Jiojio/Moment via Getty Images

Jiojio/Moment via Getty Images

The John Hancock Premium Dividend Fund (NYSE:PDT) is a closed-end fund that can be purchased by investors who are looking to receive a sizable amount of income from the assets in their portfolios. Unlike most income-focused funds though, this one does not focus its investments solely on fixed-income securities, so it is not necessary to sacrifice some upside potential in order to achieve this high level of income. This is because the John Hancock Premium Dividend Fund invests in both fixed-income securities and common stocks. The latter provides a certain amount of protection against inflation as well as provides the potential to profit from economic growth. Unfortunately, the presence of the common stocks in the fund's portfolio also reduces its income compared to what a pure fixed-income fund would have. After all, common stocks have substantially lower dividend yields than preferred stocks or bonds. We can see this quite simply in the fact that the S&P 500 Index ETF (SPY) only has a trailing yield of 1.33% at its current price. Even the supposedly high-yielding utility sector (IDU) only yields 2.84% at today's level. All of these are well below the 5% to 5.50% that can be obtained from a good money market fund, let alone the higher yields that are available in the fixed-income space. Despite the substantial presence of common stocks in the fund's portfolio though, the John Hancock Premium Dividend Fund still boasts a 9.10% yield today. That should be enough to satisfy any investor who is seeking a very high level of income.

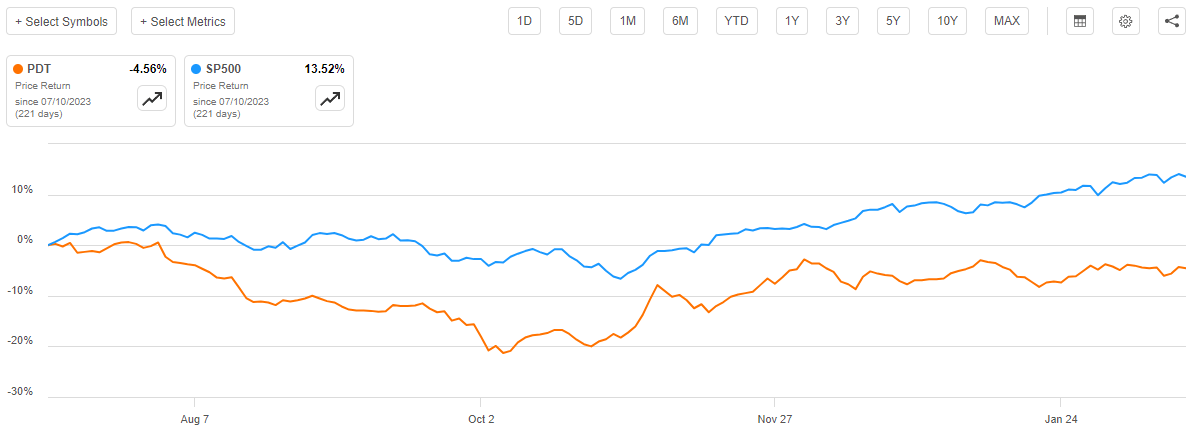

As regular readers can no doubt remember, we last discussed the John Hancock Premium Dividend Fund in mid-July 2023. It would be an understatement to say that this was a very different market environment than we have today. After all, during the summer of 2023, the market was digesting the very real possibility that high interest rates would be with us for quite some time and investors were generally pulling money out of both common stocks and fixed-income securities. When interest rates are very high, it is possible to obtain an acceptable return on investment without taking on much risk simply by parking your money in a money market fund. However, starting in mid-October, both the stock and bond markets rallied as investors began to expect that the Federal Reserve would shortly pivot and start reducing interest rates. As such, we can expect that the shares of the John Hancock Premium Dividend Fund would have exhibited some weakness for the first few months following the publication of that article and then shot upward in price. We do indeed see this, although this fund has not benefited from the recent strength in the market as many other assets. The fund's shares are down 4.56% since the date that the previous article was published, which is much worse than the 13.52% gain of the S&P 500 Index (SP500):

Seeking Alpha

This is undoubtedly going to disappoint most investors, including those whose primary objective is to earn a high level of income and not necessarily maximize their capital gains. After all, nobody wants to lose money regardless of their objectives. More importantly, though, the fact that this fund did not benefit from the market strength since the start of November reflects somewhat poorly on it.

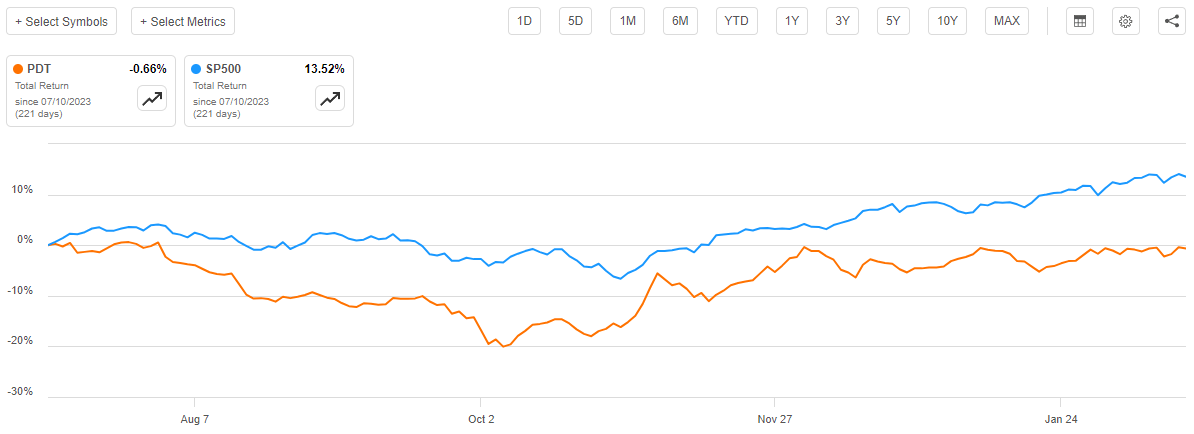

However, as I have pointed out in various previous articles, closed-end funds typically pay out most to all of their investment profits to the shareholders in the form of distributions. These funds are basically attempting to maintain a stable net asset value over time while still allowing their shareholders to benefit from investment profits. As such, we want to take the distributions paid by the fund when analyzing its performance. When we do that, we see that investors in this fund suffered a 0.66% loss since the date that the previous article was published. This is obviously still much worse than the S&P 500 Index managed to deliver:

Seeking Alpha

This is still not especially appealing for most investors, but at least basically breaking even is better than outright losing money. However, the fund is still unlikely to be as appealing as some other options that have delivered much stronger positive total returns.

With that said, the past performance of a closed-end fund or other asset is no guarantee of its future performance. As such, we should still investigate it in order to determine if purchasing some of its shares might make sense today.

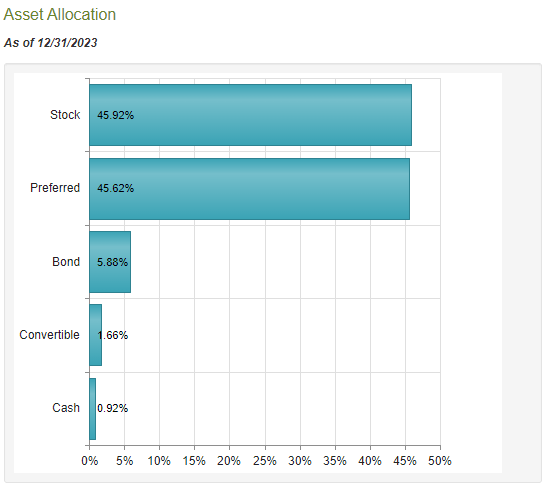

According to the fund's website, the John Hancock Premium Dividend Fund has the primary objective of providing its investors with a high level of current income. This does not really make sense considering that the fund invests in a combination of common and preferred stocks. Indeed, CEF Connect puts the fund's assets at almost an even split between the two asset types, although it is weighted towards fixed-income securities when bonds are included in the mix:

CEF Connect

As I have noted in various past articles, preferred stocks and bonds are income vehicles. They have no net capital gains over their lifetime because investors purchase them at face value and the face value is returned at maturity. Preferred stocks do not, strictly speaking, have a maturity date but they generally do not benefit from the growth and prosperity of the issuing company, so the capital gains potential is quite limited. As such, the current income objective would make sense if the fund only consisted of these securities. However, it does not make sense given the 45.92% allocation to common equities. This is because common equities are by their nature total return vehicles that are purchased by investors who are seeking both income via dividends and distributions, as well as those who are seeking to benefit from capital gains as the issuing company grows and prospers. Common equities are also not particularly good income investments due to the low yields of most equities (except for some things in the energy and telecommunications sectors). As these securities account for a non-negligible proportion of the fund's portfolio, a total return objective would make more sense here.

Of course, closed-end funds are able to realize capital gains and then distribute that money to their investors. This can be considered income to a certain degree, although it is nowhere near as reliable as would be provided by dividends or coupon payments on bonds. Nevertheless, there are some funds that invest in very low-yielding securities but still pay out fairly large yields to their shareholders. For example, some of the Eaton Vance closed-end equity funds do this. As money is fungible, it does not, strictly speaking, matter whether it comes from capital gains or dividends as far as paying your bills goes. The stock market tends to be somewhat volatile with respect to the returns that it delivers, so depending on capital gains is a much less reliable way to earn money as the fund's managers have no way of knowing whether or not they will earn enough to cover the distribution in a given year.

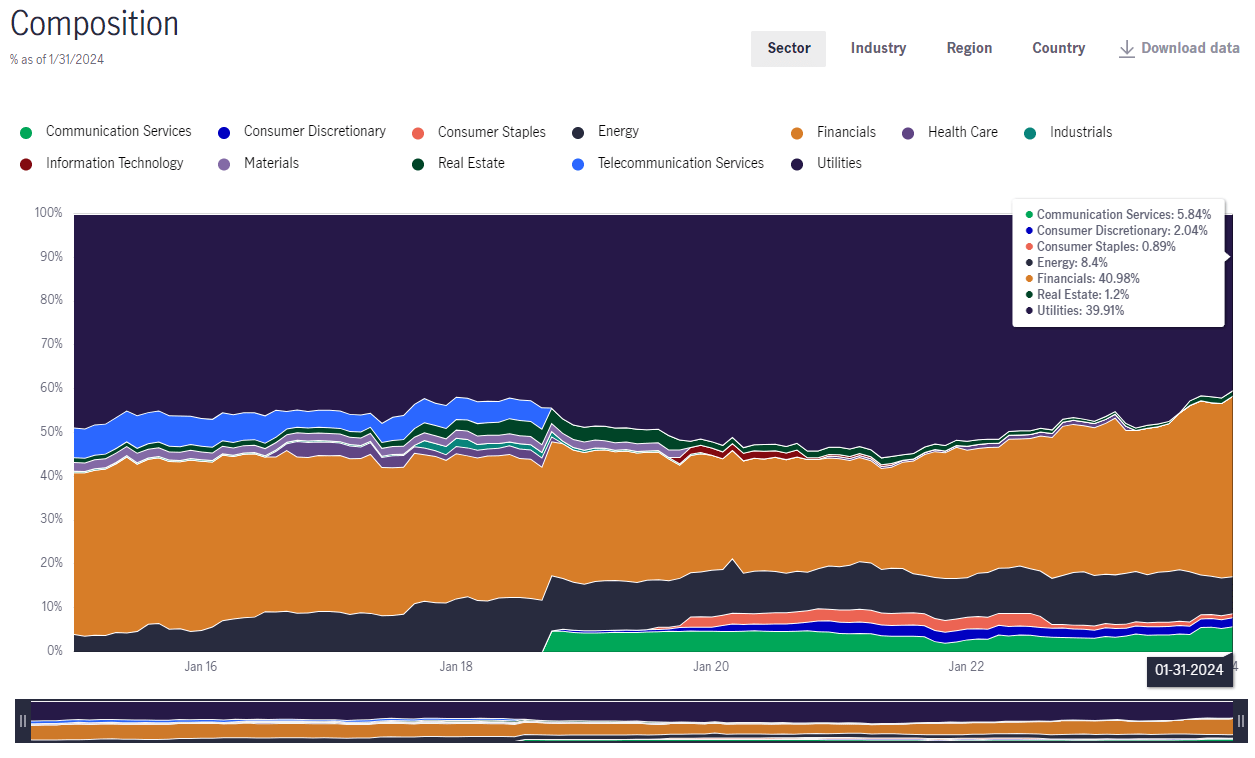

In my previous article on the John Hancock Premium Dividend Fund, I pointed out that the fund tends to maintain a high weighting towards the utility sector. This is still the case, as utilities currently account for 39.91% of the fund's assets:

John Hancock Funds

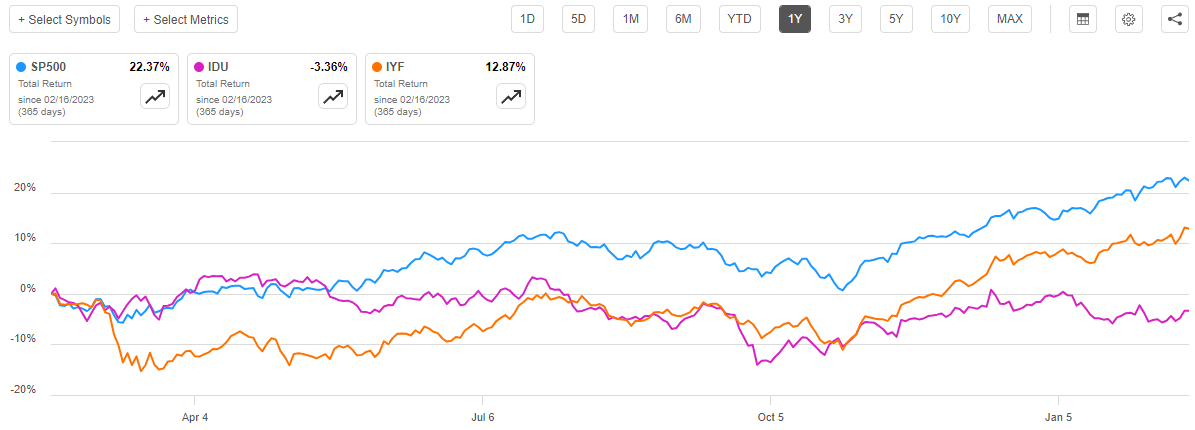

This is a much smaller weighting than the 47.43% that the fund had allocated to the utility sector when we last discussed it in mid-July. This is an apparent continuation of the trend that we have been seeing over the past year or two. At the start of 2021, the fund had 53.16% of its assets invested in the utility sector. It has been gradually decreasing its allocation to that sector since that time, bringing it down to today's 39.91%. The current level is actually the lowest level of utility sector exposure that this fund has had over the past ten years. At least some of the recent decline in the utility sector exposure could be due to the very disappointing performance of the sector relative to the rest of the market in recent months. As we can see in the above chart, the financials sector also accounts for a substantial percentage of the fund's portfolio today and this weighting has been increasing while the utility sector weighting has been decreasing. This chart shows the price performance of the iShares U.S. Utilities ETF against the iShares U.S. Financials ETF (IYF):

Seeking Alpha

As we can see, the financials sector has substantially outperformed the utility sector over the past year. In fact, the utility sector was the worst-performing market sector in 2023 and it was one of the only ones to see its sector index decline over the year. Thus, if the John Hancock Premium Dividend Fund simply used a buy-and-hold strategy over the past year, we would expect that the financial sector weighting would increase at the expense of the utility sector. The fund's strategy over the past year has not been a pure buy-and-hold strategy, but it only had a 26.00% annual turnover for its most recent fiscal year, so the fund is clearly not doing much in the way of trading. Thus, at least some of the changes that we see in the fund's sector weightings could be caused by the poor recent performance of utilities. The fund's substantial weighting to the utility sector could also be responsible for some of the fund's own lagging performance relative to the market.

The fund's website specifically states that the John Hancock Premium Dividend Fund focuses its attention on investing in dividend-paying common and preferred stocks. The fact that the utilities and financials sectors account for much of the fund's overall portfolio fit pretty well into this focus as these are two of the highest-yielding market sectors right now:

Sector ETF | Current Yield |

iShares U.S. Utilities ETF | 2.84% |

iShares U.S. Financials ETF | 1.60% |

iShares U.S. Energy ETF (IYE) | 2.94% |

iShares U.S. Healthcare ETF (IYH) | 1.11% |

iShares U.S. Consumer Staples ETF (IYK) | 2.72% |

iShares U.S. Consumer Discretionary ETF (IYC) | 0.65% |

iShares U.S. Technology ETF (IYW) | 0.25% |

iShares U.S. Real Estate ETF (IYR) | 2.89% |

iShares U.S. Telecommunications ETF (IYZ) | 2.36% |

Admittedly, the fund's portfolio might be able to generate a bit higher income if it were to trade out some of its financial sector exposure for energy or consumer staples, but the financial sector still has a higher yield than the S&P 500 Index. It is very rare to see much energy exposure in any equity closed-end fund, with the notable exception of energy-sector-specific funds, despite the sector having the highest yields available in the market. This could be due to the higher volatility of that sector relative to most other segments of the market, although it is also possible that environmental, social, and governance policies that some fund houses employ could be contributing to the lack of representation. We do still see that energy is the third-largest sector represented in the John Hancock Premium Dividend Fund at 8.4% of total assets. The other interesting thing that we see with this fund is that consumer staples only account for 0.89% of total assets despite having very high yields. The fund could probably improve its diversification if it were to switch some of the financials for consumer staples, as well as increase its income. Consumer staples are also arguably less vulnerable to macroeconomic shocks than financials, so that would also be a benefit.

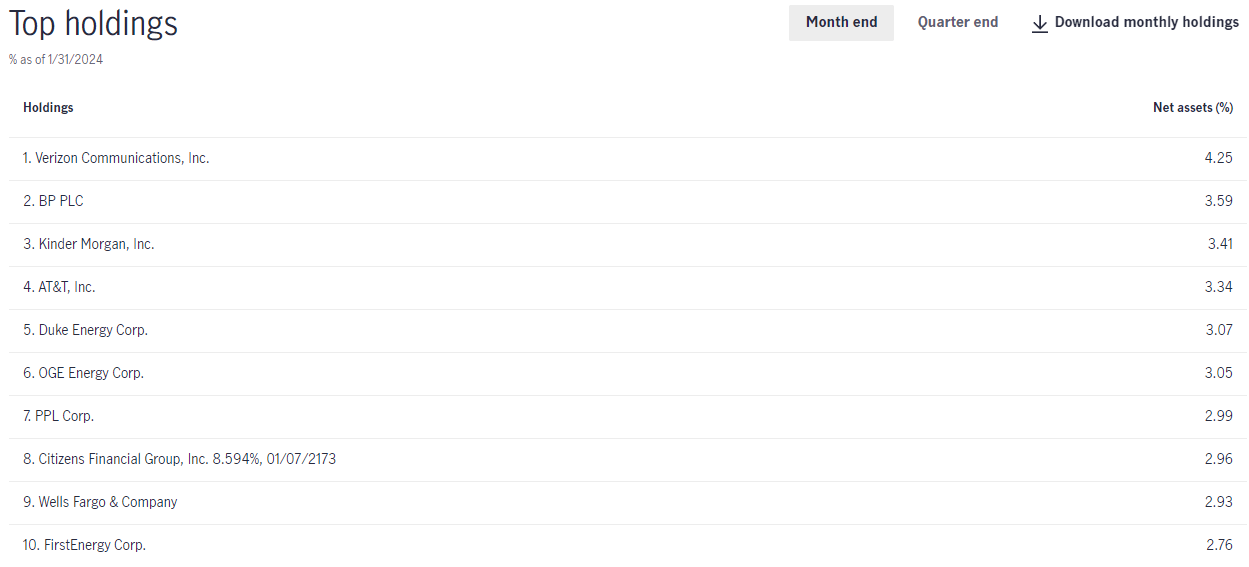

With all that said, the fund's largest positions are more diversified than might be expected. Here they are:

John Hancock Funds

Despite the fund's very low turnover ratio, we can see a number of changes here since the last time that we discussed the John Hancock Premium Dividend Fund. There are four assets that were removed from the largest positions list: The Williams Companies (WMB), NiSource Inc. (NI), Alliant Energy (LNT), and a Bank of America (BAC) preferred stock issue. The newly added assets are Verizon Communications (VZ), Kinder Morgan (KMI), AT&T (T), and the Citizens Financial Group (CFG) preferred stock issue. The interesting thing about these changes is that two utilities were replaced with two telecommunications companies. The remainder of the major changes were simply the replacement of one asset with a very similar one, so the fund's sector exposure and fundamentals were not really changed too much by the other changes. Overall, it is very difficult to argue with a few of these changes, particularly the replacement of the two utilities. After all, both Verizon Communications and AT&T have much higher yields than either of the two removed utilities and both of these companies enjoy similar cash flow stability as very few people are going to be willing to give up their cellular phones nowadays. As I have noted in numerous previous articles, cash flow stability is something that we generally appreciate as dividend investors due to the support that it provides to a company's dividend and its ability to sustain it over extended periods.

As is the case with most closed-end funds, the John Hancock Premium Dividend Fund employs leverage as a method of boosting the effective yield and total return provided by its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that borrowed money to purchase common stock and fixed-income securities. As long as the purchased securities deliver higher total returns than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective returns of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that leverage is not nearly as effective at boosting returns with interest rates at 5% to 6% as it was at 0%, so the benefit that the fund receives from this strategy is going to be much less than it was a few years ago.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. Due to this, it is important that we ensure that the fund is not using too much leverage because that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for that reason.

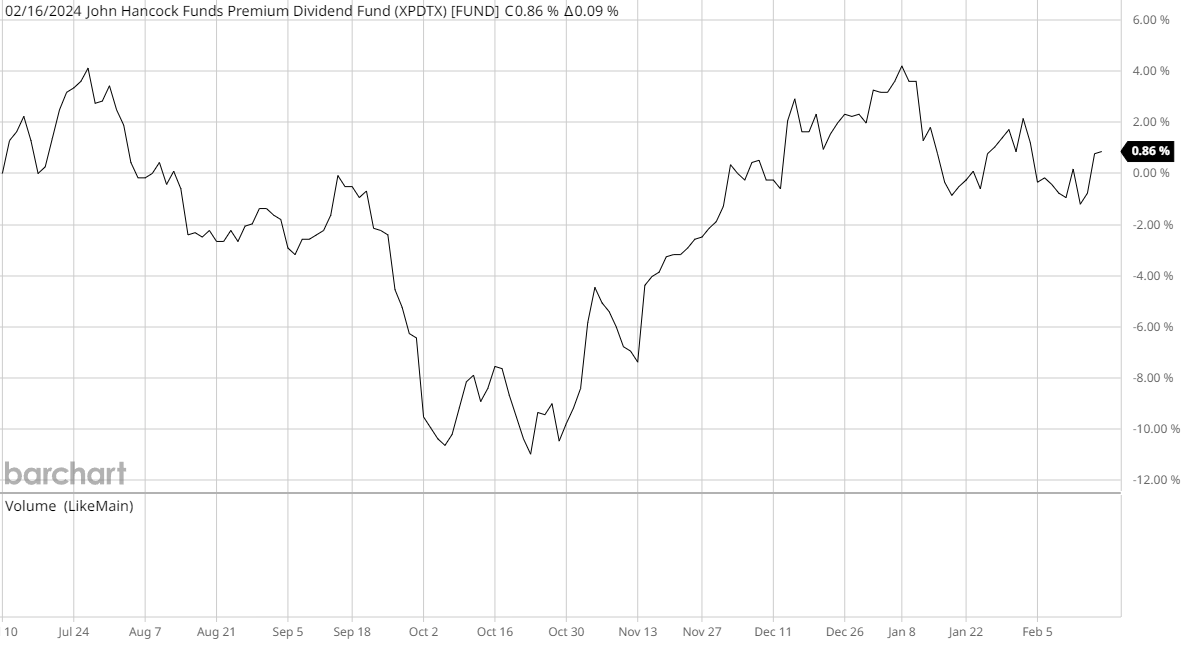

As of the time of writing, the John Hancock Premium Dividend Fund has leveraged assets comprising 39.27% of its assets. This is slightly better than the 39.40% leverage that the fund had the last time that we discussed it, which is actually a bit surprising considering that the share price is down 4.56% over the period.

However, the decline in leverage can be easily explained by the fact that the fund's net asset value is actually up since we discussed the fund on July 10, 2023. As we can see here, the fund's net asset value has increased by 0.86% since the last time that we discussed it:

Barchart

This is obviously a very different performance to the fund's share price over the same period. However, it does explain why the fund's leverage ratio decreased over the past seven months. After all, if we assume that the leverage remained static then it will now account for a smaller percentage of a larger portfolio. This appears to be exactly what happened as the total amount of outstanding borrowings is roughly the same as it was seven months ago.

As mentioned in the quote above, I ordinarily prefer that a fund's leverage be under a third as a percentage of its assets in order to reduce the risks involved with respect to that leverage. After all, leverage adds volatility to the share price, and it could even force a fund to realize losses in the event of a market decline. Over the past five years, we have seen a number of funds blow up their portfolios due to their use of leverage. The John Hancock Premium Dividend Fund is unfortunately well above that one-third level and as such it is much higher than we really want to see. While it is true that the fund's fixed-income investments allow it to carry more leverage than most equity closed-end funds, the fact that roughly half of the fund's portfolio is invested in common equities means that it should still be careful with leverage.

Overall, I would feel more comfortable with a lower level of leverage than this fund currently employs.

As mentioned earlier in this article, the primary objective of the John Hancock Premium Dividend Fund is to provide its shareholders with a very high level of current income. In pursuance of this objective, the fund invests its assets in a combination of dividend-paying common stocks and preferred stocks. Each of these securities provides a significant percentage of their total return in the form of direct payments to the fund, although the common stocks will also provide capital gains. The fund combines all of the dividend payments that it receives with any realized gains into a pool of money. It then takes things a bit further and borrows money to collect dividends and capital gains from more securities than it could afford using only its own equity capital. In most market environments, this will boost the effective returns that the fund can add to its pool of distributable money. The fund then pays out all of the money in the pool to its shareholders after subtracting its own expenses. We might expect that this would result in the fund's shares having a very high yield when we consider the impact of both the leverage and the capital gains.

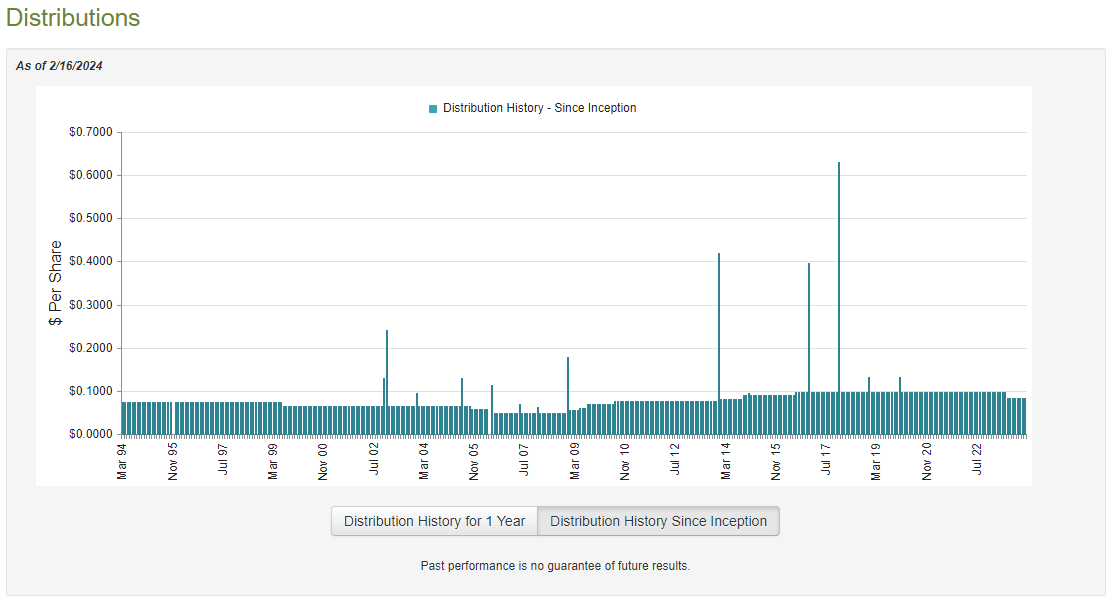

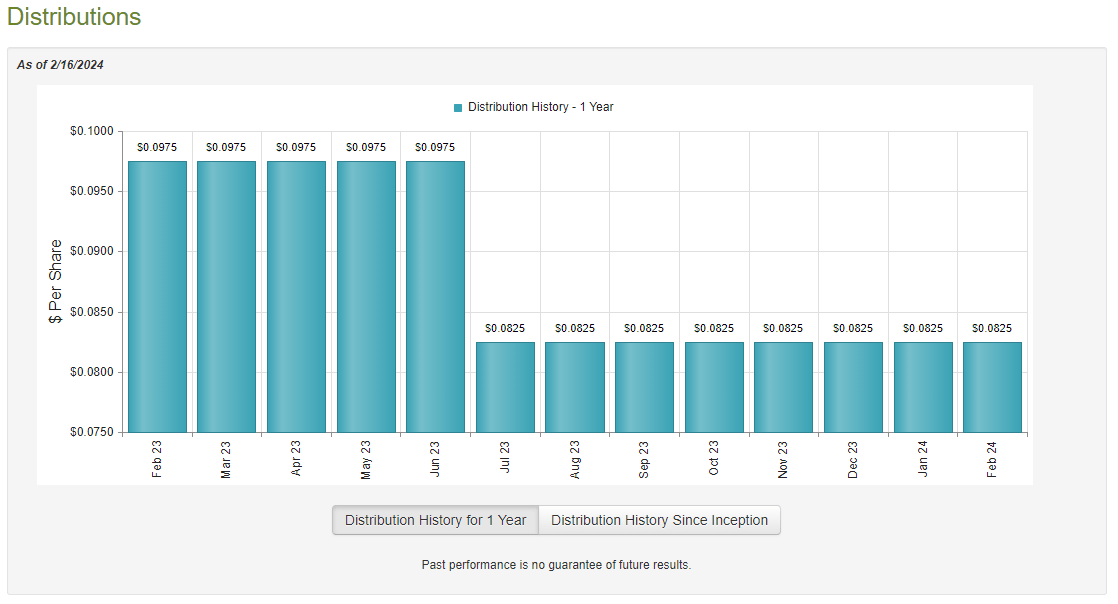

This is certainly the case, as the John Hancock Premium Dividend Fund pays a monthly distribution of $0.0825 per share ($0.99 per share annually). This gives the fund a 9.10% yield at the current share price. Historically, the fund has a pretty good track record for distribution consistency as we can see here:

CEF Connect

As we can see here, the fund has generally been growing its distribution since 2006. It has not delivered annual increases, though. There are very few closed-end funds that have ever managed to achieve an annual distribution increase due to the volatility of asset prices. This one had one of the better track records among any closed-end fund until last year when it cut the distribution in July:

CEF Connect

This recent cut will almost certainly reduce the fund's appeal to those investors who are seeking a safe and consistent source of income to finance their lifestyles or even just pay their bills. The current distribution is lower than the one that the fund paid in 2015, which almost certainly further reduces its appeal considering that prices of most goods and services were much lower in 2015 than they are today. However, most closed-end funds have had to cut their distributions over the past two years as the high level of inflation and changing monetary environment have wreaked havoc in the markets and that has caused many of these funds to take some realized losses. It is necessary to reduce a distribution in such a situation because a fund should never unnecessarily deplete its net asset value. After all, the lower the fund's net asset value, the higher the return that is needed to maintain a specified distribution, and the harder it becomes to consistently achieve.

The fund's distribution history is not necessarily the most important thing for an investor who is considering purchasing this fund today. After all, anyone who purchases the fund today will receive the current distribution at the current yield. This individual will not be adversely affected by events that occurred prior to the purchase date. As such, we should investigate the fund's ability to sustain its current distribution going forward.

Fortunately, we have a relatively recent document that we can consult for the purposes of our analysis. As of the time of writing, the most recent financial report for the John Hancock Premium Dividend Fund corresponds to the full-year period that ended on October 31, 2023. This is a newer report than the one that we had available the last time that we discussed the fund, which is quite nice to see. After all, this fund will give us a good idea of how well it navigated the challenging market environment that occurred in the summer of 2023. As mentioned in the introduction, this time period was characterized by rising interest rates and generally falling common stock and fixed-income prices. As such, it almost certainly had an adverse effect on the fund's portfolio and resulted in unrealized and possibly realized losses. This report will give us an idea of how well it handled this situation which was not available the last time that we discussed the fund.

During the full-year period, the John Hancock Premium Dividend Income Fund received $35,279,079 in dividends and $18,351,439 in interest from the assets in its portfolio. We need to subtract the money that the fund had to pay in foreign withholding taxes, which gives us a total investment income of $53,380,228 over the full-year period. The fund paid its expenses out of this amount, which left it with $23,361,899 available for shareholders. As might be expected, this was nowhere near enough to cover the distributions that the fund paid out during the period. The John Hancock Premium Dividend Fund made distributions totaling $54,565,231 over the full-year period so obviously, its payout exceeded the net investment income by quite a lot. At first glance, this could be concerning as the fund's net investment income was clearly nowhere near sufficient to fully cover its distributions.

However, the fund does have other methods through which it can obtain the money that is necessary to cover the distribution. For example, it might be able to realize capital gains by selling appreciated securities. Realized capital gains are not considered to be investment income for tax or accounting purposes but they clearly represent money entering into a fund that can be paid out. Unfortunately, the fund had mixed results at earning money from these alternative sources. Over the full-year period, the John Hancock Premium Dividend Fund reported net realized gains of $28,931,234 but these were more than offset by $96,963,351 in net unrealized losses. Overall, the fund's net assets declined by $98,046,955 after accounting for all inflows and outflows over the period. This is concerning as it strongly implies that the fund distributed far more than it could afford during the period.

However, the fund's net investment income plus net realized gains totaled $52,293,133 over the period. This was not enough to cover the $54,565,231 that was paid out in distributions, but it did manage to get pretty close. The reason for the large decrease in net asset value was due to the net unrealized losses, which we can ignore for some purposes. After all, net unrealized losses might be erased by a market rally, so as long as the fund is not realizing those losses, they do not represent destructive activity.

Overall, this fund managed to do better than I really expected considering its financial and utility-heavy portfolio. Investors may be able to take some comfort in this. As the distribution is lower today than it was over much of the time period that was covered by this report, it does seem likely that the fund can probably sustain the current distribution.

As of February 15, 2024 (the most recent date for which data is currently available), the John Hancock Premium Dividend Fund has a net asset value of $11.74 per share but the shares trade for $10.88 each. This gives the fund's shares a 7.33% discount on net asset value at the current price. This is relatively in line with the 7.66% discount that the shares have had on average over the past month. Thus, today's price looks pretty reasonable if you are interested in adding this fund to your portfolio.

In conclusion, the John Hancock Premium Dividend Fund is a blended closed-end fund that has been performing much better than the share price would suggest. In fact, the fund's net asset value has actually gone up over the past seven months despite the decline in the share price. It also appears that this fund is probably going to be able to sustain its current 9.10% yield going forward. It may be worth picking up some shares today.