VioletaStoimenova

VioletaStoimenova

I wanted to make an update on Jacobs Solutions (NYSE:J) and look at how the company’s financials progressed throughout the year. I covered the company last in July. I see that the company’s revenues are quite resilient, and the spin-off is well on its way, which gives me hope that the separation of the government services side will create a much more streamlined and more profitable company in the end, that may have a lot more power to negotiate its contracts and to achieve higher margins in the process. I am sticking with my buy recommendation, and I am excited about what’s next for the company once the separation is finalized.

As of FY23, the company had around $926m in cash and equivalents, against $2.8B in long-term debt, which has reduced by a considerable amount in FY22, which stood at around $3.36B. I don’t think this is overindulging in debt, but many investors will avoid any companies that have debt, just because it’s debt, however, the company makes around $1B in operating income, which more than covers the annual interest expense on debt by a ratio of 6 to 1. It even is above my more stringent requirement of at least 5x, whereas it is well above what analysts consider a healthy ratio of 2x. Furthermore, if the company continues to pay down debt, this should start to attract a lot more investors who may have been more debt-averse. Safe to say, the company is at no risk of insolvency.

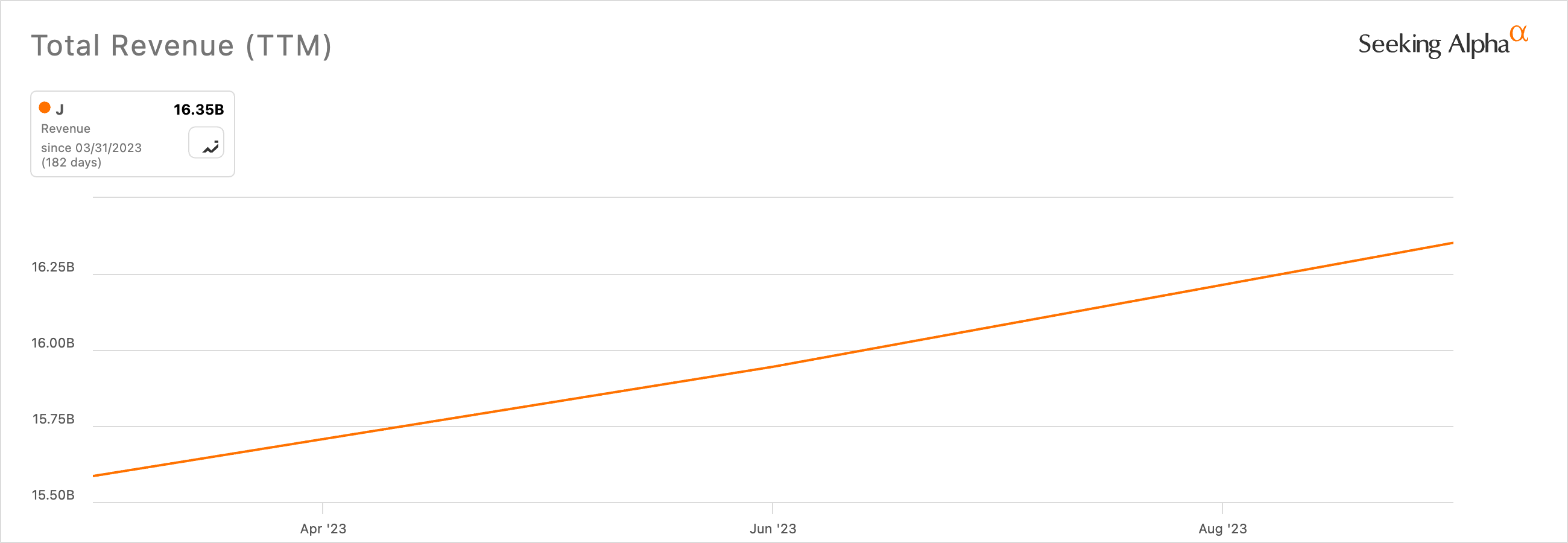

Looking at how the company’s revenues have progressed over the last three quarters, I see solid growth both sequentially and y/y, which was a little surprising given the tough economic environment we’ve been in over the last year. Many companies besides the hot ones in AI, have been reporting declines in profits, but Jacobs managed to stay on top and that shows how resilient the company is.

Revenue growth (SA)

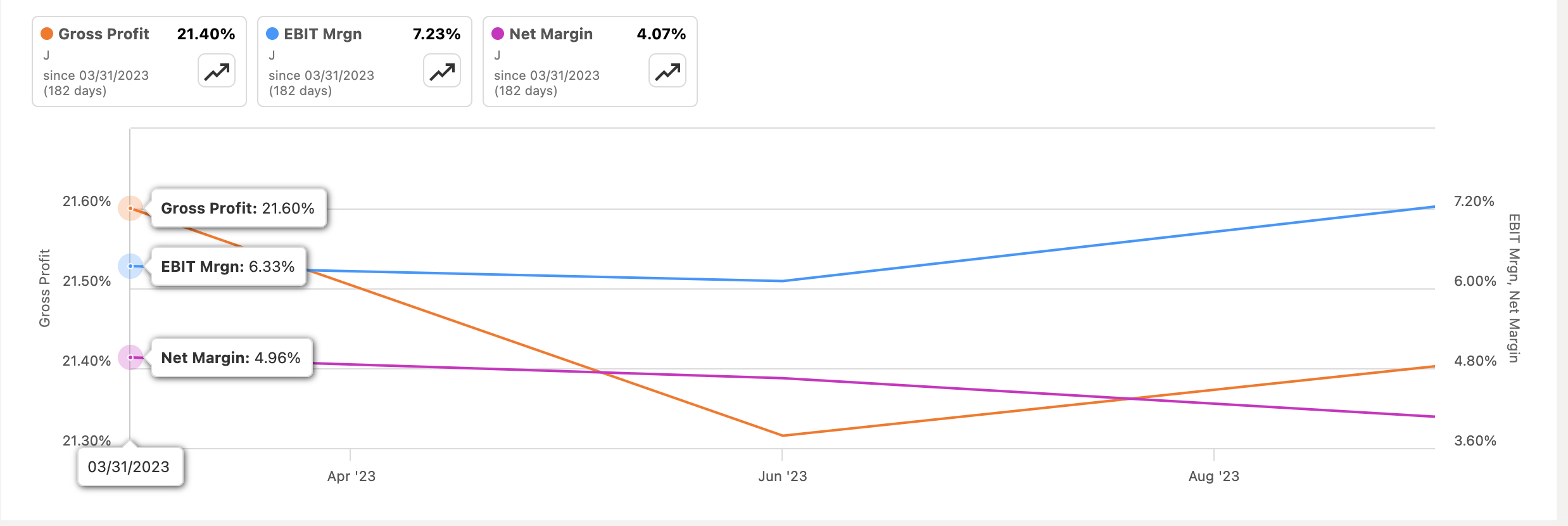

On the margins side, it’s a mixed bag. Gross and net margins have declined slightly over the last 3 quarters, while the company managed to improve EBIT margins slightly. The company is in a tight margin business as it is, so an almost 100bps decline in net margins is quite a chunk. I will touch on in the later section how the company plans to improve these and all other metrics discussed in this section.

Margins progress (SA)

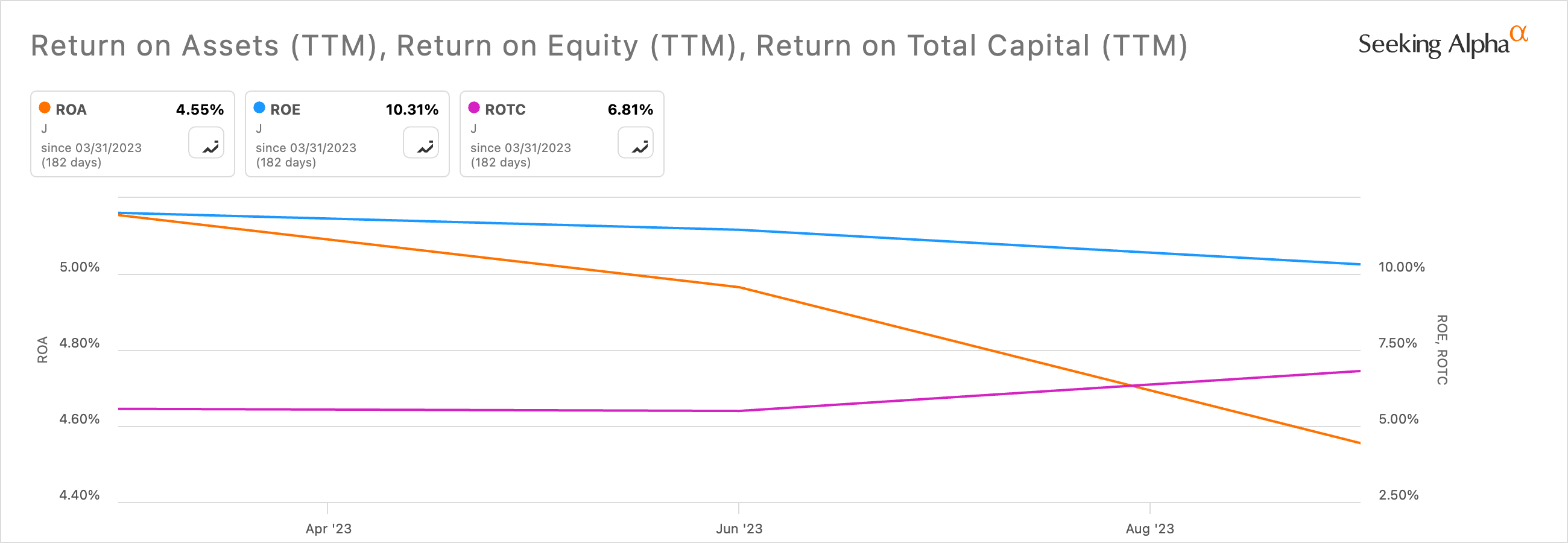

Since the company saw a slight decline in its bottom line, it’s no surprise that the company’s ROA and ROE have followed suit. It seems that the company has become a little less efficient at using its assets and shareholder capital, as expenses increase exceeded revenue increases, especially the annual interest expense which saw a 68% increase y/y. Furthermore, the company’s ROTC improved slightly over the same period, which means that the management is capable of allocating capital to more profitable endeavors.

Efficiency and Profitability (Author)

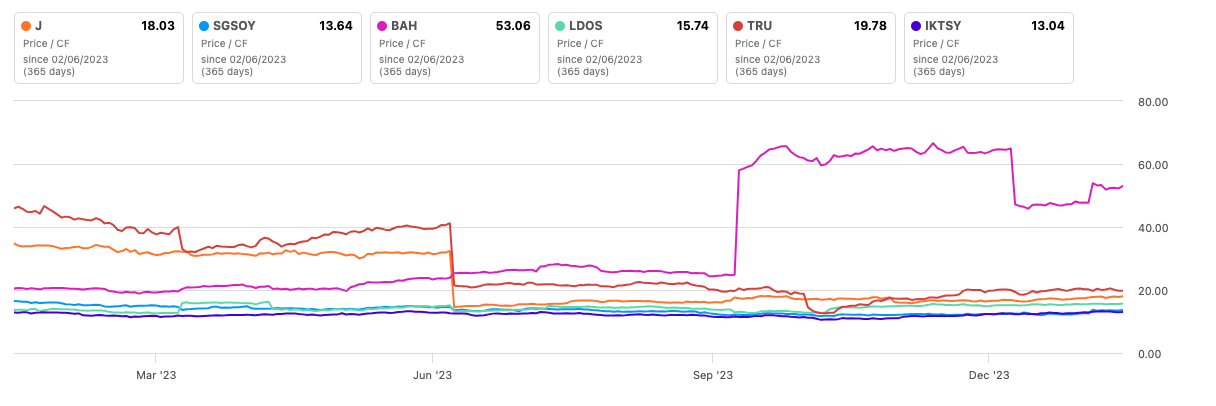

If we compare ROTC to some of Jacobs’ peers, we can see that it is very close to other government contractors like CACI (CACI) and Booz Allen Hamilton (BAH), however, KBR (KBR), which I recently covered, is enjoying a little bit more of a competitive advantage, as it seems it is getting a better deal on their contracts overall.

ROTC vs Peers (SA)

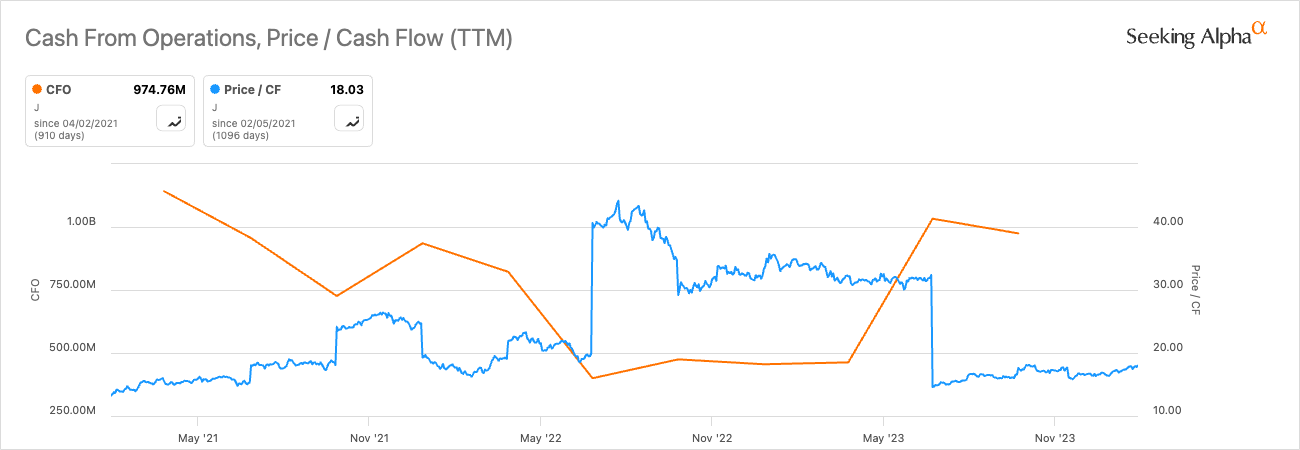

Jacobs's free cash flow has been on a roller coaster for the last few years, and it seems to be recovering in recent quarters. The company has been generating a decent amount of cash over the last few quarters, and it looks to be continuing going forward. The company’s price/cash flow is sitting somewhere at the recent bottom, which may indicate a fair price or close to undervaluation. The company's cash from operations has doubled, which brought the company's P/CF much lower compared to mid-2022. I believe the company is in a much better position now and the more-than-halving of P/CF means the company is doing much better now because its CFO is more robust.

P/CF (SA)

While comparing the metric to the company's peers (as picked by SA by default) we can see J is trading somewhere in the middle of the pack.

P/CF vs Peers (SA)

Overall, the last year for the company wasn’t the worst I’ve seen, which shows that Jacobs is a quite resilient business, and that is a business that should attract many investors who are looking for more safety. The company has been paying down its debt, which should also interest a couple of more investors to have a closer look at the company and its prospects. I am not liking the fact that the margins slightly decreased over the period, but that was mostly because of much higher annual interest expenses, while EBIT showed an improvement, which means that costs are coming down.

The company just reported Q1 ´24 results, which beat non-GAAP EPS by $0.46 cents to get $2.02 and $4.2B revenues that beat estimates by $200m, so it was a decent report. Furthermore, the backlog of $29.6B was up 4.7%, while gross profit in backlog was up 6.1%. Solid revenue growth y/y of 9.5% and very solid cash flow from operations of $418m.

The investors seem to like that the company reiterated its outlook for FY24, which is better than a downward revision. Overall, I think the report didn't have anything surprising and the stock rallied slightly on a decent report, but then came down a little and is up about 2% as of writing the article. To be honest, I would have liked a pullback a little bit to get a better entry point, but this doesn't change my recommendation.

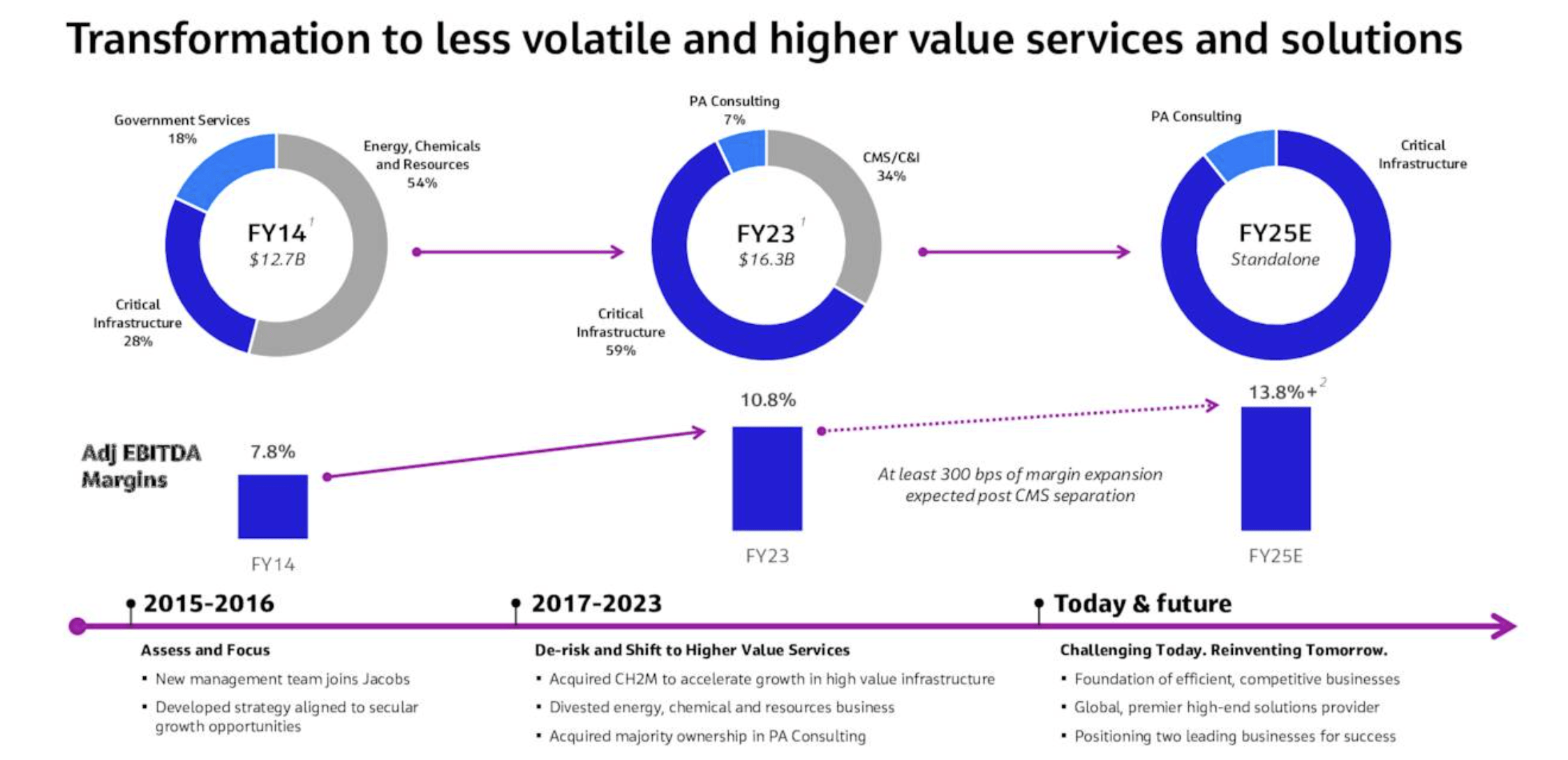

The spin-off of CMS is well underway and has passed all shareholders' and board approvals. The spin-off will take out Critical Mission Solutions and will also take with it Cyber and Intelligence government services business, which were part of Divergent Solutions. The deal is meant to be closed sometime in the second half of 2024, so it is still quite a wait, however, once that goes through, the original company will become a lot more streamlined. This should improve the company’s overall margin levels since the government side of the business will be moved to a separate publicly traded entity. I am not a fan of companies that rely heavily on government contracts as their primary source of revenue. These contracts are notorious for their thin profit margins because of the competitive bidding system, where the lowest bidder wins. Additionally, these contracts come with a significant amount of red tape and other compliance requirements, which may add to costs and reduction in the bottom line. So, I am very excited to see how the company is going to fair in the long run, once the spin-off is finalized, as I would rather own a company that may not have a ceiling to its profitability.

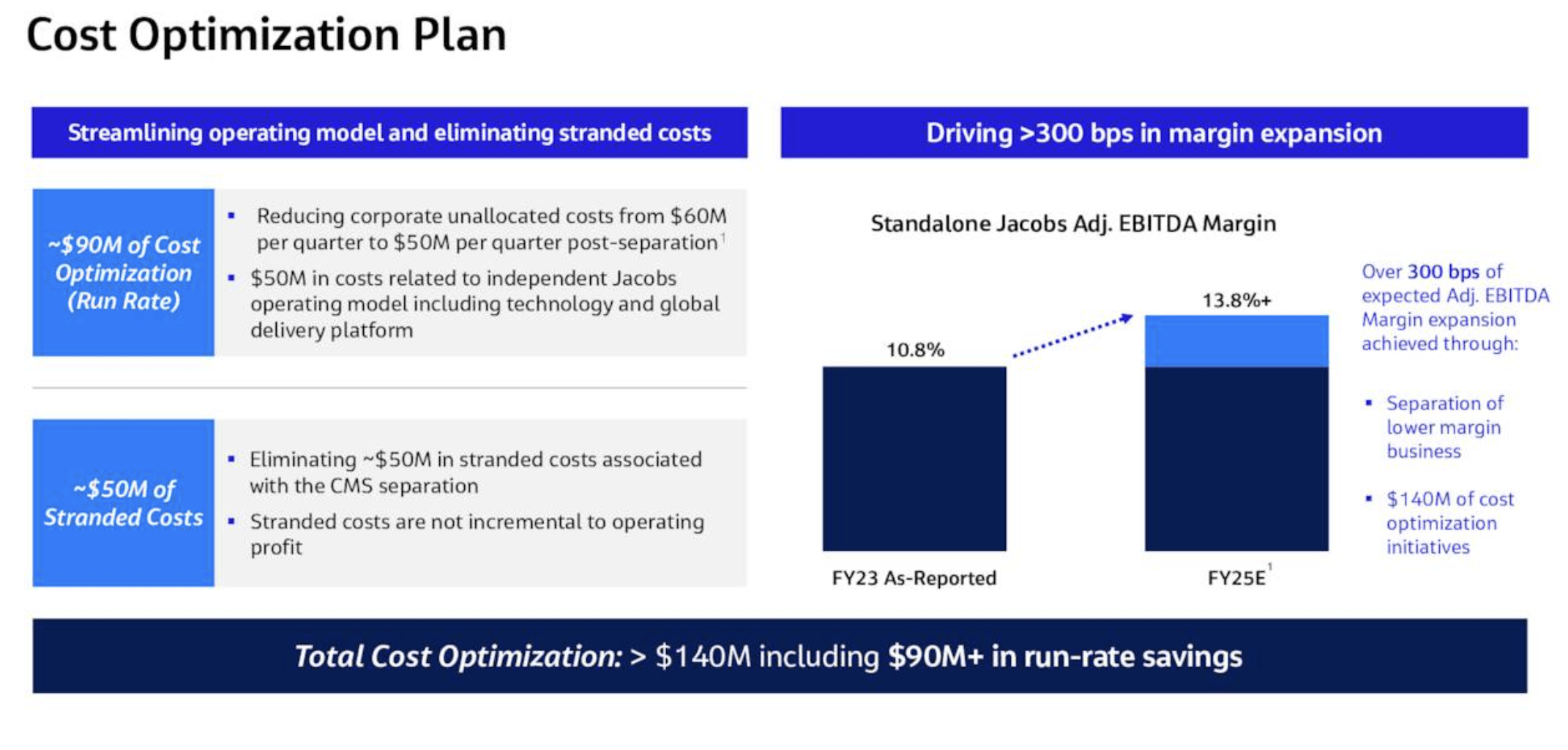

So, what is the company going to do about the margins going forward? The management is looking to execute a multi-year cost-cutting plan, which if all goes to plan, should create around 300bps improvement in margins over the next 2 years. To be honest, I don’t think it should be that hard of a job to achieve higher margins, as I mentioned earlier, these improvements should come naturally since the government contracting will be spun off, which will give the company a lot more power to negotiate contracts with private entities. As of the latest year, I calculated that the CMS segment operating margin stood at around 8%, P&P Solutions at around 10%, Divergent Solutions at 11.5%, and PA Consulting at around 20%, so naturally taking out the worst performer from the bunch will improve the company’s performance, and that is going to be attractive to many investors, including me.

Investor Slides Investor Slides

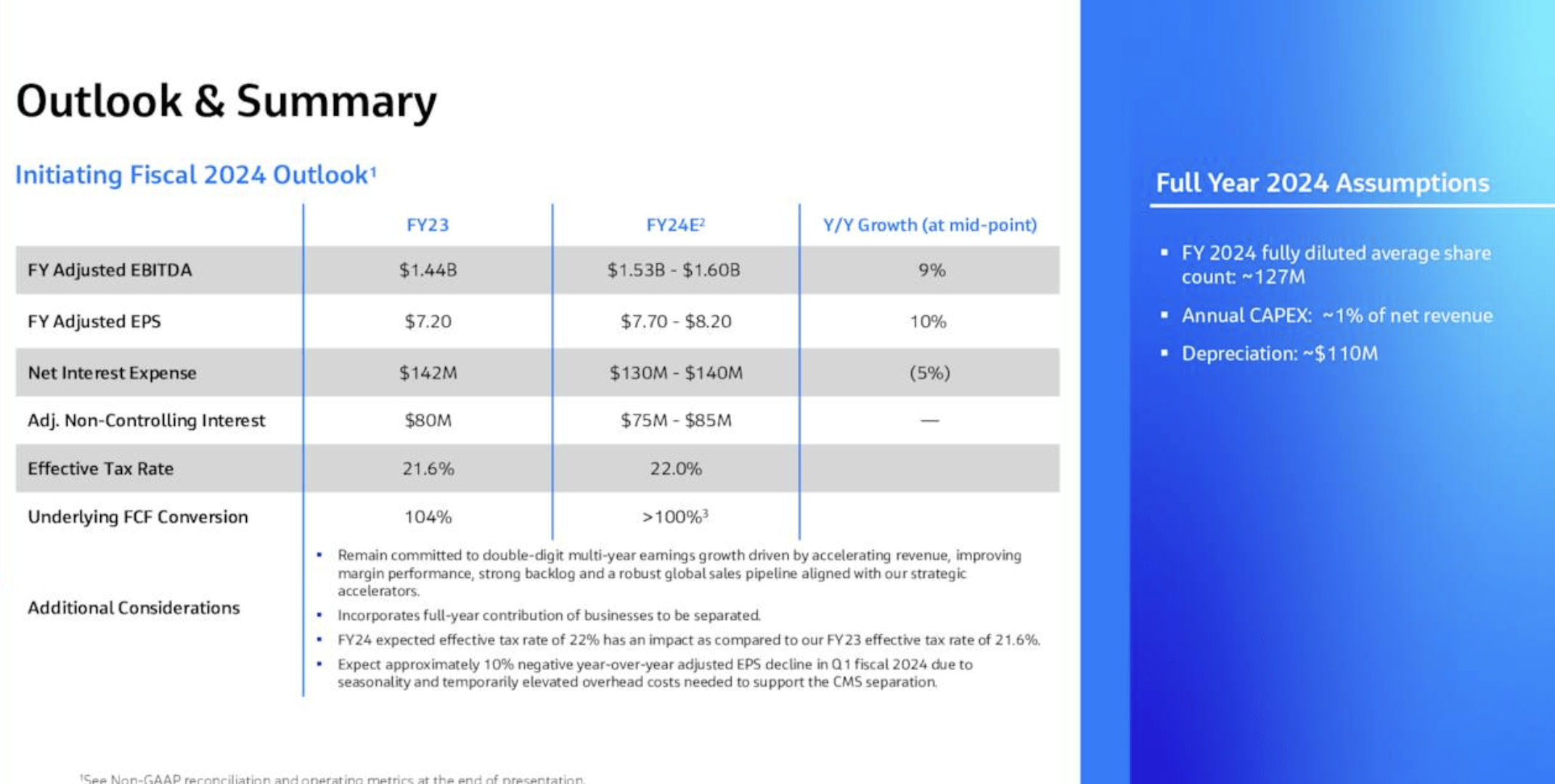

In terms of the FY24 outlook, the management seems to be quite excited about the upcoming year. The company expects to make around $8 a share in adjusted earnings, which is a decent 10% growth over this year. The company will experience some overhead costs in relation to the CMS separation, but even with this in mind, the numbers are looking great. I am also happy to see that its annual interest expense will be coming down in FY24, which should bode well for the bottom line.

Investor Slides

The risks remain the same as I mentioned in my first article, but a brief summary is that the spin-off may not create a lot of value for the shareholders because about 50% of the spin-offs create little to no value to existing shareholders, so basically a coin toss, but I feel that two separate entities will succeed as both should become more streamlined in the process.

I am very excited about the company’s transition over the next year. I mentioned in my article on KBR, that I am not a fan of government contracts as the main revenue generator, and I know that CMS didn’t make up most of the company’s revenues, but it was still a big chunk (around 28% of total revenues), so now that the company will get rid of this weight on margins, I am going to look forward to seeing how margins are going to develop over the next 2 to 3 years.

As for my recommendation, it remains a buy at this time because I am excited about the company’s potential going forward. My previous intrinsic value of the company hasn't changed because the numbers that the company provided thus far haven't altered my model, therefore an intrinsic value of $162.86 still stands, meaning Jacobs is still trading below its fair value.