Michael M. Santiago

Michael M. Santiago

The Goldman Sachs MarketBeta US Equity ETF (BATS:GSUS) is a $1.8 billion, tech-weighted, large-cap, passive fund. It’s top-heavy, with a 30% allocation to tech, with a similar top-ten concentration of 32% of the portfolio. GSUS being a passive ETF, you’ll see a very low annual turnover - 3%, currently - but it does come with a relatively high expense ratio of 0.07%. Although the sector median for ETFs sits at 7x higher at 0.49%, I still say relatively expensive because there are cheaper beta-driven ETF options available to investors, among which the one I most like is the JPMorgan BetaBuilders U.S. Equity ETF (BBUS). I see GS’s offering as a smaller and slightly younger version, and the analysis below points to a Hold at this time.

GSUS seeks to give investors exposure to about 85% of the domestic equity market in the United States. Before deducting fees and expenses, it aims to deliver returns similar to its benchmark. The benchmark has a similar composition, but the ETF uses GS’s smart beta strategies to weight them differently. Rather than the typical market cap weighting approach of the benchmark, GSUS focuses on minimizing volatility risk with its proprietary MarketBeta strategy before applying a float-adjusted market cap weighting.

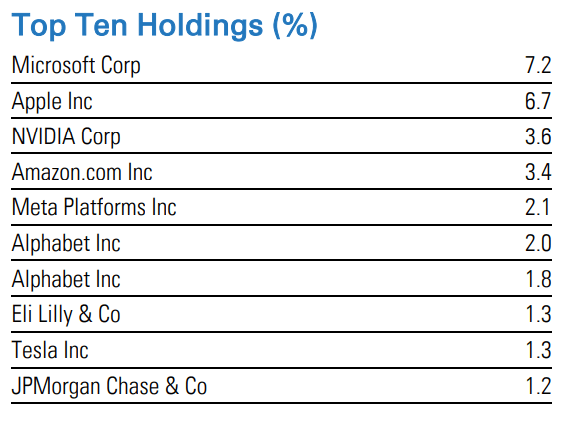

Since the ETF gives you broad exposure to U.S. large and mid-cap equities, you’re going to see the Magnificent 7 in all their glory in the top ten holdings. This ETF is designed to be a core portfolio holding that you can further diversify.

GSUS Fact Card - 12/31/2023

The advantage of such a broad-market ETF is that you’re not sacrificing diversity, and you’re getting more exposure to factors such as positive momentum, higher levels of return on equity, and profitability. The downside is that you’re not in on the dividend yields from the underlying assets; more precisely, the distributions enjoyed by shareholders might not reflect the true yield from the asset group.

That’s one of the negative features I see in this product. For instance, you get practically zero exposure to Microsoft’s (MSFT) handsome 10% dividend growth rate, which you’d have with a direct holding. Agreed, this is meant to represent a strong core portfolio holding, but that also means you’ll need to balance it with companies that might not be as profitable or have as much momentum but offer high and sustainable dividends.

On that front, you can consider looking to the BDC market where double-digit yields aren’t unusual. Even the broader VanEck BDC Income ETF (BIZD) would be a good opportunity, with its +10% yield. However, it’s important to not be alarmed when you look at the high expense ratio of +11%. The bulk of that is in the form of indirect expenses, so they don’t eat into NAV. The right way to look at BDC ETF expense ratios is the direct expenses, which in this case is 0.42%. That’s still relatively expensive, but it’s important to understand how AFFEs or Acquired Fund Fees are factored into the gross expense ratio.

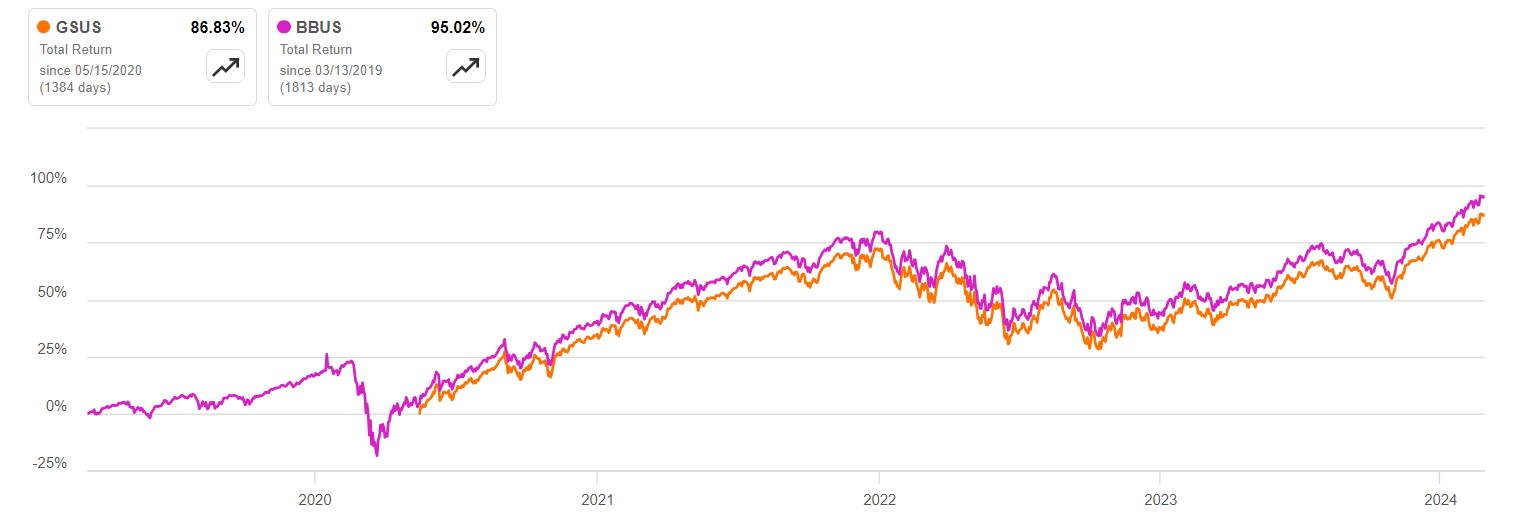

For GSUS, the expense ratio was initially set at 0.09%, with a management fee waiver bringing it down to 0.07%. As I mentioned, it’s still a little expensive for a passive fund, which is why I’d recommend BBUS as a viable alternative with a 0.02% expense ratio and a slightly better dividend yield than GSUS. I’ve commented on this ETF in a little more detail at the end.

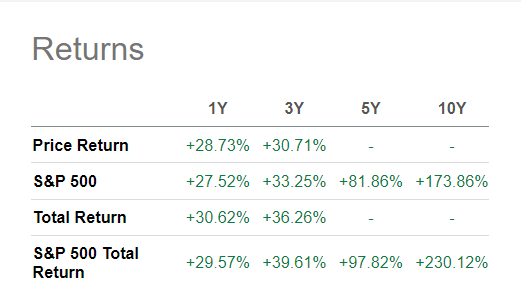

As a broad market ETF with a slight beta advantage, you’re not likely to see phenomenal outperformance with GSUS. It is meant to be a core portfolio holding that gives you exposure to the (relatively) least volatile large and mid-cap companies comprising the broader market. However, the returns have been fairly consistent and in line with the price and total return of the broader market.

GSUS Return

What’s important to note about GSUS and, indeed, most broad-market ETFs like the SPY is that the current market mix is heavily skewed towards the Magnificent 7. They’re practically carrying the market as tech continues to rally strongly. While many investors are hoping the concentration will broaden out eventually, that doesn’t seem like it’s going to happen in a hurry. In 2023 alone, the Mag 7 collectively returned 107% against the MSCI USA Index’s comparatively meager 27%. I’ve discussed this in more depth in my article on the Avantis International Equity ETF (AVDE), which you can read here.

That’s also why we’re not seeing much alpha with GSUS. This will eventually change, of course, but that would require a much broader rally from the remaining constituents of GSUS’s benchmark index.

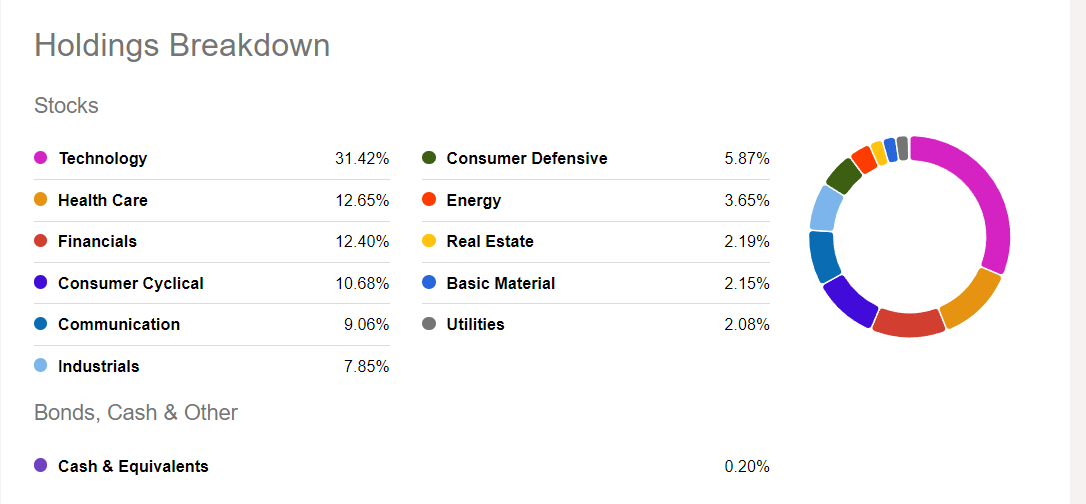

GSUS Holdings Breakdown

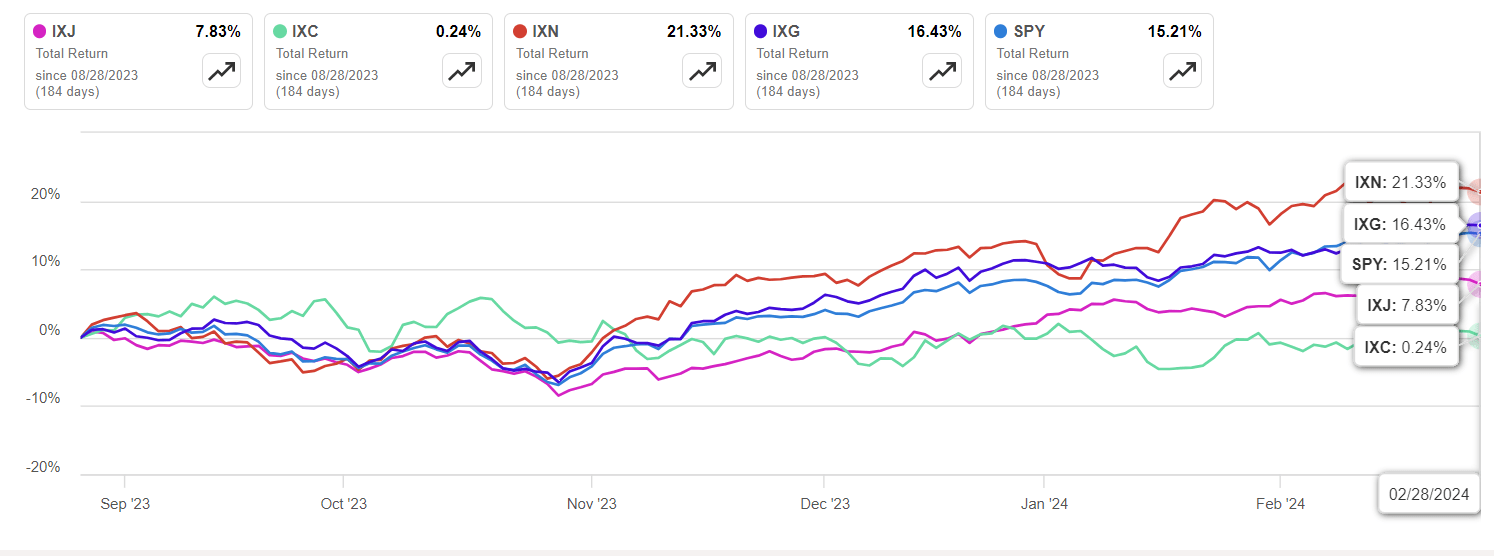

A general uplifting in healthcare and financials could alter the landscape, because of their relatively high weightings; but, for now, the AI-powered rally supporting the Mag 7 doesn’t look like it’s about to run out of steam any time soon, and healthcare doesn’t seem to be in a hurry to get anywhere fast. The financials sector, however, is showing a tremendous amount of resilience considering the state of developed global economies, and you can see this is in IXG’s one-year return below, bested only by the tech-focused IXN.

SA

So, how is an investor supposed to generate alpha when the overall market itself is rallying hard behind tech?

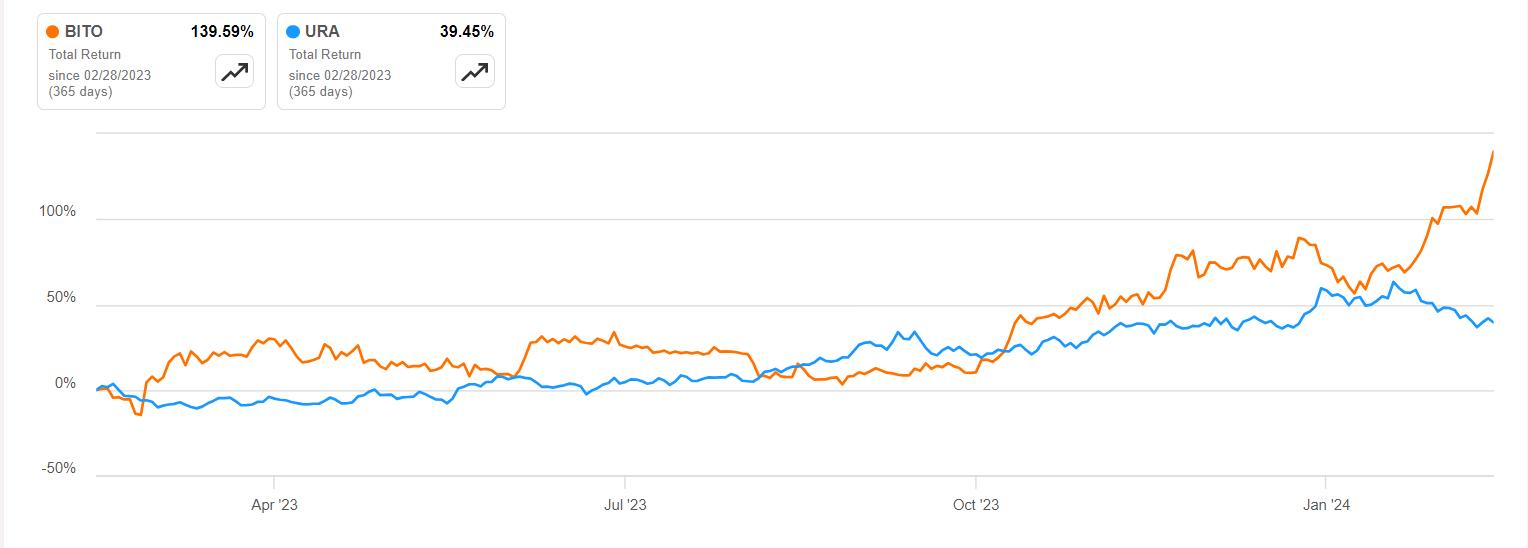

The answer is relatively simple, in my opinion. Alongside a core holding of GSUS, which will continue to mirror the performance of SP500, what you might consider doing is to complement that with high-yield ETFs like BIZD (mentioned earlier), the ProShares Bitcoin Strategy ETF (BITO) with its forward yield of nearly 16%, or the Global X Uranium ETF (URA) with a forward yield of 12%.

SA

Some of these ETFs also exhibit strong capital appreciation alongside their high yields, but they do come with heftier expense ratios - 0.69% for URA and 0.95% for BITO, for instance. The Seeking Alpha ETF Screener is an excellent tool for this purpose as it allows you to apply advanced filters to help you identify the best opportunities that are also in line with your overall investment strategy. For example, if you have an AUM cut-off below which you’d rather not go because of liquidity considerations, you can filter for that; if you’re looking for exposure to a particular sector, that option is available as well. Similarly, you can look for specific top-ten holding concentrations, asset turnover rates, expense ratios, and so on. I think it’s a great tool for ETF investors who don’t follow ETF-specific developments on a regular basis.

SA

I’d also like to discuss BBUS as a good alternative to GSUS, as I mentioned earlier. The expense ratio is lower, and it’s shown very similar total returns over the past three to five years. Any variance is primarily due to the nuances in their respective beta strategies, but the performance is quite comparable. The only difference is BBUS’s two-thirds greater asset base at a shade under $3 billion against GSUS’ $1.8 billion, and the greater liquidity if you’re after a sizeable position. The yield is slightly better on this as well.

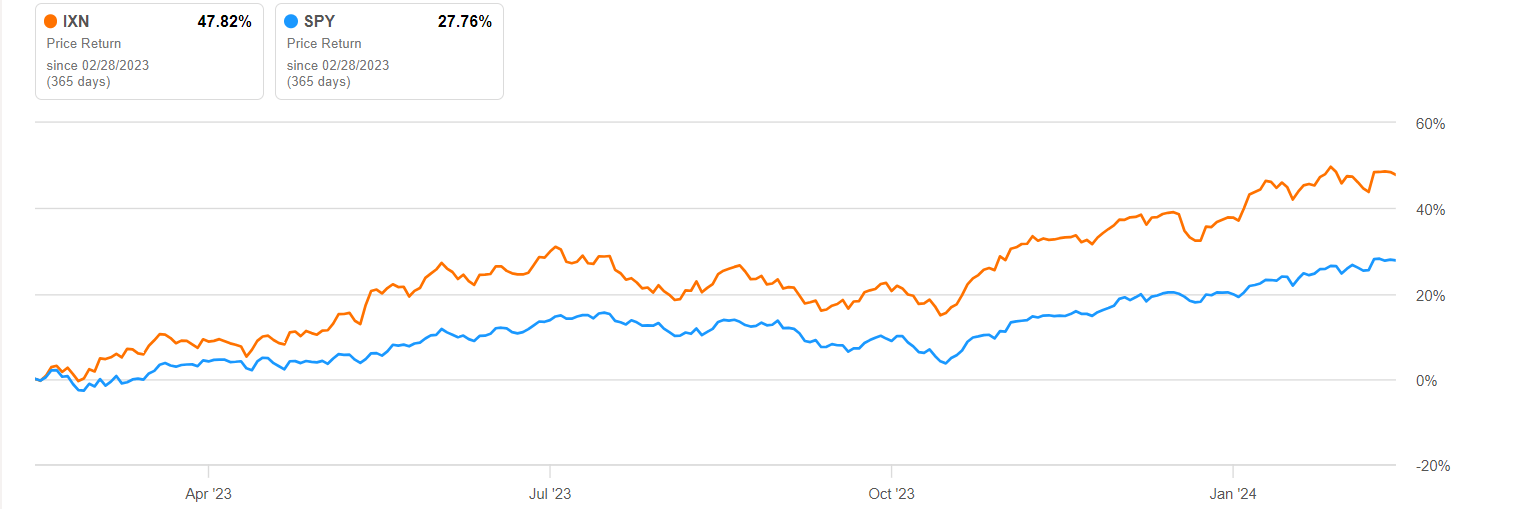

Yet another alternative to generate alpha in the current market environment is to go all out on tech with the iShares Global Tech ETF (IXN) (discussed briefly above) around a BBUS or GSUS core holding - to really squeeze out whatever alpha the tech sector can provide. You won’t get exposure to the entire Mag 7 line-up, with Alphabet, Meta, and Tesla missing from the top ten holdings, and the ETF’s expense ratio is 0.41%; however, IXN has been on a tear with a one-year price return of 49% against the broad-market SPY return of 28%. I haven’t researched better alternatives to take advantage of the tech rally (other than my coverage of the leveraged single-stock ETF - (NVDX)) but will explore that in a subsequent article.

SA

As for GSUS itself, I recommend a Hold while the market is skewed heavily toward tech and the Mag 7. For now, it’s a good core holding that will give you a base that keeps pace with the current market momentum. Using it as your foundation, you can then build an alpha-generating portfolio with some of the ETFs I mentioned. Naturally, I don’t expect you to consider this as formal investment advice, and I urge you to do your due diligence before investing in anything, but I hope this analysis has provided you with a good starting point.