Tempura/E+ via Getty Images

Tempura/E+ via Getty Images

Following my coverage of J.B. Hunt Transport Services (NASDAQ:JBHT), for which I recommended a buy rating due to my expectation that the downcycle for JBHT is likely to be over and that it should see positive volume growth ahead, this post is to provide an update on my thoughts on the business and stock. I remain positive about the JBHT recovery trajectory, as can be seen in the intermodal [IM] segment volume performance. As volume increases, positive pricing growth should follow, which collectively should drive acceleration in IM revenue growth and margins (as operating leverage kicks in). Anticipating JBHT to show recovery growth, I expect the market to value JBHT at a premium valuation compared to its historical average.

JBHT saw total revenues of $3.3 billion in 4Q23 (down 10%), which led to a full-year decline of 13% which is in line with my expectations. However, JBHT reported 4Q23 EBIT of $203 million, ending the year with $993 million EBIT, which led to a lower than expected net income of $728 million. As such, FCF also came in lower than I had expected ($144.4% vs. $234 million for FY23). All in all, I would say that JBHT performance is alright, as the key segments, IM and Dedicated, showed early signs of recovery, although International Capacity Solutions [ICS] remains a drag.

Starting off with JBHT’s largest segment, IM, while revenue was down 7% y/y, I believe the sequential improvement speaks very well of the underlying demand that JBHT is seeing. Revenue growth has improved from -19% in 2Q23 to -15% in 3Q23 to -7% in 4Q23. Notably, management has observed an improvement in monthly volume trends for the past 9 months running. In October, volumes increased by 6%, in November by 6%, and in December 2023 by 8%. I believe this points to JBHT moving past the bottom of the destocking cycle already, and the volume growth from here should remain positive. In terms of pricing, calculated revenue per load (down~13%) indicates that pricing is still negative (~6%), but I don’t think this negative pricing trend is reflective of the upcoming quarter's performance given that price is typically a lagging indicator. The fact that volume is improving sequentially is a positive indicator for upcoming pricing growth. The reason, I believe, is because an improvement in volume signifies that underlying demand for logistical services is going up, and clients would have to account for this “improving volume condition” in the upcoming bidding periods. They are likely to bid more aggressively to secure more capacity to make sure they can meet higher volume demand.

Having said that, I think it's important to reiterate the volume is historically a leading indicator while price is typically a lagging indicator with uncertainty around the timing of any potential inflection.

Yes. Brian, I would just add -- this is Brad Hicks. Similar to what Darren said, it's really way too early in the bid cycle to see what's ahead of us there. But at least from our perspective, from a trucker standpoint, rates have to go up and I can't. 4Q23 earnings results call

However, in this case, patience is required because the positive pricing impact will not show up in the P&L in the near future because bids priced in previous periods are still in place. Although the bid season has only just begun, I am optimistic about the company's prospects and their ability to increase their market share thanks to the excellent service they've delivered via their rail partners, new products like Quantum, and their service out of Mexico with GMXT, which will provide customers with more options and address their cross-border needs.

The next largest segment, Dedicated, deserves discussion as well. While growth remains negative, I thought the topline performance was not as bad as it seems. Demand for dedicated services remains resilient despite the challenging freight environment. Objectively, there was a 100bps sequential improvement, and around 300 trucks were sold in 4Q, resulting in 1,150 trucks sold in FY23. Moreover, this segment’s operating ratio also improved vs. 3Q23 once we adjusted for the extraordinary insurance losses and losses on sale. When accounting for around $20 million in insurance-related charges and a net $8.1 million increase in loss on sale of equipment, DCS operating income should be around $114 million (or an 87.1% operating ratio, a 140bps improvement vs. 3Q23).

To sum up my thoughts until here, I believe JBHT continues to move in the right direction as pressures in IM are clearly abating on this front and overall freight demand as imports have continued to be strong to end 2023. Overlaying these positive factors is that inventories appear to be nearing the end of destocking, according to the LMI (Logistics Manager’s Index). This should bode well for when retailers and other shippers decide to restock in response to either a pickup in consumer demand and/or just a need to replenish the shelves as JBHT heads into next year’s back-to-school or peak season. JBHT’s dedicated segment has also shown sequential improvements (both revenue growth and EBIT margin) and resilience in the current challenging environment, which should see further improvement in 2024 as the macro environment gets better relative to 2023.

Own calculation

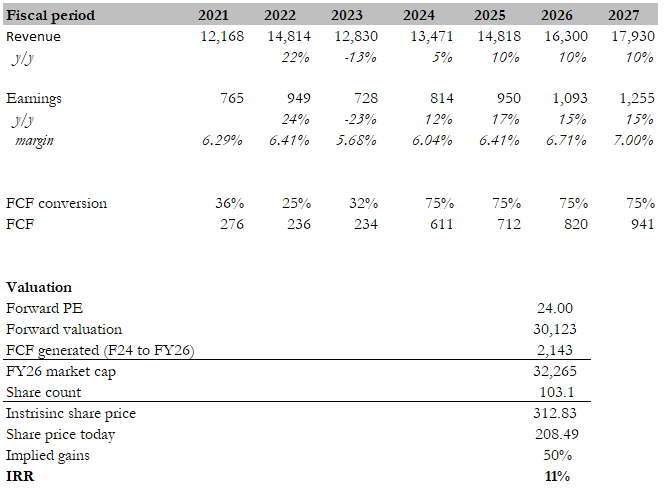

My revised target price for JBHT based on my model is ~$313. This target price is slightly lower than my previous target price as I adjust my expectations for FY24 slightly lower to reflect more conservatism in the timing of recovery. Hence, I adjusted my FY24 growth expectation by half, making it in line with consensus estimates. I took a similar action for FY24 margin expectations due to the headwind from JBHT insurance coverage. For background, JBHT purchased insurance coverage for a portion of expenses related to vehicular collisions and accidents, including a level of self-insurance (deductible) coverage applicable to each claim as well as certain coverage-layer-specific, aggregated reimbursement limits of covered excess claims. For the second year in a row, claims exceeded the existing coverage layer as settlement costs continued to escalate. I expect this insurance impact to linger in FY24, delaying the margin improvement trajectory. To reflect this change in the model, I assumed a 2-stage growth now: JBHT to recover back to the 2022 peak margin in recent years by FY25 (insurance coverage headwind should ease by then); and JBHT to recover back to the previous high of 7% margin (FY15) as it reaches the peak of this cycle over the next 4 years. However, I made a positive adjustment to the valuation that JBHT should trade at, as I expect the market to start pricing in JBHT and expect recovery over the medium term, given that it has shown positive early signs of growth recovery in IM. I assumed JBHT to trade at 24x forward earnings, 1 standard deviation above its average.

The timing of growth is really hard to pinpoint today, given the improved-but-still-uncertain economic outlook. Just last week, the Fed decided to push off rate cuts because inflation is still sticky and the labor market is still hot. If these conditions persist, the Fed may not cut rates at all. That could delay recovery as it weighs on consumer spending.

I believe JBHT is on a positive recovery trajectory, as evident in the improving volume performance, particularly in the IM segment. Despite FY23 revenues declining 10%, the sequential improvement in IM revenue growth signals a turnaround from the destocking cycle, with monthly volume trends consistently rising. While pricing remains negative, it should improve following the upward trend in volume. The Dedicated segment also exhibits resilience and sequential improvements, showcasing a favorable operating ratio.