Olivier Le Moal

Olivier Le Moal

Intra-Cellular Therapies (NASDAQ:ITCI) flagship drug is getting a lot of love from US doctors. In 2023, the number of psychiatrists prescribing CAPLYTA, a drug used for treating schizophrenia and bipolar depression 'BD,' jumped 63%, reaching a total of 36,000 physicians. That's a lot, especially when you think about how there are only 59,000 psychiatrists in the US. Here's the kicker. The growth of prescriptions outpaced that of prescribers in 2023 (85% vs 63%). This means that not only more doctors are prescribing CAPLYTA, but those already prescribing it are doing so more frequently. This is like getting a two-for-one deal on growth for 2024. But that's not all.

Through CAPLYTA, which is already a hit in schizophrenia and bipolar depression, ITCI is eying an even bigger prize: Major Depressive Disorder 'MDD.' To understand this opportunity, one must first know what 'Label Expansion' is. Label expansion is when a drug already on the market gets a nod from the FDA to treat a new disease, in this case, MDD. The company was laying the groundwork for MDD since the very start, testing CAPLYTA for multiple diseases, including schizophrenia, bipolar depression, and MMD, all at the same time, in parallel clinical trials. CAPLYTA for MDD is near the finish line, with ITCI planning to submit a market authorization application by year-end. Sure, shooting for MDD brings more risk to the table, but I think they have a real opportunity here. It adds a high-risk/reward opportunity to the solid organic growth, which only adds to the intrigue of ITCI.

CAPLYTA's growing acceptance is creating revenue growth momentum. In Q4 results announced on February 22nd, revenue reached $132 million, up 50% YoY. Now, some might be scratching their heads thinking, 'Okay, so a biotech got FDA approval and their earnings went up. Big deal, right?' But actually, it is a big deal. Not every new drug that gets FDA approval wins over the market. More importantly, this situation gives us a chance to capitalize on market reaction or lack thereof, as everyone tries to balance the facts with anticipations of wider acceptance.

According to ITCI's annual report (pp. 7), there are 2.4 million adult schizophrenia patients in the US, where CAPLYTA is currently authorized. It is a big market. Those 2.4 million US patients? They spend $12 billion at the pharmacy each year, according to a 2019 study. Most of the spending is covered by insurance, but the point is that with $462 million in sales in FY 2023, ITCI has some room to grow. So, expanding market share is one leg of my bullish case here. But here is where things get interesting. Schizophrenia drugs are divided into two classes according to their impact on dopamine. You've got first-gen antipsychotics 'FGA' that go all-in against dopamine, and then there are these newer, second-gen 'SGA' meds that are a bit gentler. Now, the industry is slowly shifting towards SGA drugs. The transition is slow because some physicians, like Dr Ken Lundow, are not fully on board. Dr. Lundow raised questions about the effectiveness and cost-benefits of CAPLYTA and all SGAs as a drug class on his YouTube channel. And he has a point. Whether SGAs are more effective than FGAs is actually an ongoing debate. But this also creates an opportunity. To understand how let's discuss ITCI's botched clinical trial in 2016.

ITCI ran a trial directly comparing CAPLYTA with Risperidone, another SGA, and they quickly regretted it when the latter showed better efficacy. Still, the FDA authorized CAPLYTA at the end. Why? It comes with fewer side effects.

Generally speaking, SGAs, including Risperidone, for that matter, are considered safer than the older FGAs, so the current trend is leaning toward this drug class. By buying ITCI, you're buying into a slow but steady industry shift, joining the side of some of the most prestigious medical associations in the US, including the American Psychiatric Association, which encourages physicians to consider SGAs in its standards of practice guidelines. Sure, the trend is slow, but on the flip side, you haven't missed it yet.

Bipolar disorder is more common than schizophrenia, and on average, bipolar patients spend about the same as schizophrenia patients. So, you're looking at quite a large market, leaving much room to grow. ITCI doesn't divide its sales by disease, but that hardly matters to our hypothesis because, with $464 million in sales, it is clear they haven't scratched the surface in either market. There are twelve SGAs that treat schizophrenia and bipolar, other than CAPLYTA, and most have been great hits, with multi-billion dollars in sales, at least before losing their patent exclusivity (today, only three SGAs are branded products, which gives CAPLYTA additional moat). So, when we look at CAPLYTA, it feels like it has a solid chance of being a blockbuster drug, too.

ITCI spends a lot on SG&A. 90% of its sales went on this account in 2023. Add in R&D and you're down $140 million in losses for the year. But this is pretty normal when you're launching a new drug, especially when it's your first. I've seen some comments questioning the viability of the business after looking at these figures. I'm aware that some analysts and investors are worried about things like ITCI's marketing campaigns dragging on too long or that revenue is tied to continued ad spending. But, honestly, I'm not convinced. Ads are important at the beginning, but then the brand becomes established, so ads and revenue are not as tied together. Then, a significant portion of the marketing expenses goes into educational campaigns for physicians, which also become less critical with time. The expense figures also exacerbate the scale of the educational campaign because of high wages. ITCI currently advertises several 'Account Manager' vacancies with a base salary of a quarter of a million dollars, just about the average pay in the sector.

ITCI's position as a one-product company exacerbates these worries, putting everyone on edge in light of its net losses. The big question on everyone's mind is whether this little biotech can achieve economies of scale or if getting snapped by a biotech heavyweight is the only way forward. And with every schizophrenia-focused acquisition, like Bristol-Myers Squibb's (BMY) purchase of Karuna (KRTX) or AbbVie's (ABBV) acquisition of Cerevel (CERE), both happening last December, ITCI's prospects of finding a partner feels dimmer.

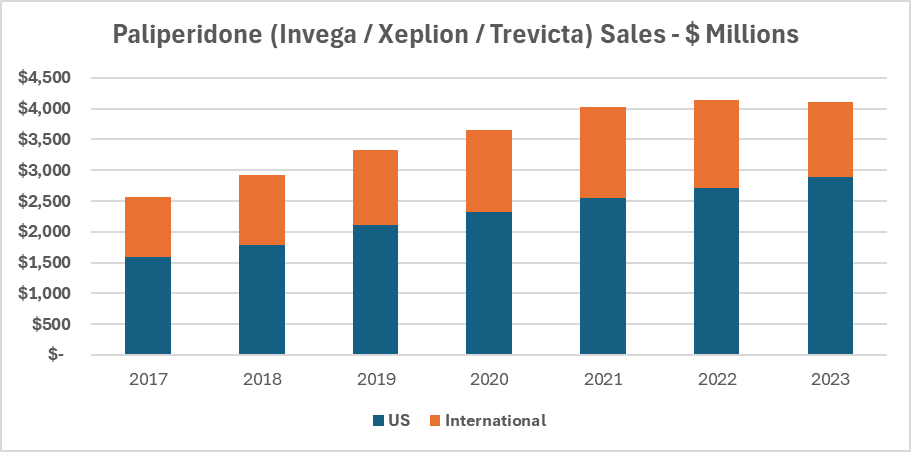

But other biotech companies started with only one product, some of which even started with a schizophrenia drug. One example is Sumitomo (OTCPK:DNPUF), a Japanese company that has found its fortune in the US. Its schizophrenia/bipolar drug, Latuda, was its primary breadwinner after its FDA approval in 2011, generating almost all sales. But since then, they branched out. As of March 2023, DNPUF generated $2.8 billion in sales, with Latuda contributing only 36%, and while the loss of exclusivity has created sales headwinds in its FY 2024 (which ends March 2024), they are still standing with a diversified portfolio and $2.3 billion in TTM sales. I imagine ITCI's path is similar to Sumitomo's and hopefully even better. Here's why I'm hopeful. Invega, a schizophrenia drug developed by Johnson & Johnson (JNJ) in 2006, lost its patent in 2015, but by that time, they already had two different formulas of the same drug, but as injections, called Xeplion and Trinza, administered every two and three months respectively, instead of the more common daily pills, making it easier for patients to stick to the treatment course. Both still enjoy patent coverage to this day, and sales are just spectacular. Just look at the chart below. Now, I think ITCI could be heading for a similar success story as JNJ's Invega, especially with its own injectable version in the pipeline.

JNJ. Table created by the author

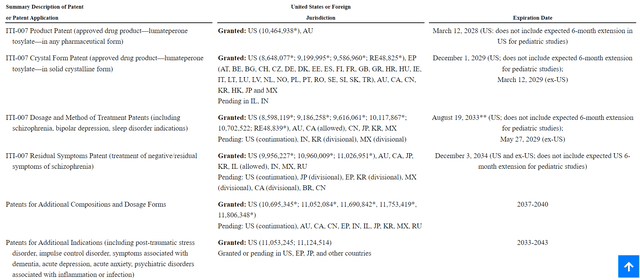

Now, I think we have a clear picture of where ITCI stands in the market. But what is the company's worth? In the pharma industry, the average net income margin is around 20%. You might see ITCI flashing a gross margin of 93% and think your Christmas has come early. But the thing is, biotechs run an ice-cube business model. They always have to put money into the business to replace drugs that go off-patent. ITCI has until 2033 before CAPLYTA's patent - in its current form - expires. It still has time, and yes, I am aware that some fellow analysts are worried about ITCI's exclusivity protection, which I think is just a small mix-up because the company decided to show off its New Chemical Entity 'NCE's' protection in its annual reports. Let's move this out of the way before we roll on valuation.

NCEs are granted by the FDA for companies whose active ingredient is novel and runs for five years starting the day a drug is approved. It is not a patent. Just an internal FDA policy to encourage innovative biotechs by adding an extra layer of protection. While showing off the NCE, they mentioned it expires in December 2024, which is expected, given that NCEs are only for five years and CAPLYTA was approved in December 2019. According to ITCI, the Base Product Patent expires in 2028. The Crystal Form patent, which means its form as a pill, expires in 2029. The Dosage and Method of Treatment patent expires in 2033, and I am yet to see a generic pharma company conducting dosage-determination clinical trials instead of waiting for established patents to expire.

ITCI Patents (ITCI)

Anyway. Back to our 20% net income margin assumption. With all the work ITCI has done with CAPLYTA and its promising phase three MDD trial this year, hitting $2-$3 billion in sales doesn't sound like a fairy tale. Crunch the numbers, and you're looking at $400 - $600 million in net income.

Now, here's something to chew on. The company didn't issue any new shares in 2023. That's not just good news financially. It shows management is serious about not diluting shares and running a self-sustaining business.

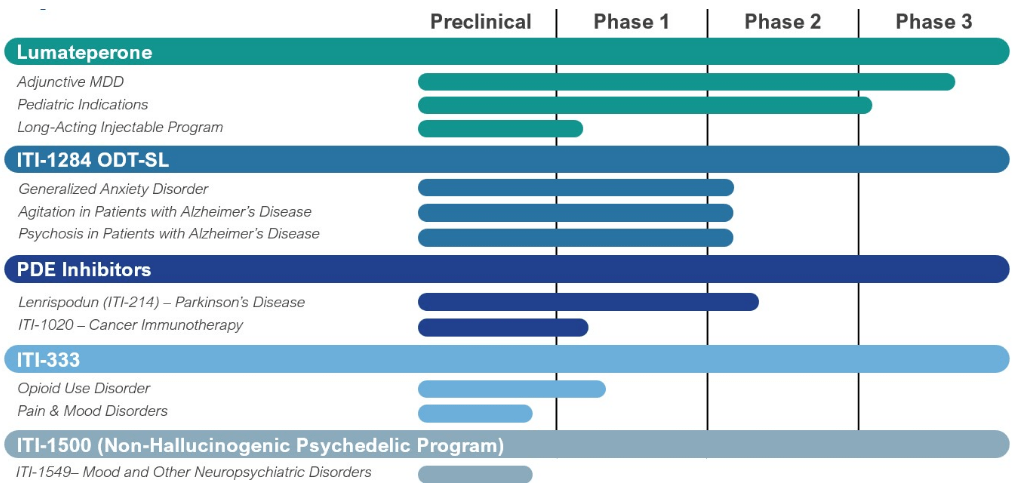

So, this $400 - $600 million in net income translates to an EPS of $4 - $6. So, with these figures, the current share price of $64 doesn't look expensive at all. Wall Street analysts see an EPS of $1.2 in 2025, based on $1 billion in sales. That translates to an income margin of 10%, which means they think operating expenses will increase by roughly 40% from $580 to $820 million. Maybe they're right, but it surely leans on the conservative side. Say ITCI has two pivotal studies in 2025; likely the two that completed phase 1 trials; CAPLYTA for Pediatric patients and the ITI-214 PDE inhibitor program. That's $200 - $250 million on R&D. The remaining $570-$620 million goes to SG&A, up about $170- $220 million (45%-55%) from what the company spent in 2023.

One might ask, between now and the time ITCI starts making money in 2025, are they going to need to raise capital? I don't think so. ITCI ended Q4 23 with a cash stash of ~$500 million (and no debt.) Operating cash outflow was just $124 million, and their net loss was $140 million. Sure, they're in the red, but not that deep compared to the cash on hand. Equally important, things are improving. In 2022, operating cash outflows were $270 million on $240 million in revenue. Last year, outflows improved: $124 million on $464 million in sales.

But there is no denying it. Part of this thesis is a pitch to take on this risk before breaking even for the potential for extraordinary gain.

ITCI Pipeline (ITCI)

One might ask, what's my downside risk? What if MDD doesn't get approved? This situation will surely limit the market scope. But the impact is multi-faceted and not entirely negative.

If the MDD program fails, less money will be spent on it. This is significant because the lion's share of ITCI's R&D budget goes to the MDD program. Sure, the loss of the opportunity is a setback, but CAPLYTA's existing markets - schizophrenia and BD - are huge. Many antipsychotic drugs became blockbusters without MDD. Risperidone (Risperdal) generated $1.3 billion in 2013 (about $1.8 billion adjusted for inflation) before losing its patent, despite all the bad publicity regarding its side effects. Olanzapine (Zyprexa) by Eli Lilly (LLY) brought in $5 billion by 2010, just before losing its patent in 2011.

Because of this, if the MDD trial doesn't go as hoped, ITCI will shift its focus to other low-hanging fruit opportunities, such as international markets and the injectables program for CAPLYTA. Comparing this to Invega and its injectables, Xeplion and Trevicta, which generated $4.5 billion last year (see chart above), even a conservative estimate of achieving half of Invega's sales suggests a bright outlook. This could mean about $2.25 billion in sales for CAPLYTA.

Axing the MDD program would also push margins at the higher end of the industry's range, potentially 30% income margin or even higher. Crunching the numbers, you have a net income of roughly $675 million. This translates to an EPS of $7, which, based on current prices, is a PE ratio of 9x.

So, yes, the loss of MDD is a setback, but the price reaction will likely be disproportional and temporary. My trading plan is to keep a foot in ITCI but also keep some cash ready to buy more if the MDD program bites the dust and the market overreacts. The price I'm paying for this is that I'm risking missing out on the portion of my capital not invested in ITCI if the MDD program gets the thumbs up and shares jump. In this case, I will also buy shares using the cash put aside for the failed MDD scenario, but now I will buy at a higher price. Now, you can do this with the same risk/reward dynamics by trading options, but that's not my forte.

So, how did ITCI perform against its strategy in Q4? Their revenue increased by 50% compared to last year, which is a bit less than the growth they had in the earlier quarters. But this is natural. The bigger you are, the harder it is to keep growing at such rates. Sales stood at $132 million, about $3 million less than what Wall Street expected, but they redeemed themselves with an above-consensus EPS. The company seems to have slowed down its hiring, and most of the discussion during last month's call revolved around the 50 sales reps hired late Q1'23 and early Q2'23. They are pretty happy with their ad campaigns and are planning a new one for next quarter.

Cost-wise, SG&A didn't really change from the last quarter but was up 10% YoY. Still, when you look at how much they grew, there are strong signs of economies of scale in play here. R&D stood at $51 million in Q4'23, up from $35 million in Q4'22, since they're pushing forward with their clinical trials. Clinical trials often cost more as they progress.

Management's main focus is to get CAPLYTA approved for more indications, with MDD being at the top of the list. We should get an update on their phase 3 clinical trial next month, and if things go as planned, ITCI will likely submit an NDA before year-end.

It is not every day that you see a small biotech not only get a foot in the door but kick it wide open. Forget for a second about its potential label expansion and the buzz around MDD trial results. CAPLYTA's momentum is already spectacular and points to a blockbuster potential (+$1 billion in sales) based on its approved conditions: schizophrenia and BD, two chronic diseases that require long-term treatment, which means a steady cash flow. And check this out: most drugs in CAPLYTA's league (the SGAs) were blockbusters. Its 86% revenue growth to $464 million in just one year is a trend mostly reserved for blockbusters. And the opportunity gets more attractive with the massive market size of schizophrenia and BD. So, whether MDD succeeds or fails, ITCI still has a good shot. With a little trading strategy to manage risk, you can make the ticker work well for you.