kamilpetran/iStock Editorial via Getty Images

kamilpetran/iStock Editorial via Getty Images

In October 2023, I covered Norwegian Air Shuttle ASA (OTCPK:NWARF) stock and market it a buy as I believed the stock’s underperformance compared to peers was not justified. Since then, Norwegian stock has climbed significantly with a 51% appreciation since my last buy rating marking an excellent entry point for those who decided to invest. In comparison, over the same time period the S&P 500 returned 16% and the U.S. Global Jets ETF (JETS) returned only 12.35%. In this report, I will be discussing the company’s most recent earnings and assess whether the rating and price target need to be changed after the significant share price appreciation.

Norwegian Air Shuttle

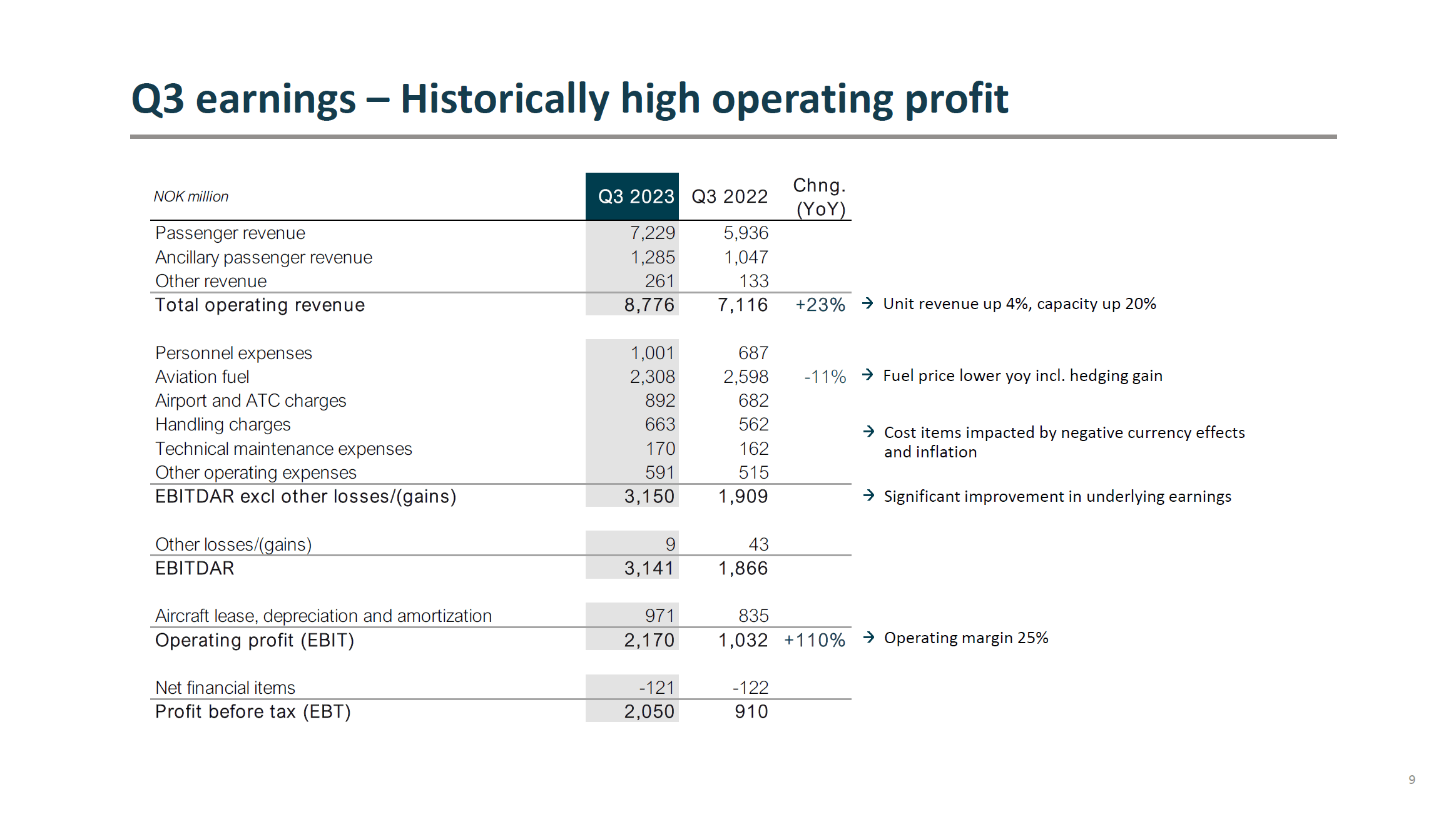

The fact that Norwegian Air Shuttle stock took off might not be a complete surprise if we look at the results that Norwegian posted. The company was able to increase its revenues by 23% including 21.7% increase in passenger revenues on a capacity increase of 17% pointing at strong unit revenues. At the same time, operating costs rose from 6 billion NOK to 6.6 billion NOK marking a 10% increase in costs but given the capacity growth of 17% this provided a favorable cost amortization partially driven by strong fuel hedges. Focusing on how strong the fuel hedging benefits were during the period: Fuel costs reduced by 11% while consumption increased by 13%.

Cost excluding fuel was 4.3 billion NOK compared to 3.5 billion NOK marking a 23% increase. So, ex-fuel cost amortization was not quite that favorable and that is driven by forex pressures of 6% and inflation of 5% partially offset by favorable cost amortization development. What we see at unit cost and capacity balance is that capacity increases currently are merely offsetting inflation to some extent but they are not truly able to offset any more than that and as long as that remains the case we will be seeing a higher operating cost basis for airlines.

Overall, looking at the results we see that EBITDAR grew 68% and operating profit more than doubled to 2.17 billion NOK. We are seeing that the business is scaling efficiently and while it is not the most efficient due to external factors such as forex and inflationary pressures, we do see strong cost execution and yield management. That is quite a difference from the Norwegian we saw years ago, back then Norwegian scaled its business without creating value. The company had added capacity, but eroded unit revenues in the process while its unit costs did not decrease sufficiently to run a sustainable business. Everything seemed to be focused on growth and there was no focus or strategy to translate growth to value. The execution from the current management is more prudent and that shows in the results.

Bookings for the November and December month also looked strong trending ahead of 2019 while the company has once again realistically brought its capacity down in the winter period by 30 to 40 percent in an attempt to take out the variable component of its costs during the lower demand months. So, the Q4 2023 and Q1 2024 quarters likely will not be the best quarters but this is a seasonal event and what will be interesting to see is how efficiently the company can bring its cost down. Given that bookings for the remainder of 2023 trended ahead of the 2019 curve, I believe that there is some positive upside to what normally is a weaker demand period for Norwegian.

Norwegian Air Shuttle

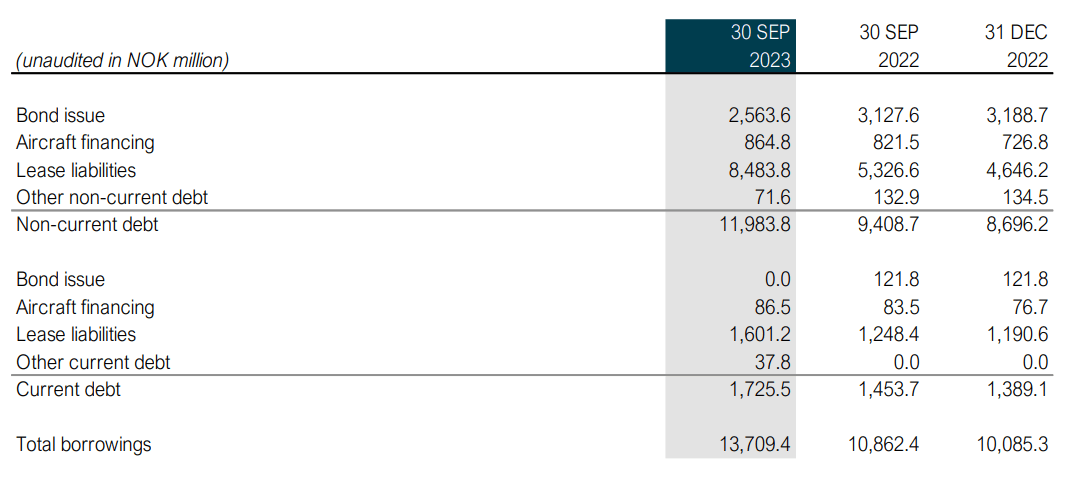

Year-over-year, total debt has climbed by 3 billion NOK which was fully driven by an increase in lease liabilities as the company’s fleets continue to grow via leases. Norwegian intends to own more of its airplane which at some point should better balance against the lease liabilities. Non-lease debt declined year-over-year from 4.3 billion NOK to 3.6 billion NOK with a manageable current debt balance. The non-lease borrowings were essentially unchanged between September 2022 and December 2022 meaning that year-to-date the reductions in debt are in the same range. Excluding lease liabilities, Norwegian had a net cash position of 5.8 billion NOK compared to 3.9 billion NOK a year ago. So, we are seeing a better debt coverage for Norwegian.

On the 24th of January, Norwegian Air Shuttle issued a profit warning and it was a positive one. As I pointed out earlier, the booking curve suggested there could be some upside to demand compared to what Norwegian has factored in and that was indeed the case and drove the operating profit expectations for 2023 up to 2.2 billion NOK up from a range of 1.8 NOK billion to 2.0 NOK billion that the company previously expected.

On cost level, the company expects 0.48 NOK in unit costs, which would be up 2%. On a 16% increase in capacity, you could be expecting around a 7% decrease on unit costs according to log-laws and even 15.5% based natural log-laws, but at this point the inflation and forex pressure are eating away some of the true gains in cost efficiency.

Analysts' consensus for Norwegian Air Shuttle for the fourth quarter is a revenue of $535.75 million, which would indicate 10.6% year-on-year growth. EBIT estimates stand at 2.2 billion NOK for the full year, which is in line with what Norwegian has guided for and is up 10% from previous estimates. This would indicate Q4 2023 EBIT of 295 million NOK compared to a 40 million NOK loss a year ago. The fourth quarter is a seasonally weak quarter, but seeing the airline turn a profit would already be good. Norwegian, prior to its restructuring, was seeing significant losses at 14% of revenues and the current guidance as well as analyst estimates are suggesting that as a smaller airline the company will now turn a profit instead of a loss during Q4 and that is encouraging.

While I am seeing a lot of positives, there are several risk factors that also need to be addressed. For quite some time we are seeing some forex pressures impacting the unit cost performance and with predominantly leased fleet invoiced in dollars and dollar denominated acquisition costs for airplanes, currency fluctuations could impact Norwegian’s results that will mostly be seen in the unit cost performance. Furthermore, Norwegian operates a fleet of Boeing airplanes and expects more airplanes to join in the years to come. However, Boeing has been barred by the FAA from raising 737 MAX production which is very likely to have an impact on the delivery schedule to Norwegian as well and I believe those delivery shifts are a watch item as the MAX plays a key role in reducing unit fuel consumption as well as executing planned growth.

The Aerospace Forum

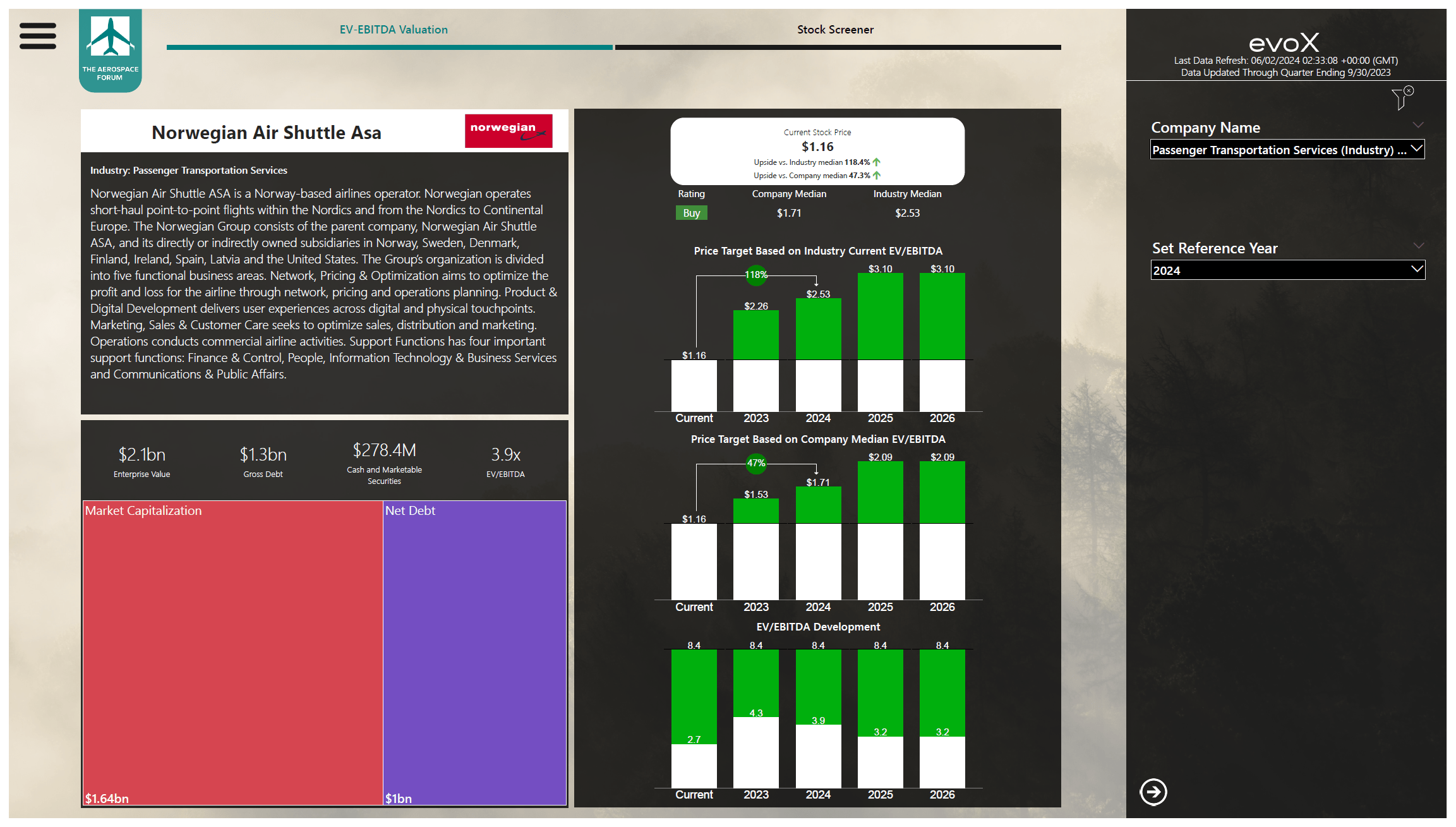

I implemented the balance sheet data for Norwegian Air Shuttle as well as projections for forward earnings and cash flows and based on that I believe that Norwegian Air Shuttle stock has around 50% upside to $1.71 per share. Determining a price target for Norwegian Air Shuttle is rather challenging because its long-term median EV/EBITDA is significantly higher than the current EV/EBITDA valuation and one can question whether the EV/EBITDA seen over the past 10 years is justified as Norwegian has significantly changed over the past two years alone. Therefore, I have implemented a company target valuation that averages the current EV/EBITDA and the median EV/EBITDA to come to a more balanced EV/EBITDA and based on that assessment which is conservative if we consider that the long-term EV/EBITDA multiple is higher there still is plenty of upside for NWARF stock.

I believe that Norwegian Air Shuttle stock remains a buy. It’s Q3 2023 performance was strong and for the fourth quarter demand has exceeded expectations. Furthermore, the company has executed well from cost perspective and it seems to have retired debt ahead of schedule, which in the current high interest rate environment can significantly reduce interest costs. It is undeniable that there are some risk factors that Norwegian Air Shuttle has to navigate, but it seems that the current management is well equipped to do so. As a result and keep in mind the forward projections, I do feel comfortable reiterating my buy rating for Norwegian Air Shuttle ASA stock.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.