Eoneren

Eoneren

Readers may find my previous coverage from last December via this link. My previous rating was a hold, as I expected, JELD-WEN Holding (NYSE:JELD) to continue seeing headwinds until 1H24 and that there were no visible catalysts that would drive up the stock price. I am reiterating my hold rating as I await a few more quarters to see how the underlying demand is trending and also to see if the Fed will indeed cut rates in 2H24. While the upside is attractive today, I think it is better to invest when JELD shows tangible progress in its results.

For 4Q23 reported on February 20th, JELD reported a decline in core revenues of 15%, driven by a volume/mix decline of 16%. At the reported level, total revenue came in at $1.02 billion, down 23.3%. By segment, North America fell 13%, while Europe fell 14%. Adj. EBITDA margins did overperform, coming in at 8.5%, mainly driven by productivity improvements, and positive price and cost were partially offset by lower volume and mix. Splitting by segments, adj. EBITDA margins in North America were 12.6%, up by 250 bps, while Europe margins were 5.7%, down 110 bps. JELD also ended 4Q with a net debt-to-EBITDA ratio of 2.5x, down by 0.2x vs. 3Q23. Management 2024 guidance calls for sales of $4 to $4.3 billion, implying core sales growth of -7% to 0%. Adj EBITDA is expected at $370 to $420 million but will be more backend-weighted as 40% to 45% of full-year EBITDA is expected in 1H24.

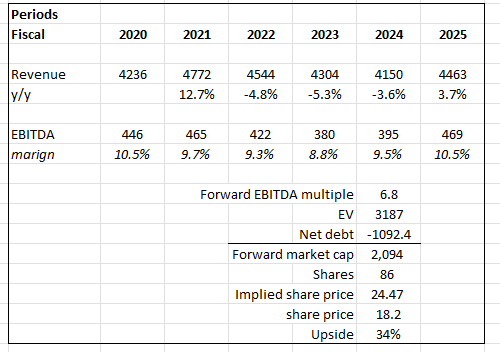

Based on author's own math

My model in this post is to show the potential upside if JELD sees a recovery in FY25 with margins improved from the various strategies implemented. Suppose JELD grows as guided in FY24 ($4.15 billion revenue at the midpoint) and sees a recovery in FY25 (likely driven by the rate cut in FY24). JELD should see positive growth in FY25. I modeled a 3.7% growth in FY25 using consensus estimates as a guide (consensus estimates over the past few years have been fairly accurate, with ~1% difference on average). On the EBITDA margin line, if JELD successfully executes, I expect margins to see improvements. As I discussed below, JELD should have no issues breaking past the previous peak margins, but to be conservative, I modeled FY25 to achieve similar margins as in FY20 (10.5%). When all of these play out, JELD should see its valuation revise upwards towards its mean as the fundamentals improve. I assumed multiples to rerate back to the midpoint of where it is trading today (6.3x) and its average of 7.3x, equating to 6.8x forward EBITDA.

As I expected, 4Q23 shows that JELD is still facing headwinds, and management guidance for at best flattish core sales growth also indicates that headwinds will persist for most of FY24. That said, there are positive signs that suggest a recovery is going to happen in FY24 (probably in 2H24).

Firstly, pricing is holding up pretty well. While core sales fell ~14%, it was mostly dragged down by a volume decline offset by an increase in pricing (~1% contribution). The 1% contribution was relatively strong if we consider that JELD is lapping heavy pricing actions from 2022. The fact that JELD is able to push through a price increase (over a high base) would imply that the demand environment is not at its worst stage. My view is that, at the worst stage, JELD needs to slash prices to drive volume. Second, there is encouragement in the fact that there are indications of a rebalancing of inventory in North America, even though volume demand is still weak due to factors such as the retail channel managing down inventory at year-end and specific non-res projects affected by financing issues. In my opinion, the retailers have to restock their inventory at some point in order to prepare for the next recovery cycle.

And by the way, we're starting to see some rebalancing of inventories as people start to better position themselves for potential growth in the back half of this year. Source: 4Q23 earnings

This restock motion will provide JELD with a strong near-term performance (from the sell-in). My expectation for this acceleration to happen is in 4Q24/1H24, when the Fed starts to cut rates, lowering mortgage rates and making them more affordable for home buyers. This would lead to increased demand for housing construction or renovation, which means more demand for doors. Another reason for my assumption in that timeframe is that it takes time for the fall in interest rates to translate into demand.

Yeah, and so we typically think about on our products on the new construction site that's more of a 6-month to 9-month lag between a start and our sales -- our lead times are pretty short, so sort of two weeks on the door side -- three to four weeks on Windows depending on the product type. Source: 4Q19 earnings

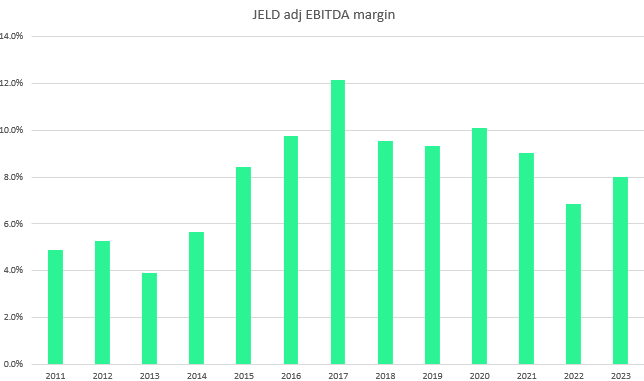

Another encouraging aspect of JELD's business is its EBITDA margins, which improved in 4Q23 despite weak core sales. This tells me that management margin improvement initiatives have been well executed and that JELD now has a structurally lower cost profile. Even better, management is targeting more savings. In FY24, management is targeting $100 million of cost savings, and I think this is an achievable target as 50% of it is pretty much in the bag already (carried over from FY23) and the balance will be from new initiatives. Looking at JELD’s historical adj EBITDA margin, there is clearly a lot of room for JELD to “recover grounds” (peak adj EBITDA margin was ~12% in FY17 vs ~8% in FY23). The $100 million cost savings is about 2% of FY23 sales, and doing some simple math, this suggests the JELD peak margin is probably in the mid-teens percentage range (12% + 2%). This also means that the incremental margin from the 5% level in FY23 is going to be huge when the next upcycle comes. In other words, near-term earnings growth is going to be elevated when JELD goes through the early phase of the recovery cycle.

Looking farther ahead, I believe peak margins could go even higher as management seems to be very focused on driving productivity. As an example, a new CPQ (configure, price, and quote) system will be implemented in Europe. This system will simplify integration with internal systems and streamline customer interactions. In five years, this system is anticipated to generate an EBITDA benefit of more than $15 million. Converting the North American door manufacturing process from batch processing to a one-piece flow is another example. Over the course of five years, this automation is anticipated to generate an EBITDA benefit of over $22 million. In the next quarters, the catalysts that drive positive stock sentiment are when management talks more about improving productivity (like streamlining the sales force, automating processes, and consolidating footprints).

So I would say that we're definitely cleaning up our distribution model and we're looking at that as we do assess our footprint and our cost to serve our key customers across all markets in North America.

And that means cleaning up our supply chain, that means optimizing our footprint, that means driving growth initiatives. And if we execute on that, which I'm very confident that we will, that puts us in a great position in the market.

In addition, we continue to right-size our manufacturing network as well as invest in automation and utilize our scale to streamline sourcing among many other smaller initiatives across the organization. Source: 4Q23 earnings

Based on author's own math

I maintain my hold rating on JELD. Despite signs of potential recovery in 2H24, I advocate a cautious stance until tangible results materialize. However, if the recovery growth does come, I expect JELD to see strong EBITDA growth, driven by its improved EBITDA margins from the cost-saving initiatives and long-term productivity strategies. The key upcoming catalyst that I am waiting for is the Fed rate cuts, which should give a much better sense of the recovery timing. Until then, I advise investors to stay conservative.