BlackJack3D

BlackJack3D

When I last wrote about AST SpaceMobile (NASDAQ:ASTS) in June 2022, it was planning to launch its Blue Walker 3 (BW3) test satellite later that year to be followed by field tests involving a mobile handset to communicate in a region of the Earth devoid of cellular connectivity.

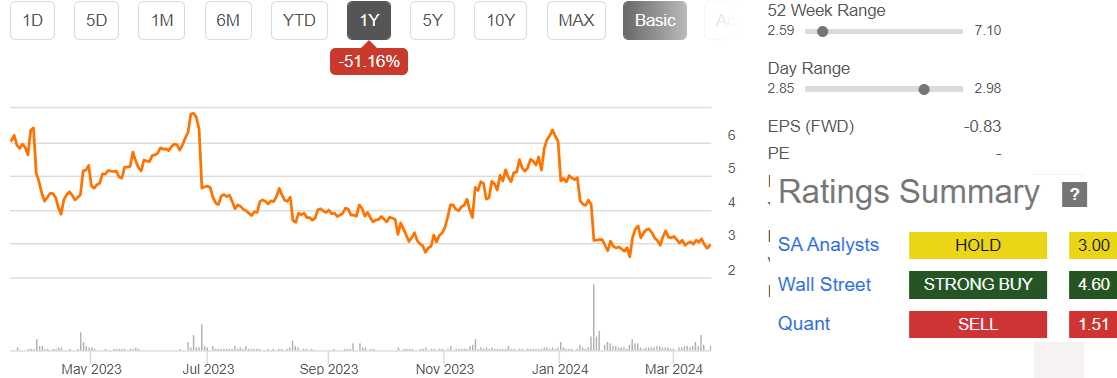

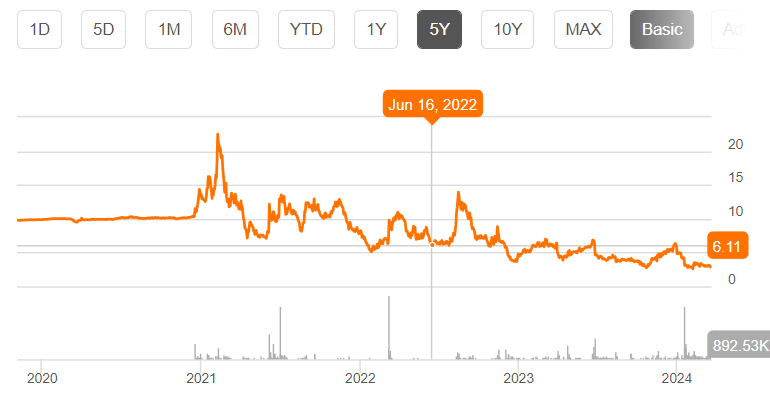

Since then, progress has been made toward commercialization, and, this thesis aims to show that it is a Buy. As such, Quant rates it as a sell, but this does not factor in the above-$300 million infusion of capital from strategic investors. As shown in the chart below, the stock was trading at under $3 at the time of writing, or well underneath its 52-week high of $7.1.

seekingalpha.com

I start by providing an overview of the industry.

First, to put into perspective the BW3 venture is analogous to setting up telecom towers in space, for relaying 3G, 4G, and 5G signals from MNOs (mobile network operators) directly to commonly-used smartphones. Such space-based connectivity allowing for voice and data communication between a standard smartphone and a satellite is something new in the sense that previously you needed either specialized satellite phones provided by the likes of Iridium (IRDM), or a smartphone equipped with a particular type of modem made by Qualcomm (QCOM) for the iPhone 15. Moreover, in both cases, the bandwidth is restricted, in contrast to ASTS's ability to offer fifth-generation cellular wireless.

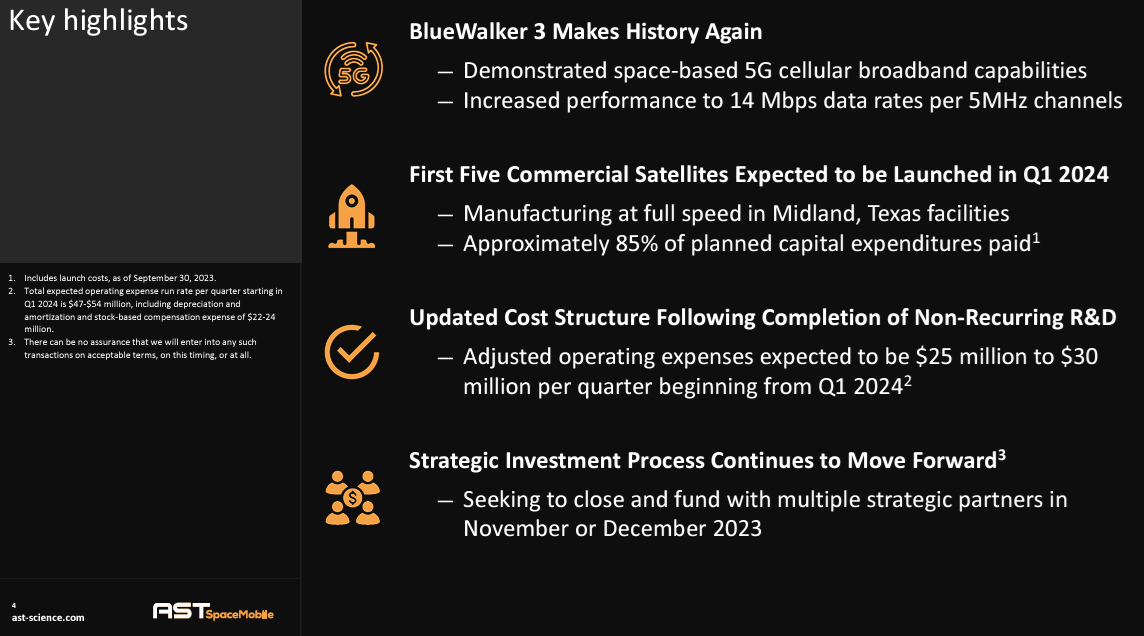

Looking further, Elon Musk's SpaceX (SPACE) beams internet from space but you first need to capture the internet signal using an antenna before making it accessible to your phone through Wi-Fi. On the other hand, with its direct-to-phone access, the ASTS approach is different, and in September last year, its engineers were able to place a call from Maui in Hawaii to Madrid through the BW3 test satellite. Also, looking at its broadband capabilities, it has achieved a download rate of about 14 Mbps (megabits per second).

ASTS Investor presentation (irp.cdn-website.com)

Now, this does not appear much considering that Starlink (STRLK) offers between 25 and 220 Mbps, but, you do not need any antenna. Also, taking into account that less than 50% of America's territory is covered by cellular networks offering download speeds greater than 7 Mbps, then you realize ASTS's direct-to-device potential since 14 Mbps is above the minimum speed for streaming videos, videoconferencing, or playing games.

These positive tests helped to prop up the stock to the $6.3 level from October to December as shown in the introductory chart, but soon afterward it lost all its gains and fell to around $3 in January and two reasons may account for this.

First, competition has emerged in the form of Lynk Global. This is another satellite-to-phone developer describing itself as the "world's only patented, proven, and commercially licensed satellite-direct-to-standard-phone system". The company already has satellites in space, has done tests, and has an agreement with Turkcell (TKC), a large Turkish wireless operator.

Noteworthily, Lynk signed a letter of intent to go public through a SPAC merger with Slam Corp. (SLAM) in mid-December last year and is backed by venture capitalists. Being publicly listed would significantly increase the amount of capital it has access to, making it a serious competitor for ASTS.

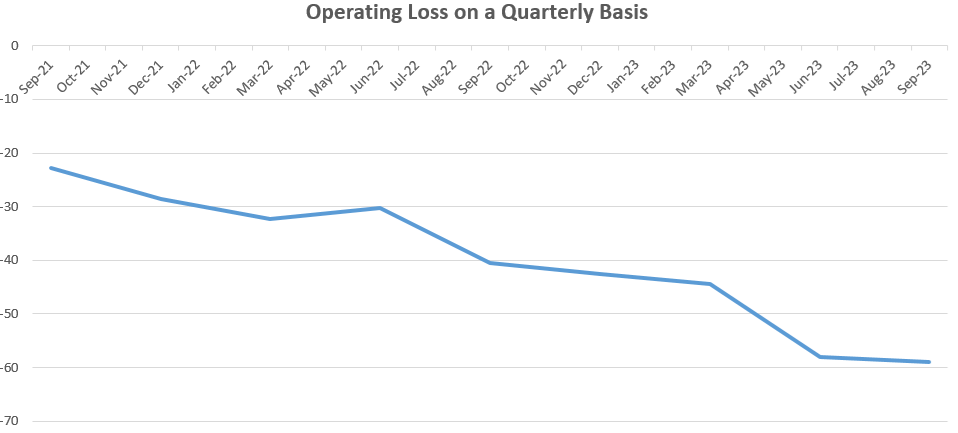

Second, volatility could also have been caused by financial results for the third quarter of 2023 (Q3)where earnings per share of -$0.23 missed by $0.02. Now, this is a loss-making company (chart below) as not only it does not generate sales but has been spending money to develop BW3 and five other commercial satellites. On top, it had to spend an additional $5 million mainly because of a potential customer requesting a change in orbit inclination for better coverage of its subscriber base.

Chart built using Income statement data (seekingalpha.com)

Now, while meeting project milestones in terms of testing is certainly positive, things like delay and additional costs adding on to what had initially been planned are not well viewed by financiers and investors alike. Also, the fact that the first five commercial satellites were expected to be launched in Q1-2024 and it is already March 21 may add to some uncertainty as to whether there is a delay.

Furthermore, a delay can imply additional expenses and adversely impact the balance sheet, especially for a company that had cash and equivalents of $135.7 million against $71.9 million of debt at the end of Q3. Along the same lines, it has already consumed $159 million of cash for operations in the trailing twelve months for a project already costing about $700 million in total since 2017.

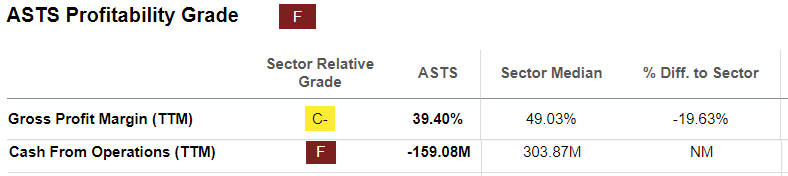

In these circumstances, ASTS obtains an F for profitability grade, largely explaining why it is rated as Sell along with the momentum factor which appears not favorable at the moment.

However, things have evolved positively on the financial front recently.

To this end, strategic partnerships with companies including American Tower (AMT), Vodafone (VOD), Rakuten (OTCPK:RKUNY), AT&T (T), Bell Canada, and Alphabet (GOOG) are now valued at $306.5 million, an amount which will be used for expanding the fleet to 72 satellites in one year. Now, depending on the timing of the inflow, this could boost ASTS's profitability grade, by improving both gross margins and cash from operations as shown below.

Profitability grades (seekingalpha.com)

Continuing on a positive note, a successful launch by SpaceX could play in ASTS's favor and constitute a catalyst for an upside.

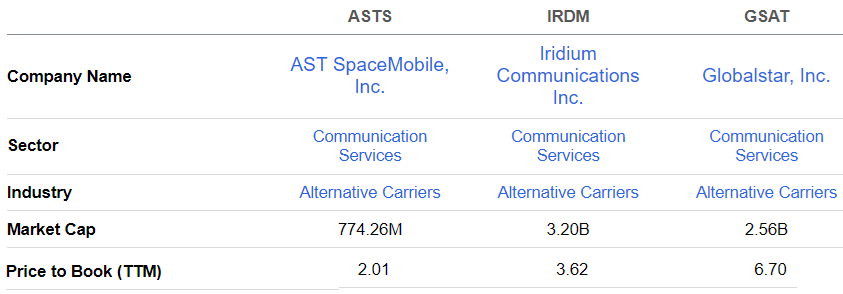

As for valuations, I perform a comparison of the company's price-to-book multiple with peers as shown below. Now, the book value is obtained by a company's total assets minus liabilities but does not take into account the value of its intellectual property portfolio which includes 3,100 patents and related claims worldwide. Thus, it deserves better, and, adjusting ASTS's share price of $2.95 based on its lower P/B of 2.01x relative to Iridium's 3.62x, I obtained a target of $5.29 (2.95 x 3.62/2.02).

Comparison with peers (seekingalpha.com)

In this respect, some may view these partnerships as diluting the shares since in return for investing, the above five companies now own 20% of ASTS, but these have allowed the satellite play to pursue the commercialization phase without resorting to the debt markets at a time when interest rates are high. Moreover, they are a testimony of confidence especially in light of its direct competitor.

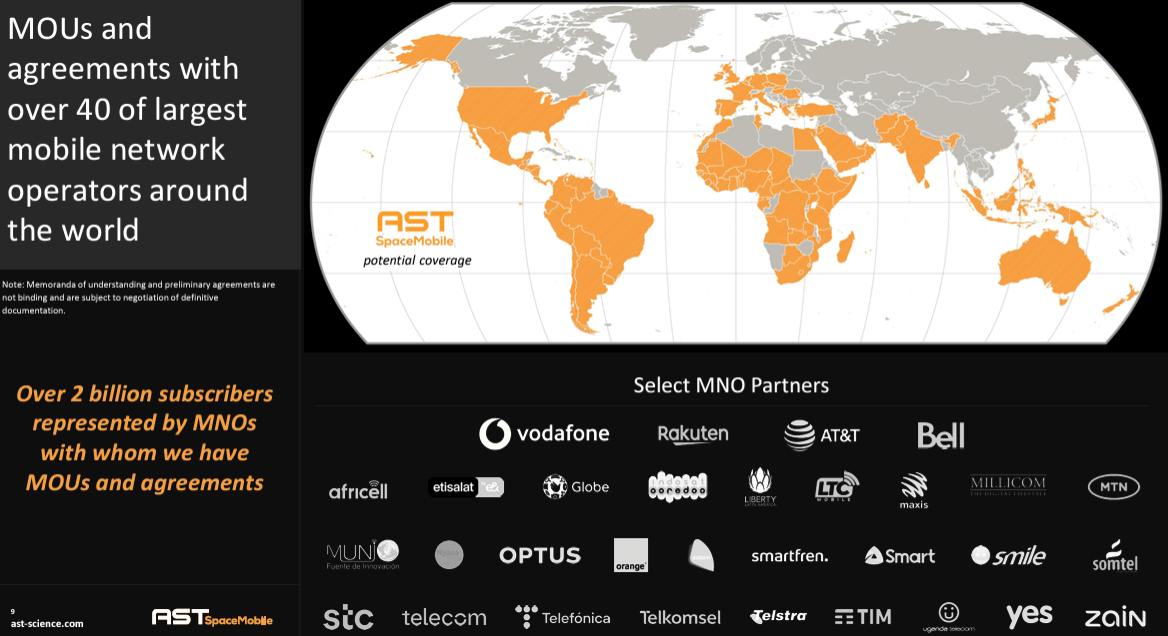

In addition, the company has signed a memorandum of understanding (MoU) with 40 MNOs across the world, one of which is Globe Telecom (OTCPK:GTMEY) (OTCPK:GTMEF) of the Philippines which is contemplating to use of satellites as an alternative to expanding its tower footprint across all of the country's island together with the required fiber backhaul. These are geographies where the cost of terrestrial infrastructure can be more than 9.5 times the cost of space-based communications as I had calculated in my previous thesis and there are many such places on the Earth where there are gaps in cellular coverage.

irp.cdn-website.com

Tellingly, these operators cover over 2 billion subscribers. Now, learning from Vodafone which intends to provide broadband services (like video calls, Internet browsing, e-mail, music streaming, and social media) to its subscribers wherever they are located, there are many use cases where operators can extend their cellular network through AST's constellation.

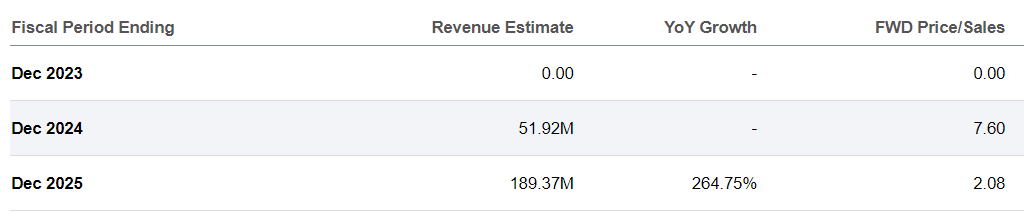

Extrapolating further, if only one-thousandth of the 2 billion potential subs opt for space-based connectivity in 2024, this comes to 2 million, and assuming ASTS obtains a $25 cut per plan, this comes to $50 million. This is nearly in line with the $52 million of revenues expected by analysts for this year as pictured below.

Revenue estimates (seekingalpha.com)

Now, I mention a $25 cut as ASTS will more likely work out a revenue-sharing scheme with the local carrier which owns the frequency spectrum together with mobile cellular infrastructure. The figure may appear on the low side, but one must bear in mind that mobile subscription plans vary widely across the globe and, additional ground-based infrastructure is needed for end-to-end connectivity. To this end, ASTS has partnered with Nokia (NOK).

In conclusion, this thesis has a Buy position based on the value of its technology (phase-based cellular broadband network) and patents which allow a commonly used phone to communicate in a region devoid of cellular coverage. In this way, a phone neither needs to be equipped with specialized modems like Apple's (AAPL) iPhone communicating through GlobalStar's (GSAT) constellation of satellites for emergency calls nor does it require the subscriber to first hook an antenna to the rooftop as is the case with Starlink. Moreover, with commercialization planned for this year, the revenue inflows should positively impact the income statement. To this end, adjusted operating expenses are projected to be reduced from $37 million-$40 million per quarter to $25 million-$30 million per quarter, at the beginning of the first quarter of 2024.

However, beware that the price target of $5.95 constitutes nearly an 80% upside, but, going forward, beware of the higher degree of volatility with the emergence of direct competitor Lynk, especially if it manages to persuade one of the MNOs which signed an MoU with ASTS to switch. Looking at past performance, I had a bullish position when I covered the stock back in June 2022 and the stock did rise to the $14 level from $6.11, but, subsequently, it dropped to below $5 as charted below. Also, do note that as a tech stock, a tighter-for-longer monetary policy may also adversely impact performance.

www.seekingalpha.com

My last thought goes to the balance sheet where the management reckons it has already reached the point of maximum spending or 85% of what was planned for building and launching satellites. Therefore, with partnership money flowing together with the commercialization phase reached, there should be an improvement in finances as the management executes.