AnthonyRosenberg

AnthonyRosenberg

I am giving Jerash Holdings (US), INC. (NASDAQ:JRSH) a sell rating due to several large risks the company is up against. V.F. Corporation (VFC) (a customer of JRSH) is currently experiencing problems with profitability and this one company made up 63% of JRSH's business sales last quarter. Five of the last six fiscal quarters VFC has had a negative net income and although the company did bring on a new and talented CEO it is unclear if the changes VFC will make to their business will affect JRSH negatively. The reason this is so unclear is because JRSH does not have any long-term contracts with their customers and anyone who gets merchandise made from JRSH can move to alternative clothing manufacturers immediately. VFC's orders also happen to be JRSH's most profitable products. If 63% of JRSH's business was lost overnight it would, needless to say, have an adverse effect on the company.

JRSH is a holdings company that makes clothing products in Jordan, focusing primarily on sports clothing and outerwear. JRSH sells the vast majority of these products to the United States of America but does receive sales from other countries, primarily Hong Kong and Jordan. 77.4% of JRSH's sales come from just two companies, VF Corporation and New Balance.

While most households are probably unfamiliar with VF Corporation, they are probably aware of the many clothing brands the company owns. JRSH makes products primarily for these three VFC brands The North Face, Timberland, and Vans.

Brands That JRSH Manufactures For VF Corporation (VFC.com)

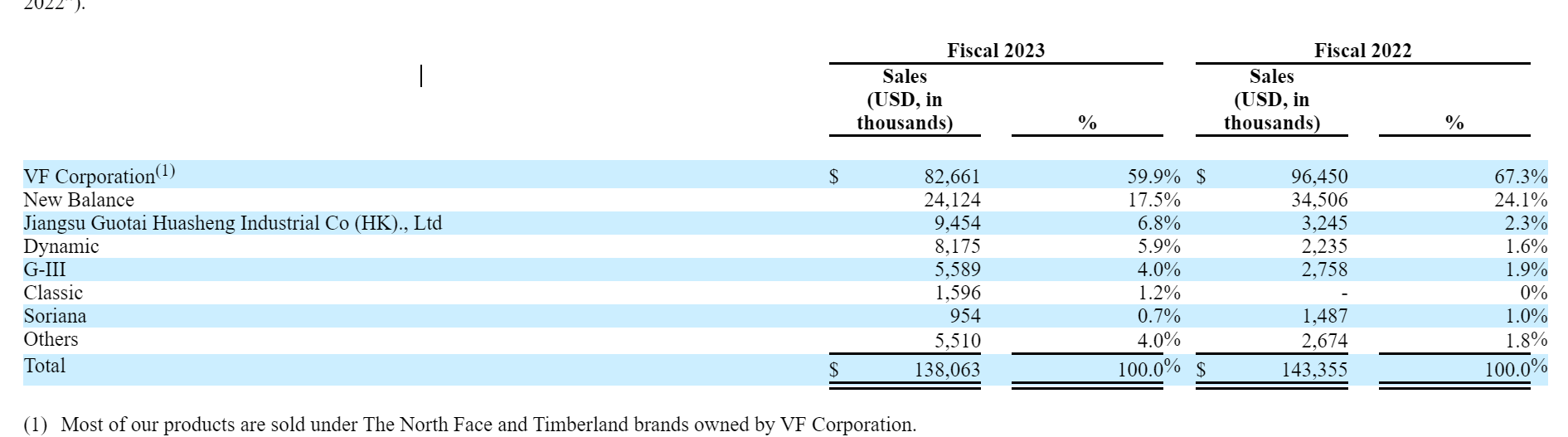

These products also happen to be some of JRSH's higher profit margin products. In JRSH's Fiscal 2023 VFC made up 59.9% of JRSH's total sales accounting for $82.66 million of JRSH's $138.06 million in total sales that year.

JRSH's Sales Fiscal 2023 And 2024 (JRSH 2023 10-K)

VFC has not had a positive net income in five of its last six quarters. In order to steer VFC back towards profitability the company's CEO Mr. Bracken P. Darrell announced this February that VFC was carrying out a strategic review of all of its brands and that any of them could be on the chopping block. Timberland has been an underperformer for VFC since the company acquired the brand in 2011 and currently there is a lot of speculation VFC could divest itself from Timberland. If this was to occur the future of Timberland's production could become uncertain.

Should during VFC's strategic review the company find opportunities to increase their margins by moving the production of their The North Face, Timberland, or Vans brands somewhere else JRSH would almost inevitably be unable to replace that sales volume. Even if they did, this new production would likely be made up of lower margin products.

JRSH is spending a lot of money betting on future sales growth. JRSH spent $8.7 million in 2022 and $13.8 million in 2023 on capital expenditures. This is being spent on increasing the production capacity of its current businesses through expanding their current facilities as well as buying other companies in order to absorb their productive capacities.

In 2023 alone JRSH spent $13.8 million on investments in new plants and machinery, the construction of a dormitory, a factory expansion, the acquisition of Kawkab Venus, and the acquisition of Ever Winland. According to JRSH's most recent 10-Q they expect to spend another $4.7 million in 2024 and $12.6 million in 2025 in capital expenditures. If VFC was to suspend business with JRSH these newly acquired assets would likely become idle and greatly impede JRSH's bottom line.

The Jordanian local sales tax rate is 16% but from 2015 to 2018 Jordan wrote an exemption for JRSH, and in 2018 that exemption was extended to February of 2024. If this exemption runs out and JRSH has to all of a sudden pay a 16% sales tax it would, for obvious reasons, likely affect Jerash's profitability. I have yet to hear an announcement from JRSH concerning this tax exemption status and before giving this stock a buy rating would want some sort of signal on what the Jordanian government was likely going to do concerning the company's sales tax.

JRSH has also had its income taxes lifted continuously since 2021. The zoning JRSH operates most of its businesses from was considered a free zone but was changed into a developmental zone and in 2021 JRSH had to pay a 16% income tax plus a 1% social contribution tax. Since 2021 that rate has increased each year and is now is at a "19% or 20% rate, plus a 1% social contribution tax". This 21% tax rate that has come up on JRSH over the course a couple of years will also likely put a damper on future profits from JRSH.

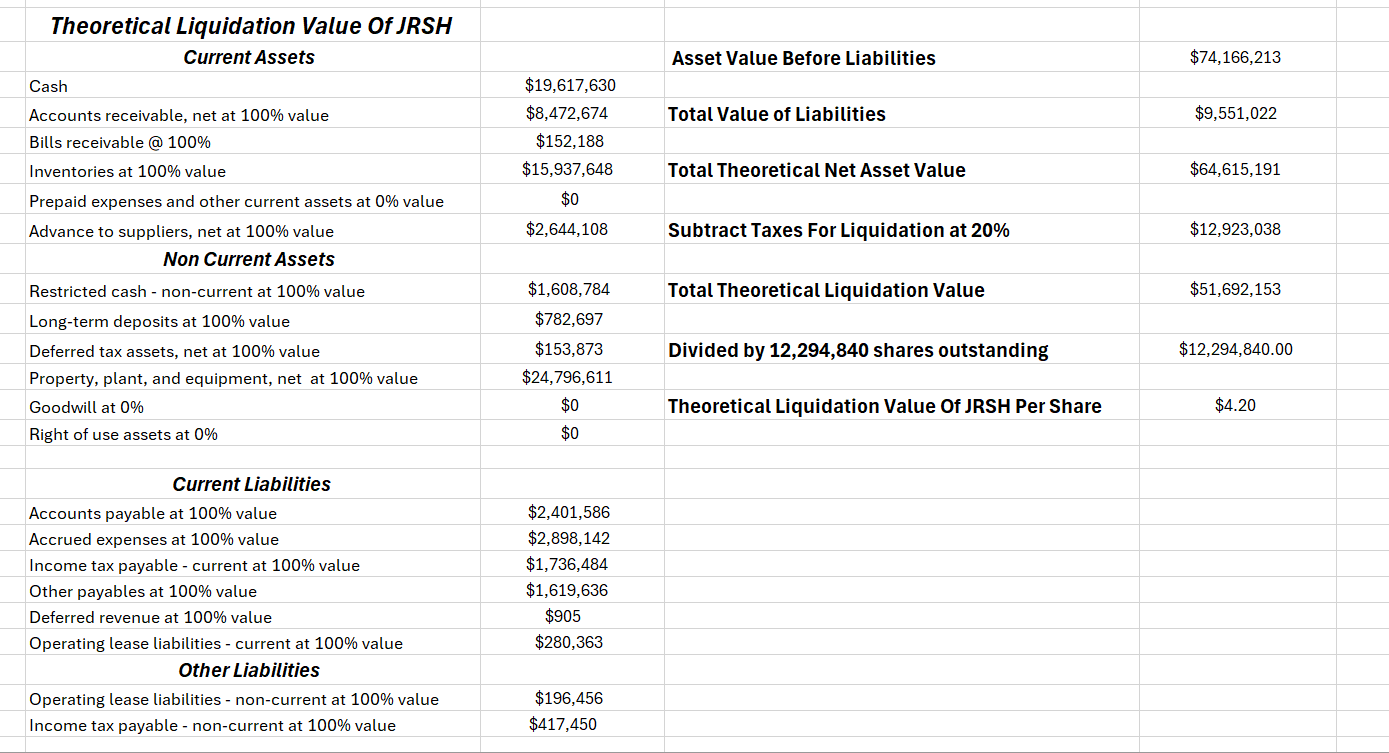

Part of the reason JRSH caught my eye initially was its impressive net asset valuation. I did a liquidation scenario and came up with $4.20 worth of asset value per share should they sell off their businesses. I added all of JRSH's assets up except for the company's prepaid expenses, goodwill, and right of use assets. I then subtracted all of JRSH's liabilities at full value. I then subtracted 20% to account for taxes associated with a theoretical liquidation sale. From here you end up with a $51.69 million liquidation value. Divide that by JRSH's 12.29 million shares outstanding and we get $4.20 of asset value per share a 37.7% upside from the current share price of $3.05.

Theoretical Liquidation Value Of JRSH (Leland Roach)

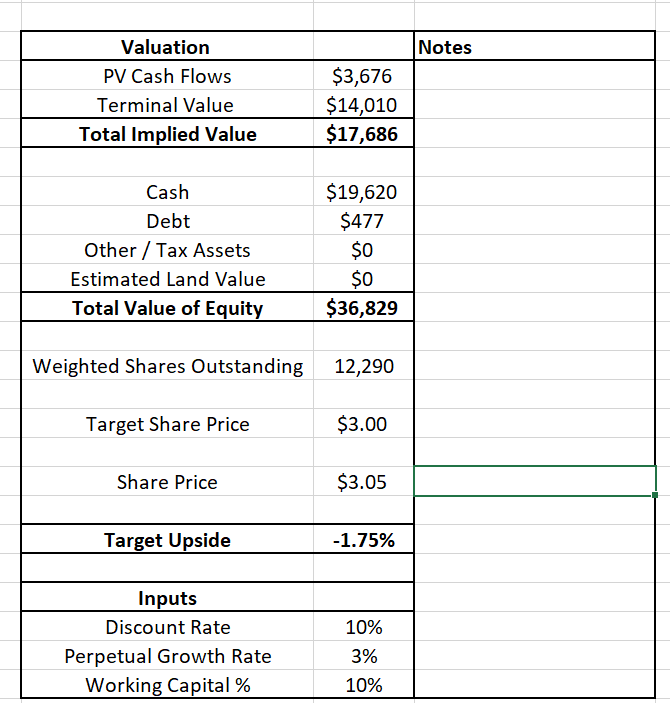

I have also ran JRSH through a discounted cash flow analysis in which case I had to make some rather large assumptions. Due to the uncertainty surrounding VFC's future decisions concerning its brands and by extension uncertainty surrounding JRSH's future revenue streams, I decreased JRSH's revenue streams for the company's fiscal 2025. I used JRSH's TTM average for their 2024 revenue figures at $119 million and then I gave them a further $10 million decrease in revenues to $109 million in 2025 as JRSH has been seeing a steady decline in revenue over the past 2 years. From this point on I assumed a 3% annual growth rate which is slightly higher than the expected average growth in apparel sales which, depending on the source, usually is estimated between 2.1%-2.8%.

I then applied a 5% EBIT margin to JRSH as that is their average annual EBIT margin over the past 5 years and then applied a 24% effective tax rate to that. I estimated capital expenditures at JRSH's five-year average except for their fiscal 2025 where they project they will spend $12.6 million in capital expenditures. I added back in JRSH's depreciation and amortization expenses at $3.4 million a year as that's been JRSH's D&A figures last year and their TTM figures this year. I also assumed a weighted average cost of capital of 10% for this DCF.

Discounted Cash Flow Analysis For JRSH (Leland Roach)

When all was said and done, I got a 1.75% decrease in price target to $3.00 a share. I do believe JRSH is fairly priced under normal circumstances.

Considering the margin of safety JRSH has in the value of its assets, and the fact that JRSH appears to be fairly valued when considering its projected discounted cash flows, I would normally consider a stock like this to at least be considered a hold. The considerations that force me to give JRSH a sell rating are overwhelmingly related to JRSH's dependence on VFC's uncertain future. Because JRSH's orders are not guaranteed via any contract VFC could give notice tomorrow it is terminating its relationship with JRSH. Out the door with VFC could potentially walk around 60% of JRSH's business. This could be devastating for a company currently undergoing so many construction projects to expand their production capacity.

JRSH's comeback story as well as its share price is in a bit of a lockstep with VFC's comeback story and share price. Provided VF Corporation continues to manufacture their clothing through JRSH it is likely that should VFC see a turn around in its business and stock price that JRSH would see a turn around in its business and stock price. I wouldn't consider buying stock from JRSH until VFC has made clearer which of its brands it intends to sell off or overhaul or whether or not it will maintain the production of its clothing at their current manufacturing facilities or if they will have to be moved elsewhere to improve VFC's margins.

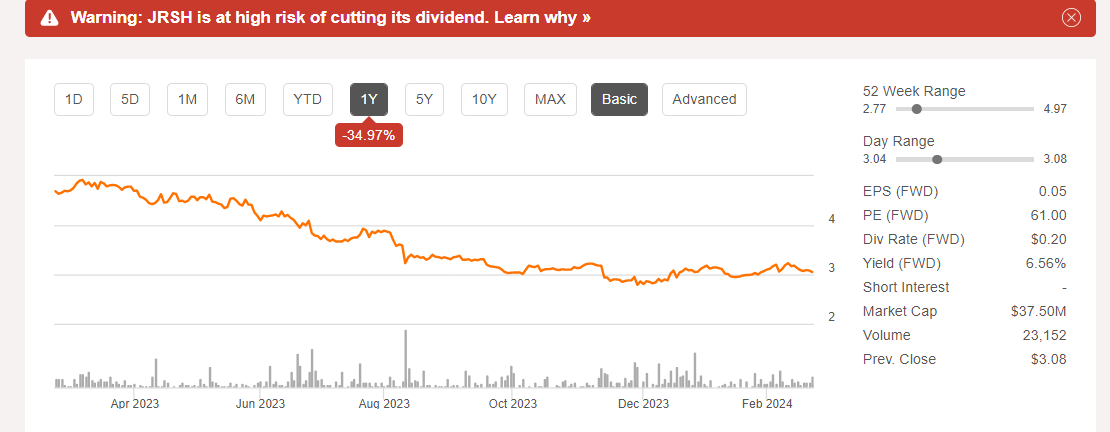

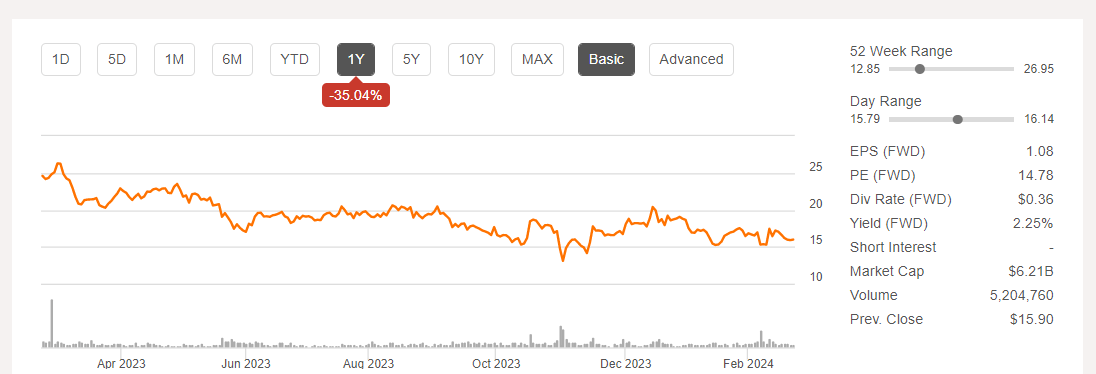

JRSH's One Year Stock Price (Seeking Alpha) VFC's One Year Stock Price (Seeking Alpha)

Once these questions are answered and it becomes clear that VFC will remain in business with JRSH, I would possibly consider a buy rating for JRSH. With that being said, if the reader is looking for an opportunity to buy into JRSH hoping for a business turnaround to be the catalyst to drive the stock price higher you may want to just consider buying VFC instead. Since so much of JRSH's future looks to be tied to VFC it might be a better idea to buy their stock when news of business improvements arise since VF Corporation has all of the leverage in this business relationship.

Despite selling for $3.05 a share significantly under my liquidation value of $4.20 and appearing to be fairly priced under a discounted cash flow which produced a price target of $3.00 a share, I am rating JRSH as a sell. I gave JRSH a sell rating, largely due to its dependence on VFC for the majority of its sales. With VFC's new CEO Mr. Bracken P. Darrell vowing all of VFC's brands would undergo a strategic review and that no VFC brand was a "sacred cow" it is uncertain currently whether or not VFC will continue its The North Face, Timberland, and Vans brands in their current states or if JRSH would even still be the ones to manufacture these products as VFC could attempt to improve their margins by moving manufacturing somewhere else. On top of this JRSH has seen its taxation within Jordan rapidly and suddenly increase over the past few years which could further inhibit JRSH's future business operations. All of these factors pooled together has led me to a clear sell rating for JRSH.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.