Daniel Grizelj

Daniel Grizelj

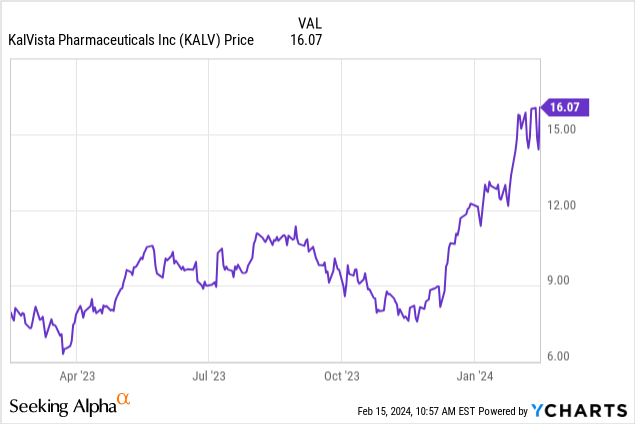

KalVista Pharmaceutical's (NASDAQ:KALV) stock is up over 65% since my "Buy" recommendation in October. On Tuesday, they announced positive phase 3 data for its oral therapy, sebetralstat, as an on-demand treatment for hereditary angioedema, a rare disease. KalVista's stock was relatively unmoved after this success, but this did come the same day inflation numbers came in higher than expected, muting hopes of rate cuts later this year by the Federal Reserve. To be fair, positive results were also largely expected, and much of it was likely priced into KalVista's stock.

The focus now shifts to sebetralstat's commercialization. I ruminate on this below and discuss whether or not KalVista continues to merit speculation after its rally leading into phase 3 data.

In its phase 3 KONFIDENT clinical trial for sebetralstat, an oral treatment for hereditary angioedema ('HAE'), KalVista showed efficacy and safety, meeting all primary and secondary objectives. Sebetralstat significantly outperformed placebo in accelerating symptom relief, with the 300 mg dose taking 1.61 hours and the 600 mg dose taking 1.79 hours, compared to 6.72 hours with placebo.

Takhzyro (lanadelumab), Cinryze, Haegarda, and Orladeyo (oral) are prophylactic therapies, while Firazyr (icatibant) and Berinert are on-demand treatments that require subcutaneous administration. These therapies vary in mechanism of action, dosing regimens, and routes of administration, creating a complex market for HAE. However, sebetralstat's rapid onset of symptom relief, oral administration, and favorable safety profile further enhance its appeal, suggesting a competitive edge in the on-demand segment of the HAE market. Given these factors, sebetralstat could well carve out a niche for KalVista, appealing to patients seeking faster, more convenient relief without the burden of injections.

Peak annual sales estimates for sebetralstat are typically near $500 million. I think this is an optimistic, but reasonable, projection. This is approximately equivalent to KalVista's current market capitalization, meaning that the business is trading at only 1x the peak annual revenue of its lead asset.

KalVista intends to submit a New Drug Application, or NDA, for sebetralstat in the first half of this year.

Turning to KalVista's balance sheet, the combined value of 'cash and cash equivalents' and 'marketable securities' stands at $103.2 million, with cash and cash equivalents at $57.7 million and marketable securities at $45.5 million. When assessing the company's liabilities, the current liabilities total $17.8 million, which includes accounts payable, accrued expenses, and the current portion of lease liability. The long-term liabilities are comprised of the lease liability net of the current portion, totaling $6.5 million. The current ratio, calculated as total current assets divided by total current liabilities, is approximately 7.2, indicating a solid liquidity position.

Over the last six months, the net cash used in operating activities was $46.6 million, leading to a monthly cash burn of approximately $7.8 million. Given the liquid assets of $103.2 million, the cash runway is roughly 13.2 months. This analysis, based on past data, may not necessarily predict future performance accurately.

Today, the company priced a $160 million share offering. This is expected to significantly extend their cash runway beyond 13 months.

According to Seeking Alpha data, KALV's market capitalization stands at $554.32 million, reflecting a moderate size in the biotech sector. The company's growth prospects are notable, with analyst revenue projections indicating a dramatic increase from $2.97 million in 2024 to $116.62 million by 2026, suggesting a commendable growth trajectory. Stock momentum is strong, outperforming SPY with a 101.51% increase over the past year, indicating robust investor interest and confidence in KALV's potential.

Short interest is substantial at 16.79%, representing a sizable bet against the stock, which could lead to a short squeeze if KALV continues to perform well. Per Nasdaq, institutional ownership is remarkably high at 106.83%, with new positions outnumbering sold-out positions (1,349,867 new vs. 809,643 sold out), highlighting institutional confidence. Notable institutions include Tang Capital Management and TCG Crossover Management. Insider trades reveal positive net activity, with 1,123,146 more shares bought than sold over the past three months, suggesting insiders are bullish on the company's future.

Based on these metrics, the company's market sentiment can be characterized as "robust," underpinned by strong growth prospects, significant stock momentum, and positive insider trading trends.

In conclusion, despite nearly doubling in the past year, KalVista remains an attractive investment opportunity due to its breakthrough with sebetralstat. The stock appears undervalued, trading at roughly 1x its estimated peak annual revenue for sebetralstat, which signals upside for investors.

However, deep divisions in investor sentiment, mirrored by a high short interest in KALV shares, suggest price swings ahead. External pressures, such as inflation and Federal Reserve decisions, could also continue to sway the biotech sector, eclipsing even the most promising innovations. Moreover, sebetralstat could struggle to gain traction in a crowded market with players much larger than KalVista. It's also possible that the FDA does not approve sebetralstat, delaying its market entry.

Diversification and hedging can protect investments from these concerns. Watching institutional and insider activity may reveal early market or corporate movements.

KalVista's sebetralstat, robust liquidity, and expected growth trajectory support a "buy" rating. The company is transitioning from clinical developments to the market, giving investors a rare chance to participate at a critical turning point. However, an informed, cautious stance is necessary to balance potential gains with financing needs and market moods.