skynesher

skynesher

The Interpublic Group of Companies (NYSE:IPG) is a collection of ad agencies, including storied McCann-Erickson, operating as one of the advertising majors in the listed landscape. We note positives here, including the US exposure, and the innate cost flexibility in these businesses, able to resist EPS declines despite sales pressure. Relative performance of IPG is good compared to some other listed examples, and the areas of weakness, namely tech and telco customers, could be bottoming right now and sales could get some respite next year, in addition to continued planned margin growth. The valuation is quite compelling, merely because there's a good degree of earnings yield and a relatively strong case for earnings growth to continue to be secular. The operational record impresses, and gives credence to a GARP case.

IS (Q4 Pres)

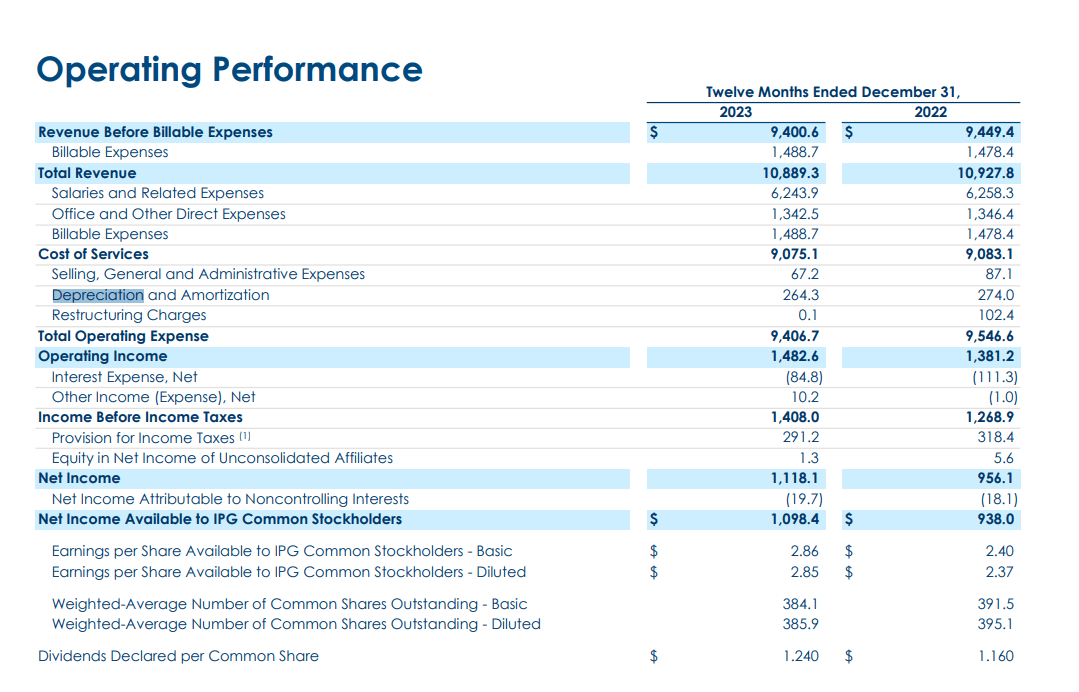

There was headline growth in revenues, but organically it was a slight decline of some 10 bps or so. In the Q4 there was both headline and organic growth just under 2%. Impressively, IPG managed growth in EPS owing to the innate cost flexibility in the advertising business, as well as a substantial cut to the SG&A line which is relatively small. EBITDA grew 11% in Q4. Almost all the expenses come from salaries and compensation, and apparently it was in benefits where they managed inflationary pressures and kept margin pressure down. Part of this was less incentive pay but also a slight reduction in headcount of a couple of percent. In all, operating income saw a clear increase, and the company is guiding to a percent or so of continued growth in 2024, and with margin improvement of around 60 bps for the EBITDA line.

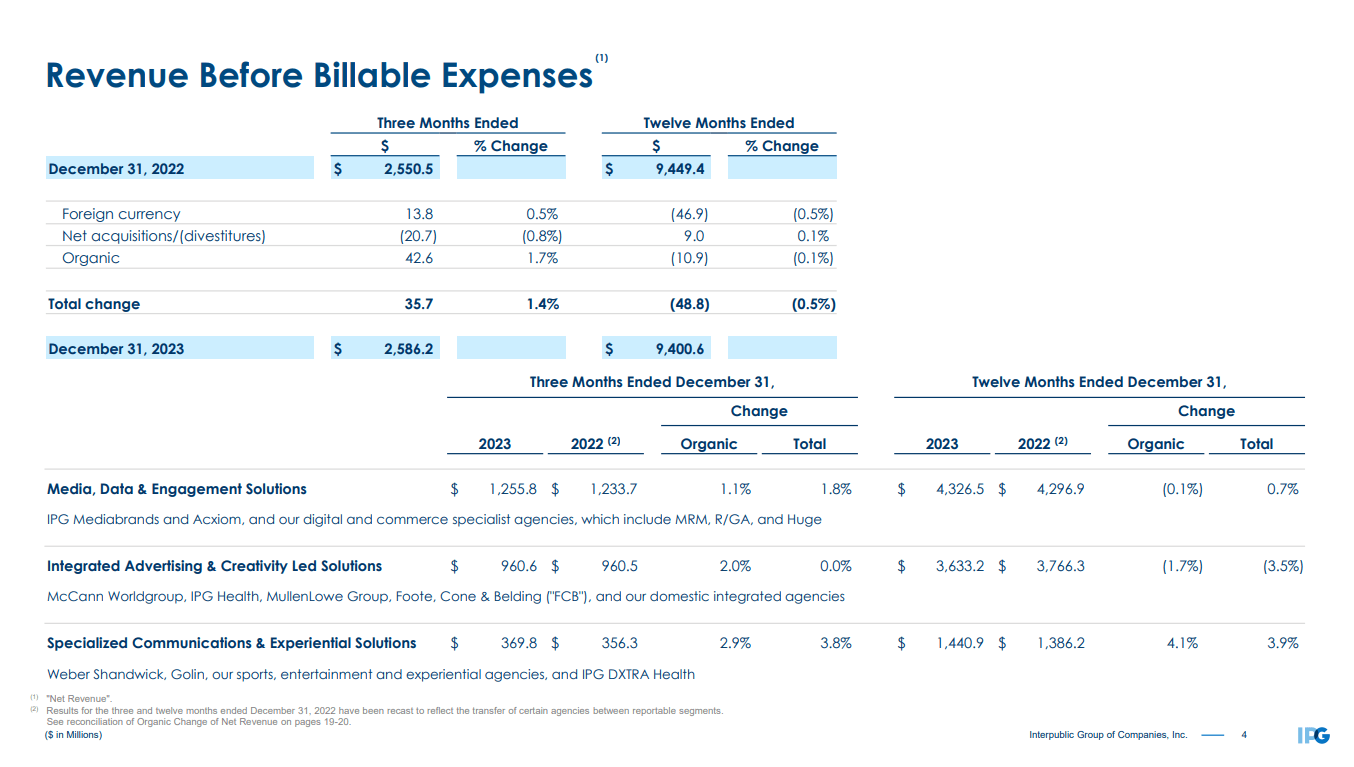

The situation in terms of revenue is quite interesting. Flattish organic performance contrasts to the results of businesses with more APAC exposure, where IPG is mostly exposed to the US. WPP plc (WPP) which has almost 4x the APAC exposure, is seeing more pronounced revenue declines due to more cost conservatism in discretionary parts of corporate budgets in China and the whole region whose fortunes are tied to China. Similarly, guidance is much stronger for IPG compared to WPP where China continues on its downward economic spiral as its systemic real estate issues persist. US saw flattish growth, but wasn't in decline, and smaller segments like Europe and LatAm did very well, with the overall international business growing at 4.3% organically in Q4, and 1.8% for the FY. US declined for the FY. The only parts of APAC that did well, where IPG also has exposure, were India and Australia, Japan and China drove the overall decreases in APAC revenues of 1.5%, which is still better than WPP.

In terms of specific end-markets, the company was dealing with clear organic pressures from tech and telco with around a 3% in effect of overall revenues. This was the main pressure, and it's important to hear from management that these pressures seem to be stabilising.

We're seeing a measure of quarter-to-quarter stability in the tech and telco sector, previously discussed budget reductions at our major technology industry clients have been a consequence of broader enterprise cost-cutting programs within those companies. And while it's still not possible to call the timing with a significant upturn in tech spending and marketing activity, we've noted a more recent stabilization in that spend.

Philippe Krakowsky, CEO of IPG

Healthcare, consumer goods and beverages did well, where healthcare has been an area of investment. Auto and transportation were under slight pressure, but that was after a very strong year and therefore tough comps. They got some major engagements like with Subway and SNICKERS, and a major AOR appointment at Walgreens for healthcare, also repeat business from major customers including Pfizer (PFE), Vertex (VRTX) and Geico.

In terms of operating segments, integrated advertising & creativity grew more in Q4 organically then the media, data & engagement solutions segment, although IA&C struggled more in the FY results. Healthcare helped a lot in IA&C. However, creative within that segment has been generally softer than media, which has been performing generally pretty well and accelerating. Also, IA&C didn't have as tough comps from more limited growth last year. Experiential was doing really well, and things like sport-related businesses and PR were part of the driving of growth in the SC&ES segment. The segments that are doing well are also those that incidentally are seeing more use cases for AI, and are generally growth and investment areas for the business, where AI has a lot of use cases in copy, targeting and in dealing with the substantial data that are used by IPG's digital marketing agencies.

Segments (Q4 Pres)

FWD PEs are around 11x. It's almost perfectly in line with close peer Omnicom (OMC). There isn't a relative case, which is not a surprise considering how closely they compete. The absolute case may be there though. Stabilisation in the weak areas, decent geographic exposures with the US consumer staying resilient, and even some growth opportunities with more productive AI-based offerings can all drive modest growth secularly, consistent with long-term trends. A 11x PE gives almost a 10% earnings yield, which is good paired with reasonable growth expectations. Definitely beats rates. Very solid operational performance is a plus too, with meaningful EBITDA growth despite organic growth slowdowns in 2023. It's not uncompelling, although we take pause just because we don't have an edge here, or see a special angle that might justify a truly below market valuation. These are discretionary markets after all, demonstrated by the pressure in some of the geographic end markets that haven't had the benefit of very solid economic results like the US.