panida wijitpanya

panida wijitpanya

It has been over a year since my last IQVIA Holdings Inc. (NYSE:IQV) “IQVIA” article, where I defended the ticker’s premium valuations on account of it being one of the leading CROs with a multitude of services and having over 10K customers including big pharma. Since that article, IQV has chopped around but the share price has tested resistance near $240 per share following their Q4/2023 earnings with a beat on EPS and revenue, exceeding market expectations. In addition, IQVIA issued bullish guidance for 2024 where they expect full-year revenue between $15.4B and $15.65B and Adjusted Diluted EPS is expected to fall between $10.95 and $11.25. It appears as if IQVIA's strong financial performance and confident guidance defends the company as a leader in the healthcare sector. Moreover, I believe the recent earnings guidance supports the bulls and the ticker’s premium valuation.

I intend to provide a brief background on IQVIA and will discuss the company’s recent earnings reports. In addition, I will highlight some key trends that investors should keep an eye on. Then, I will present some positive points for the bulls to support the long position. Finally, I will review my current plan for my IQV position as we move deeper into 2024.

IQVIA is one of the leading players in the arena of contract research organizations (CROs), offering comprehensive services for the advancement of healthcare products through Phase I-IV clinical trials. With a client base surpassing 10K, counting the top 25 global pharma companies, IQVIA is a critical component in the future of the healthcare sector. The company operates through three distinctive segments: Technology & Analytics Solutions (TAS), Research & Development Solutions (R&DS), and Contract Sales & Medical Solutions (CSMS).

IQVIA’s TAS segment is an inexorable force in cloud-based applications and services in the healthcare sector, presenting cutting-edge analytics and commercial performance metrics for a wide array of products. The company's matchless access to commercial sales and inventory data for pharmaceutical products feeds their ability to give in-depth analysis, making IQVIA the central source for pharmaceutical market analysis.

IQVIA’s R&DS segment assists healthcare companies involved in clinical trials and related projects. IQVIA can advise and support a product candidate from start to finish in its development lifecycle including offering a broad assortment of lab services.

In the CSMS segment, IQVIA offers a suite of services tailored to support a diverse array of healthcare companies to enhance collaboration with providers, patient services, and medical affairs services.

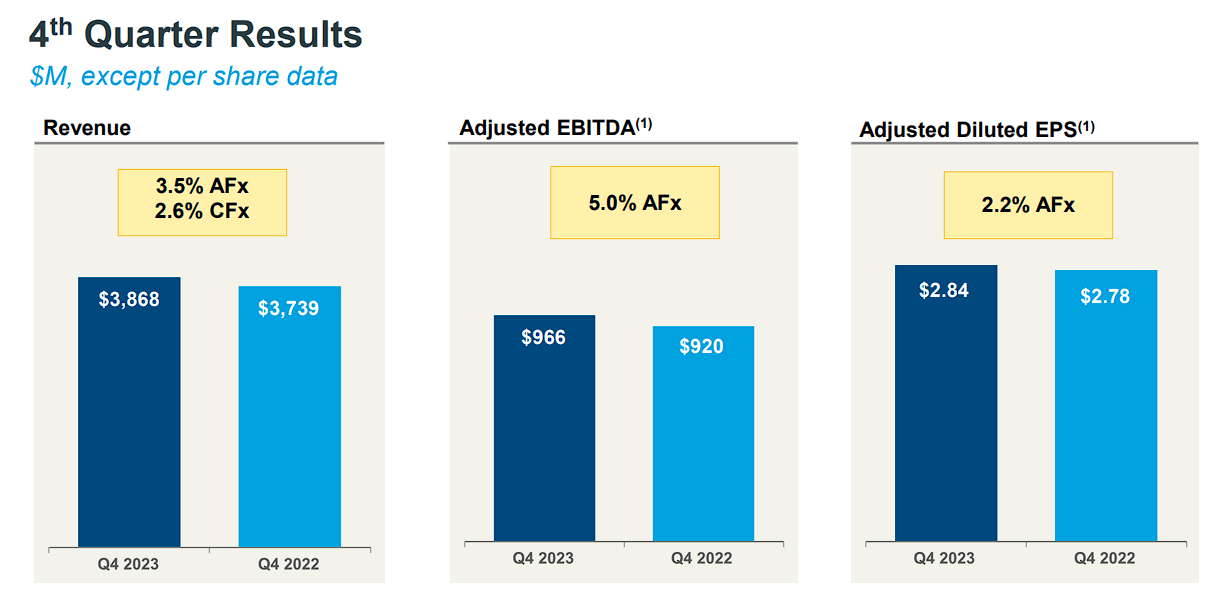

In Q4 of 2023, IQVIA recorded $3.868B in revenue, a 3.5% increase at actual foreign exchange rates, and a 2.6% increase at constant currency over Q4 of 2022.

IQVIA Q4 Results (IQVIA)

A segment-wise breakdown showed that the TAS, R&DS, and CSMS reported Q4 revenues of $1.531B, $2.151B, and $186M, respectively.

The company was able to post a Non-GAAP EPS of $2.84, beating estimates by $0.02 thanks to an impressive adjusted EBITDA of $966M and a net income of $469M. IQVIA’s balance sheet and cash flow metrics revealed the company finished Q4 with $1.376B in cash & cash equivalents, as well as $568M in free cash flow.

For the full year 2023, IQVIA's revenue moved up by 9% at constant currency, excluding COVID-related work. The company's EBITDA margin stretched, and adjusted diluted EPS surged 12%, excluding the impact of interest and tax rates. The cumulative revenue for the entirety of 2023 reached a commendable $14.984B, marking a 4.0% increase, and an annual net income of $1.358B.

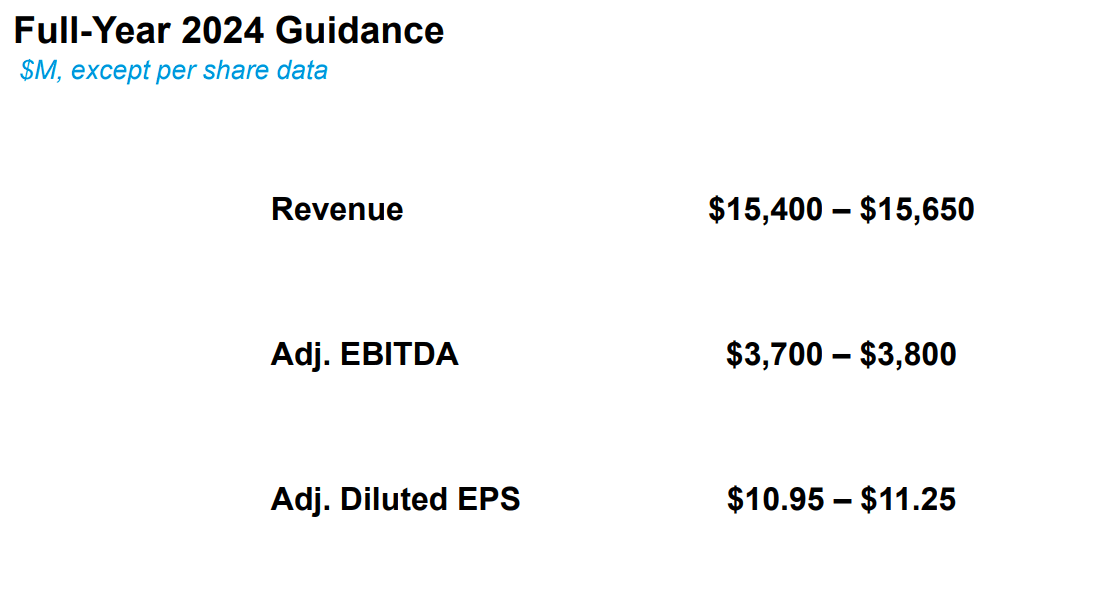

For Q1 of 2024, IQVIA expects their revenue to settle between $3.650B and $3.725B, with adjusted EBITDA falling in the $850M - $870M range, and adjusted diluted EPS coming in at about $2.45 to $2.55. For full-year 2024, IQVIA’s guidance has revenues in the range of $15.4B and $15.65B suggesting a 5% to 7% revenue growth. IQVIA anticipates full-year 2024 segment revenues for TAS, R&DS, and CSMS to be in the range of $6B - $6.2B, $8.7B - $8.8B, and $700M, correspondingly. In addition, IQVIA is looking for a recommencement of EPS growth, with adjusted diluted earnings per share expected to be up to $10.95 - $11.25, a 7% to 10% increase. Adjusted EBITDA is projected to range from $3.7B to $3.8B and continued margin expansion.

IQVIA 2024 Guidance (IQVIA)

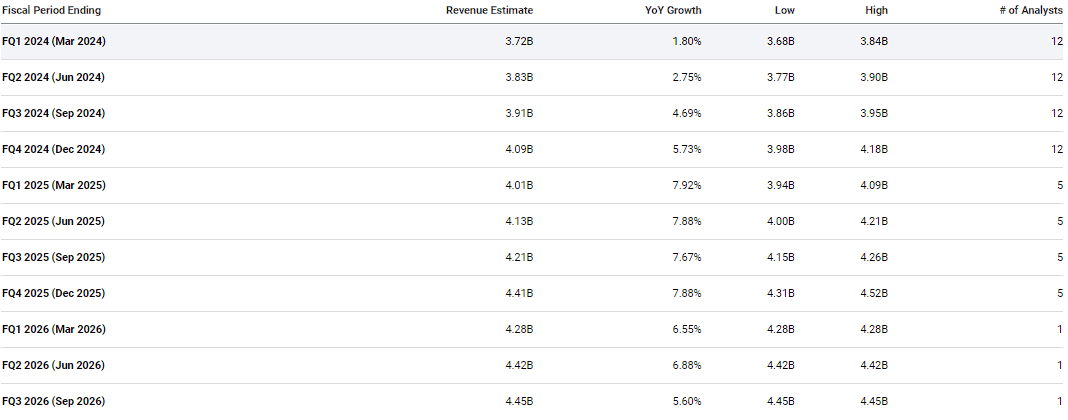

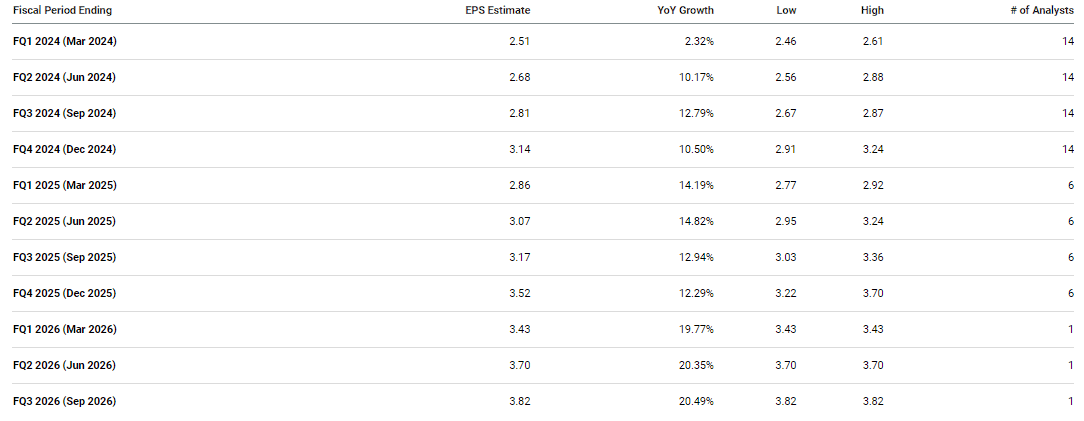

The company’s guidance does appear to match up with the Street’s expectation for IQVIA. At the moment, analysts are projecting IQVIA to report $3.72B in revenue for Q1 and an EPS of $2.51, both would be single-digit year-over-year growth.

IQVIA Quarterly Revenue Estimates (Seeking Alpha)

IQVIA Quarterly EPS Estimates (Seeking Alpha)

However, the Street also expects the growth trends to improve in the subsequent quarters with Q4 having over $4B revenue and an EPS of $3.14. Admittedly, this is not tremendous growth for 2024, but also not negligible.

When combing through the company's earnings press release and listening to their earnings call, I noted a few positive highlights and trends that IQV investors should make note of.

One of the notable positive trends from 2023 came from IQVIA's R&DS segment, which reported $2.8B in net new bookings for Q4, which was the second-largest quarter in IQVIA's history. Furthermore, IQVIA revealed that their Q4 book-to-bill ratio was 1.31x, indicating a high demand for their services from their R&DS customers.

The TAS segment has been experiencing significant headwinds due to a wary spending environment. The company explained that discretionary spending had not completely recovered. Despite these concerns, the TAS segment reported revenue growth for the quarter. In addition, there is a positive outlook for the segment, thanks to the FDA approving 55 new molecules in 2023, which is almost a 50% upturn from 2022. The company also launched new software platforms, and added 33 new clients on their orchestrated customer engagement (OCE) platform. The increased number of FDA approvals and anticipated growth in drug launches, signals potential growth from this segment in the coming quarters.

Another important trend to note is the company’s commitment to cultivating growth and expanding their capacity to serve their customers. The company has made some strategic acquisitions that will play a fundamental role in growing IQVIA's R&D abilities including clinical research coordination, study feasibility, patient recruitment, and bolstering their lab business.

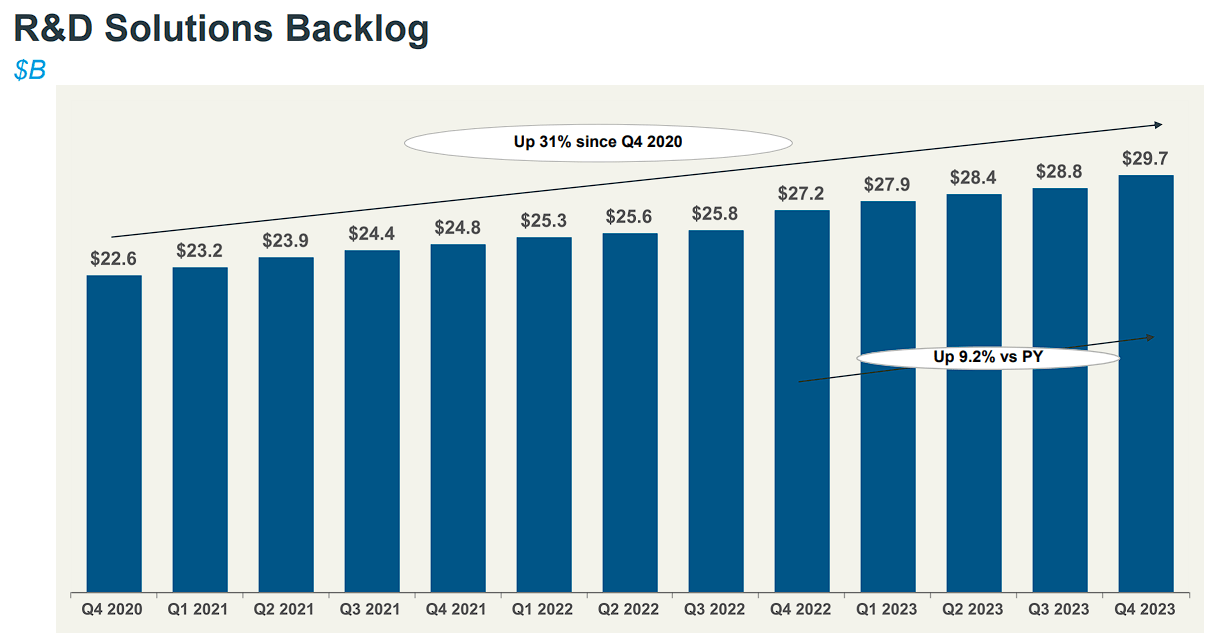

IQVIA's robust financial performance and enthusiastic guidance do point to strong trends in the CRO industry, indicating that the company will benefit from a general rebound throughout the healthcare sector. In fact, the company reported an impressive backlog of $29.7B at the end of the year, with an anticipated $7.5B expected to be converted to revenue in the next twelve months, providing reassuring revenue visibility for 2024.

IQVIA Backlog (IQVIA)

'Considering the points above, I believe the company's forward-looking guidance for 2024 suggesting revenue growth, margin expansion, and EPS growth, should be obtainable.

My IQV position has been dormant for an extended period of time, because I have been waiting for these current conditions to finally come to fruition. Not only has the company weathered the COVID-19 pandemic, but they have also made significant strides in making sure they can serve their customers who are attempting to restart their pipelines and get some programs in the clinic. As a result, I expect IQVIA to hit the Street’s expectations and IQV will follow suit.

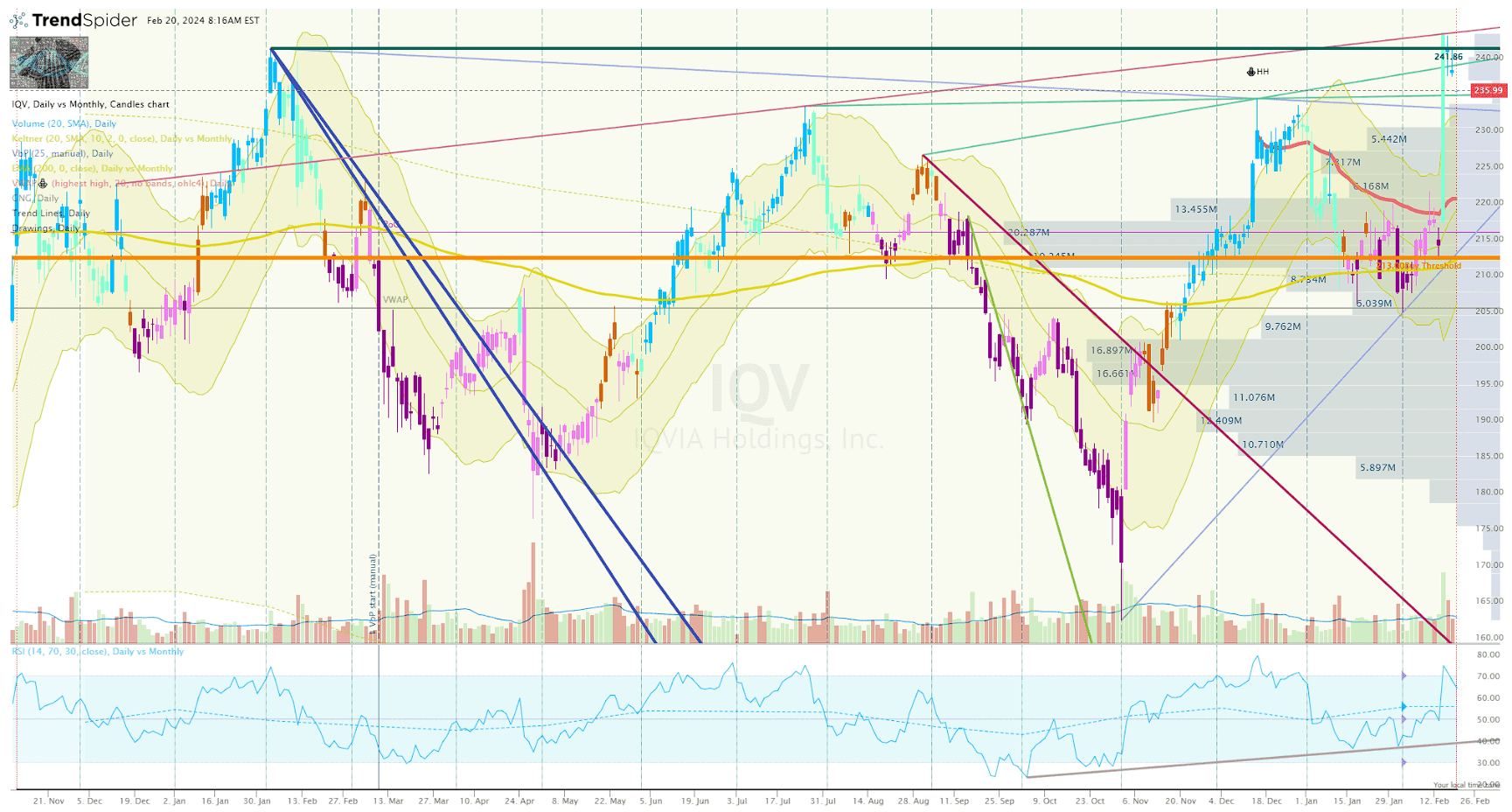

IQV is showing a nice setup at the moment with a nice double-bottom and a breakout above resistance.

IQV Daily Chart (Trendspider)

The ticker is currently trading above my Buy Threshold of $214, however, I believe I am going to have to update that level to $222 per share to adjust for the chart’s technical features. Typically, I don’t adjust my targets and thresholds solely on a single earnings report or technical analysis, but I am also considering IQVIA’s share repurchase program, which continues to provide support to the share price. At the end of 2023, IQVIA had $2.363B left in share repurchase authorization, so the company still has plenty of funds left to provide some underlying support to the ticker.

In contrast, I am sticking to my current Sell Targets to safeguard profits and return my position to a “House Money” status. However, I will maintain a small lot of shares to build a core position for a long-term investment.