Onfokus

Onfokus

iRobot's (NASDAQ:IRBT) path has diverged from previous expectations, in part, due to the terminated transaction with Amazon. The expectations were high that the deal with Amazon (AMZN) could boost sales. The offering price of $61 per share and the corresponding 22% premium to its share price showed just that. The expectations that Amazon could be a significant lever for iRobot were high. However, regulatory hurdles ended up killing the deal, which left the company to face challenges in the form of lower sales and intense competition, affecting revenue and leading to operating losses. The only bright spot in this whole deal is the $94 million termination fee.

At this point, the thesis for this stock is an old-fashioned turnaround, with its consumer brand serving as an anchor while the management streamlines the organization and the product portfolio to stabilize sales and return to profits. We have seen other examples where this strategy worked, Apple (AAPL) comes to mind. Nevertheless, for technology-focused consumer brands, these types of turnarounds pose more risks, and Nokia (NOK) comes to mind.

Now that the dust is settling, the company is trying hard to stabilize the business and support long-term growth. The company stated in its 4Q23 earnings call that the main goal is to simplify the cost structure and concentrate on core value and revenue drivers. In other words, the company wants to refocus on its most profitable segments and geographies.

The company is now releasing a plan to improve gross margins, it calls it "design to value," which is basically about removing unnecessary expenses and trying to squeeze better terms from manufacturing partners.

The restructuring will also entail reducing research and development (R&D) expenses by reducing non-core engineering positions and increasing reliance on third parties for some R&D efforts. The cuts in R&D should enable it to decrease overall R&D expenses by approximately $25 million in 2024. The OpEx is also clearly over-dimensioned to the current business level. The goal here is to reduce overall sales and marketing expenses by approximately $40 million in 2024. Both the R&D and OpEx streamlining will result in a workforce reduction of approximately 350 employees, 31% of its total workforce.

The goal of the restructuring is to improve gross margins by 9.5 to 11.5 percentage points in 2024, according to the management team in the 4Q23 earnings call. The company targets a gross margin of 32% to 34% for fiscal year 2024. The company is looking at liquidity as a top priority, aiming for significant improvements in cash flow in 2024.

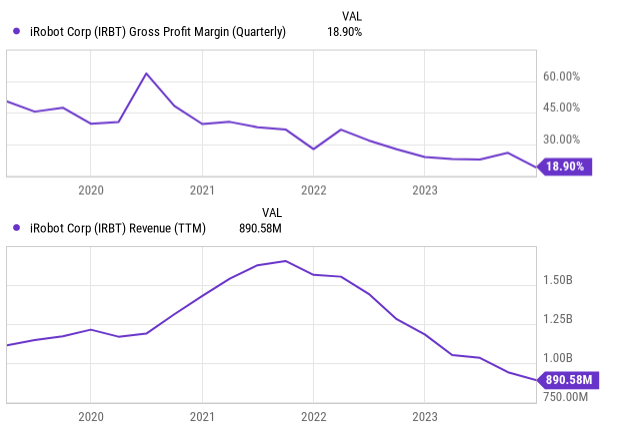

The company experienced a 14% decline in revenue in the fourth quarter of 2023, totaling $308 million. That came hand-in-hand with a significant decline in the gross margin to 19% in the fourth quarter, down 5 percentage points from the previous year. The decline is explained by higher promotion activity and fewer sales to dilute the fixed costs. Inventory management was also a headache.

YCharts

In order to partially offset these negative trends, the company was able to get a 30% reduction in operating expenses to $104 million, 34% of revenue. In any case, it wasn't enough to avoid a $45 million operating loss or a net loss per share of $1.82.

For the full year, the balance is a 25% revenue decline to $891 million, while the annual gross margin also declined to 22.5%, a 7-percentage point drop from 2022.

For 2024, the gross margins are projected to significantly improve to between 32% and 34%. Operating costs are projected to fall between $322 million and $340 million, approximately 39% of revenue, while the full-year operating margin should be negative 5% to negative 7%. There's a special note to the plan to file for a $100 million at-the-market offering program as part of their liquidity management efforts.

At this stage, this company is basically a turnaround play. The company will try to reignite its operations through its brand while trying to cut wherever possible. Our estimation of the cash burn for 2023 is close to $240 million (simply adding SBC and depreciation back to the profit). I am not using the direct cash-flow figures, mostly because those are tainted by inventory reductions, and we want a normalized picture. Given that the company still has $185 million in cash plus the $94 million termination fee, that gives it a bit more than one year to close the 2023 cash burn. Again, I am not considering inventory or receivables to provide this analysis with a margin of error. The management has said it believes it will be in positive cash flow by the second half of the year.

The company is introducing cost savings targeting gross margins at the midpoint of 33% for 2024, up from 22.5% in 2023. They also anticipate operating costs in the range of $322 million to $340 million, which is a decrease from the $399 million reported for 2023. These reductions aim at a full-year operating margin of approximately -5% to -7%. These measures have the potential to reduce the cash burn significantly. However, it is implied that the revenue goes according to plan, and with all the cutting, that becomes a frail assumption in my opinion. I believe the risk lies on the revenue side of the equation.

iRobot

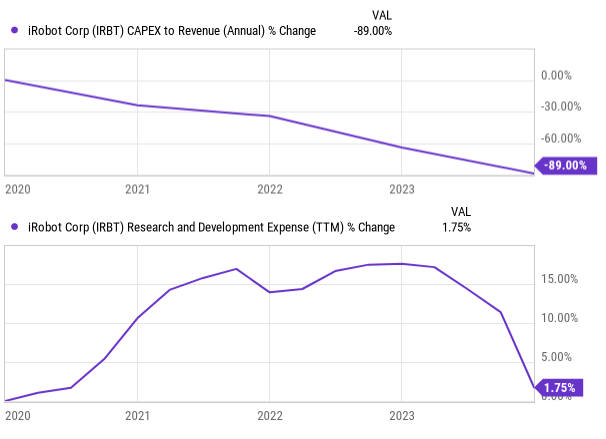

The company has already heavily slashed CapEx during the past few years. The same happening to R&D.

YCharts

At this point, I'm starting to question this whole turnaround game. How's a brand, known for outperforming rivals because customers think it's just better, going to maintain its edge when it's slashing the origin of that reputation? The big danger I'm seeing is the restructuring going too deep, skimping on essential R&D costs, and before you know it, the product's top-dog status fades away. All this while competitors now have product portfolios better than before.

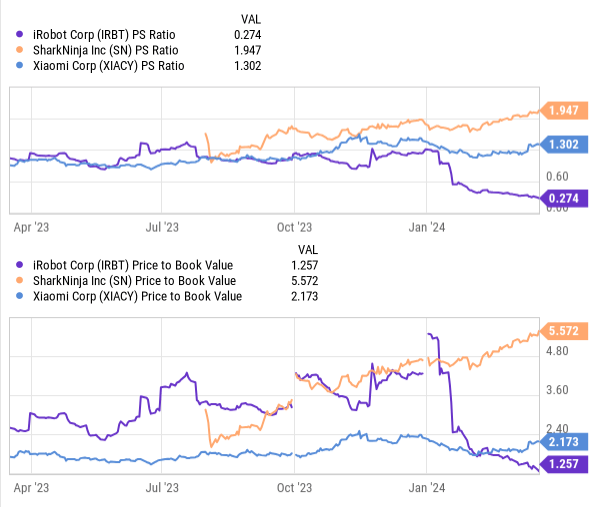

Maybe there's a silver lining here. The company's valuation is looking like a bargain compared to rivals. However, a deeper look might reveal that might not be great news. The reason iRobot is in the discount bin might be because the market thinks they are on a losing streak, bleeding profitable sales, and expected to keep sliding. And the low price-to-book value, which basically tells us that they're not keeping up on the tech front because they're not investing enough.

YCharts

In my opinion, the company faces an existential threat. The deal termination with Amazon has left them vulnerable. We can even make the point that some retailers shied away from them because of the Amazon deal, sensing the Amazon threat, which didn't exactly help sales. This assertion was supported by the CEO, Glen Weinstein, in the earnings call:

Yeah. And Jim, I'll add, I know that we have -- after we announced the transaction with Amazon in the summer of 2022, we had some retailers exit business with us, both domestically and internationally, because they viewed Amazon as a particular competitor.

There's a silver lining, though, this could be the kick they needed to trim the fat and make operations leaner. But here's the rub, for a company that thrives on being seen as the tech leader, cutting so hard on R&D could backfire. And just to add to the fun, investors have another headache to deal with. We're talking about a mixed shelf offering up to $100 million, which could further dilute their shares at possibly the worst time, with the stock hovering near record lows.

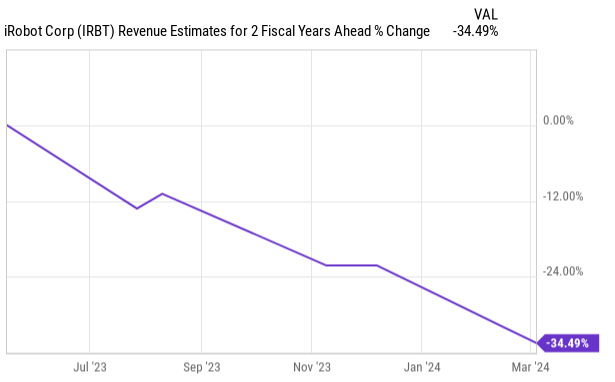

The current levels of cash, the extreme cut in R&D, the further potential dilution that hangs over the company, and the low revenue estimates for the years ahead, make me pass on this one. At this point, I don't think this is a solid enough turnaround story. It might even be considered a short to be included in a balanced long/short portfolio, with further research necessary to confirm its adequacy.

YCharts

Nevertheless, I will keep an eye on this company. Namely, I will keep looking at revenue estimations, gross margins, and R&D spending. Possible hints of a trend reversal in these metrics might warrant a reappraisal, but until then, I am on the sidelines on this one.