The Washington Post/The Washington Post via Getty Images

The Washington Post/The Washington Post via Getty Images

J&J Snack and Foods (NASDAQ:JJSF) operates in snacks and beverages, a mature industry that exhibits limited growth potential, mainly driven by price increases related to inflation. Nevertheless, the company can expand its business in the future and achieve a higher growth rate than the industry by leveraging its innovative capabilities and pursuing mergers and acquisitions, capitalizing on its strong balance sheet. As usually happens when there is potential for future growth the market capitalization is too rich and I would prefer to see a major decrease in stock price before considering buying shares.

I will quickly make a stock price and business overview, then I will discuss the company's financial data focusing on the Q1 2024 earnings, look at possible growth catalysts, and finally conclude with a valuation.

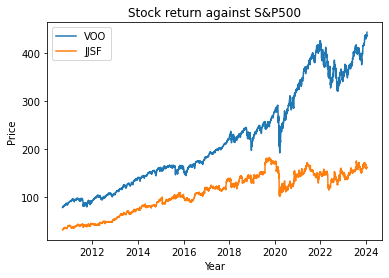

JJSF had a good performance between 1996 and 2020. However, after the COVID-19 pandemic, the stock price has mostly remained stagnant, whereas the S&P 500 had a return of approximately 110%.

Stock return against S&P500 (Image created by the author through Python library yfinance)

When a stock lags behind the main indexes, there are usually two different explanations: either the company has major problems that are affecting its performance or the stock market is missing out on a valuable buy opportunity.

J&J Snack Foods manufactures and sells snack foods and distributes frozen beverages primarily to food service and retail supermarket customers. It mainly operates in the US, Canada, and Mexico. The main products produced and distributed by the company are:

These iconic brands are sold across multiple locations: malls, fast-foods, restaurants, stadiums, theme parks, movie theaters, and supermarkets.

Even though the company operates in the food sector, an industry that I usually perceive as non-cyclical, the sale of snacks is discretionary and can easily be avoided by a person or an entire household. For example, a family might still want to go to the cinema during a crisis but may be opting to forgo snacks. The company itself in its latest 10-K considers as a risk the worsening of the whole economy. For all these reasons I classify J&J snack foods as a cyclical corporation.

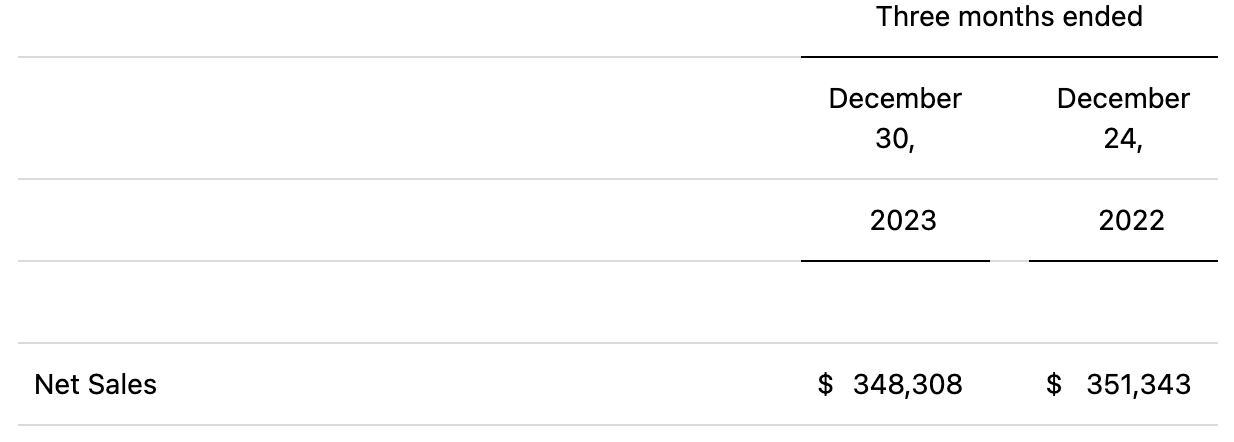

After three consecutive years of double-digit top-line growth, the company is currently facing a slowdown in sales. Overall sales decreased by approximately 1% on a year-over-year basis primarily due to a decline in consumer consumption in food service segment. The company is continuing to have good results in frozen beverages which grew around 8.5%.

Net sales result (Company's Q1 2024 press release)

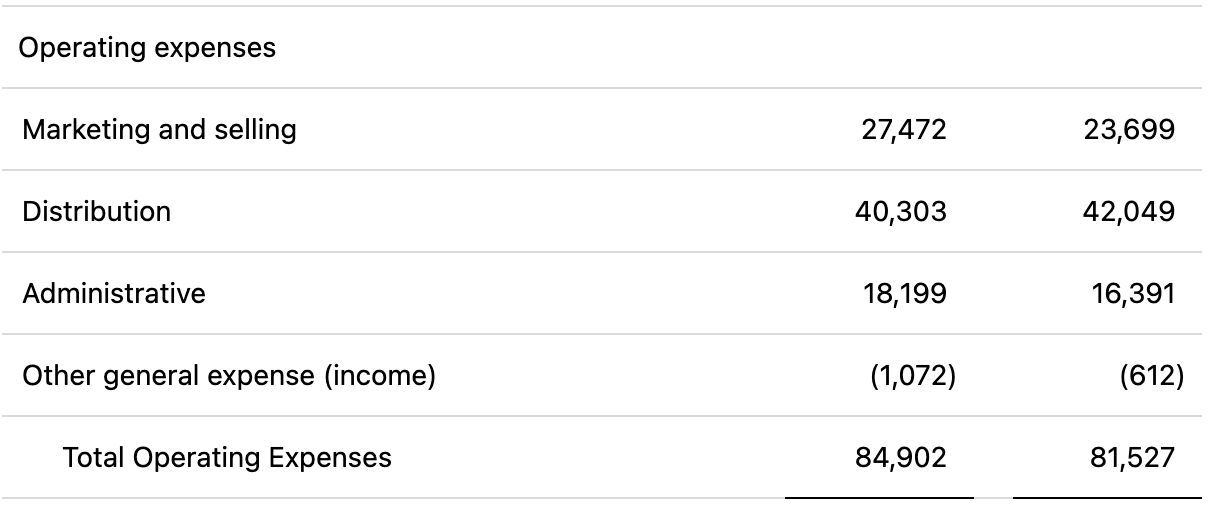

The most concerning aspect is that the decrease in revenue does not align with a substantial increase in marketing expenditures. I am not against marketing expenses, I believe that they create momentum and enhance brand awareness. However, I would expect to see a positive relationship between marketing expenses and revenue growth, and the current lack of alignment raises some questions.

Operating expenses in Q1 2024 (Company's Q1 2024 press release)

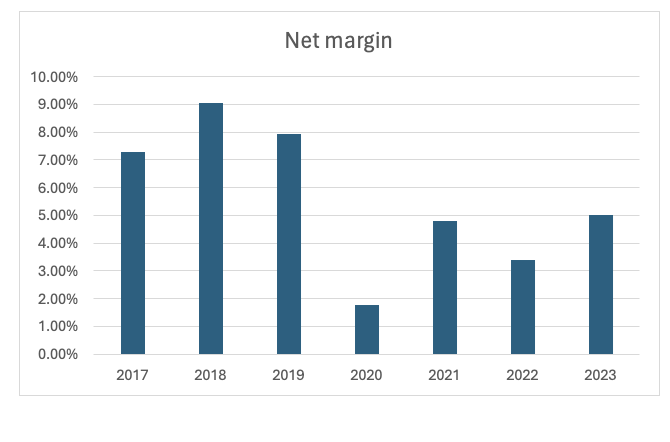

Despite the softness in revenue results, the company was able to enhance its profitability margins. Margins were one of my primary focus for this earnings call given the company's generally low margins, I would have liked to see an upward trend. These results reflect the positive impact of the company's strategy to grow higher-margin core products, along with continued improvements in overall productivity.

The company reported an increase of 20.6% in adjusted operating income, a 19.4% increase in adjusted EBITDA, and a 9.78% increase in GAAP net income. I am confident that the management team, through active strategies and an easing of inflationary pressure, will be able to continue growing the bottom line and restoring net margins at 2018-2019 levels in the coming years.

Net margin evolution (Image created by the author using Python library yfinance)

The US snack foods market is valued at around $114 billion. The industry is expected to grow at a CAGR of around 3.79% into 2029 mainly driven by an increase in products' price and a small rise in sales volumes.

Fortunately, J&J Snack and Foods has plenty of possibilities to grow at a higher pace than the average market. The company is currently working on channel expansion by securing deals with new retailers or enhancing existing partnerships. For example, in the last quarter, Super Pretzel gained availability at Wallgreens. The company can capitalize on the movie theater momentum leveraging its ICEE brand.

Moreover, there is growth potential through product innovation. For example, during the Q4 2023 earnings call the CEO highlighted the introduction of two new flavors for ICEE products: cherry and blue raspberry. I like the management team's focus on innovation, the company constantly introduces new flavors or product alternatives to align with consumers' tastes.

The company boasts a robust balance sheet with a total debt-to-free cash flow of 2.68 and a debt-to-equity equal to just 0.13. In my view, the company is well-positioned for future possible acquisitions. During the Q4 2023 earnings call, the CEO expressed optimism about future M&A operations:

Transitioning to M&A. We continue to be highly disciplined in our approach. We are evaluating opportunities that complement our brand portfolio and business model and that offer attractive shareholder returns. Financially, we have the resources and the balance sheet to invest in growth when opportunities align.

Considering all these opportunities, I believe that it is likely to see the company continue growing its sales on a double-digit base while also increasing profitability in the next years.

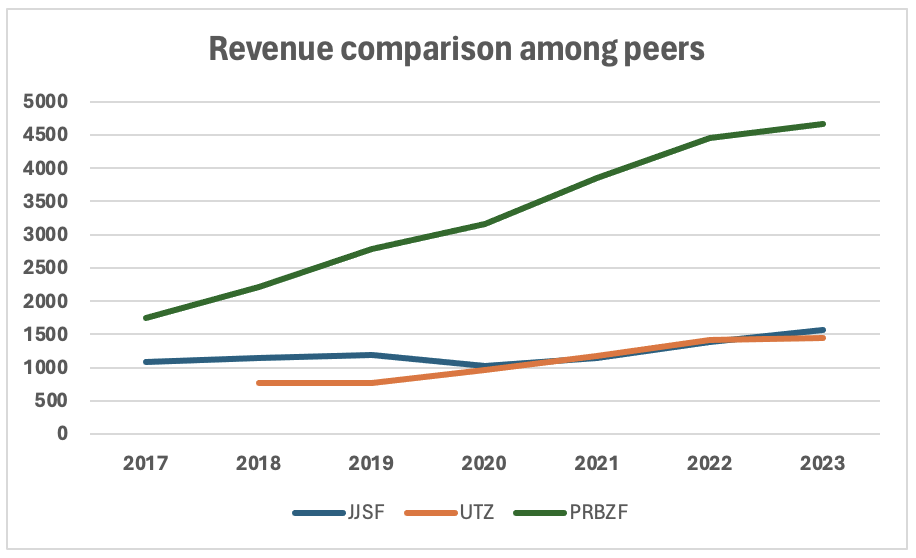

Upon analyzing the financial data and past performance alongside two main competitors, Utz Brand (UTZ) and Premium Brands Holdings Corporation (OTCPK:PRBZF), it is evident how revenue growth in recent years has underperformed compared to the company's peers. Since 2017 revenue grew at a compound annual growth rate of 5.32% whereas the other two competitors have achieved growth rates exceeding 10%. However, considering the analysis done in the previous passage about possible future expansion, I am confident that the management team can reverse this trend and start growing more than its peers.

Revenue trend and peers comparison (Image created by the author through Python library yfinance)

The snacking industry is dynamic and very competitive and it's becoming increasingly difficult to stand out and gain a significant market share. While I believe that a little competition can be beneficial for a company, in this case, the fierce landscape requires significant investments in capital expenditure, R&D, and marketing to attract new customers and retain existing ones, lowering the company's margins. Moreover, the industry is full of giant companies such as PepsiCo (PEP), The Coca-Cola Company (KO), or even Nestlé (OTCPK:NSRGY) that can easily surpass tiny companies like J&J Snack and Foods.

The company's operation and financial results are also affected by seasonality, particularly with iced brands like ICEE that have higher demand during summer. Because of seasonal fluctuations, there can be no assurance that the results of any particular quarter will be indicative of results for the full year or future years.

Since the company has a stable free cash flow and is also committed to dividend payments, I decided to evaluate it through both the dividend discount model and the discounted cash flow model and compare the results.

Let's begin with the dividend discount model.

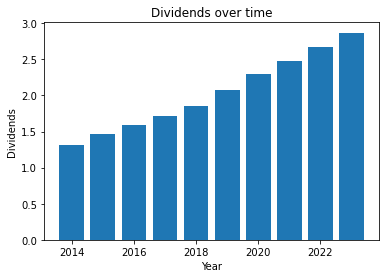

The company is committed to dividend increases to reward shareholders and I expect this trend to continue also in the future. Considering the general performance of the company and the FCF payout ratio at 69%, the dividend is sustainable. At the moment in which I am writing the article, the current yield is at 1.8%, I expect the company to slowly align with the industry average yield of 3%.

Dividends over time (Image created by the author through Python library yfinance)

On the right side of the sheet are reported the yearly dividends for the last five years and their respective growth. On the left side are computed the expected dividends for the fiscal year 2024, 3.80$ per share, considering a 10% annual return for the investment (r) and the average dividend growth for the last 5 years (g) which is equal to 5.67%. Applying the formula reported in the picture I got a value of 92.65$ per share, significantly lower than the current price of 156$.

DDM valuation (Author's calculation on Excel)

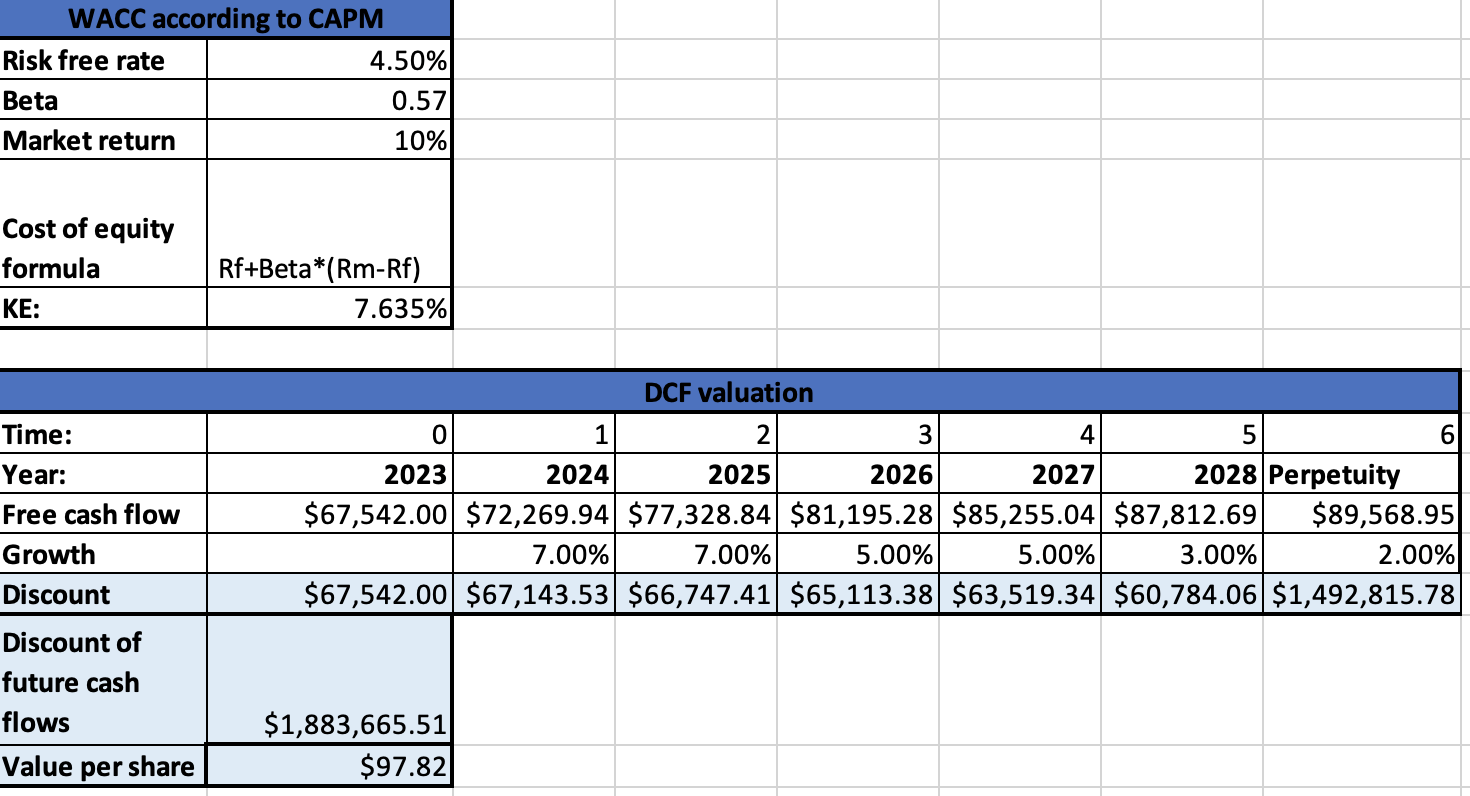

Passing to the DCF, considering all future growth catalysts in the previous paragraphs, and taking into consideration the highly competitive market, I get a fair value of $1.88 billion or $97.82 per share. These results are obtained by projecting revenue growth of 10% up to 2026, following my investment thesis, which will slow down for the remaining years. I assumed a perpetual growth of 2% and an increase in net margins up to the 2018 level (9%). I finally obtained the free cash flow by considering capital expenditures equal to 4% of revenues, and the same percentage also for depreciation and amortization. I finally computed the cost of equity following the famous capital asset pricing model formula reported in the picture below and I used it as a discount factor.

DCF valuation (Author's calculation on Excel)

The results obtained with the two models are similar and they are screaming "sell". The company is also overvalued when considering its forward P/E ratio of around 28 while the sector median is around 19. Even though the company has positive perspectives it seems that they are already priced in and I would stay away until it reaches a lower market capitalization.

J&J Snack Foods is a good company selling good products in a competitive industry. Even though it can increase its revenues on a double-digit base through different expansion opportunities, in the past few years it was not able to keep up with the same pace set by its peers and its profit margins are very low. The future good perspectives seem to be already considered in the current stock price and I would like to see a 40-50% stock price decrease before considering buying the stock.