Janus Henderson: Net Outflows Continue, Downgrade To Hold

Summary

Janus Henderson’s 4Q23 result was boosted by an unexpected turnaround in performance fees and strong equity markets.

Product investment performance and investment fee margin stability are positive factors for JHG, but ongoing net outflows are a material negative.

Whilst the Company still screens as slightly cheap, a less compelling overall investment case warrants a downgrade to Hold.

Andrii Yalanskyi/iStock via Getty Images

Introduction

Janus Henderson Group (NYSE:JHG) released 4Q23 results on February 1, 2024; the market reacted positively to the quarterly update, driving the stock price upwards by 4.4% on the day. Building on the momentum that was triggered by JHG's 3Q23 update, the company's share price is trading around 37% above lows hit in October 2023, comfortably beating the S&P500's increase of ~20.0% over the same period. At the time of writing, JHG's price stands at $30.31, a healthy 12% above the level of my most recent Buy rating published in early November 2023. In this note, I will discuss key 4Q23 positives and negatives and consider whether or not a Buy rating remains appropriate.

4Q23 Positives

Below is a summary and discussion of the key positives that I observed in the 4Q23 materials:

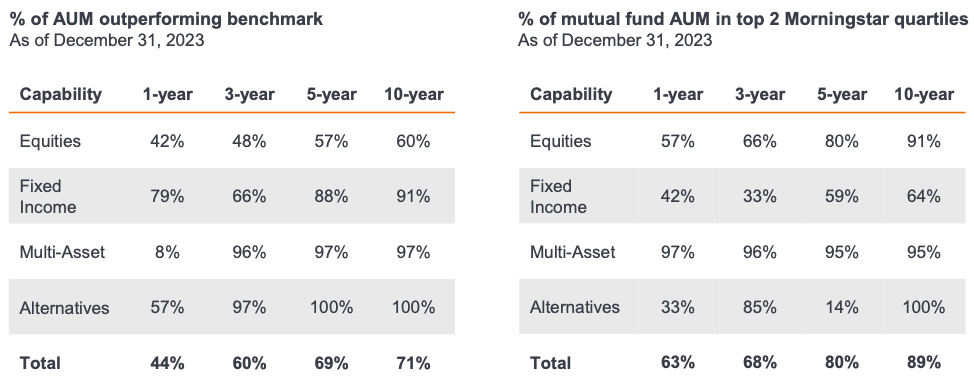

At the total AUM level, investment performance improved modestly at each of the 3-, 5- and 10-year measures on both a peer-relative and benchmark-relative basis. The deterioration at the 1-year measure was driven by Equities and Multi-Asset. I am inclined to agree with JHG's assertion that long-term investment performance is 'solid'.

Exhibit 1:

Source: JHG 4Q23 Presentation, slide 5.

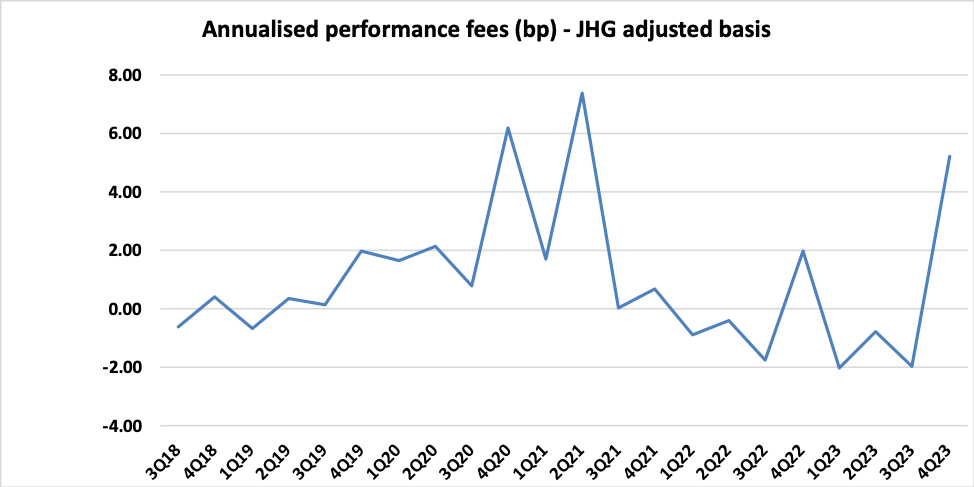

Performance fees for the first three quarters of FY23 were miserable (negative in each quarter), and at 3Q23 management lowered their guidance for FY23E performance fees to around -$45m, implying an expectation of around -$9m for 4Q23E. Actual 4Q23 performance fees of $41.7m therefore came as big surprise. It is important to recognize that the 4Q23 level of performance fees is not sustainable (refer to Exhibit 2 for context). Over the five years to 4Q23, performance fees have averaged around 1.1bp of AUM, but this average was given a healthy boost by the 4Q23 result. Note that for valuation purposes, I continue to assume average performance fees of 0.8bp pa (of AUM).

Exhibit 2:

Source: author's calculations using data from JHG financial reports.

JHG continues to face significant challenges on net flows (discussed below), but there are pockets of improved performance. JHG's active ETFs delivered net inflows of +$6bn in FY23. The group is now the fourth largest provider of active fixed income ETFs in the US market; JHG captured 20% of flows into such products in FY23. At a distribution level, both Institutional and US Intermediary generated positive net flows for the first time in many years.

4Q23 Negatives

Below is a summary and discussion of the key negatives that I observed in the 4Q23 materials:

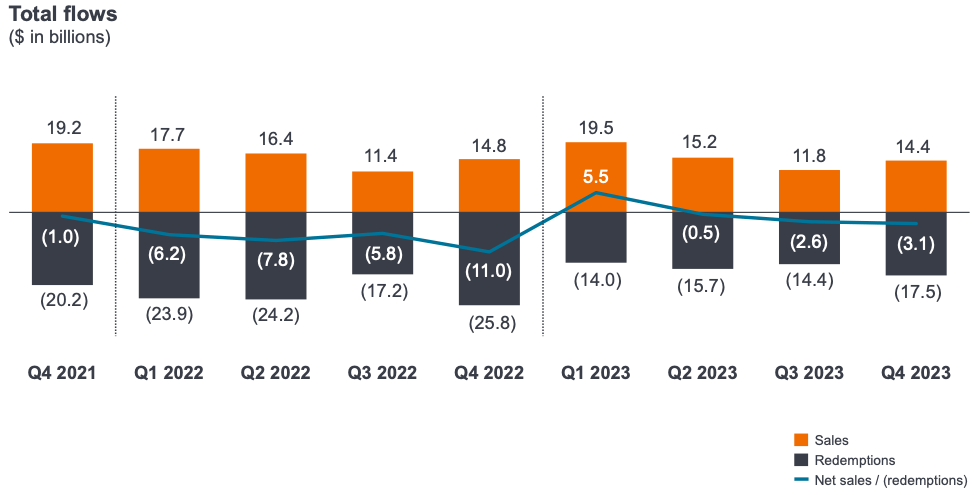

After reporting positive net flows in 1Q23, JHG has delivered three consecutive quarters of net outflows. Net flows for 4Q23 came in at a disappointing -$3.1bn. 1Q23's net flow of +$5.5bn provided an unexpectedly strong start to the year, but poor outcomes over the remainder of the year resulted in a total net outflow of -$0.7bn for FY23. Looking at the bigger picture of total AUM, FY23's net outflows represented around -0.24% of opening FY23 AUM. Fortunately for JHG, buoyant investment markets have much more than compensated for operational weakness on net flows, with AUM increasing ~16.6% from $287.3bn in FY22 to $334.9bn in FY23. Market returns boosted AUM by $29.7m in 4Q23 alone.

Exhibit 3:

Source: JHG 3Q23 Presentation, slide 6.

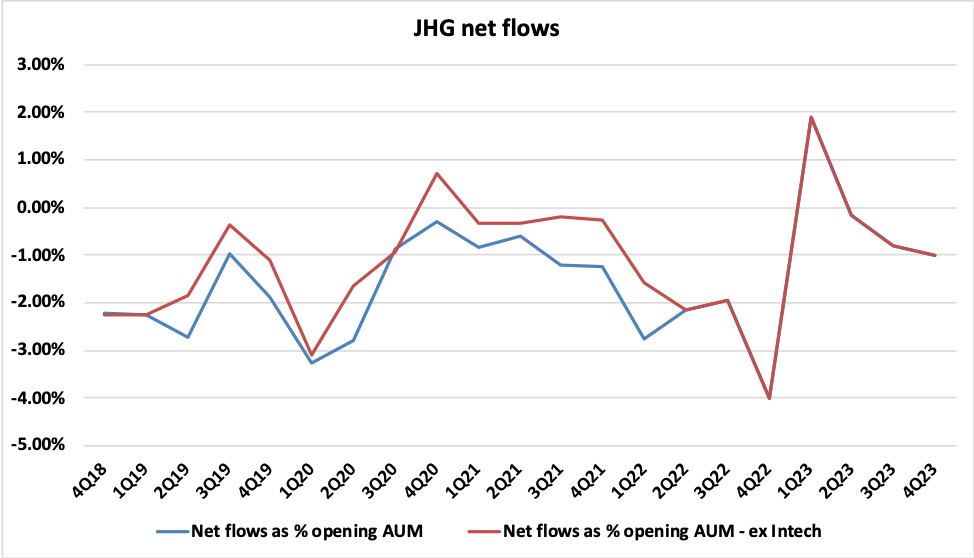

JHG's ongoing struggle with net outflows is a common feature across the funds management sector. Exhibit 4 plots JHG's net flow performance by quarter, both including and excluding Intech, expressed as a percentage of each quarter's opening AUM (with corresponding AUM including and excluding Intech AUM). Note that these percentages are quarterly rates, not annualized rates. In the absence of strong market returns, the drag on operating earnings from ongoing net outflows will become much more apparent.

Exhibit 4:

Source: author's calculations using data from JHG financial reports.

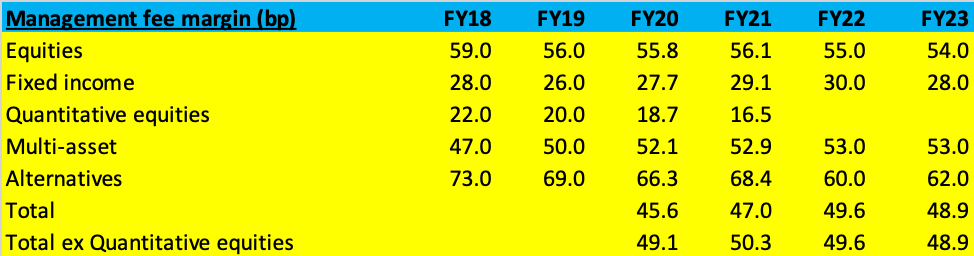

On a fee-rate adjusted basis, the mix of 4Q23's net flows was particularly negative. Higher management fee margin buckets of Equities, Multi-Asset and Alternatives each suffered outflows, with partially offsetting inflows into the much lower management fee margin Fixed Income bucket. Exhibit 5 shows how JHG's investment fee margins vary by asset class, along with movements over time in each product bucket.

Exhibit 5:

Source: author's calculations using data from JHG financial reports.

Management issued fresh guidance for FY24E expense growth. The updated guidance was in line with my expectations for the compensation ratio (43% to 45%), but non-compensation cost guidance of 'mid-to high-single digits' % above FY23 was somewhat disappointing. Ongoing investment in the business is important, but given the backdrop of ongoing net outflows, I would currently prefer to see JHG taking a tougher stance on expense growth.

Management's responses to analyst questions during the 4Q23 Q&A session make it clear that M&A remains on JHG's strategic agenda. I recognize that more positively biased analysts may see M&A as a potential upside risk factor, however I would much prefer to see JHG either grow organically or distribute excess capital to shareholders than to deploy cash on relatively small acquisitions that are unlikely to move the dial much in terms of overall group profitability.

Rating Update

JHG went ex-dividend ($0.39) on February 9, 2024. Using JHG's 4Q23 reported AUM of $334.9bn as a starting point, my normalized valuation framework generates a base case P/E of 11.1x. Note that this valuation allows for a decline in the net management fee rate to 48.2bp (from 48.7bp reported in both 3Q23 and 4Q23), and a net outflow in FY24E of -$3.0bn. Equity markets have started 2024 in a confident mood, and as of the time of writing, the average return YTD across the S&P500 and MSCI World accumulation indices is ~4.6%. Adjusting my valuation for the positive YTD influence of markets on JHG's AUM, I currently arrive at a P/E of around 10.5x. As a reminder, my fair-value benchmark for a fund manager is a P/E of around 12x.

After such a strong start to 2024, I find myself more persuaded by downside risk arguments than bullish arguments regarding where equity markets go from here. In that context, when thinking about valuation, I conclude that a current P/E range for JHG is 10.5x to 11.1x, with a bias toward the upper end. For income-focused investors, I note that when I last published on JHG in November 2023, the dividend yield was slightly above 6%; given the stock's price appreciation over recent months, the dividend yield has fallen back to a lower, but still healthy level of ~5.2%.

Whilst the valuation argument for JHG is reasonably persuasive, I was generally underwhelmed by the company's 4Q23 update. Significantly, management does not appear at all confident regarding the potential for JHG to deliver positive net flows in FY24E. On balance, and taking into account my concerns that equity markets may be slightly overheated, I conclude this review with a downgrade to Hold. I should note however, that investors with a more optimistic view regarding the outlook for equity markets may continue to see JHG as an attractive investment, and that the decision to downgrade was a rather marginal one.