imaginima

imaginima

The BlackRock Energy & Resources Trust (NYSE:BGR) is a sector-specific closed-end fund, or CEF, that is designed for those investors who want exposure to the traditional energy sector along with a high level of income. The fund manages to deliver on this promise fairly well, as its 6.14% current yield is quite a bit higher than that of most energy index funds:

Fund | Current Yield |

BlackRock Energy and Resources Trust | 6.14% |

iShares U.S. Energy ETF (IYE) | 2.80% |

iShares Global Energy ETF (IXC) | 3.17% |

However, the fund’s current yield cannot really compare to most energy partnerships or funds that invest in such partnerships. For example, the Alerian MLP Index ETF (AMLP) currently yields 7.53%. However, this fund invests primarily in upstream exploration and production companies that normally have lower yields than master limited partnerships, and so it is one of the higher-yielding ways to get exposure to those particular companies.

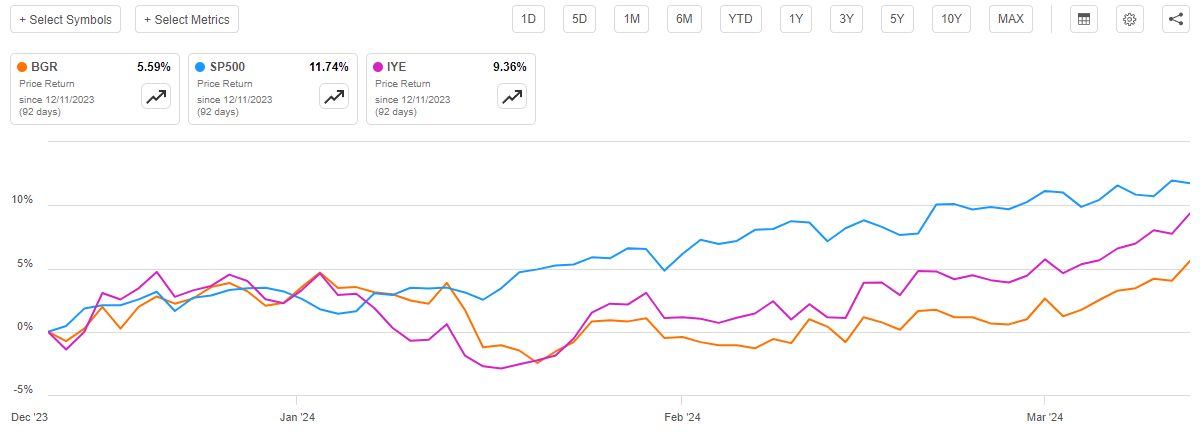

As regular readers can likely remember, we previously discussed the BlackRock Energy and Resources Trust in the middle of December 2023. The fund’s performance since that time has not been especially impressive. It did manage to deliver a 5.59% share price gain, but this is nowhere near as good as the 9.36% gain of the iShares U.S. Energy ETF or the 11.74% gain of the S&P 500 Index (SP500):

Seeking Alpha

In isolation, this is probably not going to be particularly attractive in the eyes of anyone who is considering purchasing shares of this fund. However, it is what we generally expect from this fund for a few reasons. First of all, the fund’s strategy will generally result in it sacrificing a certain amount of upside potential in exchange for a higher yield. Secondly, the fund pays out its capital gains to its investors instead of retaining them as an index fund does.

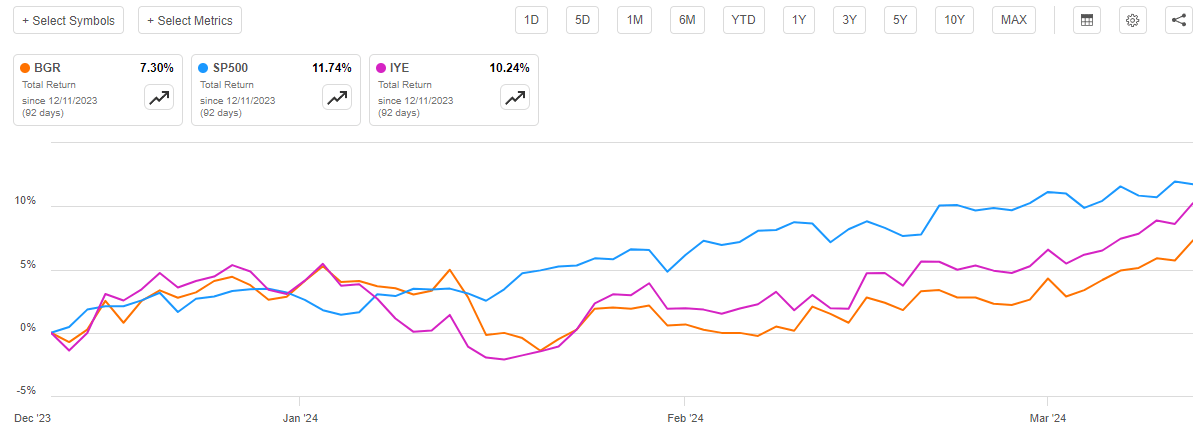

This second point is particularly important for our purposes today. A closed-end fund such as the BlackRock Energy and Resources Trust pays out most or all of its investment profits to the shareholders in the form of distributions. The basic goal is for the portfolio to stay relatively stable, but investors get sent all of the profits from the fund’s portfolio. This is the reason why these funds tend to have much higher yields than most other things in the market. It also means that we need to take the fund’s distributions into account when performing any sort of performance analysis. After all, distributions do represent real returns on their money for investors, and they also result in shareholders doing a lot better over time than the fund’s share price performance alone would suggest.

When we take the distributions into account, we see that shareholders of the BlackRock Energy and Resources Trust earned a 7.30% total return since we previously discussed the fund. This is, unfortunately, still worse than the two indices delivered over the same period:

Seeking Alpha

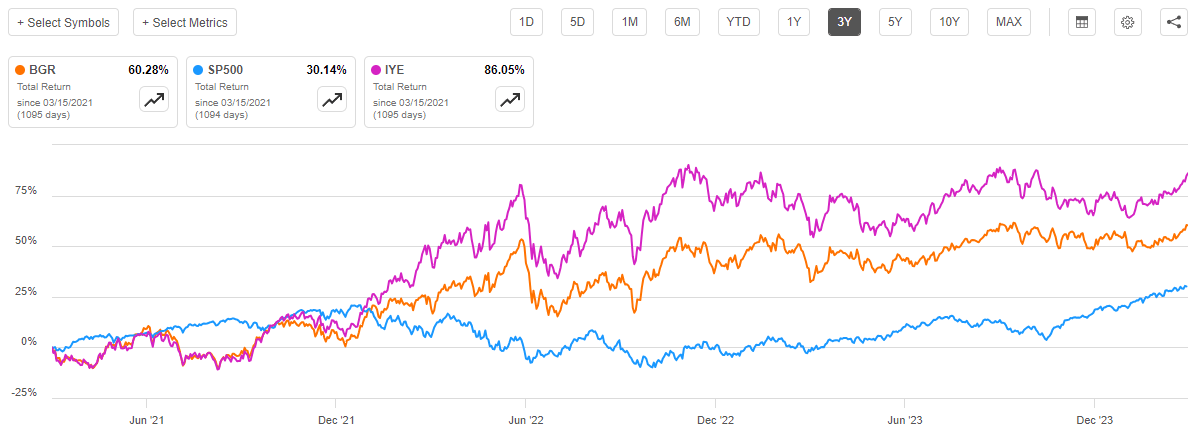

This will almost certainly be a turn-off for many investors, although income investors are sometimes willing to sacrifice a certain level of return in exchange for income. This fund has certainly done better over longer periods of time, though, as it did manage to beat the S&P 500 Index over the past three years:

Seeking Alpha

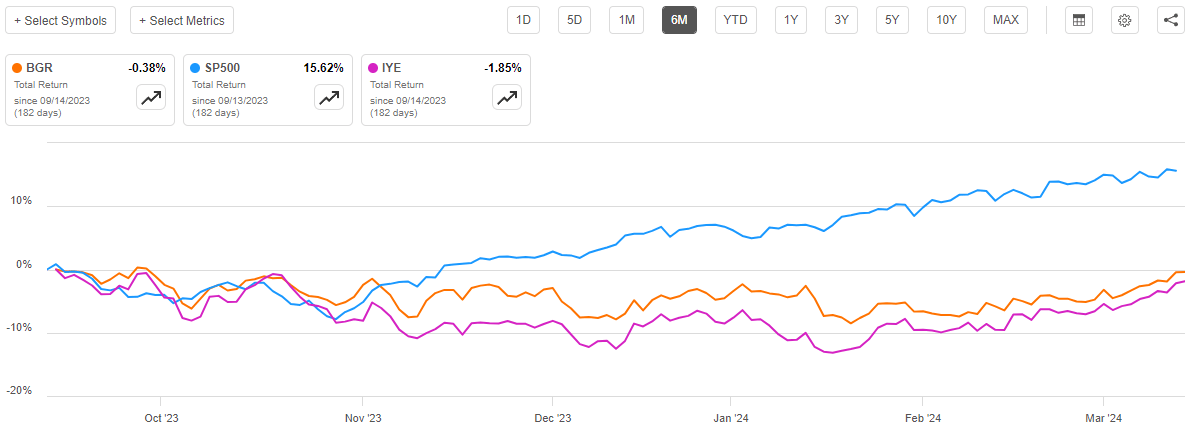

However, there is no sustained period of time in which this fund outperforms the U.S. Energy Index. It can sometimes outperform on a short-term basis when energy prices are falling, such as was the case over the past six months:

Seeking Alpha

As such, this fund is best for people who want exposure to energy companies and are willing to sacrifice a certain amount of total returns in exchange for a high yield.

As it has been a few months since we last discussed this fund, there have been a few things that have changed. Chief among them is that the fund released its full-year 2023 financial statements so we will want to pay special attention to those as part of our analysis. After all, those statements can provide us with a great deal of insight into the fund’s ability to maintain its distribution at the current level. The fund may have also altered its portfolio somewhat since our last discussion, so we want to have a look at that as well.

According to the fund’s website, the BlackRock Energy and Resources Trust has the primary objective of providing its investors with a very high level of total return. As is usually the case with BlackRock funds, the website describes in great detail how this objective will be achieved:

BlackRock Energy and Resources Trust’s investment objective is to provide total return through a combination of current income, current gains and long-term capital appreciation. The Trust seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its total assets in equity securities of energy and natural resources companies and equity derivatives with exposure to the energy and natural resources industry. The Trust may invest directly in such securities or synthetically through the use of derivatives. The Trust utilizes an option writing (selling) strategy to synthetically enhance dividend yield.

As the quote above states, the BlackRock Energy and Resources Trust employs a covered call-writing strategy to boost the effective yield that it receives from the portfolio. This is one of the reasons that I alluded to in the introduction that resulted in the fund underperforming the relevant energy indices during periods of rising stock prices. This is because the options strategy caps the potential gains that the fund can earn at the strike price of the option. It sacrifices any gains above that level that might be achieved before the options expire. Thus, in a bull market, the fund’s gains end up being lower than they would have been had the fund not sold the options. In theory, the strategy should increase the fund’s returns during periods in which energy stocks in general remain flat or decline. This is because the option premium provides a positive return, and the options are likely to expire worthlessly. In practice though, this is not always the case.

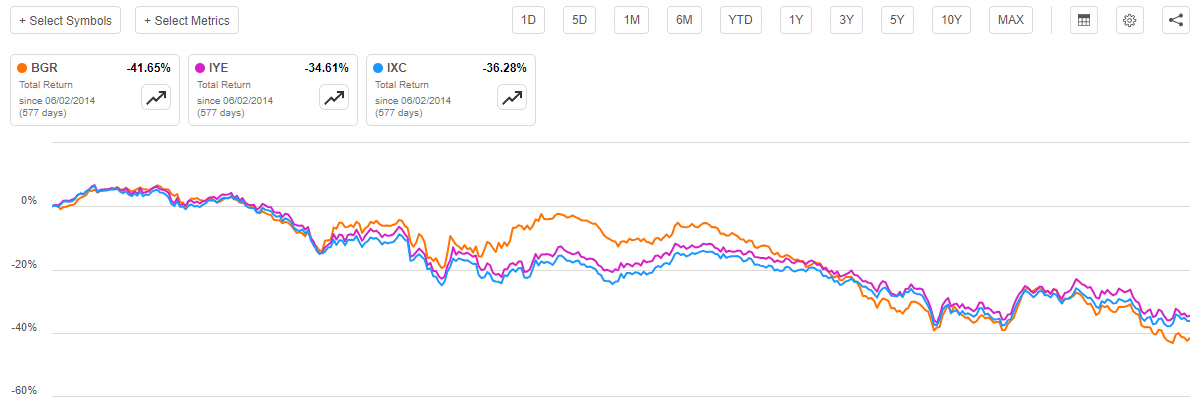

For example, consider the period stretching from June 2014 until early 2016. As long-time readers can likely remember, that was a terrible period for the energy industry in general, as Saudi Arabia was intentionally trying to keep energy prices suppressed in an effort to bankrupt the emerging U.S. shale industry. There were several companies that ended up going under, including most of the upstream master limited partnerships. Let us have a look at how this fund performed during that time:

Seeking Alpha

The above chart shows the BlackRock Energy and Resources Trust’s performance against both the U.S. and global energy indices that were mentioned in the introduction. For the purposes of this chart, all distributions paid by all three funds were included. As we can see, the BlackRock Energy and Resources Trust underperformed both energy indices over the June 2, 2014, through the end of 2015, despite the fact that its strategy theoretically should have resulted in the fund outperforming the indices over that period. There were, fortunately, a few short periods in which the fund outperformed, but overall, we can still see that the fund did not manage to deliver the performance that we would expect considering its strategy.

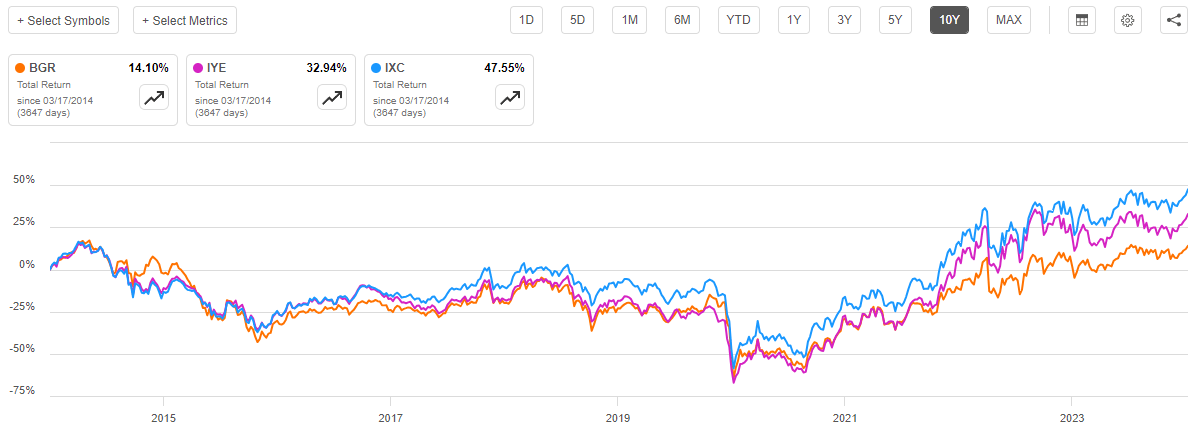

Unfortunately, the fund’s underperformance tends to compound over time. We can see this by looking at the fund’s total return over the past ten years. Here is the chart comparing it to the two indices:

Seeking Alpha

As we can clearly see, the fund substantially underperformed both indices, even when we consider that it has a substantially higher yield than either index. While it is certainly true that sometimes income investors might be willing to sacrifice a bit of total return in exchange for a higher yield, that is still a pretty big performance gap that might cause some investors to look elsewhere. However, we can see that most of the performance problems came in 2022 and extended through to the present. This was a period of generally higher energy prices than we have seen over most of the past decade, so it seems quite probable that the fund’s options strategy is the biggest factor hindering its performance.

As the fund’s covered call-writing strategy caps its upside potential, we want to make sure that it is not writing options against too much of its portfolio. After all, the greater the overwritten percentage, the weaker the fund’s potential as a way to profit from rising energy prices. Fortunately, this does not seem to be too big of a problem, as only 32.79% of the fund’s portfolio is covered by options as of February 29, 2024. Thus, roughly two-thirds of the portfolio should still be positioned to profit from gains in energy stocks.

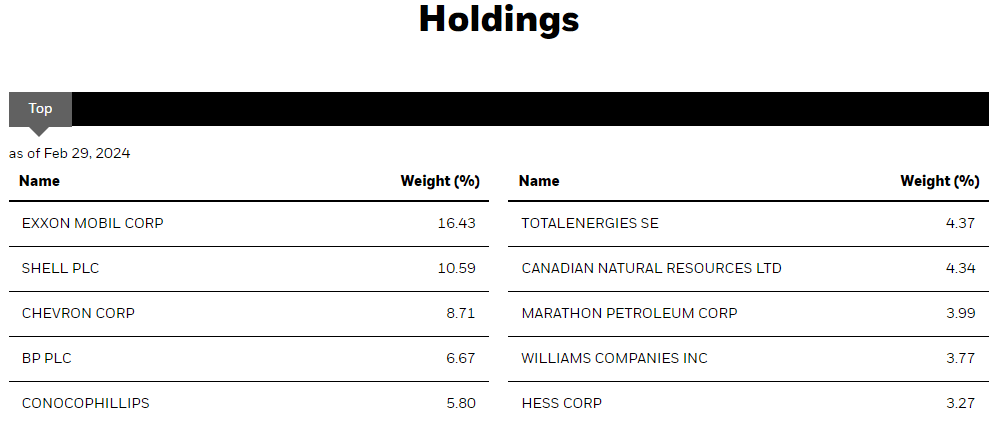

With that said, this fund does not invest in a substantial number of energy stocks. There are only 32 stocks in the portfolio, and most of them are very large energy companies. Here are the largest holdings in the fund’s portfolio as of the time of writing:

BlackRock

These are among the largest energy companies in the world, with five of them being considered supermajors by most analysts: Exxon Mobil (XOM), Shell (SHEL), Chevron (CVX), BP (BP), and TotalEnergies (TTE). ConocoPhillips (COP) is also sometimes classified as a “supermajor,” although it is not an integrated energy company nor is it anywhere near as large as the others on this list. The main point here though is that this is very much a large-cap energy fund, even though the fund does not explicitly state that on its webpage.

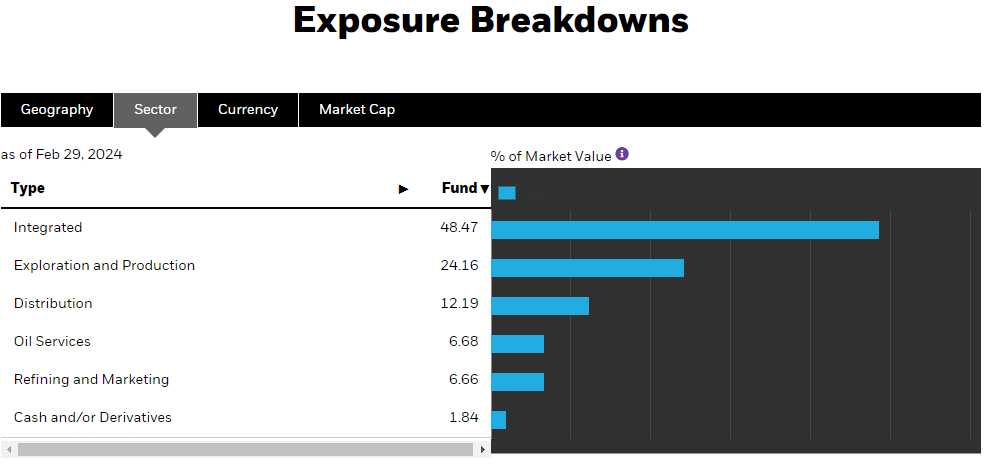

The fund’s website does point out that 48.47% of the fund’s assets are invested in integrated energy companies, however:

BlackRock

Integrated energy companies are almost always going to be giant, large-cap firms. This is at least partially due to the capital required to operate both an exploration and production unit and a refinery unit. Exxon Mobil, Shell, Chevron, BP, and TotalEnergies alone account for 46.77% of the fund’s assets, so it seems likely that these companies account for most of that “integrated” allocation. Those five companies also account for just under half of the fund’s assets, so this goes to show how concentrated this fund is compared to the indices:

Index ETF | Number of Holdings |

iShares U.S. Energy ETF | 44 |

iShares Global Energy ETF | 67 |

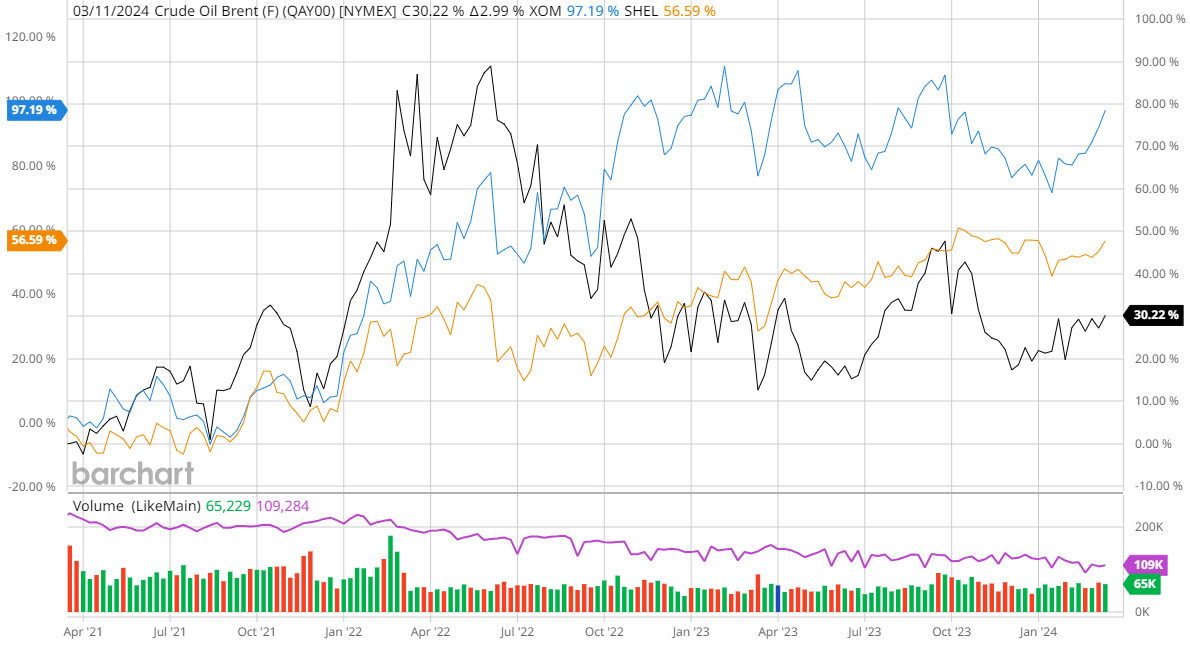

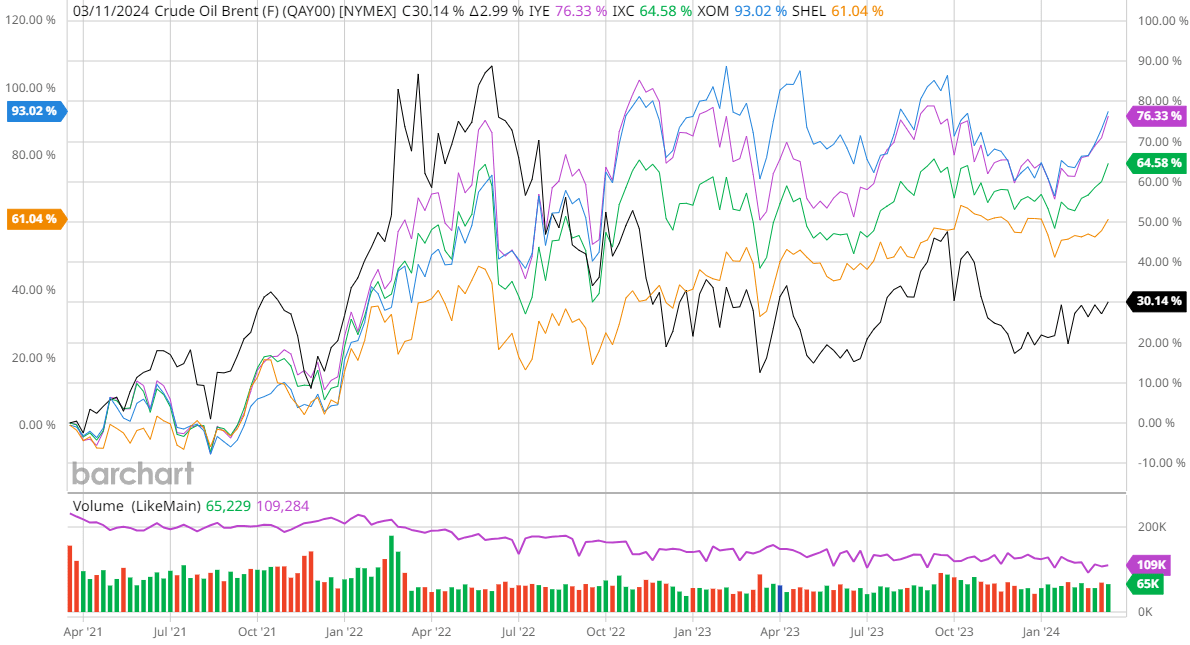

As regular readers are no doubt well aware, I do not generally like to see any fund have its assets overly concentrated in only a few positions. This is because that tends to expose the investors to idiosyncratic, or company-specific, risk. In this case, that risk could come from the fact that energy stocks have not perfectly matched crude oil prices in recent years. For example, consider the following chart:

Barchart

This chart shows spot Brent crude oil (black line) against ExxonMobil (blue line), and Shell (orange line) over the past three years. We can clearly see that both stock prices exhibited radically different performances from one another and from the global price of crude oil. The iShares U.S. Energy ETF delivered almost identical performance to ExxonMobil’s share price over the period, but the iShares Global Energy ETF was roughly between the two:

Barchart

This actually means that not only are the indices not necessarily a good way to play energy prices, but the BlackRock Energy and Resources Trust does not appear to be either. This is a similar situation to what we see in the gold mining industry, as stocks in that industry do not necessarily track the price of gold. This also means that, due to the fund’s heavy concentration in only a few names, investors are exposed to the risks of those individual companies and not just to the impact that energy prices can have on the profitability of a given company in the industry.

This could be very important right now because the fundamentals are pointing to rising energy prices going forward. As we have discussed in various previous articles here at Energy Profits in Dividends, the demand for oil has been proving to be much more resilient than has been projected by the International Energy Agency. A simple Google search reveals much the same thing. For example, an article by Irina Slav was published to OilPrice.com this morning stating:

The document came out in May 2021. In that report, the IEA said there was no need for new oil and gas exploration because the energy transition was moving fast enough to make that redundant. But did not take long for IEA to revise its view. In November of that same year, the agency called for more investment in oil and gas exploration amid a risk of a supply shortage.

Last year, the International Energy Agency’s prediction of gasoline demand came up woefully short of what actually occurred. Earlier today, the agency began predicting a supply shortage this year. In previous articles, I pointed out that other sources were predicting that the supply shortage would not begin until 2025. Thus, there are reasons to believe that we will see a near-term supply shortage, especially if the International Energy Agency’s predictions are too low once again. That should obviously have a positive effect on energy prices due to the law of supply and demand.

Although the share price of the companies held by the BlackRock Energy and Resources Trust does not perfectly track energy prices, we can still expect that rising energy prices will have a positive impact on the profits of the companies themselves. After all, we saw this in 2022, when oil and gas prices surged following the outbreak of hostilities in Eastern Europe. In the case of a global crude oil shortage, as is currently being predicted, it is almost certainly going to be a long-term condition that will have a much greater effect than simply boosting the profits of crude oil producers for a few quarters. That will probably end up having a positive impact on the share price of the companies held by the fund, as well as the fund itself. However, as we have already seen, the fund’s call option-writing strategy will reduce its total profits compared to an energy index fund.

As mentioned earlier in this article, the primary objective of the BlackRock Energy and Resources Trust is to provide its investors with a high level of total return through a combination of current income, current gains, and long-term capital appreciation. The energy sector in general tends to have higher yields than many other areas of the economy, simply due to the market failing to appropriately reward companies in the industry for delivering cash flow and profit growth. These companies simply started paying out large dividends to provide investors with a return on their money. That serves as one source of income for this fund, but it also earns a certain amount of money from the premiums for the sale of covered call options. These premiums can frequently result in very high effective yields (see here). Finally, the fund also might be able to realize some capital gains through the sale of appreciated stock. It pools all of the money that it earns from these various operations together and then pays them out to its investors, net of its expenses. We might assume that this would allow the fund’s shares to boast a very high yield.

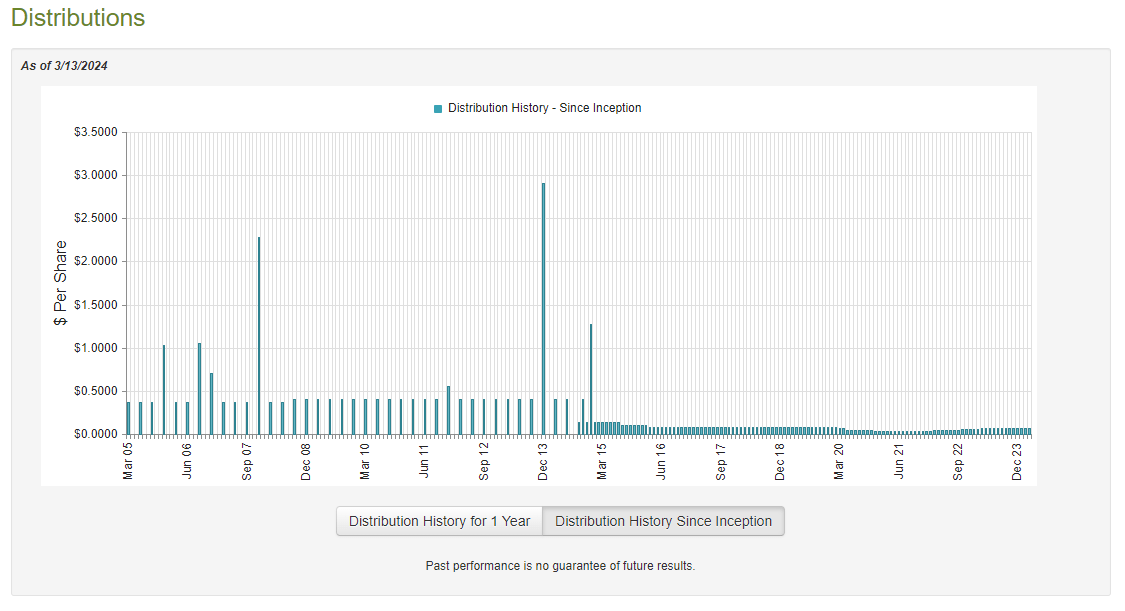

This is indeed the case, as the BlackRock Energy and Resources Trust pays a monthly distribution of $0.0657 per share ($0.7884 per share annually), which gives it a 6.14% yield at the current share price. The fund has unfortunately not been especially consistent with respect to its distribution over time, as the overall trend was negative prior to the pandemic and positive following it:

CEF Connect

This seems certain to reduce the fund’s appeal among those investors who are seeking to earn a consistent and secure income from their assets. However, it is not unexpected when we consider the events that occurred in the energy sector over the past fifteen years or so. There were, after all, two energy price crashes in the past decade that caused widespread damage to investors in the sector. If we go back a bit further, the financial crisis of 2008 also knocked down energy prices for a while. These things naturally would have had a negative impact on the fund, and it had to reduce its distributions in order to preserve net asset value in the face of such destruction. Fortunately, we do see that the fund has been increasing its distribution since the end of the pandemic as things have started to improve in the energy sector.

As I have pointed out numerous times in the past, the fund’s distribution history is not necessarily the most important thing for shareholders. After all, anyone who purchases the fund today will receive the current distribution at the current yield and will not be impacted by events that occurred in the past. As such, the most important thing for our purposes today is to determine how well the fund can sustain its distribution going forward.

Fortunately, we have a very recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2023. This is a much newer report than the one that was available to us the last time that we discussed this fund, which is quite nice to see. This report will give us a much better understanding of how well the fund handled the second half of 2023 than we had from the semi-annual report. That is nice to see since the market overall proved to be quite volatile over that period. It is also always good to have the most recent data that can be obtained when we consider a fund for investment.

For the full-year 2023 period, the BlackRock Energy and Resources Trust received $15,268,115 in dividends and surprisingly no income from any other source. The fund had to pay foreign withholding taxes on some of its positions, which left it with a total investment income of $14,590,967 over the period. It paid its expenses out of this amount, which left it with $10,408,652 available for shareholders. That alone was not nearly enough to cover the fund’s distributions, as this fund paid out $21,505,705 to its shareholders over the period. At first glance, this may be concerning, as the fund did not have sufficient net investment income to fully cover the distributions that it paid out to the investors.

However, there are other ways through which the fund can obtain the money that it needs to cover its distributions. For example, it might be able to obtain some capital gains from the sale of appreciated stock. It also gets a cash premium when it writes an option and sells it in the market. Realized capital gains and received options premiums are not considered to be investment profits for tax or accounting purposes, but they clearly do represent money coming into the fund that can be paid out to the investors.

Fortunately, the BlackRock Energy and Resources Trust did manage to have a certain amount of success at obtaining money from these alternative sources during the period. The fund reported net realized gains of $23,169,588, but these were partially offset by $15,169,570 net unrealized losses during the period. Overall, the fund’s net asset value declined by $10,510,727 after accounting for all inflows and outflows during the period. The fund repurchased $7,413,692 worth of its own stock, otherwise, it would have done a bit better than this at covering its distribution.

However, it still appears that there is nothing to worry about here. During the full-year period that ended on December 31, 2022, the BlackRock Energy and Resources Trust saw its net asset value increase by $84,989,114 after accounting for all inflows and outflows over that full-year period. Thus, the fund has managed to fully cover all of its distributions and share buybacks over the past two years. We should not need to worry about a distribution cut right now. This fund is in very good shape financially.

As of March 13, 2024 (the most recent date for which data is currently available), the BlackRock Energy and Resources Trust has a net asset value of $14.77 per share, but the shares currently trade at $12.78 each. This gives the fund’s shares a whopping 13.47% discount on net asset value. This is very much in line with the 13.51% discount that the shares have had on average over the past month. The current price therefore looks pretty good for anyone who wishes to purchase shares of this fund today.

In conclusion, the BlackRock Energy and Resources Trust is a closed-end fund that energy investors can use to obtain a fairly high yield while retaining some exposure to energy stocks. However, the fund is a chronic underperformer in most market environments compared to index funds investing in the energy sector. The fund is highly concentrated in only a few companies, but fortunately, the fundamentals for many of those companies appear to be solid, as there is a very real risk of an oil shortage later this year that will cause energy prices and the profits of these companies to increase. However, it is important to note that the price of crude oil does not necessarily correlate with the stock price of energy producers.

The BlackRock Energy & Resources Trust looks like a reasonable way to play the energy sector, although it will require that investors sacrifice some upside in exchange for income. The fund does trade at a huge discount though, so if that discount closes, it could result in some attractive gains. However, I do not see a near-term catalyst for the closure of the discount.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.