Andrew Merry/Moment via Getty Images

Andrew Merry/Moment via Getty Images

The last time I wrote on (NASDAQ:ITI) was in December 2023, and I mentioned that it has potential, but I said to wait for the breakout before entering. The breakout has finally happened, and it looks quite strong. I think ITI can be rewarding, and I will discuss the reasons behind it in this report. I am bullish on ITI, so I am changing my rating to a buy from a hold.

It recently posted Q3 FY24 results. The total revenues for Q3 FY24 were $42.1 million, a rise of 3.5% compared to Q3 FY23. Its product and service revenue saw growth, but the major reason behind the revenue growth was an increase in service revenue. The service revenue increased by 6.5% in Q3 FY24 compared to Q3 FY23. The major reason behind the growth in service revenue was the strong demand for its consulting services. The enhancements in its clear mobility platform have led to a strong demand for its service portfolio. Its gross margin for Q3 FY24 was 36.9%, which was 29% in Q3 FY23. Improved supply chain and stronger labor mix were the major reasons behind the solid margin improvement.

ITI's Investor Relations

Its net income for Q3 FY24 was $355 thousand compared to a net loss of $2 million in Q3 FY23. Even though the growth rate wasn’t significant, I still think the results were quite strong because the same quarter of last year was quite strong due to supply chain constraints in the first half of 2023. So, even the small growth suggests that the demand the company is experiencing is solid. In addition, its backlog has now reached $113.3 million, a rise of 1% compared to Q3 FY23. The improvement in the supply chain is also a positive for them because it will benefit margin expansion, which will improve the company’s profitability, and the company’s constant efforts and focus on boosting its revenue growth by enhancing its current services and products are proving beneficial for them. Recently, the management has introduced the Vantage CV system, which is used in vehicles for traffic detection and vehicle safety. They also introduced VantageARGUS CV, which will widen its service portfolio. So, the management is trying to boost its revenue growth, which is a positive sign. Additionally, despite the increased spending on R&D and the introduction of new products, the company’s balance has improved. It had cash worth $21.1 million by the end of December 2023, a rise of 27.7% compared to March 2023, and the long-term debt was reduced by 8%. So, I believe ITI is now in a strong position.

Trading View

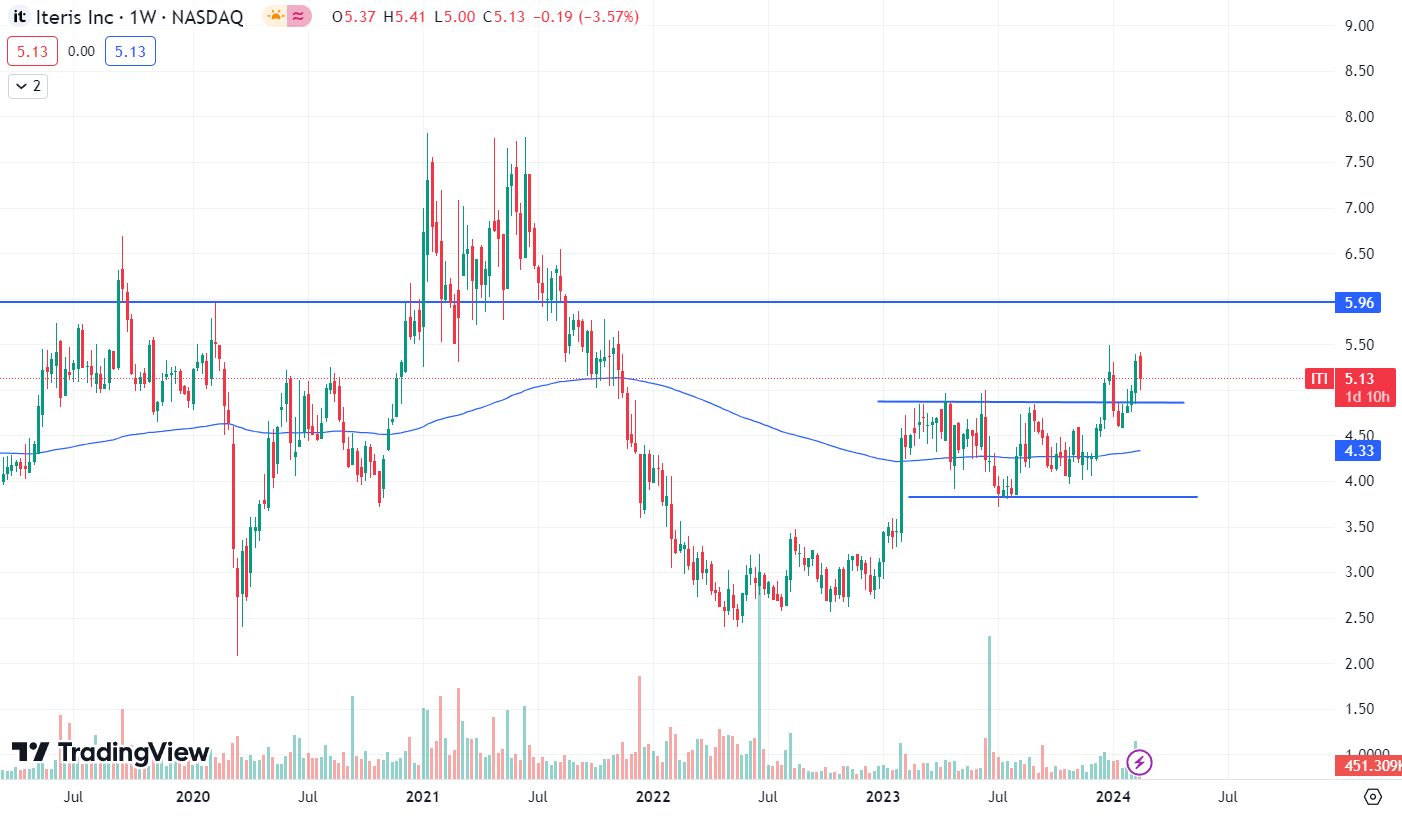

It is trading at $5.13. In my last analysis, I said that if it breaks the $4.96 level, then we might see a fresh upward momentum. Currently, the chart of ITI looks bullish with a lot of potential because it has broken the channel pattern after consolidating for about 13 months, and after the breakout, the stock price has retested the breakout level. In addition, the stock has started to trade above its 200 ema, which indicates that the stock is now in an uptrend, and I think this is just the beginning of the uptrend. Hence, I am bullish on it. The next resistance for the stock is at $5.96, which is 16% above the current level. Hence, I see it reaching $5.96 in the short term, and once it crosses the $5.96 level, then the stock can give big targets in the long term.

The current valuation of ITI looks attractive. It has a P/E and PEG [FWD] ratio of 19.16x and 0.64x, which is lower than its sector median of 25.85x and 2.07x. In addition, its sales guidance for FY24 is around $172 million, which is 10% higher than FY23 revenue. So, the positive guidance and healthy margin expectations due to improvement in the supply chain will eventually boost its EPS. So, there is a scope for P/E expansion, and I think this makes ITI undervalued. Hence, considering all these factors, I change my rating to a buy from a hold.

Their rivals often differ depending on the different product categories they compete in. The market for engineering and consulting is extremely fragmented, and quality and safety requirements are constantly changing on a regional and national level. Their rivals range in size, quantity, range, and range of goods and services provided; these include major international engineering organizations as well as smaller local or regional businesses. Their line of business, sensors, faces competition from well-established domestic and international corporations and technology. Advanced above-ground detection systems have only been adopted by a small segment of the traffic intersection industry, and their future success will depend in part on securing broader market acceptability for such technology.

Its quarterly results were positive, and the growth expectations are solid. Its balance sheet looks strong, and the valuation is also cheap. Additionally, its share price has given a breakout and might give good upside targets in the coming times. Hence, I assign a buy rating.