sakchai vongsasiripat/Moment via Getty Images

sakchai vongsasiripat/Moment via Getty Images

Jumia's (NYSE:JMIA) business has undergone a dramatic transformation over the past year, following a change in management and a shift in strategic focus. The company is prioritizing profits over growth and this continues to pay dividends, even in a challenging macro environment. I have previously written about this change could make the business viable long-term but have been skeptical about whether the company can reach breakeven just by cutting costs. Jumia's competitive positioning is also questionable given the company's small user base and asset light approach to logistics. Given the risks involved, I believe Jumia is currently fairly valued, but the range of possible outcomes is highly dispersed.

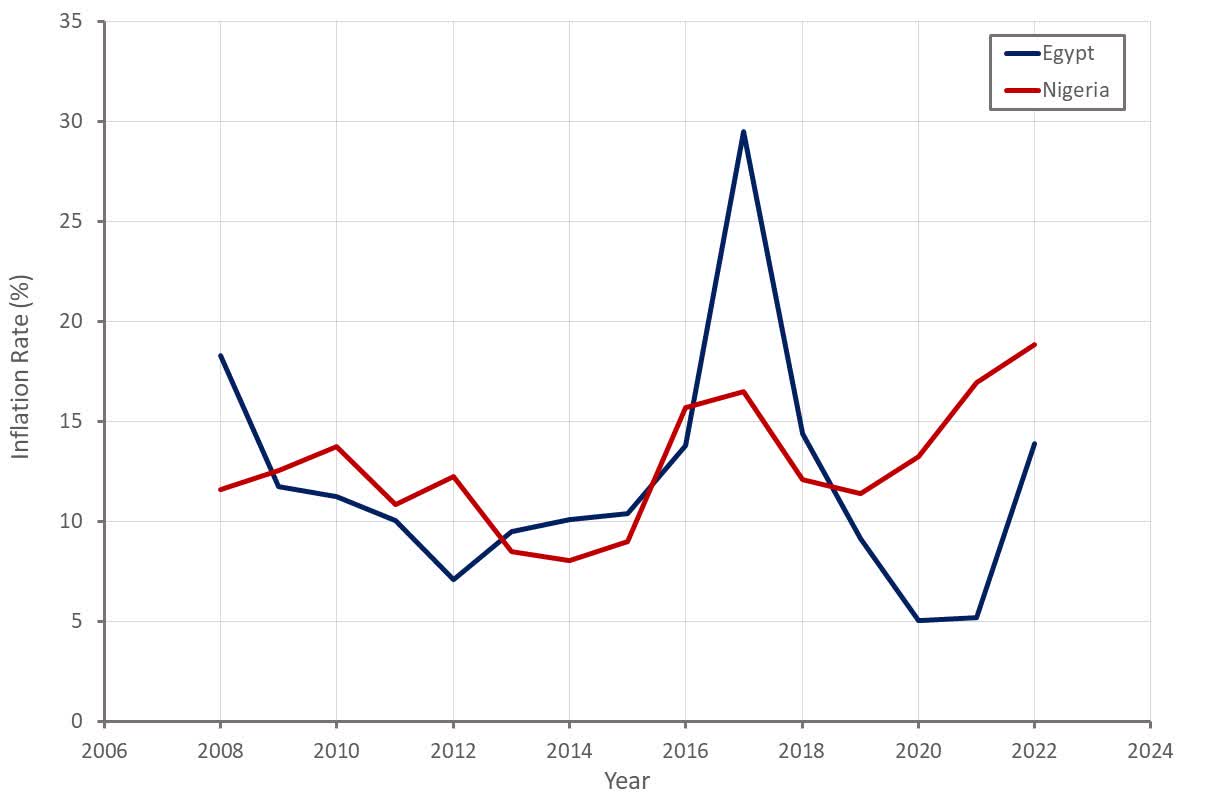

A number of Jumia’s core markets are suffering from high inflation rates, currency depreciation and scarcity of supply. This is pressuring consumer spending and has negatively impacted Jumia’s reported revenue in recent quarters. For example, Nigeria’s currency is down against the USD by around 75% over the past 5 years and Egypt’s currency is down close to 50% over the same time frame. Much of these moves have come over the past 2 years.

Nigeria and Egypt are focus markets in 2024. Jumia has made management changes and is reorganizing its supply chain operations in both countries, with the goal of reaching more consumers and increasing efficiency.

Jumia believes that the macro situation is beginning to stabilize in several of its markets, though, in some cases, supported by government policy. The IMF is forecasting sub-Saharan Africa's GDP growth to accelerate from 3.3% in 2023 to 3.8% in 2024. This should make it easier for Jumia to source goods and support customer purchasing power. In particular, lower inflation and more stable exchange rates would likely be highly supportive of Jumia's business.

Figure 1: CPI Inflation in Key Jumia Markets (source: Created by author using data from the World Bank)

Jumia has dramatically reshaped its business in recent quarters in pursuit of profitability. This includes:

Jumia recently discontinued its food delivery operations, stating that the segment's growth prospects did not justify the complexity it created. Fulfillment is a difficult activity, particularly in Africa, and food delivery was clearly not economic.

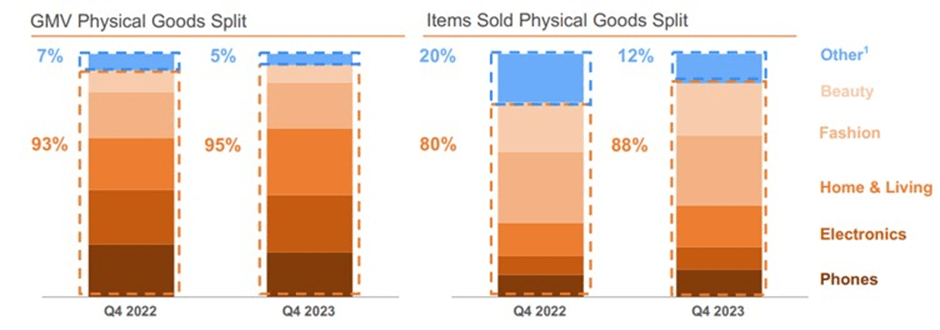

Jumia has also prioritized phones, electronics, home and living and fashion and beauty. The fashion and beauty categories now account for over half of Jumia's items sold. These are generally higher value items, which should lead to larger average order values and reduced fulfillment expenses. The categories were selected based on expected profitability, with a particular focus on logistics. Unsurprisingly, this also led Jumia to deprioritize categories like groceries where value per unit weight is generally low and there are additional considerations, like perishability.

Jumia is also trying to drive growth without relying on a large marketing budget and incentives (vouchers, free shipping, etc.). Part of this involves tapping latent demand by improving the company’s value proposition (stable prices and consistent supply). Jumia is trying to improve supply, with a focus on enabling supply from China via Jumia Global. The company is also making greater use of customer relationship management, search engine optimization, and direct traffic to lower the burden of marketing.

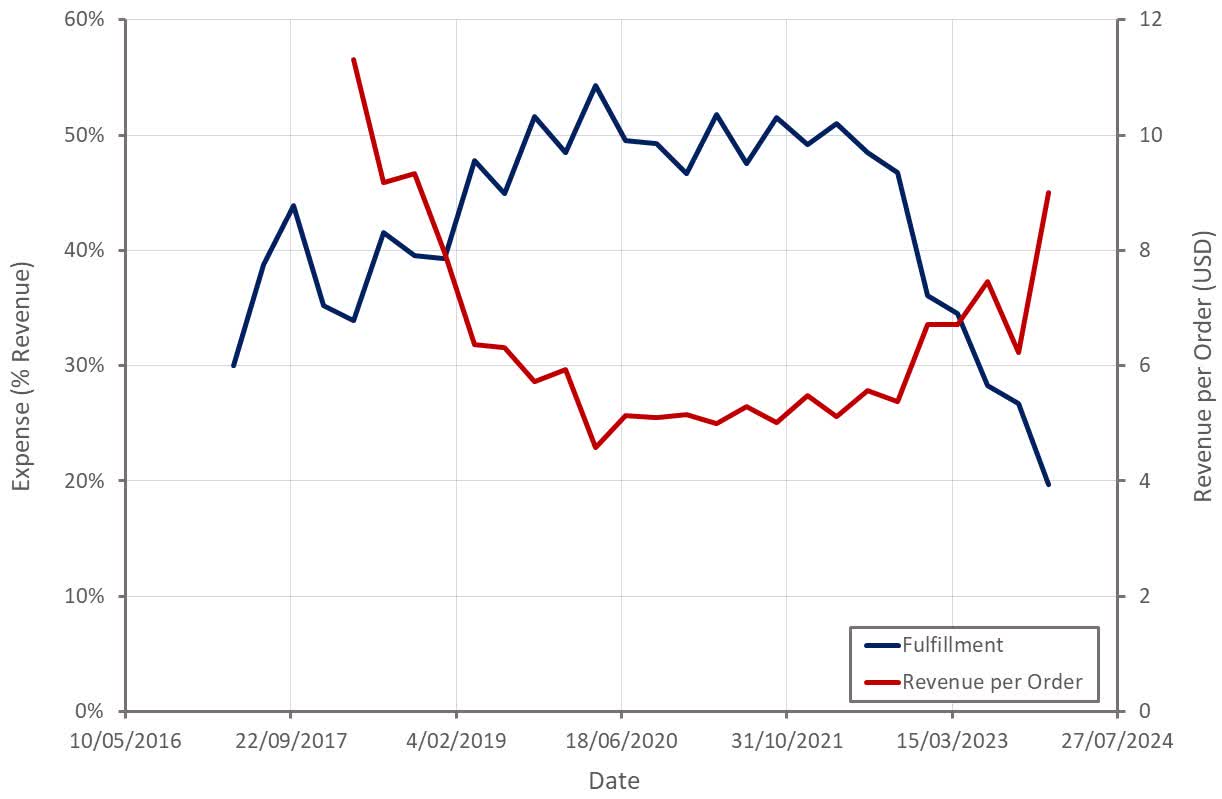

Logistics is also a focus area for Jumia, with greater efficiency being driven by the use of pickup stations. The share of shipped packages utilizing pick-up stations increased from 37% in Q4 2022 to 48% in Q4 2023, helping to reduce Jumia’s fulfillment expense per order. Jumia continues to expand its pickup station network with the goal of penetrating undertapped areas in a cost-effective manner. The company has also increased warehouse staff productivity and reduced packaging costs, amongst other initiatives.

JumiaPay could also be a value lever in the future, although I am generally fairly pessimistic towards payments over the long run. JumiaPay is currently being utilized as an enabler of the ecommerce business. Jumia is working to integrate more relevant payment methods and is trying to improve the customer experience by reducing the number of steps to validate a payment, reducing processing time and increasing success rates. Jumia is also rolling out JumiaPay on delivery, which enables customers to pay digitally upon delivery of their order. This feature has been successfully implemented in Kenya and is now being introduced to Nigeria. In addition, Jumia is developing a Buy Now Pay Later solution in partnership with third-party credit providers. Jumia hopes that financing options will drive growth in high value items, like phones and large appliances.

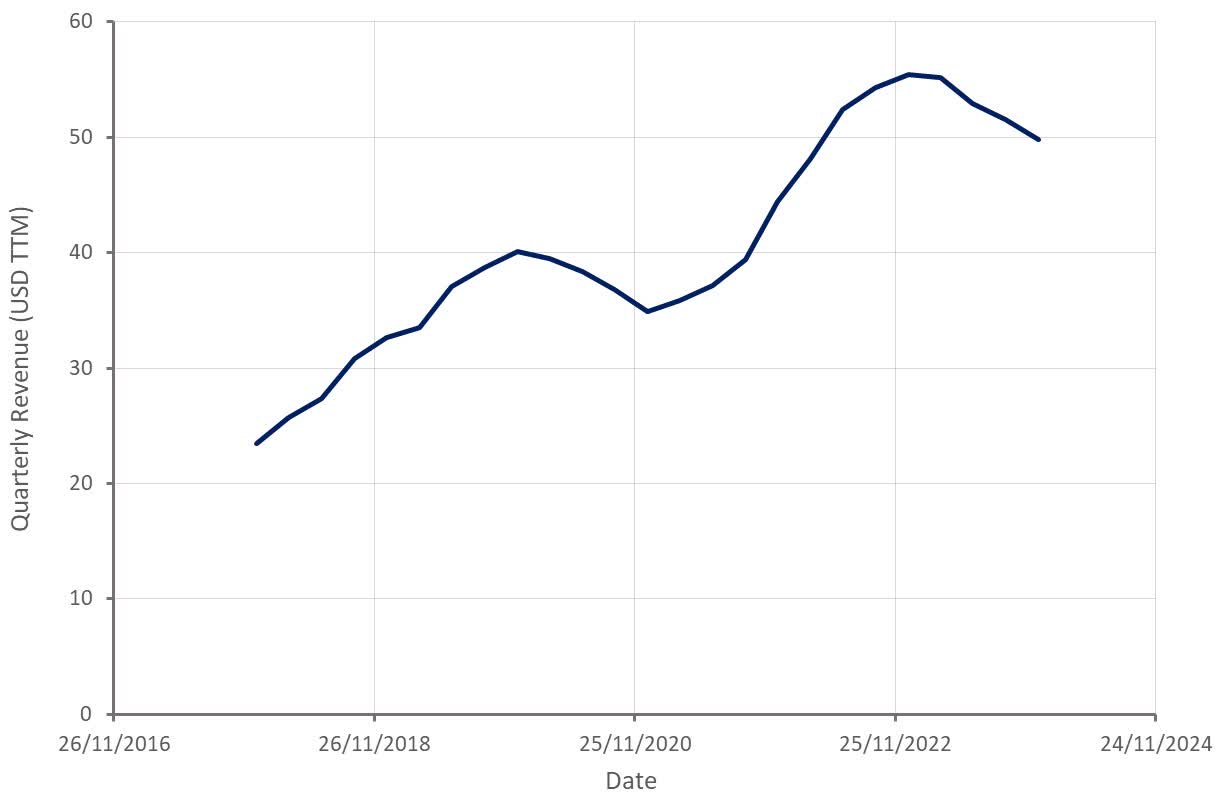

Jumia's revenue was approximately 59 million USD in the fourth quarter, down 2% YoY, but up 28% in constant currency. While growth has been anemic for a while, this is understandable given that reduced incentives and marketing spend has impacted active consumer numbers and orders.

Growth is being supported by the fact that Jumia’s revenue is rising faster than GMV, with revenue now roughly equal to a quarter of GMV. This can only be taken so far though before it begins to impact activity on the platform.

Jumia hasn’t given guidance for 2024 but expects an increase in both orders and GMV, excluding any potential foreign exchange impact. Assuming foreign exchange rates are more stable, Jumia should achieve healthy growth considering revenue has been outpacing GMV and revenue per order has been rising.

Figure 2: Jumia Revenue (source: Created by author using data from Jumia)

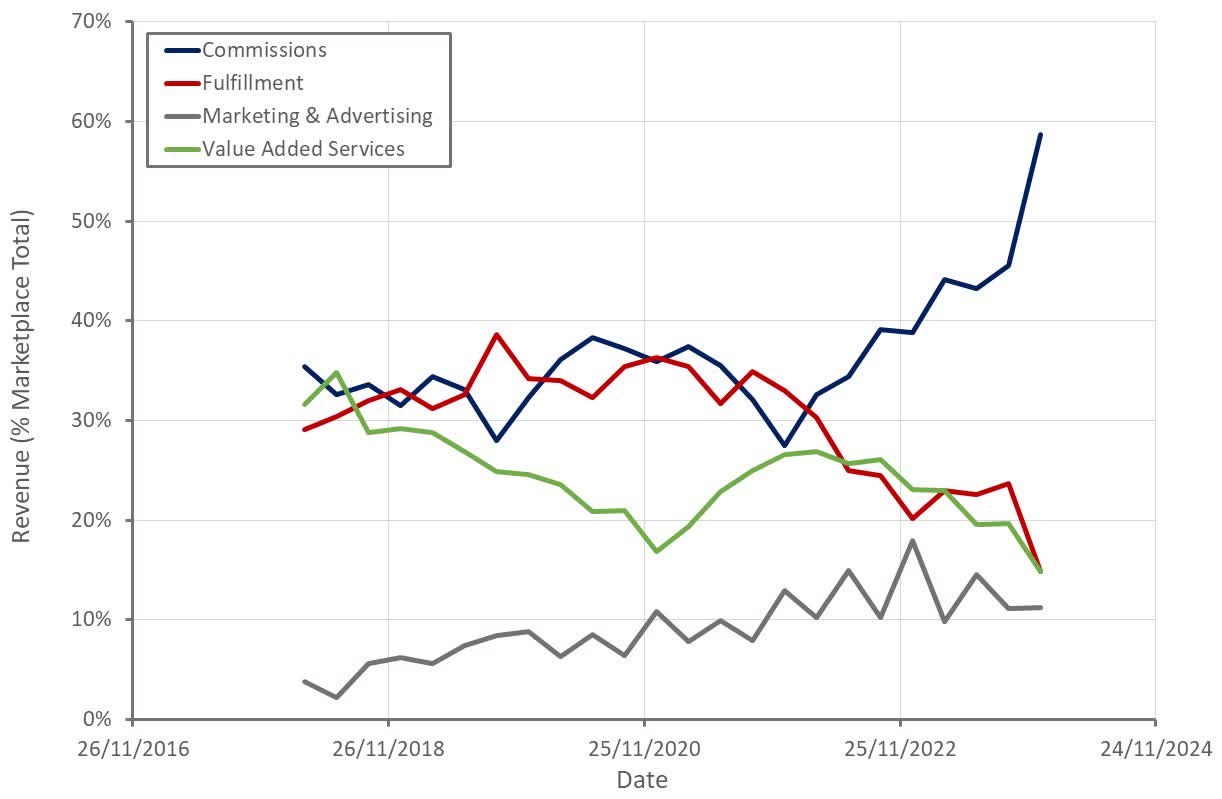

Marketplace revenue was down 10% YoY in the fourth quarter and up 22% on a constant currency basis. This is in large part the result of Jumia's move away from uneconomic activities (fulfillment and value-added services). Marketplace commissions and first party sales have been robust, with first party revenue driven by sales to retailers, distributors, and other corporate buyers.

Figure 3: Jumia Marketplace Revenue (source: Created by author using data from Jumia)

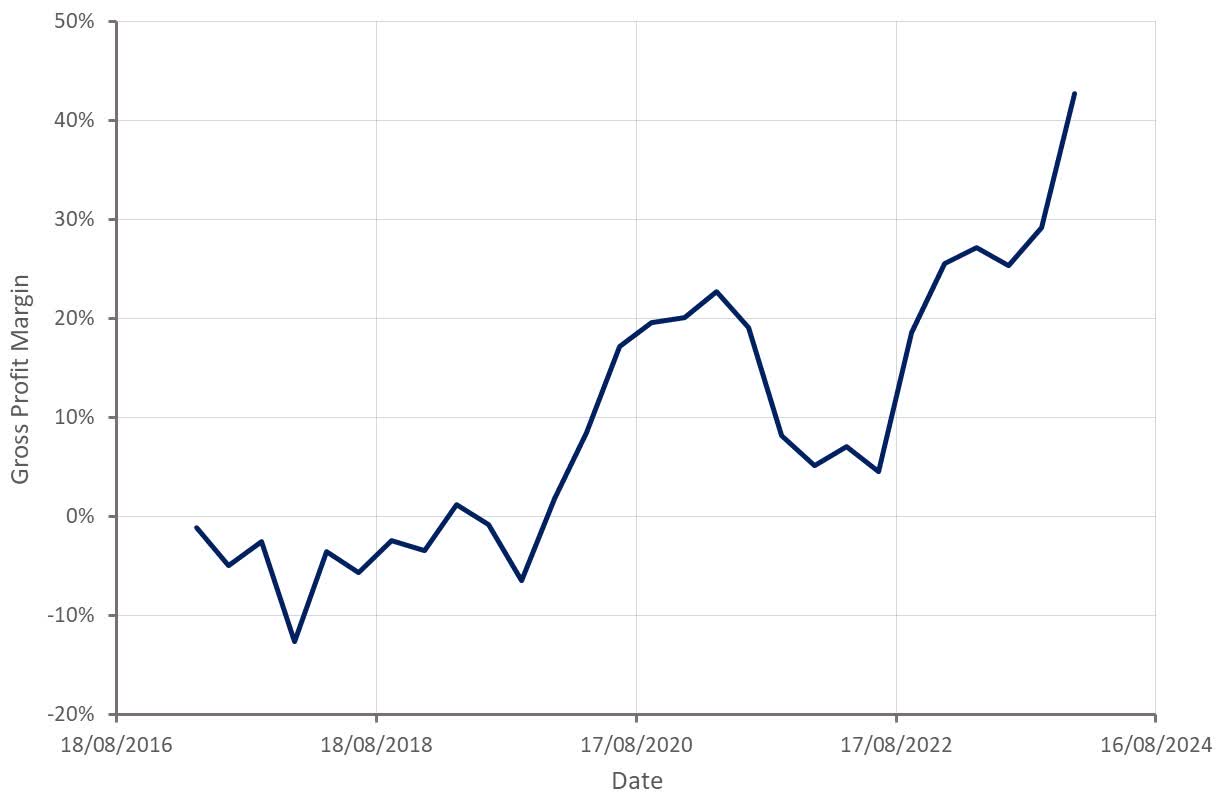

I consider fulfillment expenses part of Jumia's COGS, and by this methodology the company's gross profit margin continues to rapidly improve as the company focuses on activities with profitable unit economics. Jumia now has a genuine shot at profitability, dependent on its ability to cost effectively attract and retain customers and reach sufficient scale.

Figure 4: Jumia Gross Profit Margin (source: Created by author using data from Jumia)

Average order value continues to trend higher on the back of Jumia’s focus on higher value categories (phones, electronics, home & living, fashion & beauty), helping to reduce the burden of fulfillment expenses. Free shipping was also creating a lot of low value orders, and this has largely been eliminated.

Figure 5: Jumia GMV by Category (source: Jumia) Figure 6: Jumia Fulfillment Expense (source: Created by author using data from Jumia)

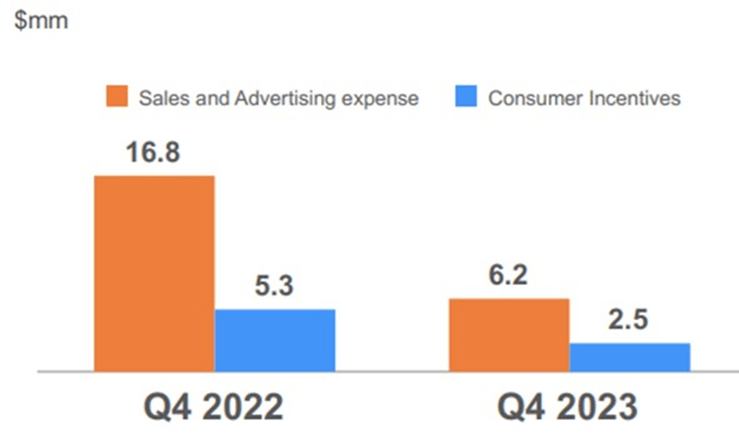

Jumia has also managed to reduce the burden of operating expenses with a range of initiatives. For example, product development has largely been relocated to Africa, reducing Technology and Content costs. Jumia has also cut back on marketing and is leveraging CRM and SEO to try and reduce costs further. In addition, Jumia has significantly pulled back on incentives, with 43% of orders benefitting from consumer incentives in Q4 2022, compared to only 28% in Q4 2023.

Figure 7: Jumia Advertising and Consumer Incentive Costs (source: Jumia)

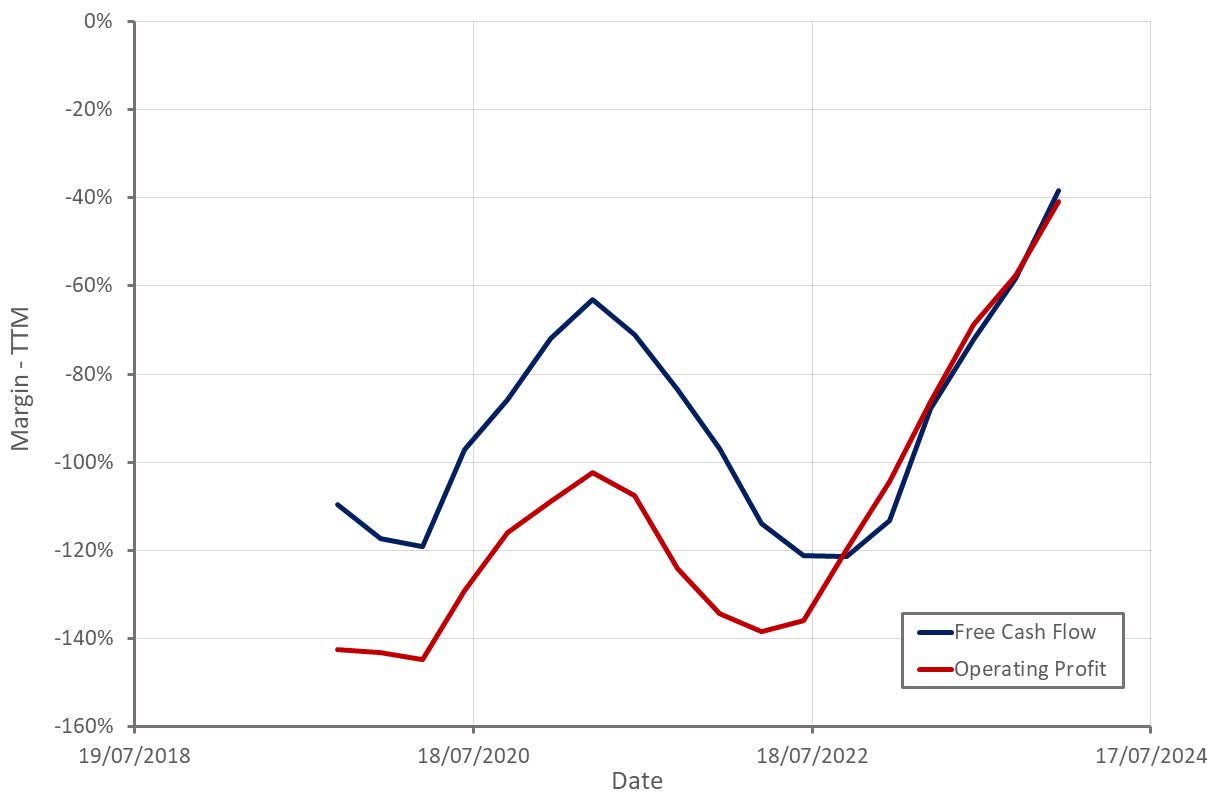

Jumia still isn't profitable on a GAAP basis or producing positive free cash flows. If the current rate of improvement were to be maintained, Jumia could be within a few quarters of profitability, though. Regardless, cash burn has been reduced to a point that liquidity is no longer a near-term concern, though.

Figure 8: Jumia Operating Profit Margin (source: Created by author using data from Jumia)

While Jumia has achieved a dramatic turnaround in recent months, this already appears to be priced into the stock. I believe Jumia is probably now around fairly valued, but there is a large amount of uncertainty involved. If growth begins to rebound, breakeven is achieved and Jumia begins to build a sustainable competitive advantage through a larger user base and logistics footprint, the company could be worth much more. If growth remains modest and margin improvements begin to stall, Jumia's stock could begin to look expensive. For now, I remain skeptical about the company's competitive advantage and ability to drive profitable growth long term, recent results have been surprising, though.

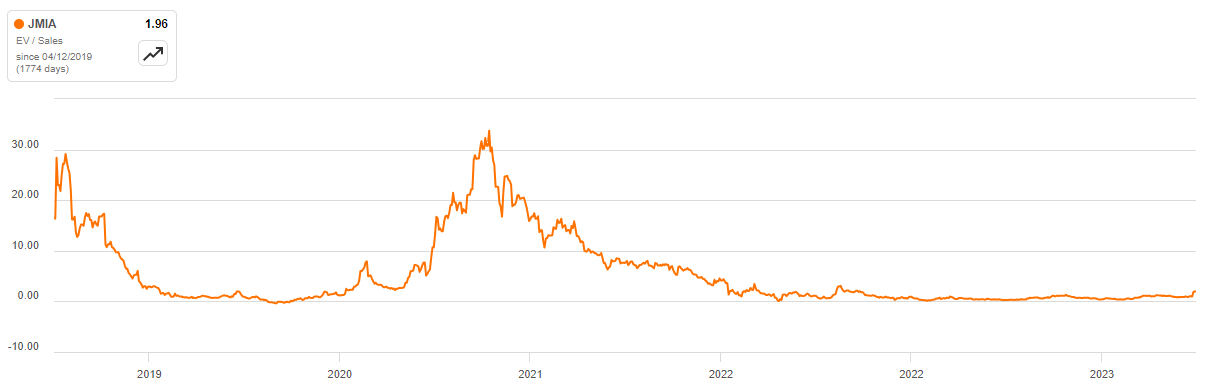

Figure 9: Jumia EV/S Multiple (source: Seeking Alpha)