FatCamera/E+ via Getty Images

FatCamera/E+ via Getty Images

In this article, we want to talk about how to manage the ETF holdings in your investment portfolio. First, we'll explain our philosophy when it comes to portfolio strategy so you can decide how to best allocate your funds based on your financial situation.

Further, we believe that if you don't have the time or interest to select individual stocks, you should invest the equity portion of your portfolio fully in ETFs.

When managing this investment portfolio, one approach is to shift the proportions of different stocks within our equity/stock allocation, while keeping the overall amount invested in equities steady.

Now, here's why we think investors should overweight, or allocate more of their equity portfolio to, the iShares Russell Mid-Cap Growth ETF (NYSEARCA:IWP) compared to an S&P 500 index fund like the SPDR S&P 500 ETF (SPY). We have two main reasons for this recommendation.

First, we believe mid-cap companies have the most to gain from advancements in artificial intelligence today.

Second, mid-caps were negatively impacted over the past few years by high inflation and rising interest rates. As inflation continues to moderate in 2023 and rates peak, mid-caps stand to see a surge in their operating performance and stock prices by 2024. They should enter a period of peak financial returns.

Let's start by going over some basic concepts of portfolio management as we discuss how investors should allocate money between different ETFs.

First, one great thing about ETFs is that they have very little default risk. This is not just because they invest in a diverse group of holdings, but also because they periodically remove underperforming assets and add new top-performing ones to their holdings list. This ensures that even if some companies fail, they are no longer part of your ETF before that happens.

Understanding this, the next thing an investor should focus on is allocating money based on their personal risk tolerance. Typically, if you have retired or don't have a steady income stream from a job or rental properties, and are relying on retirement savings to live on, you should allocate most funds into fixed-income ETFs like the iShares 20+ Year Treasury Bond ETF (TLT). We recently published an article to recommend that fixed-income investors allocate more money to this long-term bond ETF.

If you have a steady income but high upcoming expenses - like saving for kids' college or medical bills - you should also put some money in a fixed income. This can lower the risk of losing your income stream in case of a layoff.

Choosing individual stocks is a whole other ballgame. Actively investing in individual stocks is the only strategy that involves keeping cash on hand to take advantage of economic cycles or market dips to get better returns. We can get more in-depth on that in a future article. For now, our focus is on investing in ETFs.

So in our opinion, as long as your basic living expenses are covered, rather than letting cash sit around, you should consider putting 100% of your remaining investable money into stock index funds like the SPY, QQQ, or IWP, which we are going to discuss later. This is after setting aside 6 months of living expenses (housing, food, transport, etc.) in safe assets.

When looking over longer time horizons of around 10 years, stocks in general deliver superior returns compared to more conservative assets like bonds. That's why many financial advisors benchmark returns or set investment goals over decade-long periods.

Why 10 years specifically? Well, it's kind of a rule of thumb we use because that's around the length of the average economic cycle historically if you look back at recessions in the early 2000s, 2008, and 2020. Of course, cycles aren't always so consistent - some stretch longer than a decade or prove shorter.

But 10 years gives us a reasonable approximation to smooth out ups and downs. Even with temporary crashes mixed in, stocks reliably outpace inflation and offer stronger compound growth on that timescale whereas bonds see much flatter total returns. You need stocks for your money to actually grow rather than just tread water over a full cycle.

Put simply - if an investor has cash they won't need to access for at least 10 years, they almost always will do better investing in stock index funds versus lower-risk, lower-return fixed income assets.

Why do we recommend going 100% into stocks rather than keeping some cash on hand? Good question!

To explain, we used Amazon (AMZN) stock as a case study to compare the returns from consistently investing over time versus trying to "time" the market by waiting to buy during dips.

If you had auto-invested $100 each month into Amazon stock starting in January 2007, just before the financial crisis, you'd have seen a 1205% total return and 17.4% annualized return on your money by now. Not bad!

But what if you held off investing that $100 until after the crash, starting in November 2008? Even though you bought shares at lower prices during the dip, your overall return is less - 861% total and 16.3% annualized.

Yahoo finance, LEL

Counterintuitive, right? Here's why:

By waiting, you "missed out" on compound returns from 31 additional $100 investments in 2007-2008 when shares were pricier. So you ended up investing $13,000 total versus $11,800 by trying to time the bottom. That opportunistic waiting game cost you over $55,000 in lost profit!

Of course, if you nail perfect timing and dump a lump sum into the dip, returns can be astronomical. Putting that $1,300 cash to work in late 2008 resulted in a 20.7% annualized return. Not bad! But that's very hard to execute consistently.

Yahoo finance, LEL

This lesson applies to most blue chip stocks and index ETFs too, since long-run returns wash out short-term crashes. The power of regular, earlier compounding usually wins out.

So while having some "dry powder" on the sidelines sounds smart, our analysis shows keeping 100% invested from the start leads to better overall returns for most long-term portfolios.

Now that we've covered some core portfolio strategy concepts and the pros and cons of timing the market, let's chat about why investors may want to overweight the iShares Russell Mid-Cap Growth ETF compared to other index funds like the S&P 500 ETF.

The IWP fund aims to closely match the returns of the Russell Midcap Growth Index. This index is made up of medium-sized U.S. companies that are showing strong growth trends.

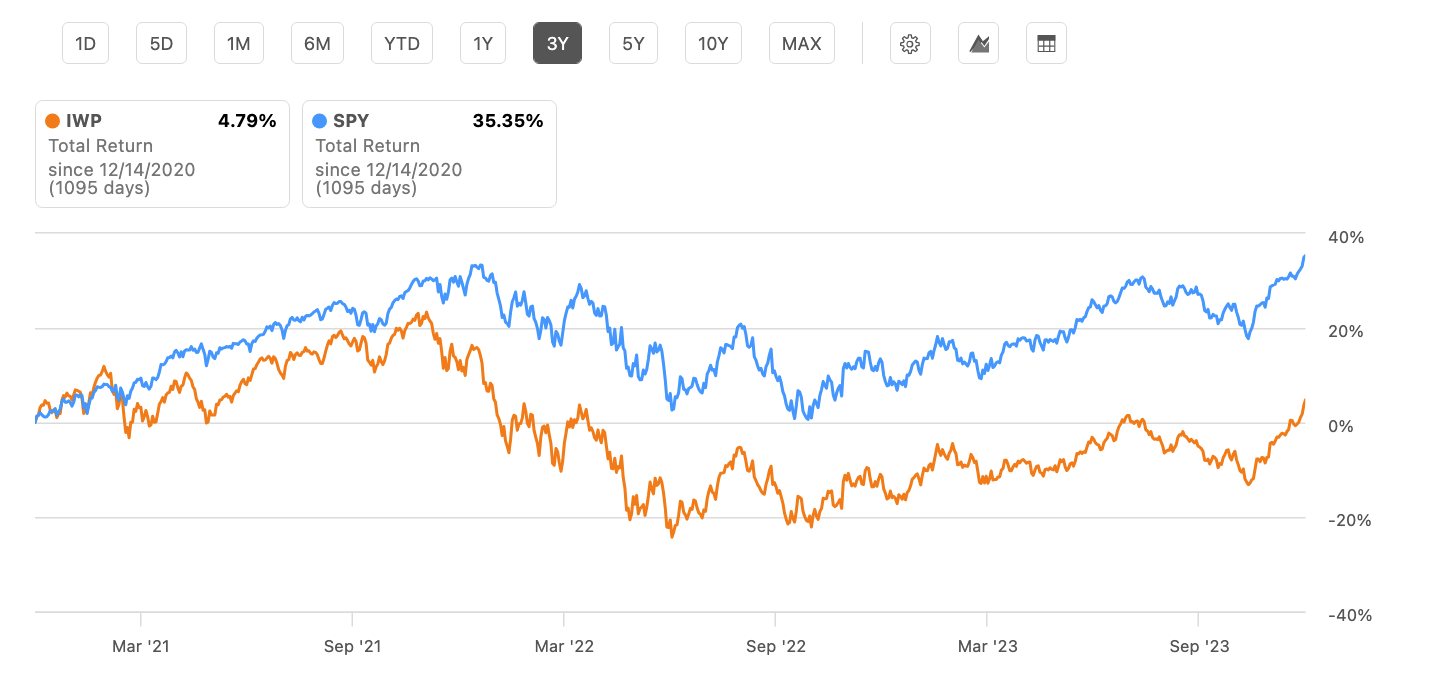

When looking at returns over the past 23 years since IWP first launched, it has outperformed the S&P 500 pretty consistently. Total returns for IWP have reached 578% cumulatively since 2000. Meanwhile, SPY returned only about 498% over the same timeframe. The main reason is that even though mid-caps tend to be higher risk than large blue chip companies, they also often have stronger growth trajectories over time thanks to their nimbleness.

Seeking Alpha

However, IWP finally hit an air pocket relative to SPY in 2021 and so far in 2023 as inflation spiked and interest rates rose aggressively. Those macro headwinds hit mid-cap companies disproportionately hard in the near term. But even factoring in this recent underperformance, IWP's total price returns of 4.7% for the past 3 years underperformed the S&P 500's 35% total return.

Seeking Alpha

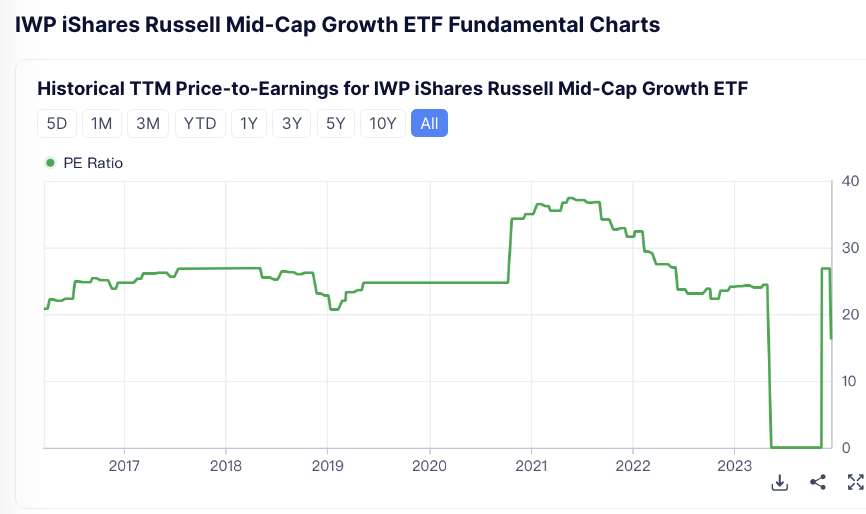

To understand if IWP seems expensive or cheap right now, we can look at its P/E ratio over time. IWP's current P/E is 16.34x. Looking back over the last 10 years, the range has been between 16.2x on the low end and 37.4x on the high end, with a median of 24.7x. So with the ratio presently at 16.34x, that puts it at the very bottom of the 10-year range.

Gurufocus

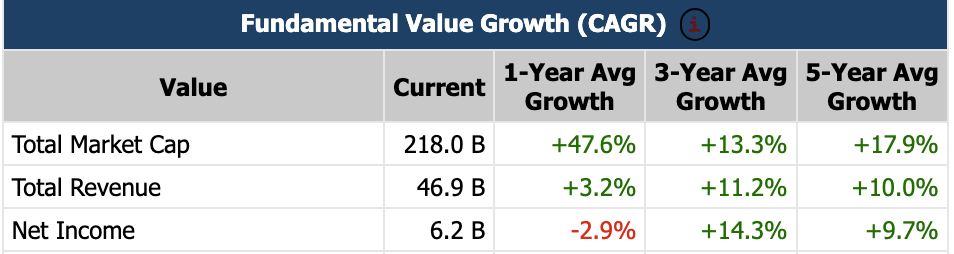

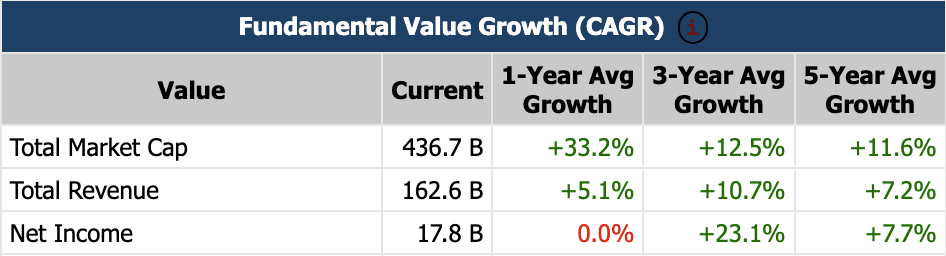

This doesn't match up with the strong financials the ETF's underlying companies have reported lately - 6.4% revenue growth and a 69% increase in net income in 1-year average growth. So the market may have underestimated its value.

IWP (Market Chameleon)

SPY (Market Chameleon)

QQQ (Market Chameleon)

Further, we think conditions are set to turn favorable for IWP again by 2024 for a couple of key reasons:

First, advancing AI technology stands to provide a boost to enterprises before reaching mass consumer adoption.

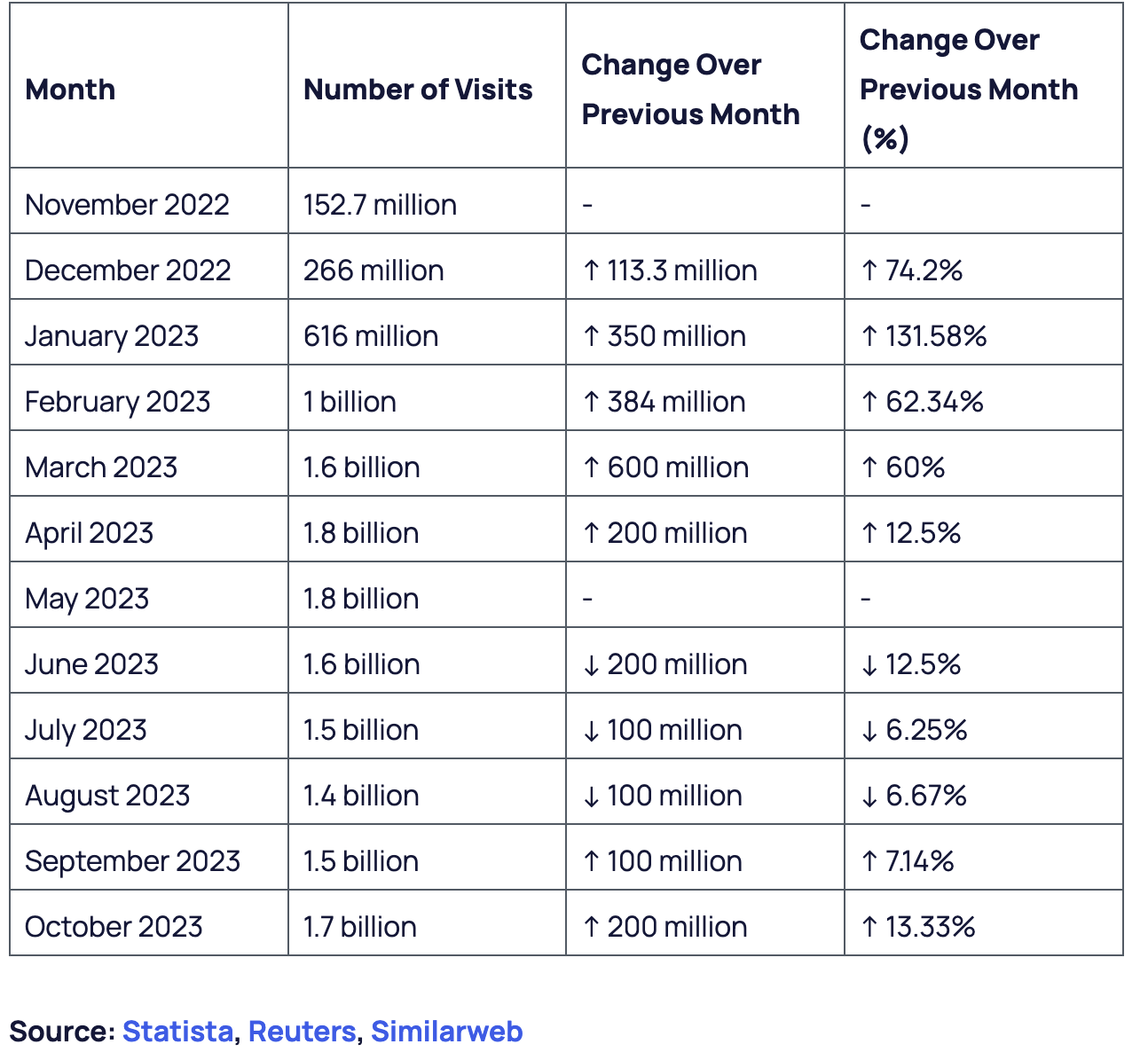

There's no doubt the rise of large language models like ChatGPT drove breakout growth for AI leaders like Microsoft in 2023 through increased enterprise cloud usage. ChatGPT traffic has grown 10x since last November to 1.7 billion monthly visits.

But while these models now draw 100 million+ weekly consumers, user growth seems to have plateaued for now as the average person finds limited use for AI chatbots. Their visit traffic stalled out last June.

ChatGPT stats (Statista, Reuters, Similarweb)

Hence, we think most of the AI productivity gains so far come on the business side. PowerPoint helper tools save time for staff to build presentations. Spotify (see our Strong Buy coverage) uses AI to lower the costs of crafting ads. Customer service chatbots reduce labor needs. And individuals mainly leverage AI to improve work output, not for personal use.

This suggests to us that enterprises will be the greatest near-term beneficiaries of AI, especially nimble mid-cap firms. The way we see it, businesses and enterprises are primed to start leveraging AI tools to lower operating costs right now.

We think the types of growing mid-sized companies held by IWP could make ideal early adopters of AI tools. Compared to giant corporations, these medium companies likely have a few key advantages when it comes to deploying new technology:

First, they are still small enough to be nimble. They can pilot AI projects without layers of bureaucracy slowing things down. And if AI drives efficiencies, they have the flexibility to reduce headcount or shift resources faster than a behemoth corporation could.

Second, as growth companies, they are still adapting their business models. AI could allow them to optimize and scale smarter. Large caps with entrenched ways of doing business might be less willing to disrupt their model to incorporate AI.

Rising profitability usually directly translates to richer valuations too. So we think mid-caps legitimately have the upside to see their P/E ratios rebound as AI and tech integration drive margin upside over 2023-2024.

If you feel like you already missed the boat on investing in large-cap AI leaders like Microsoft or Google, allocating more to the IWP could be a savvy way to still benefit from expanding AI adoption.

Secondly, many mid-caps were already squeezed by the 2022 inflation spike and rising interest rates before macro conditions crushed demand. Still investing to expand and unprofitable, higher costs and weaker sales doubly damaged them.

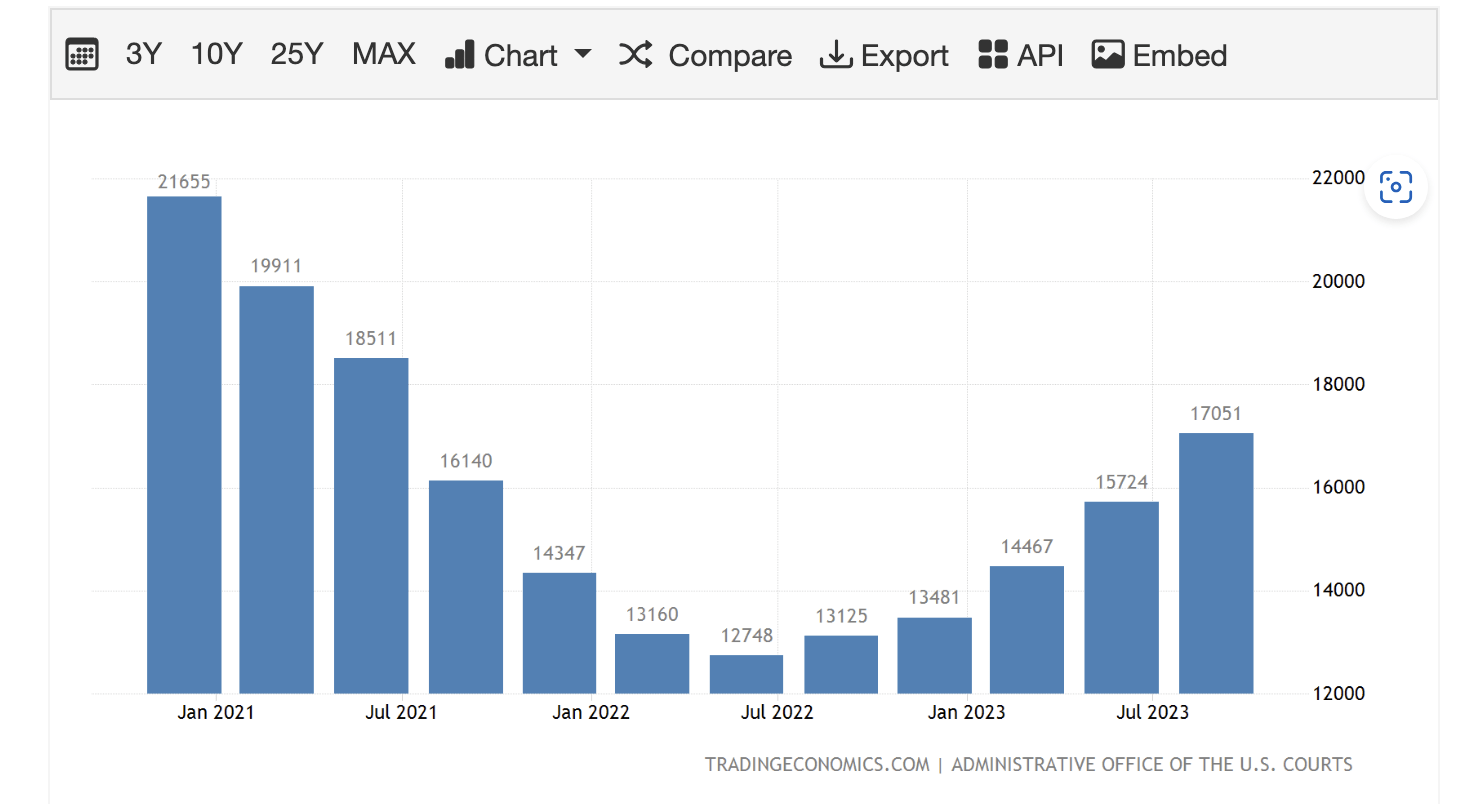

The bankruptcy figures back this up - smaller firms were most vulnerable in both the 2020 COVID recession and the 2022 inflammatory economy.

But those who survive this trial by fire should emerge stronger than ever. As rates peak and inflation fades through 2023, the operating backdrop improves and they can regain their footing.

Trading Economics

We don't want to gloss over the risks to our bullish IWP thesis. There's always a chance small and small caps continue underperforming large-cap index funds like SPY - especially if inflation or recession make surprise comebacks later in 2023 or into 2024.

However, our economic analysis suggests the US is primed for a cyclical upswing rather than continued gloom and doom.

For example, employment and wage growth and job openings remain resilient despite tighter Fed policy designed specifically to cool the job market. This gives us confidence inflation pressures are genuinely starting to fade on their own as consumers and businesses adjust to a post-COVID normal.

Most importantly, core inflation gauges like housing costs are calming from 2022's breakneck pace based on recent data. As inflation falls back near their 2% target over 2023, the Fed is already hinting they'll cut interest rates in 2024 to keep real yields neutral rather than restrictive.

This impending shift to a stimulative policy stance aligns perfectly with our view. An inflation plateau paves the way for consumers to return once rates decline. And falling yields are especially beneficial to the mid-cap growth stocks that populate IWP.

None of this means there is no possibility of runaway inflation or financial instability sinking the economy again. But based on the preponderance of evidence today, we believe risks are firmly tilted to the upside looking out to 2024.

To wrap up, our overall take is that investors who don't have time to select individual stocks should remain fully invested in ETFs rather than trying to time market dips.

When allocating across ETFs, the long-term growth trajectory still favors overweighting funds exposed to mid-cap stocks, like the IWP, over S&P 500 flagships like SPY.

In our view, IWP's recent underperformance is just a temporary weakness as mid-caps took an outsized hit from the pandemic disruptions and inflation whiplash of 2022. Their nimbleness can be a curse in periods of economic instability.

But as the Fed plans potential future rate cuts in 2024 and inflation seemingly plateaus thanks to still-strong employment and wage growth, we see mid-caps recovering vigorously. Their agility makes them prime beneficiaries of both the expected AI revolution and returning consumer demand as rates ultimately fall.

So, while IWP carries short-term volatility, its risk-reward looks highly compelling at current valuations. We'd overweight IWP within overall blended ETF portfolios to benefit as business conditions improve over 2023-2024.