Daniel Grizelj/DigitalVision via Getty Images

Daniel Grizelj/DigitalVision via Getty Images

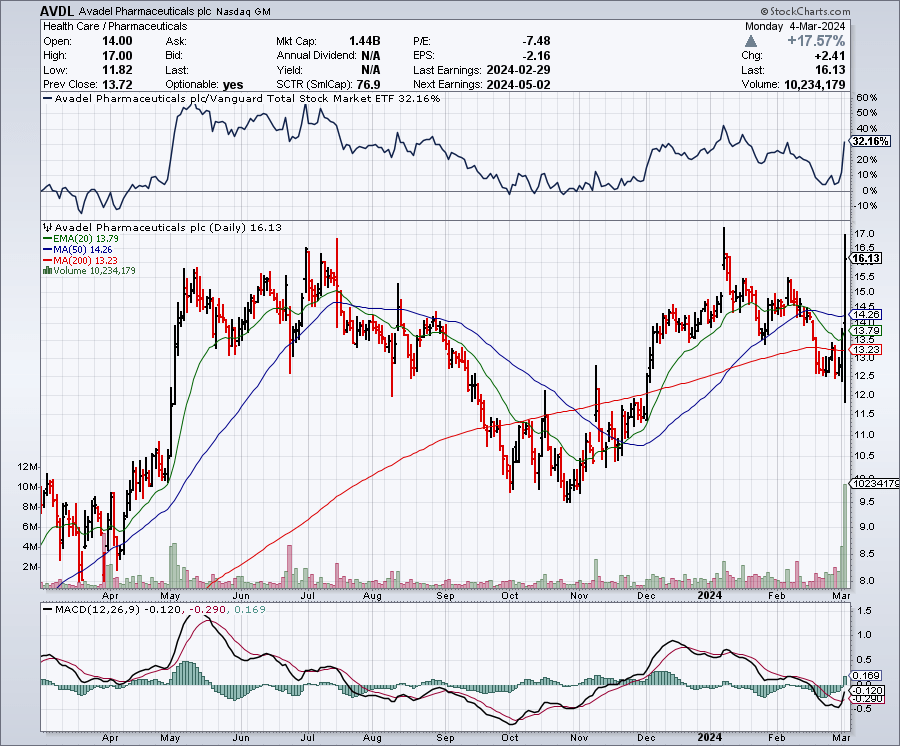

Avadel Pharmaceuticals plc's (NASDAQ:AVDL) stock is up 51% since my "Buy" recommendation in November, and we've had a couple of key updates that took place on Monday.

Seeking Alpha

First, the company reported Q4 earnings. Then, a jury awarded Jazz Pharmaceuticals plc (JAZZ) a 3.5% royalty rate on Avadel's Lumryz after ruling that Lumryz infringes on Jazz's Xyrem patent. The following article describes these events more in detail and updates my investment thesis.

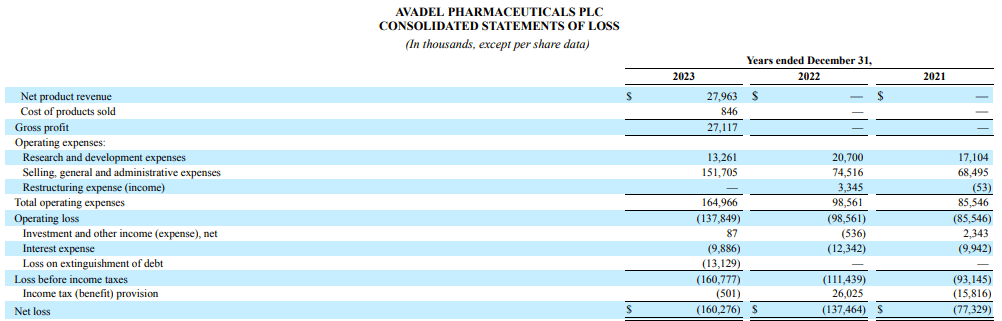

For the fourth quarter of 2023, Avadel recorded sales of $19.5 million from Lumryz (approved in May), its narcolepsy treatment. Remember that Xyrem and Lumryz are both sodium oxybates, so they are basically the same. However, Avadel's Lumryz only needs to be taken once a night, while Xyrem has two dose requirements. This dosing advantage within a multi-billion dollar narcolepsy market formed the bedrock of my initial optimism in Avadel.

According to Avadel, more than 2,200 patients had enrolled in RYZUP (the company's support services) as of January 31st, and more than 1,200 patients had started therapy.

Turning to patients who have initiated therapy, as of December 31st, there were 1,000 patients who had initiated the LUMRYZ treatment and that number grew to greater than 1,200 by the end of January. Typically, the start of the year can be more complicated to initiate new therapies, so we were pleased to see that we did not lose any momentum in getting new Lumryz patients started. Importantly, the majority of these patients are commercially reimbursed.

Although Avadel's net losses are not yet curbed by Lumryz's launch, the company projects achieving operating breakeven this year "when there are approximately 1,300 to 1,500 commercially reimbursed patients on therapy." The company also pointed to lower-than-historical (<25%) discontinuation rates relative to twice-nightly oxybates. This suggests that the company's high SG&A costs relative to revenue gains are temporary.

Avadel

These are positive developments. Lumryz seems to be catching on, and the fact that Avadel anticipates achieving operating breakeven this year highlights their optimism. For 2024, the company agreed with the revenue consensus of $155 million, "including the possibility the 2024 revenue could be higher if actual results for Lumryz, such as the rate of increase in commercially reimbursed patients, the total number of reimbursed patients who are treated with Lumryz, and net pricing outperform the assumptions currently used by the sell-side."

Just hours following Q4 earnings, Avadel's stock rose 18% after a court favored Jazz in a patent dispute over a sleep disorder drug, but awarded Jazz a lower-than-requested royalty rate; Avadel also secured a patent victory. According to the Seeking Alpha update, Jazz had been seeking a royalty rate as high as 27%. Obviously, the higher the royalty rate, the less profit Avadel can make. A royalty rate of 3.5% is a pittance in comparison to the worst-case scenario and should have no significant influence on Avadel's bottom line.

Of course, this isn't the end of the litigation matters, as Jazz has issued at least four formal complaints. Jazz has also sued the Food and Drug Administration for approving Lumryz (page 96). Oral arguments are slated to begin in April.

Turning to Avadel's balance sheet, the combined liquid assets total $105.1 million, juxtaposing this against a diverse array of liabilities, including long-term debt and lease liabilities, among others. The current ratio, calculated as total current assets divided by total current liabilities, is approximately 3.64, indicating a strong ability to cover short-term obligations.

The net cash used in operating activities over the last year was $128.5 million, translating to a monthly cash burn of approximately $10.7 million. Given the liquid assets, the cash runway is estimated to be around 9.8 months, cautioning that these figures are historical and may not directly predict future performance.

The odds of requiring additional financing within the next twelve months are deemed high, considering the current cash burn rate and operational funding needs.

However, assuming the company achieves $25 million in quarterly revenue in either Q1 or Q2, they have the option of drawing upon the second tranche ($45 million) of the Royalty Agreement they signed last year.

According to Seeking Alpha data, AVDL's market capitalization stands at $1.23 billion, signaling a moderate scale within the biotech sector. Growth prospects appear strong, with revenue projections showing a staggering 449.10% increase in 2024 and continuing triple-digit growth into 2025. Compared to the SPY, AVDL's stock momentum over the past year (+44.73%) significantly outpaces its 9-month and 6-month performances, hinting at a volatile but potentially upward trajectory.

StockCharts.com

Per Fintel, the short interest is substantial at 13.61% of the float, indicating a high level of investor skepticism or speculative interest. Institutional ownership is robust at 61.94%, with notable movements seen in new and sold-out positions-2,182,306 shares newly acquired versus 988,592 shares sold out. Key institutions like Janus Henderson Group and Polar Capital Holdings show confidence in their significant holdings. Insider trades reveal net negative activity over both the past three (-73,000) and twelve months (-60,475), suggesting cautious or profit-taking behavior from those with intimate knowledge of the company.

Evaluating these dynamics, AVDL's market sentiment is qualified as "adequate," balancing strong growth prospects and institutional confidence against high short interest and recent insider selling trends.

In conclusion, Avadel's recent advancements and the resilience shown in the face of challenges, positions it as a compelling "buy" opportunity for investors seeking exposure to the biotech sector. The company's successful navigation of a patent dispute with Jazz, securing a manageable 3.5% royalty rate, removes a major overhang on the stock. The robust patient uptake of Lumryz, coupled with its unique once-nightly dosing advantage, underscores Avadel's potential to capture a significant share of the multi-billion-dollar narcolepsy market. Moreover, the company's projections of at least $1 billion in peak annual revenue for Lumryz appear reasonable, especially since the drug has orphan exclusivity. In light of this, the stock's near-$1 billion valuation appears to be an inefficiency on behalf of the market. Financially, the company's strong balance sheet and the prospect of reaching operating breakeven in 2024 enhance its investment appeal. However, investors should weigh the inherent risks, including the ongoing litigation with Jazz, the high cash burn rate, and the potential need for additional financing, which could dilute shareholder value. Despite these risks, Avadel's strategic positioning, projected revenue growth, and the underpinning of institutional support suggest that the stock's upward momentum is likely to continue, making it worthy of another "buy" recommendation.