Paulo Fridman/Corbis News via Getty Images

Paulo Fridman/Corbis News via Getty Images

Reviewing Cielo's (OTCPK:CIOXY) investment thesis since my last coverage, I have taken a neutral stance on the company. Cielo, a payments company, was in the process of recovering from the challenges of 2022, marked by significant macroeconomic headwinds in Brazil, including an interest rate hike to nearly 14% and a challenging credit environment in the first half of 2023, which impacted the company's revenue and transaction volume.

Throughout 2023, Cielo implemented crucial cost-reduction measures, expanding its presence in mid-tier businesses. Additionally, a more favorable interest rate environment in Brazil in the second half of 2023 contributed to a gradual recovery in the company's profitability. Since October 2023, Brazilian equities have rallied, driven by interest rate cuts, resulting in a surge of approximately 40% in Cielo's shares up to the present moment.

More recently, in early February, Cielo reported its fourth-quarter 2023 results, which lacked significant traction. While profit growth remained modest in the quarter and saw a slight decline on an annual basis, there were no significant adverse developments. However, the notable development was the announcement of a public offering to privatize the company by its two controlling shareholders, Bradesco (BBD) and Banco do Brasil (OTCPK:BDORY). Their proposal offered limited upside potential compared to the current share price of Cielo's ADR.

Although my discounted cash flow ("DCF") analysis and comparison of valuation multiples with domestic peers suggest potential undervaluation based on the current share price of around $1 per share, the IPO proposal adds an extra layer of risk to adopting a more bullish stance on Cielo. The offer does not present significant attractiveness in terms of upside potential.

Unexpectedly, Bradesco and Banco do Brasil have proposed a public buyback offer for Cielo. The offered price is R$5.35 per share (approximately $1.07 for the ADR at the current exchange rate), but it will be adjusted by proceeds, including the R$410 million Interest on Equity (JCP) to be paid in April 2024.

If the offer is accepted, Banco do Brasil would hold 49.9% of Cielo's capital, while Bradesco would hold the remaining 50.01%. Banco do Brasil has a 28.65% stake in Cielo, and Bradesco holds 30.06%. Cielo's free float stands at 40.57%.

The limited potential compared to the offer price is likely to stimulate discussions about the valuation of the buyback offer, reminiscent of the situation when Itaú Unibanco (ITUB) closed the capital of Redecard in 2012. Based on Cielo's (CIEL3) closing price on the Brazilian Ibovespa on February 21, 2024, of R$5.29 per share, the offer price of R$5.35 would result in only a 1% upside. Factoring in the JCP to be received, the upside might turn into a downside.

On one hand, the involvement of the controlling shareholders as buyers raises concerns about conflicts of interest in the buyback offer. However, from a business perspective, the takeover bid makes sense for Banco do Brasil, Bradesco, and Cielo. The competitive landscape has evolved significantly, and the outlook for sustained profitability is dim. Itaú's success with Rede and Santander Brasil's (BSBR) with Getnet in integrating cross-selling of banking products and acquiring has outpaced that of Bradesco; Banco do Brasil and Cielo.

Another motive for the bid is the complication involving Cateno (Banco do Brasil's credit card interchange revenue, sold to Cielo in 2014). Both banks still view acquisition as a critical component of the card ecosystem.

The strategy behind Cielo's buyback offer was also a focal point in Banco do Brasil and Bradesco's conference calls for the fourth quarter of 2023. According to Bradesco's CEO Marcelo Noronha, the offer is pursued to bring Cielo's acquiring business closer to the two banks. He also emphasized that there are no ongoing discussions about a potential spin-off of the Cateno unit.

Tarciana Medeiros, Banco do Brasil's CEO, also noted in the Brazilian bank's conference call that the decision to close Cielo's capital aims to operate more assertively in the market. Bradesco and Banco do Brasil executives expressed confidence in the operation's success.

It is also probable that the terms of the public buyback offer will be deliberated with minority shareholders going forward and that the move holds strategic value for sectoral developments. Initially, it may negatively impact competition from other acquirers, such as StoneCo (STNE) and PagSeguro (PAGS), by accelerating competition in small and medium-sized enterprises (SMEs).

Cielo reported another weak quarter despite some positive aspects. The fourth quarter of 2023 saw higher transacted financial volume (TPV) in acquiring, which expanded, along with robust results from Cateno. Cateno benefited from increased volumes and a more favorable product mix, leading to a new profit record. Additionally, lower financial expenses were recorded consolidated due to the decrease in the Brazilian interest rate (Selic).

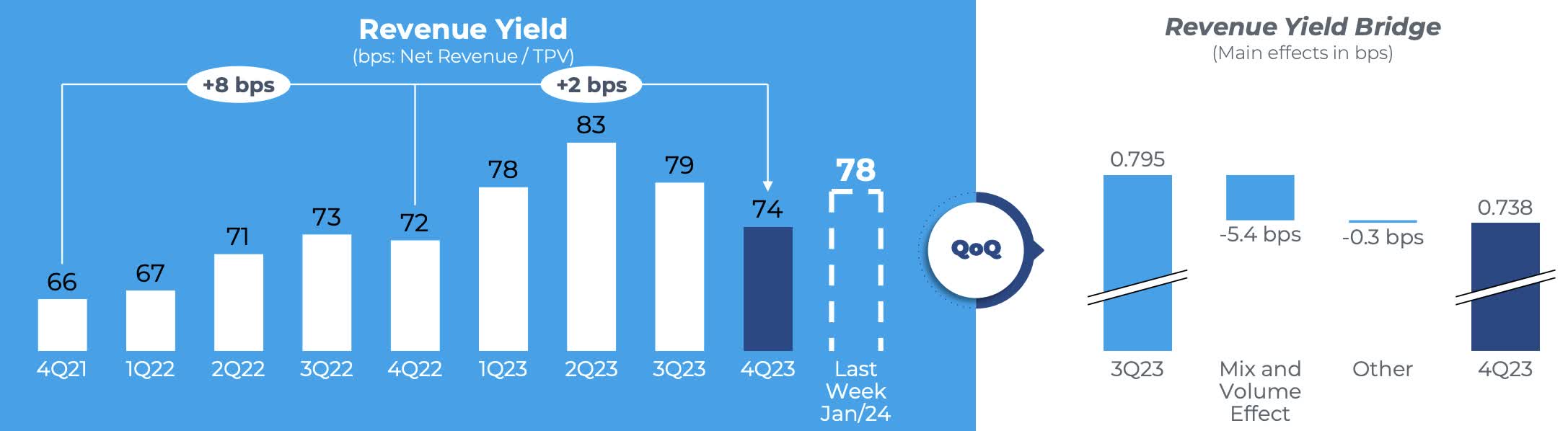

Despite some positive aspects, Cielo's recent quarter also showcased several negative trends. Firstly, the acquiring yield experienced a significant decline quarter-over-quarter, attributed to factors like customer base renewal. Secondly, there were notable customer losses during the period. Thirdly, expenses surged considerably due to ongoing restructuring efforts, indicating potential challenges in cost management. Lastly, there was a concerning quarterly drop in the penetration of term products, suggesting potential difficulties in product adoption or market competitiveness.

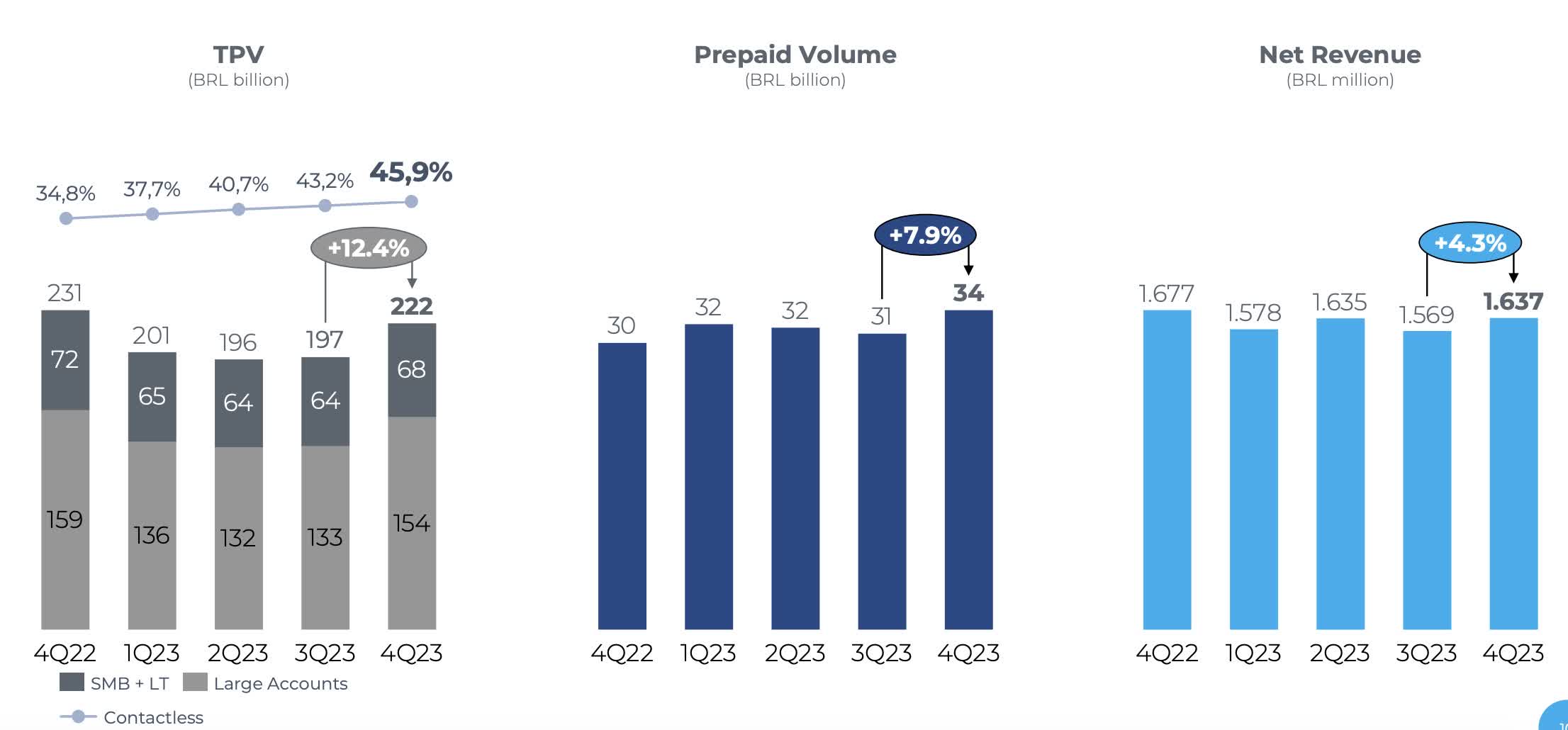

Looking deeper into Cielo's results, the financial volume transacted (TPV) showed a quarterly improvement, totaling R$221.85 billion, a quarterly increase of 12.4%, despite a 4.1% annual drop. Debit card transactions were the worst performer year-over-year, contracting by 8.4%, while credit transactions fell by 1.1%.

Cielo's IR

The number of customers declined, indicating a gradual loss of market share to other acquirers in the Brazilian market, particularly StoneCo and Pag-Seguro. Cielo reached 870,000 users, representing a drop of 5% from the previous quarter and 18% from the prior year.

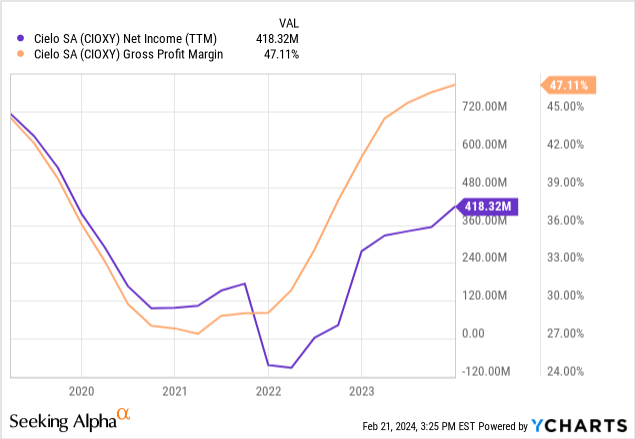

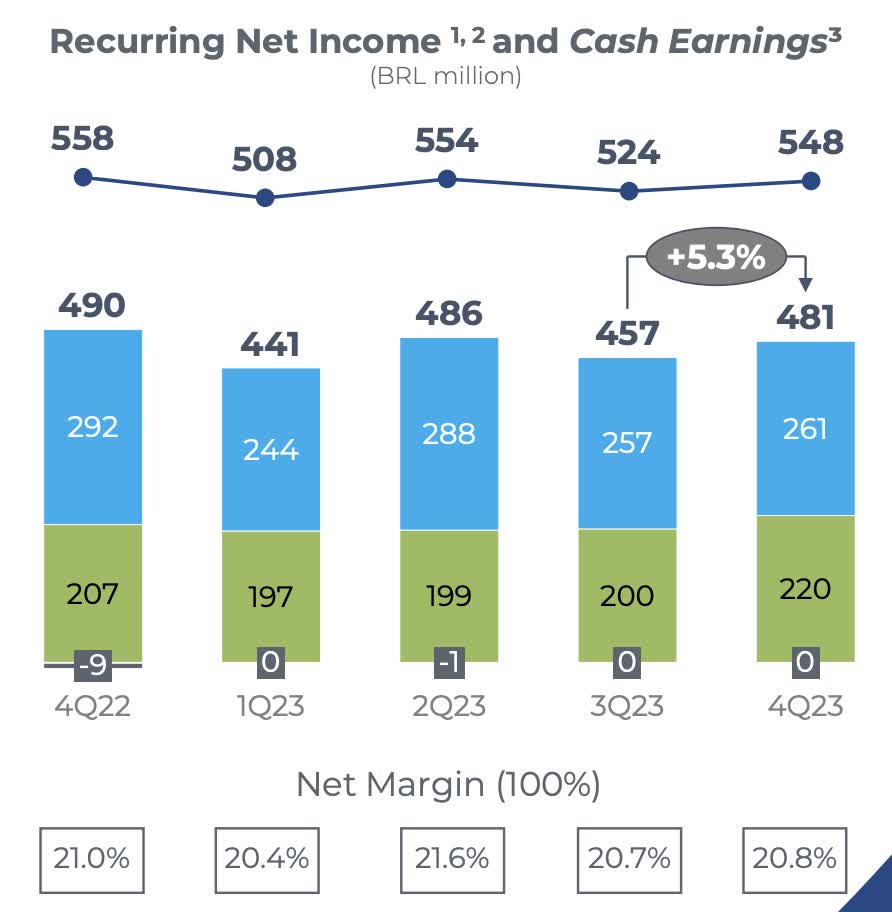

Cielo recorded revenues of R$2.8 billion, marking a 5.8% increase compared to Q3 and a 0.6% increase compared to Q4 2022. The slight year-over-year rise was attributed to improved yield in Cielo Brasil and increased volume in Cateno, partially offset by reduced volume in Cielo Brasil. The company reported a net income of R$1.9 billion in 2023, representing a 26% growth over 2022. In the quarter, net income reached R$481 million, a 5% increase from Q3 and 1.9% below 4Q22.

Cielo's IR

Regarding the acquiring yield, the year-over-year expansion reflects a better mix with a more significant share of credit cards. However, there was a drop in yield quarterly due to seasonality and customer base renewal. The company did not attribute the decline to price effects, as in the previous quarter.

Cielo's IR

Expenses totaled R$1.99 billion, up 7.6% in the quarter but down 4.0% year-on-year. This increase was impacted by total costs, with a 4% quarter-on-quarter increase in COGS and a sharp rise in operating expenses by 14.8% in the quarter and 32.4% in the year. These increases were mainly due to initiatives at Cielo Brasil, inflationary pressures on expense structures, and increased operating expenses at Cateno driven by personnel costs.

Given the limited upside to the takeover bid, corresponding to $1.07 per share for the ADR, investing in Cielo at the moment may not be very encouraging. Although minority investors may push for a higher price, recognizing the value of the acquisition and integrated banking services, the current price may be considered fairly valued.

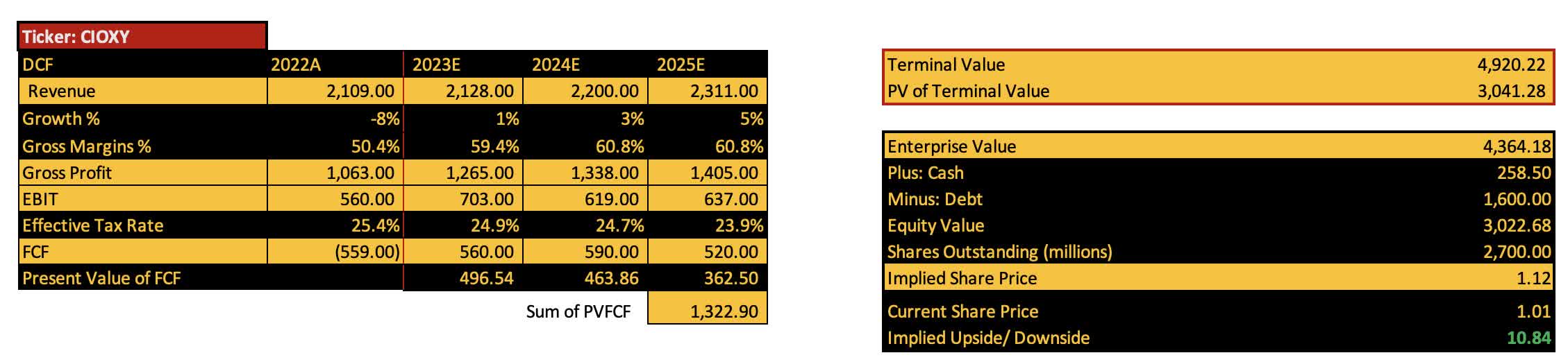

However, examining Cielo's valuations using the DCF discounted cash flow model reveals a relatively low upside potential compared to market assumptions. Incorporating a WACC of 12.7%, which includes a beta of 1.12, a risk-free rate comparable to U.S. 10-year Treasury bonds, a country risk of 4.4%, along with long-term inflation in Brazil at 3.5%, the nominal equity cost stands at 13.65%, with a tax rate of 25.4%.

S&P Global Intelligence, Koyfin, Company's filings, calculations by the author

Based on assumptions from S&P Global Intelligence via the Koyfin platform, the equity value amounts to $3.022 billion, resulting in an implied share price of $1.12, representing an upside of around 10.8%.

Additionally, when considering valuation multiples, Cielo trades at a GAAP P/E of 6.7x, significantly lower than its Brazilian peers. For example, StoneCo trades at a GAAP P/E of 26.3x, with a revenue growth forecast of 41% for 2024, and PagSeguro trades at a GAAP P/E of 13.3x, with a revenue growth forecast of 16% for the current year.

Seeking Alpha

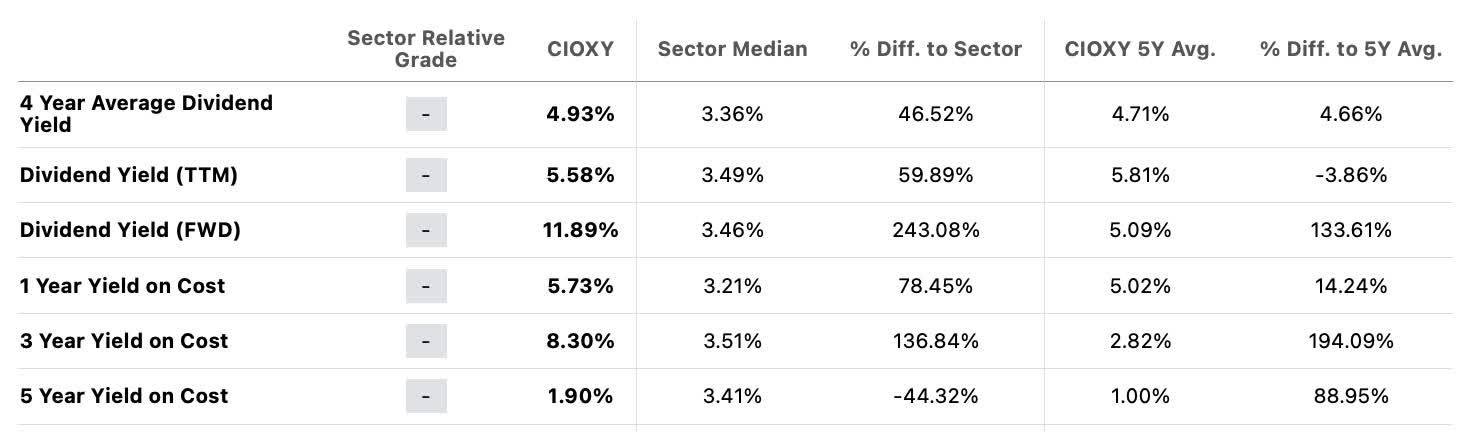

Despite these factors, Cielo's dividend potential remains a significant positive. Historically, Cielo has offered a dividend yield of 4.9% over the last four years and has a forward yield of 11.8% for the current year, making it an attractive income stock.

Seeking Alpha

Cielo once again reported weak quarterly results, indicating a continued decline in its market share within the acquiring and payments sector. However, the results were not catastrophic, partly due to the strong performance of Cateno, which boosted TPV during the quarter.

The key aspect surrounding Cielo's results is the proposed takeover bid to privatize the company at around $1 per share for its ADR, suggesting a modest upside potential. Nevertheless, this bid is expected to face resistance from majority shareholders.

Despite being significantly undervalued compared to its peers, my DCF analysis based on market assumptions indicates that Cielo has limited upside potential. Therefore, adopting a bullish stance on the company in light of the takeover bid seems risky. However, it's worth noting that Cielo could still offer robust dividends, with a potential yield of over 10%.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.