Michael Warren/E+ via Getty Images

Michael Warren/E+ via Getty Images

Johnson Outdoors (NASDAQ:JOUT) is a leading global manufacturer and marketer of outdoor recreational products. Johnson Outdoors operates through multiple brands, offering a diverse range of outdoor gear and equipment for various recreational activities such as fishing, camping, diving, and water sports.

JOUT

Whilst our rating of JOUT may not imply such, we consider the company a high-quality business. This is primarily due to it being a global market leader across a number of outdoor recreational verticals. The company has used product innovation and M&A to expand its total addressable market, building numerous brands and awareness among an educated and sticky customer base, allowing for solid growth and market share gains.

Whilst this is positive, the company is in the midst of a short-term financial squeeze. Inventory levels are far too high and demand is not allowing for an orderly unwind. Management will likely need to continue to discount, further pressuring margins and FCF. With inventory turnover at 1.5x, while its historical level was ~3.5x, this will take a number of quarters.

Acknowledging there are attractive qualities with JOUT, its peers are performing far better and appear less cyclically sensitive, implying greater long-term value. We do not currently see enough to rate JOUT a buy and instead rate it a Sell.

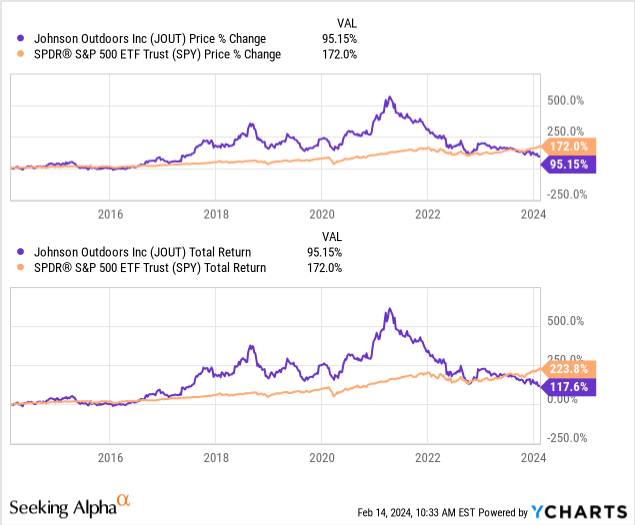

JOUT‘s share price performance has been volatile, with considerable gains during the post-pandemic period followed by a sharp draw-down as its financial results have declined.

Capital IQ

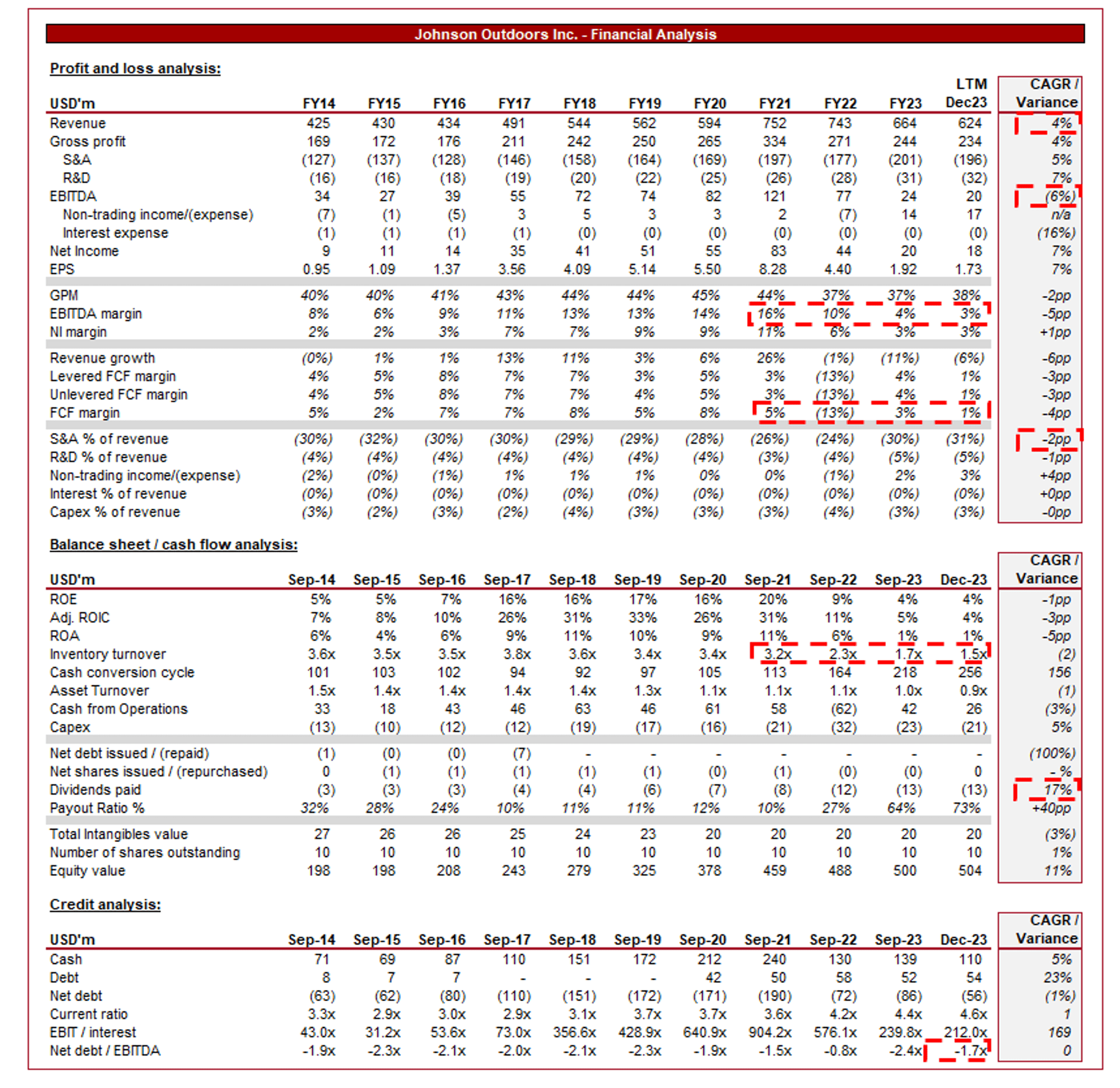

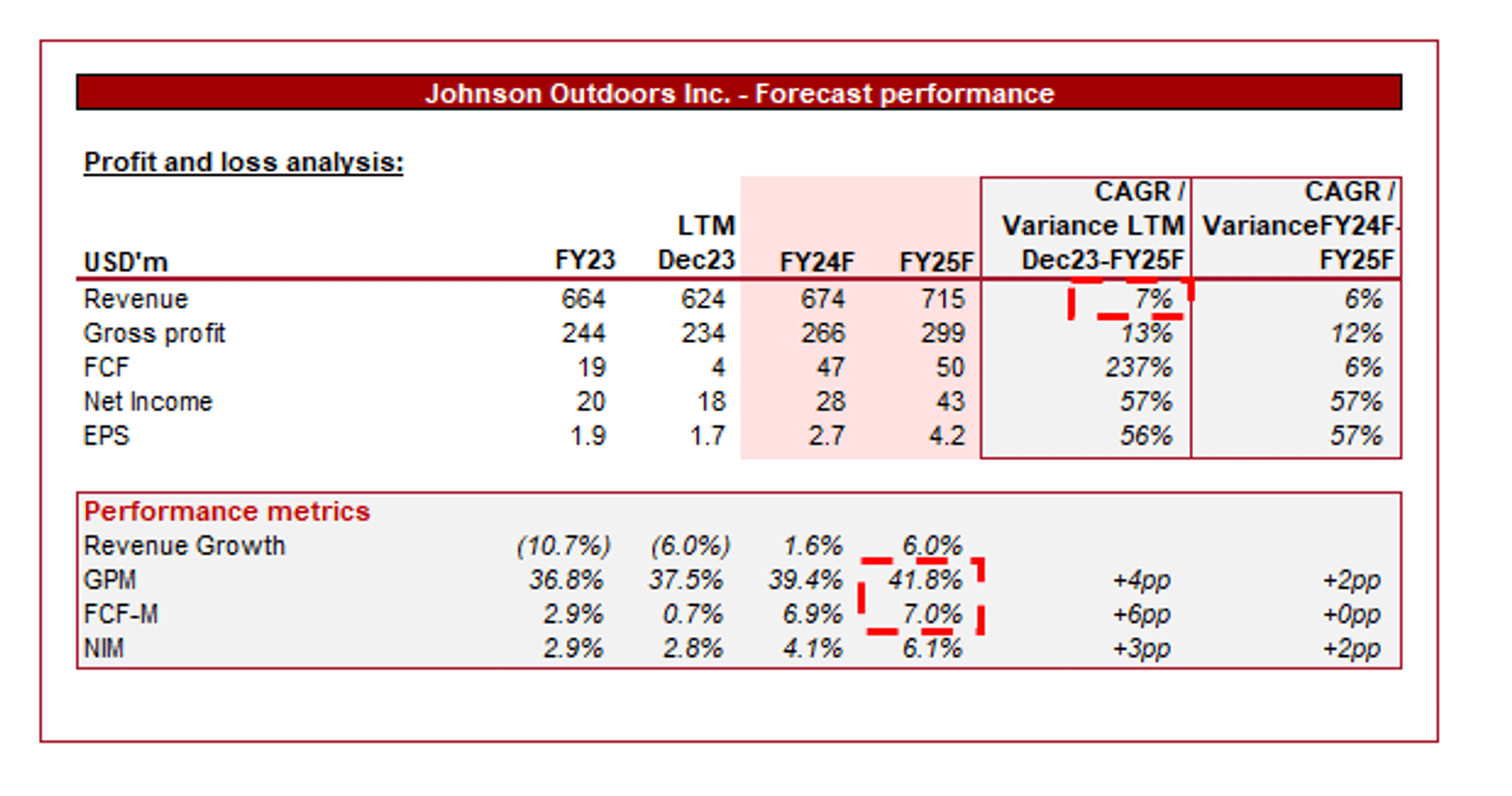

Presented above are JOUT's financial results.

JOUT’s revenue has grown at a CAGR of +4%, a rate that is depressed by its recent performance with its revenue still below its FY21 peak (+8% rate into FY21).

Business Model

JOUT

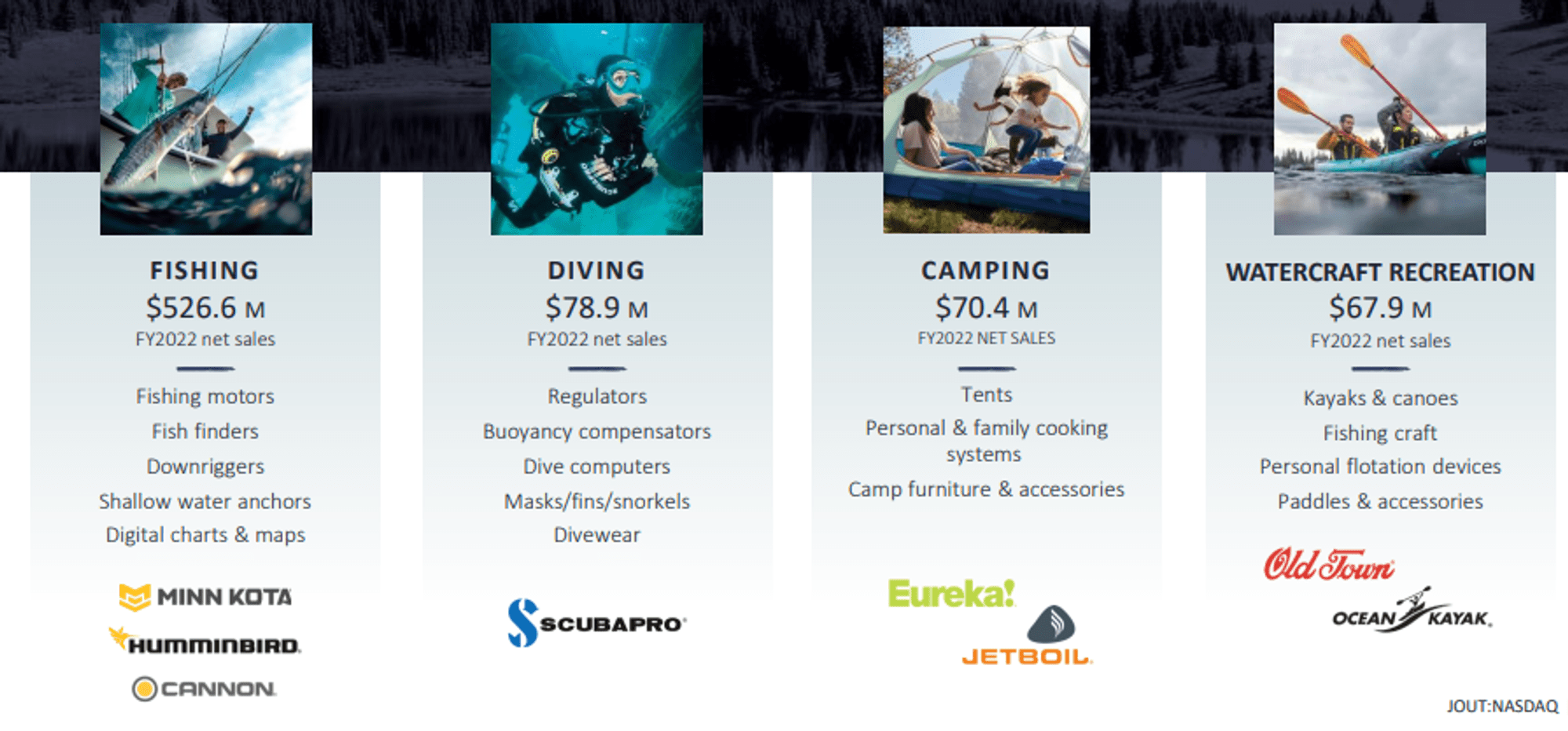

JOUT offers a wide range of outdoor recreational products across various categories, including fishing, diving, camping, and watercraft. This diverse portfolio caters to different outdoor enthusiasts and allows the company to capture market share in multiple segments. This is while it remains within its area of expertise, allowing for shared competencies and marketing.

JOUT owns several well-known and respected brands in the outdoor industry, including Minn Kota, Humminbird, Old Town, Ocean Kayak, and Eureka!. These brands have strong brand recognition and loyal customer bases (who are educated and passionate about outdoor sports), contributing to consistent sales growth and good market capture from new customers in their niche verticals.

JOUT utilizes a multi-channel distribution strategy, selling its products through a combination of direct-to-consumer channels, specialty retailers, mass merchants, and e-commerce platforms. This diversified distribution network ensures broad market coverage, which is important given the niche nature of its products, as well as de-risking the company regarding sales generation.

JOUT has a strong global presence, with distribution channels and sales operations in North America, Europe, Asia-Pacific, and other regions. This global footprint maximizes its revenue generation potential and further enhances its brand.

Recognizing the importance of environmental conservation, JOUT incorporates sustainable practices into its product development, manufacturing processes, and supply chain operations. By prioritizing environmental stewardship, the company aligns with the values of eco-conscious consumers and enhances its brand image.

Outdoor Recreation Industry

The industry is expected to grow well during the coming years, with a CAGR of +6% into 2028. This is likely to be driven by the growing demand for outdoor gear and equipment, especially among millennials and Gen Z consumers. This was partially accelerated by the pandemic, as well as the general interest in activities as the world is increasingly digitalized.

Competitive Positioning

We believe JOUT has a strong competitive presence within its industry, for a number of key factors.

JOUT is committed to producing high-quality, durable products that withstand the rigors of outdoor use. With this perception of long-lasting durability, the company has earned the trust of customers and cultivated a positive brand reputation. This underpins a portfolio of iconic brands which enjoy strong brand recognition and loyalty among outdoor enthusiasts.

The company is increasingly prioritizing innovation and invests heavily in R&D (+7% CAGR) to develop cutting-edge products that meet the evolving needs of outdoor enthusiasts. Features such as advanced fish-finding technology, lightweight materials, and ergonomic designs further differentiate JOUT's products in the market. Given the niche nature of the industry, its considerable scale compounds its competitive position.

JOUT’s diverse product portfolio spans multiple outdoor recreational categories, reducing dependence on any single product or market segment, while allowing for reinvestment of cash across segments.

Finally, collaborations with strategic partners, including retailers, distributors, and outdoor organizations, expand JOUT's reach and market presence. Its scale and brand value provide it with unrivaled exposure to consumers, compounding its scope to capture new customers.

Growth and margin progression

Whilst JOUT has a strong business model, marketing leading brands, and industry tailwinds driving the company forward, its growth rate of +4% appears underwhelming. We attribute this partially to the greater-than-expected demand post-pandemic, contributing to a subsequent slowdown as some have abandoned these hobbies and others have purchased high-quality goods that are yet to need replacing. This said, the growth rate to FY21 was +8%, which is what we would expect but inherently captures this bump.

For this reason, we do believe an improvement in execution is required to grow comfortably. Management is turning its focus to operational improvements to lift margins, likely a response to near-term issues. Whilst we concur with this, we believe more needs to be yielded from its investment in innovation. This, alongside marketing, is a core component of Management's strategy but the returns appear to be diminishing.

Current economic conditions represent headwinds for the company. With elevated rates and inflation, consumers are cutting back discretionary spending as living costs grow as a proportion of total income. Whilst spending has shown resilience, in part due to a sticky labor market and wage inflation, highly discretionary segments are still struggling.

Looking ahead, we see rates beginning to step down in mid-to-late 2024, followed by expansionary policy in full force in 2025. This will likely mean near-term pain is ahead.

Capital IQ

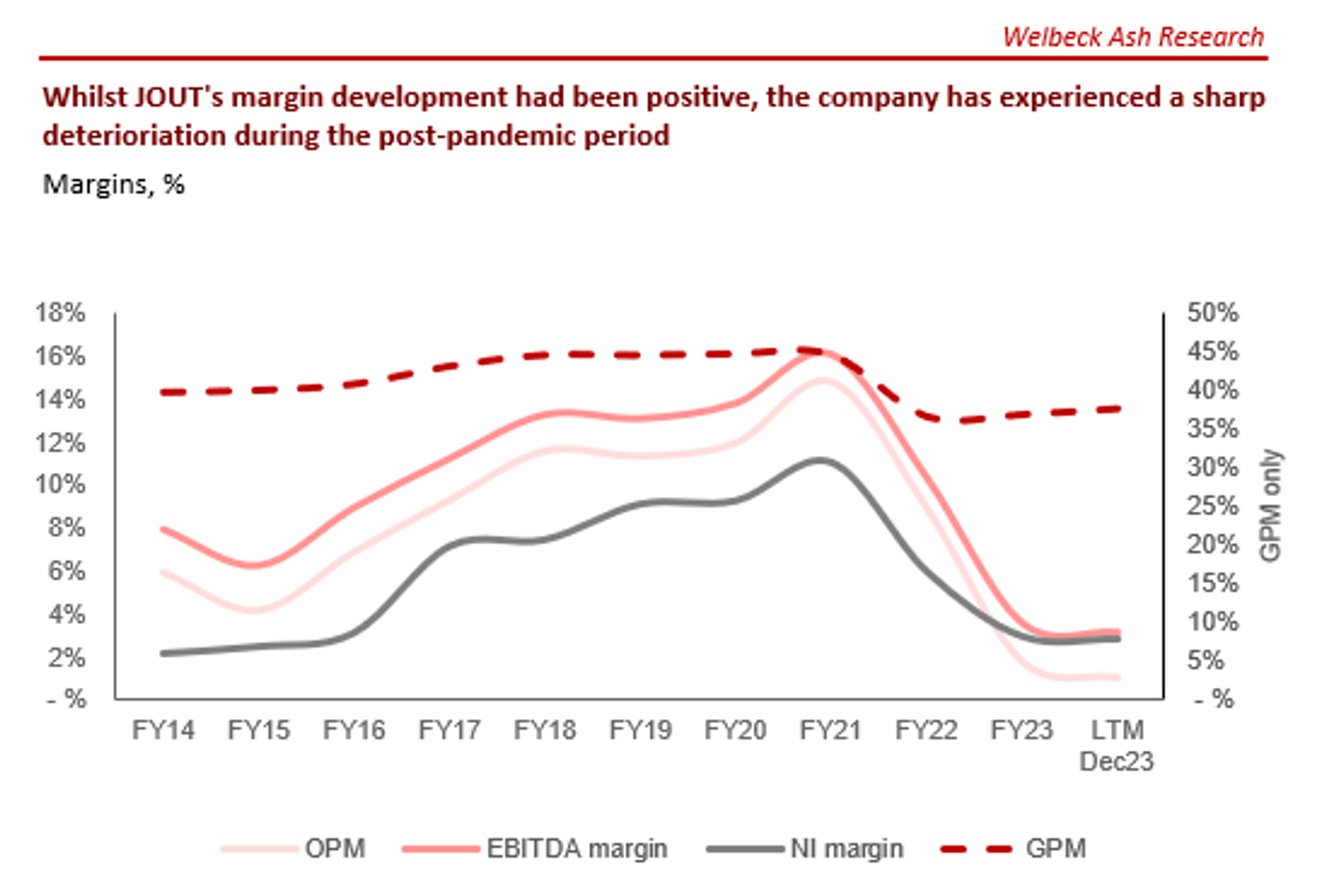

The run-up in JOUT’s share price was a reflection of its margin improvement, with the company peaking at an EBITDA-M of 16% before declining to its current 3% level. This decline is primarily on a GM% level, reflecting inflationary pressures and increased discounts to protect sales.

We do expect margin improvement but the visibility of this is low. In the next 5 years, we expect JOUT to push back toward an EBITDA-M of 10%, although it appears unlikely it can cross 12% during this period. JOUT has shown the ability to operate closer to ~15% historically but we feel a discount to this "normalized" level needs to be applied due to the progress lost in recent quarters, as customers will be hesitant to accept consistent price increases.

JOUT’s recent performance has been poor, with top-line growth of +6.6%, (8.2)%, (50.9)%, and (22.3)%, in part due to the sale of its Military and Commercial Tents product line. Further, its margins continue to fall and its inventory turnover has fallen to 1.5x.

The company is in a weak position. Management has likely been caught off-guard, contributing to a bloated level of inventory, an increased need to discount, and an inherently weak level of demand. We believe this will exaggerate the headwinds the company is currently facing, implying further downside ahead.

We believe the current near-term squeeze/deterioration will only cease once sufficient inventory is liquidated to realign with a normalized conversion cycle. At an inventory turnover of 1.5x and a breakeven FCF margin (~1%), we suspect it could be another quarter or two at a minimum.

Capital IQ

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting flat growth in FY24, followed by an improvement to +6% in FY25. Alongside this, margins are expected to incrementally improve.

We expect FY24 to be more difficult than analysts predict. The company has found itself trapped in a corner with the level of stock it holds and will not easily unwind. For this reason, the coming 2-4 quarters, will be dominated by GM% weakness and inventory sell-offs.

Opportunities

We see the following opportunities in the coming years:

Notable threats

We see the following threats to its trajectory:

Seeking Alpha

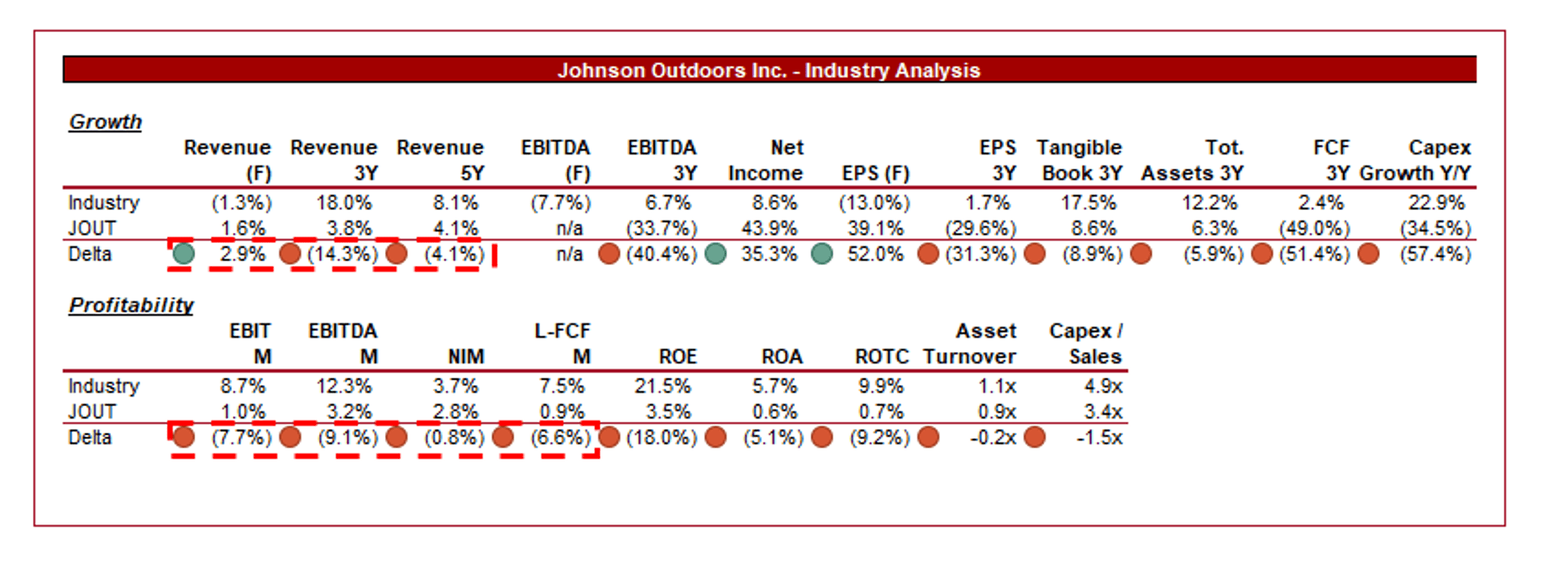

Presented above is a comparison of JOUT's growth and profitability to the average of its industry, as defined by Seeking Alpha (20 companies).

JOUT is currently underperforming its peers, with lower growth and margins relative to its peers. This is a reflection of its disappointing development in recent years, weighing the company down. Whilst the company exploited the post-pandemic bump in demand, sufficient focus was not given to brand building and growing its customer base, leaving JOUT susceptible to reduced interest. The inherent quality and nature of its products mean repeat purchases can be slow, which is why new customer wins is critical.

Whilst we are bullish on the company's brands and market position, it is likely JOUT has failed to maximize its capture of industry growth. Further, due to the niche nature of its target audience, JOUT will struggle further to capture strong growth, albeit this should have been compensated for through margins (which has been the case historically).

Even if it reverts to an EBITDA-M of ~10% and a growth rate of ~6% in line with its industry, JOUT would still be an underperformer. It appears its specific segment is inherently weaker than other leisure segments.

Capital IQ

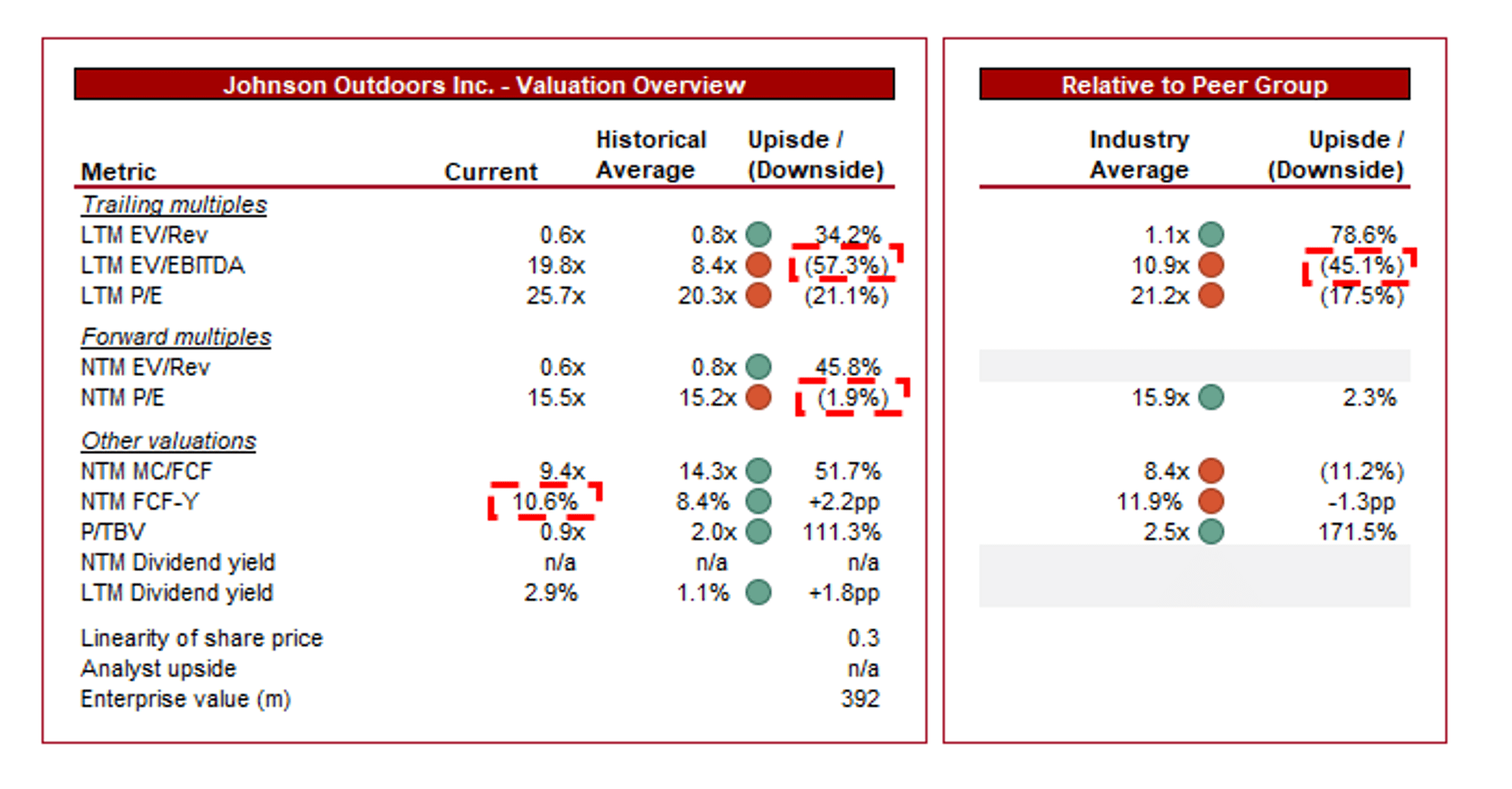

JOUT is currently trading at 20x LTM EBITDA and 16x NTM P/E. This is a premium to its historical average.

A premium to its historical average is justified, unusually, as we can be relatively confident that some margin improvement will occur. Once this occurs, the premium will evaporate. To illustrate this, on an NTM basis, its FCF yield is at a premium of 2.2ppts.

This said, the company is only at a small discount to its peers on a NTM basis (2.2%), which implies further margin improvement must be delivered in order to justify its financial weakness.

Overall, we believe JOUT is likely overvalued. It is priced for recovery, which creates execution risk, while not wholly reflecting the near-term headwinds that will make said execution difficult. We believe the current downside is ~10-15%, as this would imply a sufficient discount to its peers on an NTM basis to account for its financial weakness.

JOUT is fundamentally an attractive business, operating strong brands in a niche industry, underpinned by a solid business model. The company has experienced strong brand development among an educated customer base, allowing for stocky demand and a strong reputation.

This said, the company is facing considerable headwinds as demand continues to soften, and its short-term execution has left the business in a pinch, with the risk FCF will turn negative in 2024.

We believe there is material uncertainty as JOUT’s new normalized level of performance, which will likely be below its peers, while 2024 will be a difficult period as rates remain elevated. For these reasons, despite seeing potential with the company, we rate it a sell on trajectory.