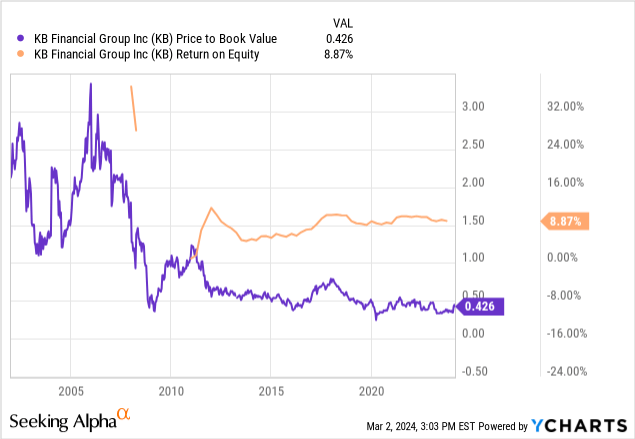

To be clear, KB Financial isn't completely out of the asset quality woods just yet, but its best-in-class capital position and the prospect of rate cuts later this year should keep the group well on track to meet its targets. Relative to a sustained high-single-digit % return on equity profile, the bank's current ~60% book value discount offers a compelling entry point, particularly with a big corporate reform ('value up') catalyst on the horizon.

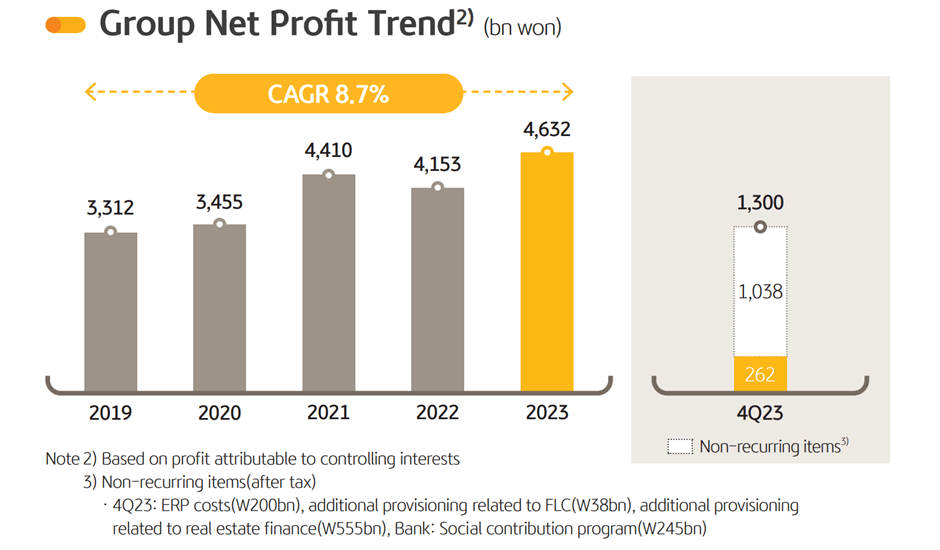

For the most part, KB Financial has continued to post resilient earnings numbers through a challenging period. Q4 2023 was more of a 'kitchen sinking' quarter, though, as some very significant provisioning led to a below-par net income result. Adjusted for one-offs, on the other hand, the group maintains impressively resilient underlying fundamentals, particularly on the non-bank side, where rising profits from the securities and insurance subsidiaries have helped massively. In contrast, the core banking business is stalling out, as a combination of peaking interest rates and higher funding cost pressures led to a slight drop in net interest margins. Still, the relative NIM defensiveness stands out relative to peers, many of which saw their margins peak far earlier. The higher non-bank contribution is another key differentiator, in that it adds a defensive element to KB Financial's otherwise rate-sensitive earnings base.

KB Financial

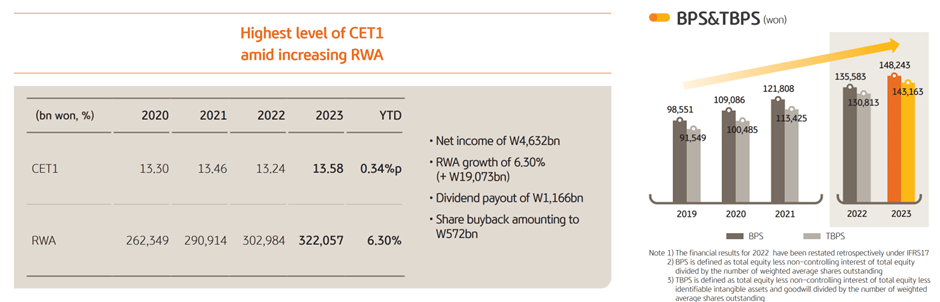

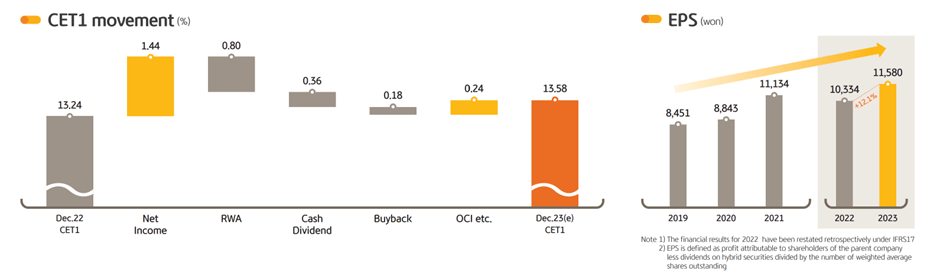

Looking past the headline earnings number, though, management's full-year shareholder return payout, comprising both buybacks and cash dividends, was (rightly) well-received by the market. Note that the 2023 payout is up five to six percentage points from 2022, with the buyback portion almost doubled this time around. The announcement was also significant in that it erased any lingering doubts about strategic continuity under new CEO (and former Vice President) Yang Jong Hee, who only just took the helm late last year. Even after upsizing the capital return, there remains capital headroom for more returns going forward (CET1 well above the 13% minimum, including a stress buffer.), so a >40% total shareholder payout may well be on the cards for 2024.

KB Financial

Provisions may have been sharply higher, but the group's non-performing loan ratio increased by a very modest ~8bps sequentially, while delinquency rates actually dropped relative to last quarter. So even if we do see a non-performing loan ratio spike sometime in the future (vs. the currently low 0.8% level), the bank should be well-covered. For now, though, I see KB Financial's two major asset quality risks, from equity-linked securities (tied to Chinese indices that have suffered heavy losses) and property, as very manageable. Yes, KB Financial has more China equity-linked securities exposure than other banks and could well face the regulatory music down the line. But in light of the Chinese equity resurgence over the last month, the bank could get away with a smaller fine than many expect. And on the real estate financing front, exposure is more limited and higher quality (think better terms and better collateral) than the smaller lenders, many of which will bear the brunt.

KB Financial

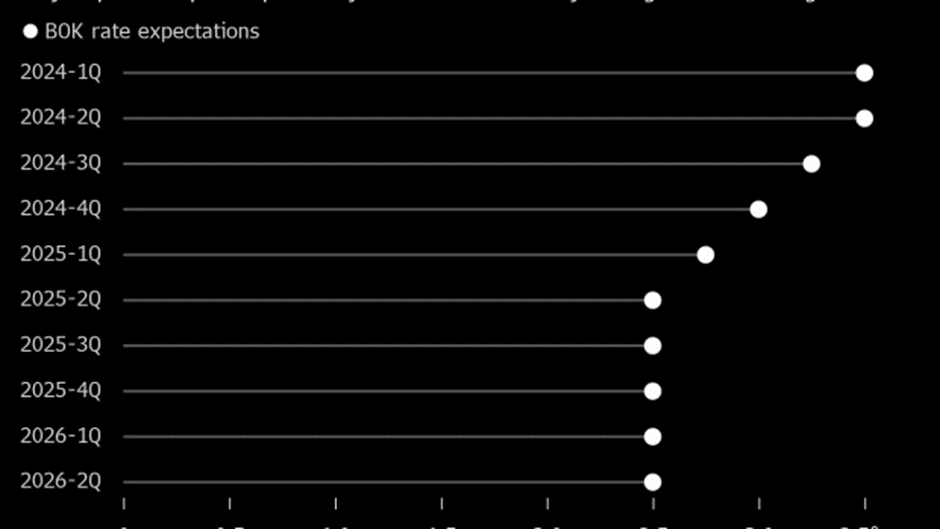

Perhaps the biggest asset quality tailwind, though, is that the Korean central bank, the Bank of Korea (the BoK), looks poised for interest rate cuts later this year. Fundamentally, the case for a pivot is compelling - in addition to a series of disinflationary monthly prints and the prospect of easing supply-side pressures globally, Korea has seen slower growth, particularly on the domestic consumption side. In the likely event we see inflation converge with the BOK's 2% target soon, I wouldn't be surprised to see a more aggressive monetary easing path than many expect.

Beyond addressing the asset quality overhang, non-interest income gains from the securities portfolio will also be worth keeping an eye on, as one-offs here could spring some upside surprises in a declining rate environment. So for the near term at least, KB Financial will probably be a net beneficiary of lower rates - despite a likely initial hit to net interest margins.

Bloomberg

KB Financial may have re-rated in recent weeks on the heels of a resilient quarter and a smooth CEO transition, but the risk/reward remains very attractive here. Not only is this among the very best dividend plays in Korea at the current mid-single-digit % yield, but it also has a clear path to an increased payout (buybacks and dividends) in 2024. Meanwhile, concerns about asset quality, even if warranted to some extent, are more than accounted for in the ~60% book value discount. Inversely, the market is assigning little value to KB Financial's capital adequacy nor to its diversified earnings base, which should quite easily support the capital return story through the cycles. Ahead of a catalyst-rich next few months, featuring potential rate cuts in H2 and a market-wide 'value up' program to narrow the 'Korea discount,' there's still plenty to like here.